Hello QAVvers

It’s another Tuesday.

The AORD has had a down week.

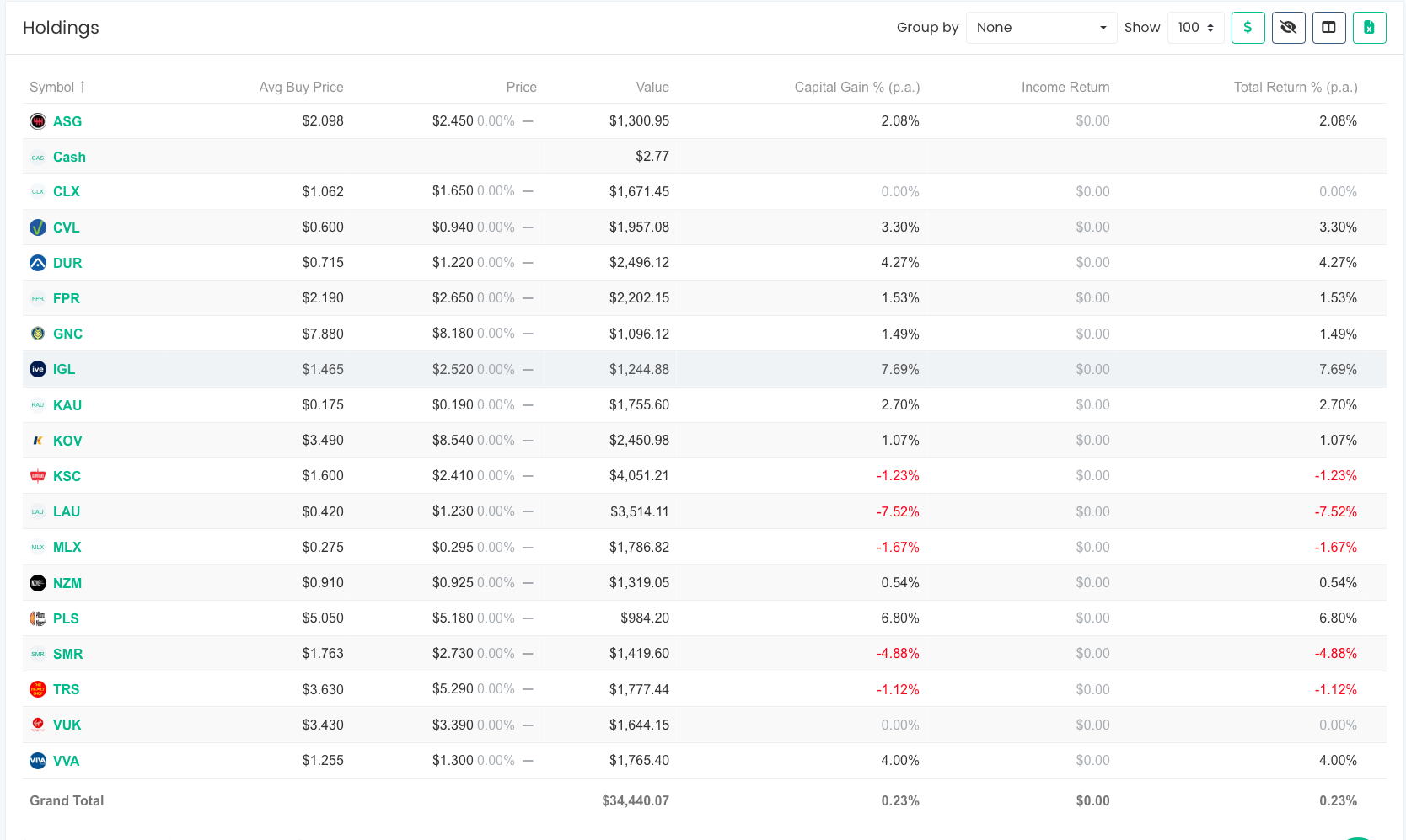

Let’s have a look at the portfolio.

