Hello QAVvers

It’s another Tuesday.

The AORD reminds me of Hokusai’s Great Wave Off Kanagawa.

We’re just waiting for that swell on the far right of the image.… BTW, did you know this wood carving, thought in the West to be “so Japanese” is actually a blending of Japanese and European art? And that it represents the threat of dangers coming to Japan from the ocean? It was carved in 1831, just 23 years before the US sailed gunboats into Japan to force the country to trade with them. Commodore Matthew Perry (not the actor from Friends) handed the Japanese a letter from President Millard Fillmore, basically saying, “Hey, open up, or we’ll make you.” Japan, realizing they were technologically outmatched and didn’t want to end up like China (which was being carved up by Western powers), decided to negotiate and signed the Treaty of… Kanagawa. Anyway… that’s enough art history for this morning.

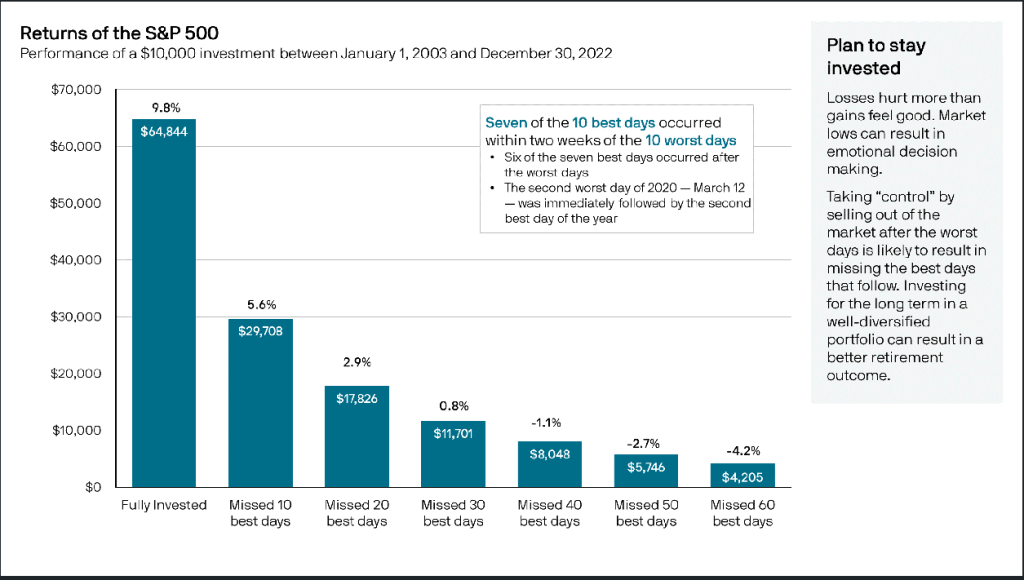

Just a reminder during these dark times at the bottom of the swell why we stay fully invested:

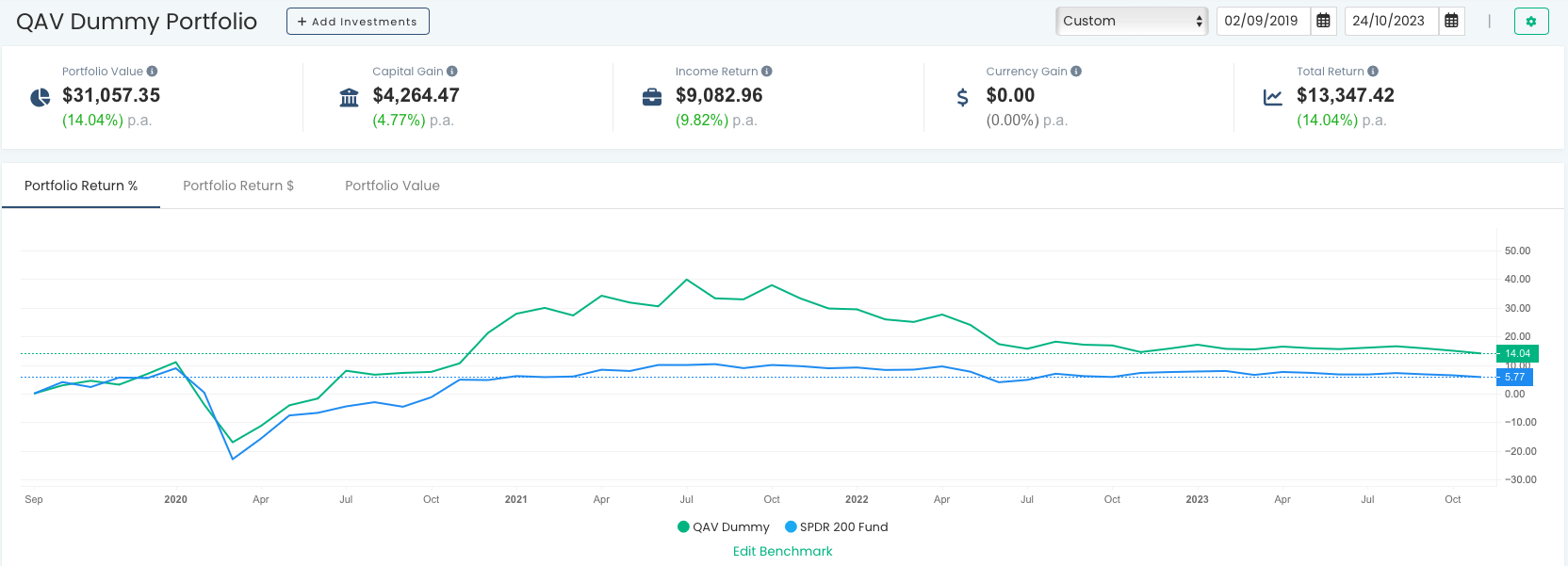

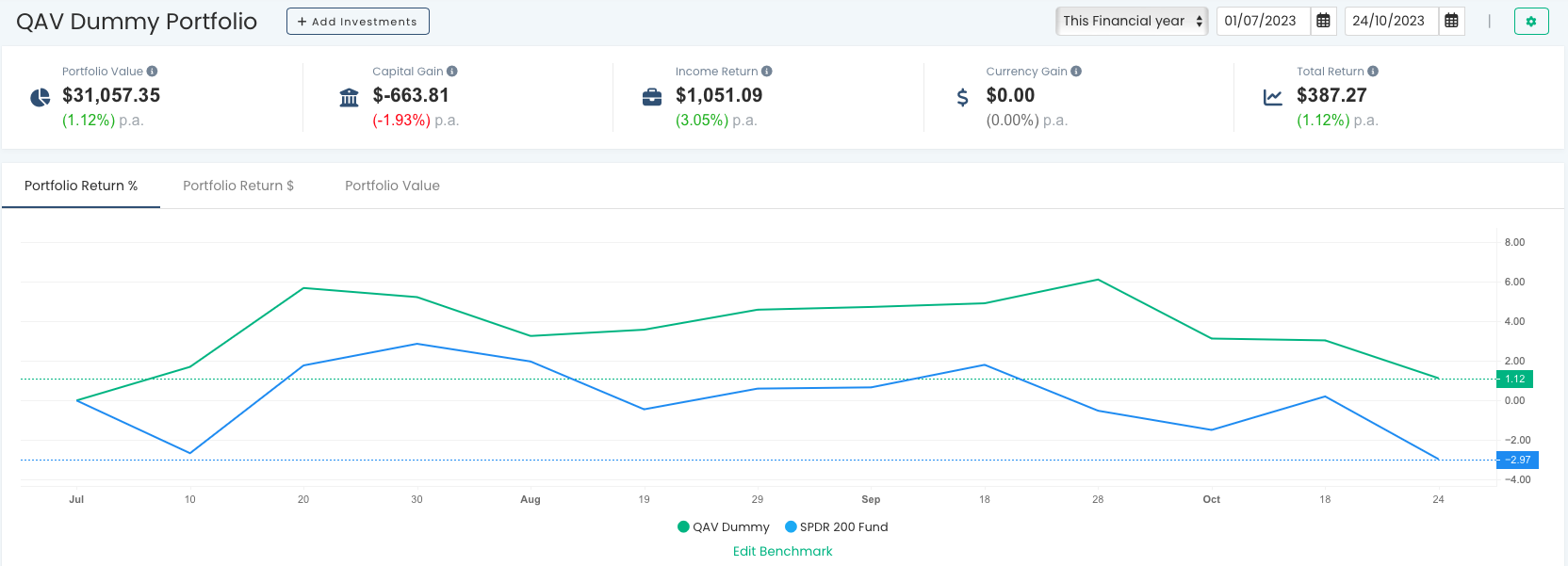

Let’s have a look at the portfolio.

QAV PORTFOLIO REPORT

The Dummy Portfolio is performing well against the benchmark over multiple time frames.

SINCE INCEPTION (02/09/2019)

FY REPORT

RECENT TRADES

In the last 7 days we sold NZM and AMP and bought OML and ANZ.

FREE WEBINAR

I’ll hold another one in a few weeks.

STOCKS OF THE WEEK

During the last week, we traded some stocks in our Light portfolios. Details here.

** As always, please check our work, DYOR, and consult a financial advisor before making any investing decisions.

BUY LIST

Each week we produce a buy list that we share with our members. The intended primary purpose of this buy list is for club members to use as a reference for comparing their own buy list. In theory, all of our buy lists should look pretty similar each week.

As always, please check our work, DYOR, consult a financial advisor before making any investing decisions.

THIS SECTION CONTAINS CONTENT WHICH IS VISIBLE TO QAV CLUB SUBSCRIBERS ONLY.

LAST WEEK’S EPISODE

FREE EDITION:

Also in the Club edition, we’re also talking about: Gold is a buy; PGH 2BL example; Chuck Feeney died; Joe Aston’s final Rear Window; Has TK found a maximum size where a portfolio stops getting ‘QAV like returns’?; Imagine the markets were to theoretically close for 10 years…

Episode Transcription

[00:00:00] Cameron: Everyone recording? Yes, I can

[00:00:01] Cameron: see little red lights. Welcome back to QAV, TK and ak.