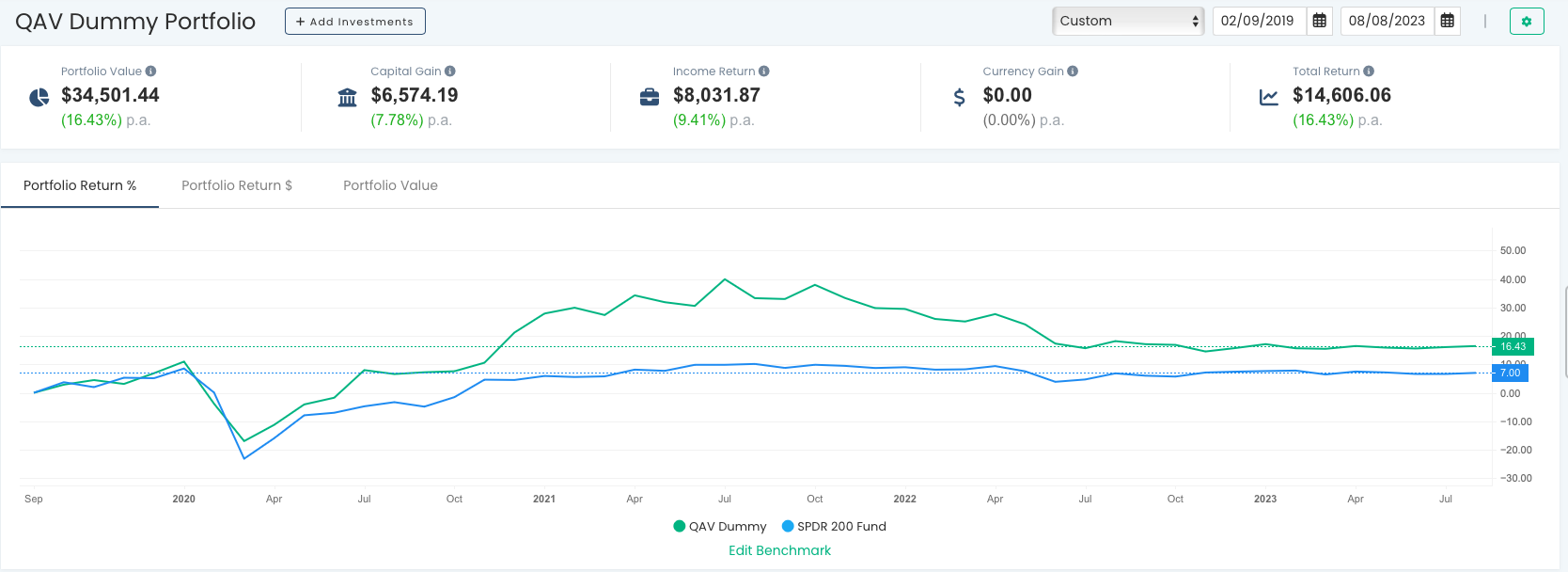

QAV PORTFOLIO REPORT

INCEPTION REPORT

We’re still outperforming the STW by ~2.5 times since inception (02/09/2019).

You can always check out the live version of the portfolio chart here.

Here are how the stocks have performed in the last 7 days.

RECENT TRADES

No trades in the last week.

STOCKS OF THE WEEK

During the last week, we also traded some stocks in our Light portfolios. Details here.

** As always, please check our work, DYOR, and consult a financial advisor before making any investing decisions.

BUY LIST

Each week we produce a buy list that we share with our members. The intended primary purpose of this buy list is for club members to use as a reference for comparing their own buy list. In theory, all of our buy lists should look pretty similar each week.

THIS SECTION CONTAINS CONTENT WHICH IS VISIBLE TO QAV CLUB SUBSCRIBERS ONLY.

LAST WEEK’S EPISODE

THIS SECTION CONTAINS CONTENT WHICH IS VISIBLE TO QAV CLUB SUBSCRIBERS ONLY.

Detailed highlights of the episode:

THIS SECTION CONTAINS CONTENT WHICH IS VISIBLE TO QAV CLUB SUBSCRIBERS ONLY.

Episode Transcription

Cameron 00:09

Welcome back to QAV, Tony. This is episode 631. We’re recording this on the first of August. You’re in the great metropolis of Wagga Wagga again this week.

Tony 00:23

I am, yes. The great metropolis. The overcast, cold metropolis of Wagga Wagga.

Cameron 00:23

How’s the Gulf in Wagga Wagga this week?

Tony 00:31

Don’t know yet. We’re playing tomorrow and Thursday, I arrived here last night.

Cameron 00:35

All right. Where else? What else is news, TK, before we get into stuff? Anything else you want to report?

Tony 00:40

In my life or in the stock market?

Cameron 00:42

Yeah, in your life? What’s going on?

Tony 00:45

I’ll save it for after-hours, but I’ve been down at Cape Schanck. I spent some time with Alex, which was nice. Lovely. She’s busy painting for her first Affordable Art Show.

Cameron 00:56

Cool.

Tony 00:58

Went to the MCG a couple of times to watch football, which was good fun. Caught up with some friends.

Cameron 01:04

Did you get a new Starlink?

Tony 01:06

I think it’s been delivered to Sydney. I’ll take it down there next time.