[00:00:08] Cameron: It’s the, Kynaston attack with me today. Kynaston’s coming to me in stereo from Sydney. Welcome, Tony. Welcome, Alex.

[00:00:16] Tony: Hey Cam

[00:00:18] Alex: Thank you.

[00:00:18] Cameron: Hey, Tony. Why

[00:00:20] Cameron: you wanna tell everyone why you’re in

[00:00:21] Cameron: Sydney? Alex,

[00:00:22] Cameron: sitting in the room

[00:00:24] Cameron: adjacent to the man himself, you’re TK

[00:00:27] Cameron: adjacent.

[00:00:29] Alex: Yes, I am. Um,

[00:00:31] Alex: well, we tried to be really

[00:00:32] Alex: clever and sit together, and of course that didn’t work. So

[00:00:36] Tony: Our

[00:00:36] Tony: microphones

[00:00:37] Tony: bled into each other’s recording.

[00:00:39] Alex: Yeah. No, I’m up here cause

[00:00:40] Alex: we, um, my partner and I’ve been on a seven week tour of

[00:00:46] Alex: the East coast and we’ve come back down to Sydney. So we’re here with mum and dad for a

[00:00:50] Alex: couple of nights, which is lovely and means that I can be here for the recording in person, kind of together.

[00:00:58] Alex: Slightly separate.[00:01:00]

[00:01:00] Cameron: You’ve been camping around Australia.

[00:01:03] Alex: Yeah. East coast. So up to Cairns, I got up to the Daintree, um, and then back down. Yep. We have a tent on top of a car, which actually works really well. I was saying to dad just before I slept better in that tent than I did when we were actually staying at people’s places. So a bit of adjustment now back in regular beds.

[00:01:23] Cameron: Was it like an air mattress or a real mattress?

[00:01:27] Alex: No, it was like, um, it was like a foam layer.

[00:01:31] Alex: Like two, foam layers that kind of look like an egg carton and then sheets on top.

[00:01:37] Cameron: Oh, right. Ah, comfy. That’s great. What was the highlight of the

[00:01:41] Cameron: trip for you?

[00:01:42] Alex: Um, I’d say K’gari, Fraser Island. That was pretty fantastic.

[00:01:46] Alex: definitely go back there. And then I Sean, my partner did a scuba diving with a board. thing for three days. And I

[00:01:55] Alex: went on a tour to the Daintree and that

[00:01:56] Alex: was pretty fantastic because, we didn’t really see anything all day. We [00:02:00]apparently,

[00:02:00] Alex: apparently had a 90 percent chance of seeing crocodiles.

[00:02:03] Alex: Didn’t see any,

[00:02:05] Alex: but

[00:02:05] Alex: as we’re coming back to cross back

[00:02:07] Alex: over to the South Daintree, there are a bunch of cars that were stopping on the road and

[00:02:11] Alex: the tour driver was like, okay, get out your phone. Something’s obviously

[00:02:14] Alex: coming up. someone

[00:02:16] Alex: spotted a baby cassowary to the left. of the bus. Somehow they’re like brown.

[00:02:21] Alex: So they’re camouflaged. And then we’re like, Oh, the parent’s around somewhere. So we turned around and

[00:02:27] Alex: here’s this like dad cassowary, like three meters from us. It was amazing. He was like, he had probably a 10 percent chance at most of seeing a cassowary.

[00:02:35] Alex: so it was pretty special.

[00:02:38] Cameron: No crocs, but you saw a cassowary. How tall was it They’re like huge, right?

[00:02:43] Alex: I think they they’re usually

[00:02:44] Alex: around six feet ish. So person size, tall

[00:02:47] Alex: person

[00:02:48] Alex: size.

[00:02:49] Cameron: Well, that’s fantastic. I’ve never seen

[00:02:51] Cameron: a cassowary in the, in the, in the natures. fantastic. Yeah, lovely.

[00:02:57] Alex: cool. So it was [00:03:00] like 34 or something, and then we’re going back to Melbourne and it’s about 14. So I’m going back

[00:03:04] Alex: to

[00:03:04] Alex: my natural habitat.

[00:03:07] Cameron: Mine

[00:03:07] Cameron: too. I’m jealous. It’s 30. 2

[00:03:10] Cameron: degrees in my office in Brisbane this afternoon. I didn’t even go upstairs

[00:03:15] Cameron: in the nice aircon, sweltering. Anywho, how are you TK? How was your trip back from Cape

[00:03:22] Tony: Yeah, good,

[00:03:22] Tony: thank you. it’s been wet the whole time. It’s now caught up with me in Sydney and raining today. But yeah, no dramas. It was good. Had a, good trip. Had a couple of days to myself at Cape Schanck, which was lovely and, and then drove back to Melbourne and then back to Wagga and then back to Sydney over the last couple of days.

[00:03:40] Tony: So, good to get out of the car today.

[00:03:45] Cameron: and sit at a desk and do QAV? Well, you couldn’t play

[00:03:48] Cameron: golf

[00:03:48] Tony: Alex and I went down to the gym, so that was good before.

[00:03:51] Cameron: Oh, good. Well, let’s get into it. This is episode 642, we’re recording this on the 17th of October [00:04:00] 2023, and this time it really might be different, Tony. I snuck this one in, it was in my notes to you this morning because I read it after that.

[00:04:08] Cameron: Howard Marks in the Financial Review. Being quoted this morning. Chanticleer, Howard Marks just said the most dangerous words for investors. The Wall Street icon has made one of the biggest calls in his career by predicting those who confuse brains and a bull market might be about to suffer. Sir John Templeton’s famous warning that this time it’s different.

[00:04:32] Cameron: Comprises the most dangerous words an investor can utter because they invariably mean rationalizing valuations that look high relative to history. But Howard Marks, the Wall Street icon and founder of Oaktree Capital, says we often forget that Templeton also said the phrase may actually be true 20 percent of the time.

[00:04:52] Cameron: Which is why Marks feels justified giving his latest memo the provocative title, This Time It Really Might [00:05:00] Be Different. Of course, at this point, I have to play this. It is different every time. It’s always different, Tony. It’s never the same. Thank you, Alan Kohler. Uh, here’s Howard Marks central message.

[00:05:12] Cameron: The decline in interest rates that started around 1980 appears to be over, and markets and economies are starting to transition to a new regime where economic growth may be slower,

[00:05:22] Cameron: profit margins may be lower. Default rates may be higher, asset values might not keep climbing,

[00:05:29] Cameron: money may not be as easy to borrow, and investor psychology may not be as uniformly positive.

[00:05:36] Cameron: The final point is important. Mark says, the vast majority of investors have, quote, with relatively few exceptions, only seen interest rates that were either declining or ultra low or both, end quote. But I’ve also lived in a world where easy money has caused distortions that investors have, in effect, grown accustomed to.

[00:05:56] Cameron: It causes things to be built that otherwise wouldn’t have been built, investments to be [00:06:00] made that otherwise wouldn’t have been made. And risks to be born that otherwise wouldn’t have been accepted. Basically, cut a long story short, what he’s saying is that the last 30 years of investing has been an anomaly with declining and then low interest rates.

[00:06:18] Cameron: And anyone who got good returns over that period think they’re geniuses, but really it was just a bull market and low interest rates. And this time it might really be different. And we could be in a long period now of rising interest rates or at least stable high interest rates and lower asset returns, lower performing shares.

[00:06:41] Cameron: What do you think about that, Tony? And it also could just be Howard Marks trying to get people to read his memo.

[00:06:48] Tony: oh yeah, I’m not a fan of Howard Marks memo, or Howard Marks really, despite the fact that, you know, obviously I acknowledge that he’s been a successful fund manager and investor over a long period of time, but it [00:07:00] wasn’t, it was only a couple of months ago he was telling us, I think it was him, he was saying he was convinced by his son to buy tech stocks again.

[00:07:07] Cameron: No, Bitcoin.

[00:07:08] Tony: Pick or something.

[00:07:09] Cameron: crypto. Yeah. Buy crypto.

[00:07:10] Tony: Yeah. Anyway, but to address his points rather than to address him Yeah, I mean there’s a bit of truth in what he’s saying. We have had a Long term decline in bond rates or bond yields I should say And so there has been tailwinds behind the stock market However, it hasn’t been like a steep straight decline from top left to bottom right.

[00:07:35] Tony: It’s been plenty of interest rate ups and downs along the way. And certainly during my investing time, there has been, um, yeah. So, but perhaps we have had a, um, A sweet spot for equity investments, but along the way there were definitely times when interest rates were high, at least as high as they are now.

[00:07:56] Tony: And, and you know, the market did what it did, it’s doing now. It did [00:08:00] just, and it goes through that horrible cavitation period where there’s some kind of shakeout and difference of opinions, and then eventually it corrects itself and keeps going because The market’s been around for more than the last 30 years, and it’s been going up for more than the last 30 years.

[00:08:15] Tony: So, longer term, it’s been, it’s been going up for the last 100, 150 years. So, you know, it will continue to do so, but it’ll be different sectors. high interest rates will favor some sectors over others. They certainly won’t favor the rocket to the moon. unprofitable, you know, startup companies that are going to be unicorns supposedly, and therefore you pile in with cheap money.

[00:08:42] Tony: and it will favor. More solid quality companies that have been around for a long time and have been through high interest rate cycles before. it’ll probably, I think it’ll probably favor banks, and financial type stocks, may hurt commodities, but again, sometimes the cycles and commodities.

[00:08:59] Tony: [00:09:00] isn’t, isn’t one to one correlation with interest rates. So yeah, so there’ll be swings and roundabouts as there always is. stock market’s not going to close. It’s not going to go broke. it’ll eventually ride itself in this current environment and get on with it.

[00:09:11] Cameron: So business as usual,

[00:09:12] Cameron: you

[00:09:13] Tony: Yeah. Yeah. I mean, there’s a lot of people out there trying to grab headlines and I’m not one of them, but it’s just like, yeah, like it’s, this time isn’t different. If you take a long enough time scale, we’ve been through this before, we’ve been through wars in the Middle East, we’ve been through oil shocks far worse than this, we’ve been through interest rates much, much higher than this,

[00:09:39] Tony: all those things

[00:09:39] Tony: that, you know, the market’s

[00:09:41] Tony: seen before, and yet it still trudges along, going

[00:09:45] Tony: up the hill to a sort of average sort of 9 or 10 percent return over a long period of time.

[00:09:51] Cameron: What were the interest rates like in

[00:09:53] Cameron: Australia in the, early nineties?

[00:09:57] Tony: Early 90s. So that was the… [00:10:00] Recession we had to have. And yeah, I

[00:10:02] Tony: mean, the first mortgage I had on a house had a 15. 75 percent mortgage rate against it. So bond yields were probably around about nine or 10%. And you know, the, the, the interesting thing about the, the. Economic environment when something like that happens is it favors retirees and, and, and people who just want a safe return.

[00:10:23] Tony: They put their money into banks, get paid a decent yield, or they put their money into annuities and get paid a decent rate of return, and they

[00:10:31] Tony: retire happy and safe

[00:10:33] Tony: and pull a caravan around Australia until they fall off the perch and don’t, don’t have to

[00:10:37] Tony: worry about their, their income. So to some extent, that money goes outta the stock market and goes into.

[00:10:43] Tony: You know, bond or bond like,

[00:10:46] Tony: products like annuities. but there’s still a heck of a lot of money left in the stock market.

[00:10:50] Tony: And, you know, again, when that

[00:10:52] Tony: period of adjustment washes through, business gets on with it and the stock market starts to climb again.[00:11:00]

[00:11:00] Cameron: Looking at the All Ords, September 1990 it was around about 1, 400 and 10 years later it was about 3, 200.

[00:11:10] Tony: Right.

[00:11:11] Cameron: at least some of that period we had a high, much, much, much higher interest rates than we have now. The market seemed to handle it okay.

[00:11:18] Tony: Yeah. And that tends to be the case. It’s more, I guess, you know, I’m not, I’m not going to produce any factual evidence for this. My feeling is that it’s the turning points that the market doesn’t like when it goes from easy money to paying a more realistic or average amount for bond yields or borrowings, that it, it’s that kind of turning period in the market, the market becomes manic depressive for a while and then settles down and shakes out, you know, all the companies that can’t afford to pay.

[00:11:49] Tony: And just like it doesn’t reverse when, you know, if interest rates start to decline again, the market will take off. It’ll go through another period of, you know, adjusting to a new environment and [00:12:00] different sectors will have their day in the sun. Yeah, again, obviously with very high interest rates, it’s a tough economic situation.

[00:12:09] Tony: People start to go broke. People can’t,

[00:12:12] Tony: you know, pay their mortgages if they lose their jobs, all that kind of thing. So there’s certainly, I’m not saying it’s sunny days all the time, but as you said, the stock market still went up, over the 10 year period from, from that time on.

[00:12:26] Cameron: Well, and, you know, I guess to be fair, getting back to Howard’s point, interest rates came down a lot over that 10 year period. I’ve got a chart here that says in 1990 they were at about 18%, 17, 18%. Then they dropped early 1992, they were down about… 7.5% and then they went down to about five, back up, down, up, down, up.

[00:12:51] Cameron: Came down sort of after the G F C, um, to around about three, 4%. Went up a bit and then came [00:13:00] all the way down to 2022. So in that period from, so 2012 to 2022, we saw a decline all the way down to zero. But there was a period there definitely from like 2000 up to 2010. Where they, they went up by 50 percent roughly, went from just below five up to seven and a half.

[00:13:21] Cameron: Um, so

[00:13:24] Tony: And yet that was my sweet spot for

[00:13:25] Tony: returns because it was coming out of the GFC. and again, the market was adjusting. There was a, if I remember in about 2012, there was some kind of mini crash in commodities and everyone was throwing their

[00:13:37] Tony: hands up and, like that period between 2010 and 2012, there was just tremendous turmoil, eruptions in the market, and

[00:13:46] Tony: I made heaps of money by just following the process.

[00:13:50] Cameron: actually I was talking about the decade before that from like 2000 to 2008, leading up to the GFC. Really?

[00:13:57] Tony: Same thing though, you know, it was [00:14:00] the tech crash coming out of 2000, then it was the World Trade Center, then it was the second Gulf War, which meant oil prices were going through the roof. It’s very reminiscent of today’s market, where you have People like Dalio and Howard Marks coming out and saying, Oh my God, this is, you know, this time it’s different.

[00:14:22] Tony: We’ve never had this before and that before, and this all happening at the same time, and it’s a crazy place and all this kind of stuff and, you know, grabbing headlines. But again, it was a really profitable time for me to invest. I seem to recall, I started really going in heavy in the market. After the World Trade Center collapsed, um, and in about 2003 2004, the market went into a bull run all the way through until 2007 2008 with the GFC.

[00:14:53] Tony: So,

[00:14:54] Cameron: yeah, I’m looking at it here, the All Ords, August, September 2000 was, [00:15:00] 3200, as I said earlier, 3200, by, end of 2007, it was 6, 779.

[00:15:10] Tony: not much, not much more than that today though, isn’t it?

[00:15:14] Cameron: Yeah, that’s right. It doubled over that eight year period when interest rates were, went up by 50%.

[00:15:22] Tony: Yeah.

[00:15:23] Cameron: So not a lot of correlation, at least in that. So anyway, there you go.

[00:15:28] Cameron: That’s enough of that story. Let’s move on.

[00:15:31] Tony: And that’s what I find with Howard Marks. That’s, that’s kind of how I’ve always approached these, his

[00:15:35] Cameron: not always on the mark.

[00:15:38] Tony: Yeah, it’s, uh, yeah, enough of that update. Move on. That’s probably the best commentary you can have on him.

[00:15:43] Cameron: All right. Market updates. Uh, well, it’s a shit show out there. Let’s just,

[00:15:50] Tony: But this time it’s different.

[00:15:51] Cameron: it. gold is a buy though, we, we agreed off air, which meant that a couple of good companies became a buy for [00:16:00] us this week, WGX and RMS, Large Cap Stocks, so check those out folks if you haven’t already, I have added a bit to my personal portfolio and the live portfolio.

[00:16:12] Cameron: We’ve already held some RMS, but they both went through a quick sort of spike yesterday too. Apparently we’re not the only people who pay attention to the gold three point trend line, I think, because both of those, when they hit our radar yesterday, were already spiking. So get in there while you can, if you want.

[00:16:32] Cameron: Do not take that as financial advice. See your accountant. Talk to a financial advisor first, but check them out. Portfolio update! It’s going well, but, I did sit down this morning to do my weekly report to follow up on the conversation we had last week about large caps versus small caps in the dummy portfolio. I don’t know if you saw my

[00:16:56] Cameron: newsletter that I sent out this morning, you saw that? Did you see, you saw the breakdown? [00:17:00] So if I look at all of the stocks that we’ve held this financial year, And then, divide them up by large caps, and large caps is market cap over a billion, and small caps, I’m just saying anything under a billion.

[00:17:15] Cameron: It does seem that, like, our highest performing stock is SMR, which is a large cap stock, it’s up 45 percent so far this financial year, and I’m only looking at this financial year. But, Overall, the large caps, haven’t performed as well as the small caps. That said, we have twice as many small caps as we have large caps.

[00:17:39] Cameron: So, you know, I don’t know how, I don’t know how to make sense of that, really. I mean, I guess I’m buying small caps because large caps just aren’t on the buy list as often as small caps are. Or, you know, at, at, during the market, volatility, the small caps became buys before large caps did. Possibly because a lot [00:18:00] of them don’t have the same amount of eyeballs or coverage or analysts.

[00:18:03] Cameron: And we pick them up before the rest of the market does. But anyway, for whatever reason,

[00:18:07] Cameron: we bought… More small cap stocks than we have large cap stocks. We’ve held this financial year and they’ve certainly outperformed as far as their portfolio is concerned.

[00:18:17] Tony: And look, that, that makes sense because as you said, like if you look at the ASX, which is ranked by market cap, you know, the ASX 300 is 300 stocks, but you know, stocks over a billion dollars, I’m going to guess and say it’s maybe 30, 40 stocks fit that criteria. I’m not sure what the number is, but it’s going to be a, it’s going to be a lot more small cap stocks that you, you can shop, you know, to find things to buy than there are large cap stocks.

[00:18:44] Tony: So that’s just a factor of. Using a market cap weighting of the ASX, so that’s the first thing. the second thing is that… It’s, you know, makes logical sense that a small cap has potentially a lot higher to go if it takes off than [00:19:00] a large cap stock does. but, but you borrow, but you know, on a risk adjusted basis, it doesn’t say you should put all your money in small caps because they can also go down quite quickly too.

[00:19:11] Tony: They’re just more volatile and large caps tend to be less volatile. And as I said, as well, there are, you know, It does tend to move in cycles where small caps underperform and large caps outperform and then vice versa. So, yeah, it’s, it’s, to me, it’s never been a thematic thing about whether you buy a small cap or a large cap, it’s just, uh, buy the next thing on the buy list.

[00:19:33] Cameron: And obviously people like yourself and those of us that are trading in our super portfolios where we have large ADT, large market cap restrictions, you know, we don’t have the choice. Anyway, you have to buy large cap stocks. So the playing field is limited, but it does explain why I think it was Steven who pointed out in an email to me last week that.

[00:19:54] Cameron: He has a high ADT restriction as well. And that his performance over [00:20:00]the last couple of years has been aligned with yours and my super portfolio, uh, as opposed to the dummy portfolio. And I think his thesis is probably correct that it’s been the small cap stocks that have, uh, helped the dummy portfolio outperform our, uh, Own portfolios.

[00:20:19] Tony: And the benchmark. Yeah.

[00:20:22] Cameron: Yes. Yeah, exactly.

[00:20:24] Tony: I think so. I mean, the only other thing I can think of is that, you know, now QAVs are out there and we’re transparent with when we buy and sell and, um, you know, maybe our members are all buying and selling at the same time. And they’re all, they, the majority of them have an ASX 300 threshold, uh, and we’re stepping on each other’s toes in some way.

[00:20:45] Tony: And maybe people listening in who aren’t even QAV members are also following what we do You know, jamming

[00:20:50] Tony: us,

[00:20:50] Cameron: be a good thing though, if

[00:20:51] Tony: I would have thought,

[00:20:53] Cameron: it would push the price up, not down.

[00:20:56] Tony: well, yeah, that’s what I thought too. I mean, I was thinking about this a lot [00:21:00]lately as one of the, you know, things is that in my thoughts about why have I only performed for the last two years or, you know, it’s been, been while I’ve been doing QAV, um, and If everyone buys at exactly the same time, and then that buying sort of pressure stops, maybe the stock retreats again, and we force the sell, and then we all sell on the same day, and then it rebounds again after a little while after that, so there could be something in it, but I haven’t been able to figure out exactly what, with any sort of factual analysis yet.

[00:21:31] Cameron: Well, that’s a theory. Alright, there you have it people. Don’t buy what Tony’s buying.

[00:21:36] Tony: you be a bit random out there please, people?

[00:21:39] Cameron: Yeah… You’re messing with his returns. Hey, can you um, pull up the bread later for me? I got a technical question to ask him.

[00:21:46] Tony: Go

[00:21:47] Cameron: Bring up… Bring up PGH. I’ve had a couple… like this recently, both in terms of looking at US stocks and, uh, Australian stocks. So you can see on the chart that the [00:22:00] bread letter says that it’s above its second buy line,

[00:22:02] Tony: Yes.

[00:22:04] Cameron: it’s been a Josephine lately.

[00:22:07] Tony: Yeah, it’s just gone above it. It’s above that now. Yep.

[00:22:11] Cameron: just gone above the sell line, but in my mind, it’s still a Josephine because it’s got another little peak there on the right of the second buy line.

[00:22:20] Cameron: So apologies for people listening to this at home, but just trust me. So, so to the right of the second buy line, there’s another little peak and then it drops down again. Now. When I spoke to Brett about this yesterday with respect to another stock, he said, well, it’s because, and if you drew a ruler between the H1 and then that little peak on the right there, it doesn’t cross the line.

[00:22:47] Cameron: It just goes straight through the two peaks and there’s no third point for a three point trend line,

[00:22:55] Tony: Right. Okay. Yep.

[00:22:56] Cameron: Because it just cuts straight through that. So he said the way the [00:23:00] code works is it needs to be able to find that third point where the graph crosses it. Which is why it’s not drawing a second byline there, but I think, to me, that’s still a Josephine.

[00:23:11] Cameron: Now, I could just draw another line through that and say, well, it’s above that line, and therefore it’s good to go. But that’s not a three point line, really, so… I’m left wondering, should I just shut up and listen to the Breda later on this, or, and say, no, it’s not a Josephine, even though it has dropped back a bit from its month end a couple of months ago,

[00:23:35] Cameron: or,

[00:23:36] Tony: looking at the bread later and it’s the current price for PGH is 72 cents. Previous month closes 70. So it’s, I

[00:23:44] Tony: think it’s, it’s not, it’s above its buy line and it’s not a Josephine. I think it’s a buy.

[00:23:49] Cameron: yeah, but you go back a couple of months and it was higher than that. So there’s

[00:23:51] Cameron: a, there’s a little peak there

[00:23:53] Cameron: that’s higher than 73 cents, go back two months.

[00:23:57] Tony: So you’re saying like if it was last month and there was a, it was a [00:24:00]Josephine

[00:24:00] Tony: last month. Yeah.

[00:24:03] Cameron: Well

[00:24:03] Cameron: even, uh, yeah, like it’s

[00:24:06] Cameron: it’s gone up and it’s been retreating,

[00:24:08] Cameron: it’s, and I can’t draw a second byline through that

[00:24:12] Cameron: peak.

[00:24:14] Tony: Yep. So you’re saying the short term trend is down, is what you’re saying?

[00:24:19] Cameron: Yes.

[00:24:20] Tony: Yeah, except it has turned up in the last couple of days it looks like, or this month.

[00:24:25] Cameron: Yeah. It’s peaked up above the month close, but the month close was down on the

[00:24:29] Cameron: previous month close, which was down on the previous month’s close. So I don’t know. I look at that and I go, well, is that positive sentiment or not? Yeah.

[00:24:38] Tony: Well, I think the first thing to say is if you’re not confident and you think it’s not positive sentiment, then don’t buy it. But for me, the way I’m looking at the graph is it could be a falling knife, but the speed at which it’s the graph is descending has stopped and actually turned around kind of. We got a flat bottom back in May when the price was 65 cents and it’s holding [00:25:00] above that.

[00:25:00] Tony: So, um, I understand what you’re saying, but I’m looking at it saying it could also be the start of an uptrend, but you know, there’s no rush to buy. You could wait another month and see what happens.

[00:25:10] Cameron: yeah, well, there’s not a lot to buy at the moment though, so, this, this was at the top of my buy list, and I was like, yeah, I don’t know, yeah, okay, I just wanted to get your thoughts on how to read a chart like that, but at the end of the day, like, I do go by my gut now, if I, if, if, if the chart says it’s a buy, but to me it looks a bit slippery, I’m like, hmm, yeah,

[00:25:34] Cameron: I

[00:25:34] Tony: by your gut now. Your gut,

[00:25:35] Cameron: Yeah, yeah,

[00:25:36] Cameron: yeah,

[00:25:36] Tony: works a lot better than 30 years of investing

[00:25:38] Cameron: Ha ha

[00:25:39] Tony: Okay, good. That’s great. Can we, can we do a podcast with your gut? Hello, welcome to Cam’s gut.

[00:25:45] Cameron: Ha ha ha ha ha ha ha ha ha. Hello! I just watched that Seinfeld episode last night, where his

[00:25:51] Cameron: girlfriend’s stomach makes rumbling noises and he turns it into a little character. La la la! And she gets upset and leaves him.

[00:25:59] Cameron: [00:26:00] Anyhoo. no, it’s just, it’s not the process. It’s, I’m not sure that the, the rules in the chart, uh, accurately telling me that it’s above a second byline or not.

[00:26:12] Tony: Okay. No, that’s fair. I think if you’re unsure, then don’t go. It looks fine to me. I trust the bread later, but, um,

[00:26:20] Tony: yeah.

[00:26:20] Cameron: what you’re saying is if

[00:26:21] Cameron: I don’t know, I should vote no.

[00:26:24] Tony: Oh, don’t start

[00:26:25] Tony: that.

[00:26:26] Cameron: Oh! Ha, ha, ha, ha, ha, ha,

[00:26:28] Tony: oh, oh boy. Thank you for bringing that up again, I thought I

[00:26:31] Cameron: ha, ha, ha, ha, ha. Man, I’ve been, I’ve been just, I don’t know, depressed the last couple of days,

[00:26:38] Tony: Yeah, I’m so ashamed to be Australian.

[00:26:41] Cameron: Me too, I’m embarrassed to be Australian

[00:26:43] Tony: miserable bastards out there.

[00:26:46] Cameron: I can’t, I just, uh, anyway, let’s not get into that.

[00:26:50] Tony: No, Alex and I have already had a half, hour or two of grieving over that one.

[00:26:55] Cameron: yeah. Oh, man, just. Yeah, I don’t know. I’ve got [00:27:00] nothing to say. Chuck Feeney died, Tony.

[00:27:04] Tony: Yeah, I actually didn’t know about him until you sent me the link. I probably would have come across him, but I hadn’t remembered who he was.

[00:27:13] Cameron: Um, the man that Warren Buffett called My Hero died aged 92. And apparently he is the guy that put together the Giving Pledge, by the sounds of it. He was a billionaire. Made his money through investing in cigarettes, sandwiches, liquor,

[00:27:37] Tony: Duty Free Stores,

[00:27:39] Cameron: S. servicemen. Yeah, duty free to U. S. servicemen overseas in the 50s and 60s.

[00:27:45] Cameron: Uh, interestingly, tried to keep his name out of the media. Partially because of all of the tax free benefits he was getting from selling stuff duty free, as I understand it. But! Also decided he was going to give [00:28:00] away all of his wealth. He famously said, I want the last check I ever write to bounce. I’m not sure if that actually happened, but he gave away,

[00:28:09] Tony: That’s your motto too, isn’t it? And the one before that, and the one before

[00:28:15] Cameron: is, I just hope the next check I write doesn’t bounce. I just, uh, um, the, uh, don’t depress, I’m already depressed over the vote. Tony, don’t depress me more. He, uh, he apparently gave away everything, all of his billions, left, kept 2 million for himself and his wife to live on. Um, so not nothing. But, uh, he and his wife lived in a two bedroom apartment in San Francisco, drove an old Volvo.

[00:28:45] Cameron: Traveled economy class and commercial airlines, but gave away 99. 975 percent of his

[00:28:53] Cameron: fortune, according to Mother Jones. He kept about 25

[00:28:57] Cameron: for every 100, 000 he gave away.[00:29:00]

[00:29:01] Tony: that’s impressive. Um, Alex, what do you think about that? Shall I give away all my money?

[00:29:05] Tony: Before you inherit?

[00:29:07] Alex: Well, I’m going to be a super famous artist, so,

[00:29:10] Alex: you

[00:29:10] Alex: know,

[00:29:11] Alex: enjoy your life.

[00:29:12] Tony: I agree.

[00:29:13] Alex: Just putting some positive thinking out

[00:29:15] Cameron: Oh, that’s on record

[00:29:16] Tony: yeah, so as soon as you sell a painting for a million bucks, I can start

[00:29:20] Tony: giving

[00:29:21] Alex: Sure. as soon as

[00:29:22] Alex: you

[00:29:22] Alex: start buying my

[00:29:23] Alex: paintings for a million bucks,

[00:29:24] Alex: you’re going to start

[00:29:24] Alex: giving it away.

[00:29:26] Tony: Right, so I give the, I buy the paintings off you and then you give the money

[00:29:30] Alex: Uh, that’s, yeah, no, not quite.

[00:29:37] Tony: Anyway, yeah, I mean, it’s a great story. If, um, people should look him up. I was actually impressed by the second article you sent me about how he’d given a heap of money to scientific research in Queensland.

[00:29:49] Cameron: Yep, he helped fund the University of Queensland, the Queensland University of Technology, the Institute for Molecular Bioscience, Australian Institute for Bioengineering and [00:30:00] Nanotechnology, the UQ Centre for Clinical Research and the Queensland Brain Institute. He is QUT and

[00:30:09] Tony: smallest Institute? We need a bigger

[00:30:11] Tony: microscope. We need a bigger microscope at the Queensland Brain Institute.

[00:30:15] Cameron: Yeah, well, it’s simple research. They just go, yeah, we couldn’t find any. Let’s move on.

[00:30:20] Tony: Yeah. Dark matter. That’s what we call it.

[00:30:22] Cameron: He was QUT’s and UQ’s greatest individual donor. And there’s a walkway at the university named in his honor. University of Queensland, Feeney Way. I’ve walked down Feeney Way. And, and, uh, didn’t really know anything about him.

[00:30:40] Cameron: So there you go. What a, what a life well lived and, uh, very huge in the generosity. And I know you and your wife, uh, believe in generosity. That’s part of the reason why you do the show.

[00:30:52] Cameron: And your lovely wife wrote a book

[00:30:55] Cameron: that, uh, well, the gist or the gist, the [00:31:00] gist,

[00:31:00] Tony: I can never remember. I think it’s the

[00:31:01] Tony: gist of generosity, isn’t it, Al? Do you

[00:31:03] Alex: Yeah, gist of

[00:31:04] Alex: generosity.

[00:31:05] Tony: It’s always been confusing.

[00:31:06] Alex: The gist of generosity, yep.

[00:31:08] Tony: Yeah, that’s what I thought. I always get confused though.

[00:31:11] Cameron: Yeah,

[00:31:12] Tony: And, and look, and we give, we don’t give away millions to charity, we give away the charity now, and Jenny’s on the board of the Breast Cancer Research Foundation.

[00:31:21] Tony: And just going back to the Feeney bequests to the, or Feeney donations to Queensland Research. You know, for all those knuckle dragging people who voted no out there, who say to me from time to time, ah, scientific research, what’s the, you know, bloody hell, I never used algebra since I studied it at school.

[00:31:41] Tony: Queensland University came up with the vaccine for cervical cancer. So, you know, go home and ask your wife what the benefit there is in donating the scientific research with that little factoid.

[00:31:52] Cameron: People tell you that they don’t like science, what?

[00:31:56] Tony: Yeah, I mean, I’ve had people,

[00:31:57] Cameron: need to hang out with a higher class of

[00:31:58] Cameron: people,

[00:31:59] Tony: I, well, [00:32:00] I do. That’s, that’s true. If you, if you find someone, let me know, but,

[00:32:05] Cameron: Oh! Hey!

[00:32:07] Tony: I mean, the three, except for this present company, I am doing it right now, but that’s once a week, right? But, um, oh yeah, I get all this shit all the time. I know, you know, what did I study maths at school for?

[00:32:18] Tony: I never use it now. Okay, well, give me your phone. Give me your sat nav, give me your car. It’s like… It’s because you don’t happen to use them. Somebody a bit smarter with a bit more gump an application did and you have to thank them for it. Sorry, I’m on my soapbox there. I’ve just had a… Unfortunately, Australia is going the way of the US where it’s just… Dumb people are being manipulated and they’re starting to say the same things as I hear people in the US say, and it’s just so annoying.

[00:32:46] Cameron: it’s late stage capitalism, Tony.

[00:32:48] Tony: Is that what it is?

[00:32:49] Cameron: Yeah. Yeah, I think so. It’s, um, you know, it’s, there’s a lot of money tied up in keeping people dumb and ignorant and saying stupid stuff. [00:33:00] So they vote the way you want them to vote

[00:33:02] Cameron: and they don’t pay attention to the things that you don’t want them to pay attention to.

[00:33:07] Cameron: And the whole QAnon Trump, Trumpy Fox News sort of brain virus that infected the U. S. is infecting people here. And I look, I’ve been saying this for, on my shows for 20 years. My fear has always been that we would go the way of the U. S. And I’ve been

[00:33:25] Tony: And we are,

[00:33:26] Cameron: We are, yeah, sliding down that.

[00:33:29] Tony: when I hear the rubbish coming out of people’s mouths, particularly from one side of politics about the voice, it’s just, yeah, it, we’re, we’re on, we’re already there. It’s unfortunate, but we’re already there.

[00:33:42] Cameron: Anywho, moving right along, Joe Aston, Joe Aston’s farewell column, did you read that?

[00:33:49] Tony: I did. Yeah, it was great. He’s a good writer, isn’t he?

[00:33:53] Cameron: It was delightful. He just took a swing at everyone and anyone.

[00:33:59] Tony: Well, I [00:34:00] was waiting for the paragraph on what the lawyers cost or what the defamation amounts were for settlement and all that kind of stuff, but he didn’t touch on that.

[00:34:10] Cameron: There was some stuff, I mean, apart from the fact that, um, it was just fun and he just took shots at a lot of Australia’s richest people. I liked his analysis and, you know, it sort of reflects Sort of a lot of the stuff that we’ve talked about over the years and we’ve said on the show, um, where he just talks about sort of the, the level of respect that are given to rich, and successful business people in this country that they probably don’t deserve.

[00:34:43] Cameron: Yeah, again, he talks about the stories and the narratives and

[00:34:46] Cameron: that kind of stuff, but I, I like some of this stuff. He says, We all wrap ourselves in soothing stories to dilute our insecurity and feel legitimate and worthwhile in the world. That’s how I recognize the patterns of delusion and corporate egomaniacs [00:35:00] because I’m accustomed to seeing them in myself.

[00:35:03] Cameron: And then he goes on to say, You can analyze their inventions and half truths because the best lies are lies of omission. And you can say, this man is talking pure crap, dear reader. That’s difficult or even impossible to do as a reporter when you’re relying on their voice, not your own, to tell the story. So that’s the first thing.

[00:35:23] Cameron: Like, Stephen Mayne, when he was on our show, when he’s been on my other shows before, talked a lot about that, how Journalists really, by and large, business journalists in particular, just regurgitate what they’re told and they don’t, uh, analyze it or break it down very often. So, at the end of the day, the general public is just getting fed whatever the PR department of the business wants them to be fed.

[00:35:47] Cameron: And he says, these people are often just the highest paid person in the building. I mean, if Twiggy wants to be crazy, at least he’s got his name on the door. The ones who are completely deluded are the ones who’ve just commando crawled to the top [00:36:00] of the steaming pile, and then expect us to adore them.

[00:36:03] Cameron: You haven’t taken any risk, pal. You’ve just lucked in. That’s the other inopportune truth about this caper. Luck plays a huge role in business, though you’d never know it from the heroic self narratives of chief executives. It’s never enough either to be recognized for your commercial acumen. That’s the soulless part of the capitalist endeavor.

[00:36:23] Cameron: You also need to be loved for your charity, patronage, and your highly selective corporate social responsibility. You can’t just be Mr. Profit, you’ve got to be Mr. Altruism, Mr. Community. The desire to be fated is all a part of the rarefied delusion state. Like, I’m not adverse to seeing these guys, uh… Spend money and be altruistic and do good things for the community.

[00:36:45] Cameron: But, uh, yeah, I do agree with him that, uh, there’s a huge amount of luck and survivor bias in a lot of these business narratives.

[00:36:55] Tony: absolutely. And I, you know, openly admit from my experience with corporate, [00:37:00] it’s not the smartest person or the best business person who gets to

[00:37:03] Tony: the top. It’s generally the best networker.

[00:37:06] Tony: And the best sycophant.

[00:37:07] Tony: So, yeah.

[00:37:09] Tony: And, and my, my test for that

[00:37:11] Tony: is, and you can do it yourself, but over the years, I’ve looked at all the people who’ve walked out the door after being

[00:37:17] Tony: a CEO of a top company and they’ve generally walked out with 20, 30, 40

[00:37:22] Tony: million. And you look for their name on the BRW rich list in 10 years time, not there,

[00:37:30] Tony: they don’t know how to allocate capital, they don’t know how to invest, they don’t know what to

[00:37:33] Tony: do with money. And yet they were in

[00:37:35] Tony: charge of, you know, employing a hundred thousand

[00:37:38] Tony: people and pushing. Capital Allocation Around,

[00:37:42] Cameron: What, what do they tend

[00:37:44] Cameron: to do when they retire?

[00:37:47] Tony: Oh, Go On Boards, Go On Junkets, Go Into Thick Packs, uh, A lot of them just fade away. Um, yeah, I couldn’t, it’s, it’s an interesting question, but probably the board route’s the most common. [00:38:00]

[00:38:00] Tony: Um, and you know that, yeah, they may not be motivated to make any more

[00:38:05] Tony: money. So I I give them that, but, uh, you know, they made a lot of money and they’re just going to enjoy it and that’s fine.

[00:38:12] Tony: But, but my point is that they didn’t get to the be CEO of the

[00:38:16] Tony: company because they were good at business. They got there because they

[00:38:18] Tony: were good at manipulating people and networking and. And probably playing Machiavellian

[00:38:24] Tony: games to get to the top. As Joe Astin said it much more succinctly, Commando crawling up the pile of shit.

[00:38:30] Tony: That’s, that’s their core competency. And, uh, and look, you know, um, uh, case in point, and I’m not singling this person out for any particular reason, other than they’re the most recent, um, Have a look at what Alan Joyce does. He’s, um, he’s gonna, you know, picked up 15 million bucks on his way out of Qantas.

[00:38:49] Tony: You may have to hand some of that back, I guess, if there’s a big shareholder backlash, um, at the, uh, you know, in the near future. Um, but yeah. Um, I doubt if we’ll [00:39:00] see his name on the BRW rich list in the future, but yeah, compared to Twiggy Forrest, who, who is, is different. He built the business up from scratch, took all the risks and yeah, he might be a bit

[00:39:10] Tony: crazy, but at least he’s, as Joe Astin said, has his name on the door and he’ll probably stay on the rich list for the rest of his life.

[00:39:18] Tony: Very different, very different people, which is why we like owner founders in the checklist.

[00:39:23] Cameron: Hmm. All right. That’s all I’ve got on my talking list. What have you got?

[00:39:28] Tony: Nothing. I’ve got Alex, she’s here. She’s going to ask some questions. I’ve got a pulled pork.

[00:39:35] Cameron: Lovely. Who are you pulling?

[00:39:39] Tony: Pulling down. Uh, Parenti.

[00:39:43] Cameron: Lovely. Get into it.

[00:39:44] Tony: this, was a request, uh, from last week. I suspect it was a request because Parenti has just finalized an acquisition of a company called DDH1 that was on our buy list. So perhaps it wasn’t implicit, [00:40:00] wasn’t explicit in the question, perhaps it’s implicit.

[00:40:02] Tony: The person who asked it was wanting to know whether they should stick with Parenti now that DDH has been merged into them, rolled into them. Uh, and I’ll go through that. Um, so first thing to notice, to note is that Parenti, so code is PRN, is currently a cell on the bread loader. So it’s a three point trend line cell.

[00:40:24] Tony: So, um, you know, bear that in mind as I go through all this. I’m not… Saying, uh, I’m not recommending it to anyone to buy. I’m, I’m doing this as, uh, uh, because someone asked for it. Uh, so the company, if people don’t know, it’s a large mining contractor and following the, it’s merger on the 6th of October,

[00:40:43] Tony: so just in the last week or so, uh, it’s now the largest mining Services Contractor on the ASX and probably one of the largest ones in the world.

[00:40:55] Tony: The merger with DDH1 was good. Perenti prior to the [00:41:00] merger was basically an underground mine contractor. DDH was a large drilling supplier. So that was, I guess, a part of the business that Parenti didn’t have. So it’s still within the mining services space, but it’s, I guess, diversifying away from just doing underground mine works.

[00:41:20] Tony: I think that’s probably a good thing for them. It seems like a reasonably canny sort of merger of, uh, of two companies. The, it was done by what’s called a scheme of arrangement. So there was never any sort of, uh, fierce takeover battle for this company. Um, scheme of arrangements are often used. In the Australian market, in a nutshell, the acquiring company approaches the target board and says, Hey, um, we’re not prepared to go through an on market sort of duel for the company.

[00:41:49] Tony: Here’s our deal. If you like it, uh, you know, put it to a shareholder vote, we’ll put it to a vote of our shareholders. And then they take it to a judge to, um, give [00:42:00] it a tick and it goes through, um, as a merger under corporations law. So that’s what’s happened in this case. PRN paid 50 million in cash for DDH, but issued 279 million in shares and offered those as part of the payment to DDH1 shareholders.

[00:42:21] Tony: And they had a choice that they could, DDH shareholders could take the cash. Uh, or take the shares or take a component of both up until the 50 million was exhausted. Uh, so it’s, this is a bit of a tricky one because when I get to the numbers, they’re based on the pre merger. So this is DD, this is Parenti prior to DDH I’ll talk about.

[00:42:44] Tony: We won’t know what the numbers look like until December or till February rolls around really when we get December’s numbers, which is the post merger numbers. So just bear that in mind. But a couple of, I guess a couple of points is the. I think [00:43:00] the announcement about the, the offer was made in about July and the shares of PRN have fallen since then.

[00:43:08] Tony: Um, I think they were around about 1. 20 or so in July and they’re now down to about 1. 06. So that, I mean, that could also be because the market’s down, um, in that time and there’s been plenty of things going on in the world, the pressing share prices, but it could also be that the people who have done their due diligence and Put the Proforma balance sheet and Proforma P& L together for the merge entities and worked out that, you know, it’s, um, it’s not a bad deal, but it’s, it’s probably, um, you know, the sum of the parts might be 10 percent worth, worth less than what they were separately, perhaps.

[00:43:43] Tony: Uh, so sentiment’s important in this one, and as I said, this company’s just become a sell. If it did turn up, and it could because the, the Parenti numbers were strong, the DDH numbers were strong. Put them together, they should be. Strong when you combine them, but [00:44:00] I haven’t done that piece of analysis because it would have taken all day to go through the numbers and make assumptions, etc.

[00:44:06] Tony: Uh, but I suspect even though it’s a sell now, it’s just a sell. It’s only, you know, it’s less than 10 percent below its buy line, so it could, you know, in an upturn, see it come back onto the buy list as a merged entity. Um, so just bear that in mind when I’m going through these comments, comments. So a bit, a bit more about Perenti, um, 11, 000 employees, so very large, operates in 30 mines around the world.

[00:44:33] Tony: Uh, plus they now have, since the merger, 100 drilling sites, and we know that, um, miners are always trying to drill for, uh, new ore veins to either extend their current projects or to, to find new ones. Um, but Perenti’s been around for 36 years, so it’s been around for a while. Uh, works… Across Australia, Africa, North America, UK and Europe.

[00:44:56] Tony: So it’s, it’s a pretty large company [00:45:00] in their little sphere.

[00:45:01] Tony: Even though the companies, the parent companies are called Parenti and until recently DDH, uh, people might know some of the brand names which have been absorbed into these two over the years. So companies like Barminco, SWIC, and Oztrail. I think they were all listed on the ASX at some stage. And I think SWIC and Oztrail, in the time we’ve been doing QAV, have been on the buy list.

[00:45:27] Tony: Um, so they, they might be known to us. Uh, some of our listeners. Uh, the other point I wanted to call out about, uh, Perenti is that, uh, as soon as they merged, they announced a buyback program and they hadn’t been buying back shares in financial year 22. So this may just be a continuance of that. However, it’s interesting that they’re, they’ve issued new shares and now they’re buying them back.

[00:45:52] Tony: So it could be like a nice tricky way to. Reduce the purchase price of DDH. [00:46:00]If they issued shares, the share prices dropped back 10 percent and they’re going to buy them back. It’s a, it’s a nice way of getting a bit of a discount on the original sticker price that they offered for the company. Uh, but I think what’s also driving it is this company doesn’t pay a dividend.

[00:46:19] Tony: And I suspect the reason why it doesn’t pay a dividend is because it. Doesn’t have any or many franking credits because a lot of its income is coming from overseas from Africa and from the US and from Europe and you only get franking credits for tax paid in Australia, so

[00:46:35] Tony: I suspect that they’re seeing buybacks as a different way of distributing excess cash to the benefit of shareholders, but that started up within a week of the deal being done, so I thought that was interesting.

[00:46:49] Tony: Thank you. The other interesting thing I found out was that the company sold 150 million of non core business and assets just prior to announcing its offer for [00:47:00] DDH. Uh, and if you recall, they offered 50 million plus issuing new shares. So they do seem to be a board that’s pretty savvy at capital allocation and capital management.

[00:47:11] Tony: So I think that’s probably a tick, um, to them. And, uh, the, uh, Managing their capital well, um, low debt, uh, huge amounts of cash. I think there’s about 300 million of cash sitting on the balance sheet as of the 30th of June. They’ve obviously spent some to acquire this company, but, but not all of it. So that’s a good sign, um, to go through the numbers and some of the other numbers on this company.

[00:47:38] Tony: Uh, it’s a, it’s a reasonably large company. It has an ADT of just over 2 million per day. So it’s. Very liquid. I’m doing my numbers on a price of 1. 045, so

[00:47:51] Tony: 1. 045 per share, which is less than the consensus target, which is good. I’ve just noticed Stock Doctor’s gone back to giving us a [00:48:00] forecast value for a while, that’s stopped, but the forecast value on Stock Doctor is 1. 375, so the company’s Um, well below that price and the fact that they’re buying back their shares suggests that the company thinks they’re undervalued as well.

[00:48:14] Tony: Uh, Stock Doctor financial health is strong and steady. Uh, there’s no owner founder, so, uh, we can’t give it a tick for that. Sometimes there is with these companies, but I suspect that they’ve been, uh, you know, part of the little companies that have been bought up as this company has evolved. But no owner founder on the board.

[00:48:34] Tony: Um, the PE is 8. 26, which is not the highest or the lowest, although it’s reasonably low at the moment, but we don’t score it. Interestingly enough, again, prior to the merger, uh, PropCaf is only 1. 6 times, which is Really, really cheap. And I guess that’s a testament to the cash the company’s throwing off. So that’s, um, that’s something that’s in its favor.

[00:48:57] Tony: And I would think with a low prop CAF like that, [00:49:00] even with the acquisition, it’s probably still going to be on the buy list once December numbers come out. But I guess that’s a prediction and I’ll wait and see.

[00:49:08] Tony: The share price of 1. 45 is greater than IV1 but less than IV2, so it gets a score for that. IV2 for this company is 1. 86, largely driven by forecast increase in earnings per

[00:49:21] Tony: share. I wasn’t able to… Tell whether the forecast was based on the merger or whether this was kind of a pre merger forecast. I suspect it takes into account, um, the merger because, uh, consultants are forecasting that the earnings per share should increase by nearly 50%, which, uh, on a growth over PE basis gives us a 5.

[00:49:45] Tony: 89 times number, which is way above our hurdle of 1. 5, so it scores well for that. Again, on the valuation metrics, and this is pre merger, the net equity per share for this company is 2. 34. Current share price is around 1. [00:50:00] 05, so it’s trading at less than half its book value, which is amazing. We hardly ever see something that deeply discounted to assets.

[00:50:08] Tony: There is a bit of a difference between net equity per share and net… tangible assets of about 20%, but even if you use net tangible assets, you’re still buying it really cheaply, um, compared to what you, um, compared to what the equity and asset value is that’s available. I think the difference is probably going to be goodwill because, uh, the company has grown by acquiring other companies and, and, um, as we know, the difference between You know, the book value of an acquired company or the asset value of an acquired company and what they pay for it gets put onto the, um, the balance sheet as goodwill.

[00:50:44] Tony: So I think that’s what’s happened here. Um, without going into heaps of detail on that, that could be a good thing or a bad thing, but it’s only about 20 percent different. So it’s not going to be, um, material to the conversation about how cheap this company is, given you, you’re buying it at, um, [00:51:00] half its book value and maybe 80 percent if you use net tangible assets.

[00:51:05] Tony: Uh, In terms of the manually entered data, it doesn’t have consistent, consistently increasing equity, but it is close. I think it… Um, the, the year where it didn’t consistently grow its equity was probably pandemic related, but it’s certainly back on track to, to, to do it now, so that may change in about, um, over the next couple of halves and in 12 months or so.

[00:51:28] Tony: Uh, all up the quality score for this company is 9 over 16, which is only 56%. So that’s, that’s, uh, something to watch out for. It’s not, not, um, it’s kind of medium. It’s not overly high, not overly low, but it’s not, not, it’s not great. Uh, and the QAV score overall is 0. 35, which is very high, um, we don’t have it on our buy list because it is a 3 point trendline sell, but if it wasn’t, it would come out pretty high up on the buy list and be a high ADT stock up there, [00:52:00] so I haven’t gone through and done the pro formas, um, on the merged entity, but I suspect, because this is a large ADT stock, there are analysts out there who are watching it closely, and we’ll see, you know, their numbers reflected in the sentiment, um, in the share price for this company.

[00:52:17] Tony: I wouldn’t be surprised at all if it… Gets an upturn as, as people do crunch numbers and, um, and I guess more information flows through from the company, perhaps at the quarterly reporting time or the AGM. And, uh, we see this come back onto the buy list. Um, summary and pros and cons. So, pre acquisition, the numbers were really good.

[00:52:40] Tony: All the metrics were up in terms of sales and profit and cash flow. Uh, so that, I think that was all good.

[00:52:46] Tony: Again, I made a note here to watch for December numbers. So I think that’s, um, when we get to see the

[00:52:51] Tony: first sort of set of results with merged numbers. Uh, I guess the question someone might be asking if they had a DDH [00:53:00] and didn’t take the cash offer is,

[00:53:02] Tony: should they, what should they do now? Stay as a DDH

[00:53:05] Tony: shareholder or sell?

[00:53:07] Tony: I guess if it was me, I’d probably sell

[00:53:09] Tony: now because it has become a three point trend sell. Uh, and I say that, you know, Fully knowing that it could become a buy again, because it’s not too far below its buy line. But yeah, I would sell until we get some clarity on those numbers. Uh, having said that, the, even though the share price is a bit lower than it was when the merger went through, the buy price is dropping each month as well, so next, you know, even if the share price didn’t move from here, it wouldn’t be a stretch of the imagination to see the, it cross the buy price in the next sort of six months.

[00:53:41] Tony: So, one to watch for sentiment. Um, pros and cons, uh… It’s, um, I, I think that the, the d the PTI board showing themselves to be good capital allocators, the company has very good, very strong cash flow. D D H did as well. It was on our, on our bio [00:54:00] list site. I can’t see that changing too much in the future. Uh, a big pro for is it’s, it’s trading on very low prop calf numbers.

[00:54:08] Tony: Uh, and, but it does have a, uh, a low quality score. And, um, interestingly enough, the slogan for this company is Expect More. And that’s kind of how I thought might be a good tagline for this is that I would expect more and better quality score results from a company, um, which appears to be this cheap and well managed.

[00:54:29] Tony: Uh, Expect More was kind of a comment I used to get sometimes on my report cards at school. So when I slacked off, so, um, Uh, that’s the positives for the company. The negatives, um, I remember doing a deep dive on DDH and that company, which will become a big part of the merge company, um, is really all about drill rig utilization, and I do recall going back, uh, in commodity downturns in the past that Drilling companies can get stranded holding onto [00:55:00] assets which just aren’t being utilized and then they become unprofitable.

[00:55:03] Tony: Now, um, I’m not sure if DDH has leased their drill rigs and they can return them in that situation, or whether they own them and they’re paid off or whatever, but that is a risk with this kind of company. If there is a global downturn and mining activity comes off, that’ll hurt them. Uh… I guess, um, it’s probably belongs in the positive camp, but it

[00:55:27] Tony: could be a risk. Uh, their earnings are boosted by the low Australian dollar because a lot of their earnings come from overseas. And so when the Australian dollar is low, they get translated back into the local currency with a bit of a bit of a margin boost that’ll go away if the Australian dollar starts to rise, but at the moment it’s a good.

[00:55:46] Tony: Tailwind for the company. Um, but it’s, again, it’s one to watch. And, um, I guess the other issue for them is they don’t, they aren’t getting a hold of many franking credits. They did say they will review their dividend policy going forward. [00:56:00] Um, so the buyback might change into being, uh, a payment, a dividend payment if they get enough ranking credits, uh, which they might get from DDH, which has a large presence in Australia.

[00:56:10] Tony: So yeah, interesting company to go through. Thanks for the question, um, requesting it. Uh, Let’s watch the space and see, first of all, what Sentiment does over six months, and then secondly in February when we get December numbers, what the Merchant Entity looks like.

[00:56:26] Cameron: Yeah. I remember when its results came out, when they had like record results at the end of the last financial year and the share price crashed by 12 percent or something, and.

[00:56:37] Cameron: We’re all like, what the hell? One of our Light members is actually, uh, works at PRN and, uh, remember he sent me an email at the time saying, quick feedback from the CEO, market didn’t like lack of a dividend, given consideration of a dividend was previously stated when leverage was under one. But with refinancing due next year, they wanted to keep some [00:57:00] buffer, plus allocation of future funds slash investments to electrification, risk management, and mining technology, which have a number of years payback rather than shorter term returns to shareholders.

[00:57:11] Cameron: Loss of first U. S. tender and big local tender weren’t seen as large negatives. And I asked him if he wanted to try and get the CEO to come on the show. He said he’d work on that for us.

[00:57:23] Tony: Okay. It’ll be interesting to get him on. Or her. Um, but it could also have been, I think the announcement of the merger was, um, raised soon after their results. So that could have also played into that mix. Large share issuance coming up.

[00:57:39] Cameron: Yeah. Good stuff. Alright,

[00:57:43] Cameron: well, time for questions. Alex, are you going to channel the other

[00:57:49] Cameron: Alex? What are you going to do for us today?

[00:57:52] Alex: I feel like I’ve been really over

[00:57:53] Alex: representing the Alex’s recently, so I’m going to do

[00:57:55] Alex: Charles’s.

[00:57:56] Cameron: You are right?

[00:57:58] Cameron: Oh, you’re going to start with the [00:58:00] Charles, okay.

[00:58:00] Alex: Um, so Charles

[00:58:01] Alex: says, I have a cheeky question for you guys. Imagine the markets were to theoretically close for

[00:58:07] Alex: 10 years and you had to fully invest and buy 10 businesses on the ASX this week. Please list the top 10 you would commit to. Note this

[00:58:15] Alex: game does not allow more than two LICs

[00:58:18] Alex: two ETFs and, two

[00:58:19] Alex: banks.

[00:58:20] Alex: Good luck.

[00:58:21] Tony: Hmm. Yeah, I don’t think I have, I don’t have 10 because I only sort of did this this morning and it’s cracking my brain. Uh, I probably would start with the LICs first of all, and, and definitely put Australian Foundation investments in there. Um, Probably Washington Sol Pattinson’s, I think they’re well managed and, uh, perhaps Argo, which is another big one on the ASX.

[00:58:48] Tony: If people want to know my views on Licks, I can go back to some of the shows at the beginning. They’re a good way to start investing, I think, and the AFI has been around as long as the share market. It’s very well run, yet [00:59:00] market like returns and good dividends. So, um, that would be very close to the top of my list.

[00:59:05] Tony: In terms of other comments about this game, uh, I wouldn’t be buying mining company stocks, so that takes a lot of, a

[00:59:15] Tony: lot of companies straight off the table. I did think about FMG, Fortescue Metals Group. Um, I don’t know what that company is going to look like in 10 years time. It may be a green hydrogen company or it might be, um, an iron ore company or a bit of both.

[00:59:28] Tony: I’m not sure, which, um, was the reason I’m not going to nominate it. Uh, but just generally, I probably wouldn’t want to go into a commodity company for 10 years. Blindly and not being able to trade it. I think the commodity cycles,

[00:59:43] Tony: you know, are probably shorter than 10 year ones, so.

[00:59:46] Tony: Um, there is oftentimes a long term

[00:59:49] Tony: commodity cycle, which is much longer than 10 years, and to put that into perspective, when I first started working Uh, back in the mid 80s, um, I did see a graph of the [01:00:00] ASX and I think it was, the biggest sector was mining.

[01:00:03] Tony: And then, um, about 20 years later, the biggest sector was finance and mining had shrunk and now we’re back to both being dominated by financials and mining. So there are some big swings over long periods of time, but I wouldn’t feel company comfortable now suggesting a mining stock to be held for 10 years.

[01:00:22] Tony: Um, so my nominations are number one, Credit Corp. I’ve always liked Credit Corp, and I kind of like my thinking behind this game is what are the companies I’ve owned over long periods of time? They’ve kind of always been on the buy list, and I’ve had them in my portfolio. I do trade in and out of them, but they’ve been around for a long time, and the first one’s Credit Corp.

[01:00:43] Tony: But I say that knowing that it’s a, it just turned into a sell today. So it’s not, it’s either a great time to buy, um, but it’s, it’s not one that I’ll be holding for much longer. Um. Barl, I think it’s a great, well run company in a niche [01:01:00] sector in the market and I think it will do well longer term. And I wouldn’t at all be worried under its current management to put it aside for 10 years.

[01:01:08] Tony: Next, next cab off the rank is Macquarie Group. Um, I’ve always admired, you know, the, the plucky, Bank that’s taken on the global big plays in investment banking. They do a great job, um, and the culture’s great and their risk management’s great. The famous loose tight risk management, um, structure where you can basically do what you like as long as, as long as it’s within their broader risk management parameters.

[01:01:35] Tony: So it does tend to foster entrepreneurship, entrepreneurship in a large company, which is the best of both worlds. I think I’ve got the benefit of the balance sheet. And they’ve got an entrepreneurial approach to growth. So MQG is on my list. And the third one is JB Hi Fi, which again is another company I’ve admired for a long time.

[01:01:57] Tony: And it’s been on and off our buy list and I’ve owned it [01:02:00] at different times over the years. I think they dominate their category, very low margin retailer dominating that sort of electrical category. It’s, it’s my go to shop if I need to buy something. You know, like podcast microphones or a new laptop or whatever.

[01:02:16] Tony: Um, yeah, so very well run. And, uh, it’s, it’s, it’s got a moat to use Buffett’s terms. I think that were the three I came up with. Um, there are other possibles which I’d put on the list, but they’re not. Buys at the moment. So they tend, the problem with this game is you’re looking for a quality company. First of all, you’ve got to have a company that’s going to survive 10 years.

[01:02:37] Tony: It’s going to be around, um, and probably still be listed. Uh, so you’re looking at companies which are quality, uh, and you’re still trying to find something which you can grow or is a, is a decent buy now. So my next company would be ARB. Uh, which is the manufacturer of four wheel drive accessories. Um, I’ve followed their story.

[01:02:59] Tony: Um, it’s pretty [01:03:00] much paralleled my investment investing career and I have owned them in the past, but because they are such a well run company with great metrics, uh, they, they, their price is up. So I’m not the only person who thinks they’re a good company in other words. And, and they’re usually trading at the expensive end of valuation ranges.

[01:03:17] Tony: I haven’t looked at them recently, but they probably still are there. They haven’t been on the buy list for a very, very long time. Um, but certainly a quality company, which I think is well run and will be around for 10 years and, uh, and we’ll have some growth prospects. And I’m going to nominate one more, uh, Nick Scali, NCK.

[01:03:34] Tony: Um, again, uh, being around for my investing. Lifetime, oh, maybe a bit shorter than that, I think it was in the 1990s time period, um, but yeah, well run, owner founder, uh, it’s, it’s, sticks to its knitting, it’s got the drop ship model down pat when it comes to Furniture retailing. So you want to buy a sofa, you can get a quality sofa [01:04:00] cheaply, but you have to wait for 12 weeks before they go back to China and manufacture it and then have it delivered to you.

[01:04:06] Tony: So that’s a great model. It’s a niche model and they’ve made, um, you know, good returns for shareholders along the way. So they’re my five plus a couple of licks. I couldn’t get to 10, um, in thinking. The other point I wanted to make was I did some quick calculations. I thought, okay, that’s my. 10 year holds.

[01:04:25] Tony: How have they done over the last 10 years? And this is why this game is so tough. Credit Corp has gone up about 170 percent over that 10 year period, but that’s only 5. 4 percent CAGR over 10 years. Macquarie Group over the last 10 years is up 13 percent CAGR. JB Hi Fi is up 7. 9%. So I think the average of those three is about 8.

[01:04:52] Tony: 7%, which is probably about the index, um, performance, which kind of swings me back to buying [01:05:00] Australian Foundation Investments again, uh, to find something which is going to be around for 10 years. and outperform the market is, I think, pretty hard to do. And it’s certainly been my experience. And one of the reasons why I’m not a buy and hold value investor is so many value investors are.

[01:05:20] Tony: I think everything goes in cycles, including valuation. And it’s a hard game to play. If it was an easy game to play, I’d buy my 10 stocks and then come back in 10 years time and rub my hands together. But that’s not the way this tends to work out.

[01:05:35] Cameron: Hmm. Well, for me, I’d just buy Alex’s paintings, because that’s the best bet,

[01:05:45] Tony: Yeah, well that, she’s got a, she’s got a, um, three month wait, so the model on that one too is three year wait, some of those.

[01:05:53] Alex: Yep. Dropshipping from China.

[01:05:55] Tony: Yeah.

[01:05:56] Cameron: Ha ha

[01:05:57] Tony: You’re like the Simpsons, you outsource all the cartooning to Korea

[01:05:59] Tony: [01:06:00] and they come back

[01:06:01] Cameron: ha ha ha.

[01:06:02] Tony: with the finished product.

[01:06:03] Cameron: I think, like, the next 10 years is going to be interesting, um, not every business is going to be dramatically affected by artificial intelligence, but a lot of them will be, and a lot of the economy will be.

[01:06:15] Cameron: I think this is going to be a really dramatic 10 years. I’ve spent the last, uh, week, Uh, deep diving interviews with Ilya Sutskever, the chief scientist at OpenAI.

[01:06:30] Cameron: And just listening to him sort of project where they’re going from here and what he thinks is going to happen. And, you know, he’s expecting, they’ve got a lot of runway yet to, with the current model of large language models before they have to move to a different. model for artificial intelligence. But, um, yeah, I think it’s going to be a really dramatic decade.

[01:06:55] Tony: Yeah, it probably will be. And who knows what’s going to develop between now and then and, you [01:07:00] know, be the next big boom thing. I don’t, we, we won’t know. in advance what that’s going to be. Yeah, I mean, I get your point about AI and it will change things dramatically, but so did the internet and other, you know, the locomotive and the car and all those.

[01:07:16] Tony: And, uh, the way it tends to play out, in my experience in Australia at least, is that The large companies roll with it and, you know, absorb AI and change their business practices, but there’s still large companies at the end of it. Um, and I, I did consider putting companies like, you know, ComBank and Coles and Woolies, um, on this list of 10 stocks, but I think they’re probably just going to get index returns as well over that time period.

[01:07:44] Tony: But I would be fairly certain that they’d be around, um, in 10 years time, which I think is the first hurdle. To assure yourself off when you’re playing this game. Second hurdle

[01:07:55] Cameron: big. It’s all going to be Bitcoin, Tony.

[01:07:57] Tony: yeah, we, would you buy Bitcoin now and then come back in [01:08:00] 10 years time and see how you went?

[01:08:02] Cameron: No, I would not.

[01:08:04] Tony: but Bitcoin was going to change business.

[01:08:06] Tony: I mean, you know, I’ve listened to endless podcasts of, uh, what’s that guy? Cuban, Mark Cuban. And, um, all those guys from the States saying, Oh yeah, Ethereum is going to, you know, blockchain the world and forget about central banks and banking in general. It’s all going to crumble. It’s like, okay, are still here.

[01:08:26] Cameron: we’ll see. Anyway, good question, Charles. Thank you for that. Uh, okay. So I’m going to read Alex’s question.

[01:08:33] Tony: These are left over

[01:08:33] Cameron: from last week’s Alex Franklin’s questions, left over, TK has mentioned learning about three PTLs from a book or publication. Can he please share the name of that resource? He’s shaking his

[01:08:44] Cameron: head.

[01:08:45] Tony: I’m really embarrassed. I still, I still can’t recall what it was called. And it was, um, I mean, the story of it was this would have been after the GFC when I was casting around, trying to find a good way to put some kind of, um, [01:09:00] sentiment into my investing, which was largely value based, but buy and hold.

[01:09:04] Tony: Prior to the GFC, uh, and it was an ebook. It was like a six page PDF and I think I paid about 20 bucks or 30 bucks for it. Um, it just was like one of those, uh, pop up ads on Yahoo Finance or something as I was on the internet back in those days. Um, and, uh, you know, read their presentation and bought their product and then they disappeared.

[01:09:29] Tony: So, um, and the PDF is. Sitting on an old Microsoft XT or I B M XT in a landfill somewhere, from the,

[01:09:39] Cameron: I asked ChatGPT

[01:09:41] Tony: from the early.com era? Actually, no, it wouldn’t have been, it would’ve been from the about, yeah. 15 years ago probably. Yeah. So, uh, I’m sorry Alex, I can’t point you towards it. I’d love to go back to it. Um, ’cause it laid it all out really well.

[01:09:57] Tony: Um, made, made some good points about not getting [01:10:00] too carried up in the. Uh, away with the rules and, and keeping some sort of common sense approaches to it. And, uh, and I do recall their claim was that they were getting, that their returns were about 15 percent per annum, um, just using the three point trend line.

[01:10:16] Tony: So, um, that’s what, one of the things that attracted me to research it. And, uh, but I adopted it as, as we know, as my way of, of using sentiment rather than going into, um, moving averages and all the other, many other ways you can. Do technical analysis, which I also looked into and never really appealed, A, because they were super complex and B, because they always had more exceptions than they had rules.

[01:10:43] Tony: And I kept tying myself up in the nuts trying to use them. So, um, yeah. Sorry, I can’t help you, Alex.