Cameron 01:11

I read a report the other day. Did you know that Elon Musk, since 2019, has been sending a rocket into space every week with a dozen or so satellites on it. He now has over four-and-a-half-thousand satellites in space, which is more than 50% of all the satellites in space, are now owned by Starlink, Musk, one of his operations. His plan in the next few years is to get them up to forty-two-thousand satellites around the Earth. They said there’re already so many satellites now that it’s starting to affect astronomers’ ability to see the night sky. He’s going to increase that by tenfold in the next few years, and they’re all going to be flashing a big bright X logo to promote… Just think about that. Like, we’ve been putting satellites into space since the 50s. He, in four years, has put up the majority of them, in the last few years. I guess it pays to buy your own rocket company.

Tony 02:12

Yeah. Well, they’re smaller. Aren’t they only shoebox sized, each satellite. Yeah. But yeah, but what, I mean, my issue is that is how reliable is it all, because my Starlink busted, and I called the guy who installed it after mucking around for a while myself and going online and trying to get help and things which was hopeless. And he said, “yeah, everyone’s having troubles, mate. Just send them an email and we’ll send you a new one.”

Cameron 02:36

Right?

Tony 02:37

Yeah, not very good.

Cameron 02:39

That’s good customer service, though, if they’re replacing it. It’s like Apple customer service. You take in your iPhone, “yeah, just have a new one.”

Tony 02:44

No, for sure. It’s good that way, but they can’t be making much money if he’s sending up all those satellites with rockets and then basically giving away the equipment because it breaks.

Cameron 02:55

You have to wonder what he’s going to do when he’s got forty-two thousand of them up there, what his plan is, apart from Starlink.

Tony 03:01

Earth’s going to look like Trantor. Isn’t Trantor the middle of the Foundation where it’s been so over developed, it’s got a big iron circle around it?

Cameron 03:13

Mm-hmm. Well, maybe, you know, they’ll capture the sunlight beaming back down to earth as energy but you have to pay ninety-nine bucks a month to get your sunlight.

Tony 03:23

To charge your car.

Cameron 03:24

Anyway, let’s talk about the market. I did our portfolio analysis this morning. We’re still up, you know, two-and-a-half times the index since inception. It’s been sort of a flat week for us. Our portfolio was down 0.41% over the last week, but old mate TRS was the stock of the week. It was up seven, which is interesting. I saw that this morning, I was like, oh, I wonder what that means for where the market thinks the economy is going when the Reject Shop is up 7% in a week. But then today, CCP took a 15% hit. They came out with their results, and apparently the Australian economy is doing much better than people thought. Chanticleer wrote about it in the financial review: “Why this 15% share price plunge is good for the economy. Investors punished distressed lender Credit Corp after it revealed very good news for the rest of us. The number of Australians who can’t pay their bills is hardly the interest rate rises. The number of Australians struggling to pay their credit card bills is small and showing few signs of growth despite repeated interest rate rises, the soaring cost of living, and a softening economy. Credit Corp boss Thomas Beregi, whose business buys books of distressed credit card and personal loans customers off the banks, says the Australian consumer is still in really good shape, with few borrowers either in arrears or default.” That come as somewhat of a surprise to you, Tony?

Tony 05:02

What does come as a surprise is that Thomas Beregi does this every year, if not every half, and then the share price reacts accordingly. So, he is a classic under-promiser and over-deliver. So, you know, the results came out today, and good on Credit Corp: they’re always first cab off the rank. So, can’t be too hard to have the results out a month after the shut off of the books. But you know, everyone drags their feet except for Credit Corp. Anyway, he’s first out, he always says consensus forecast is too high. “We had a good year, profits up 10%. Blah, blah, blah. But gee, next year is looking tough.” It’s been like that for at least fifteen years. He’s been around for a long time, and every half I see him do it. So, I’m quite relaxed about Credit Corp and the results. I’ll just watch it rebound, because it tends to do this. This is probably an indictment of the fund managers who follow it. Surely, if you’re following this company, you’ve seen Beregi and his pattern over the years, and you know that he’s going to come out and say, “we’ve had a good year, but the future looks bleak.” And that resets the share price, and then he outperforms and the share price booms. That’s been the modus operandi for a long time. So, yeah, I’m thinking that it’s a buying opportunity when Credit Corp drops like this, not a must sell.

Cameron 06:33

Somebody asked on the Facebook group if you would rule one it or just hold on, and would you make an exception because of the circumstances? I replied, “Tony never makes an exception with the rules except for when he does.”

Tony 06:50

Yeah, correct. Well, it’s still above my rule one price.

Cameron 06:53

Yeah, mine too.

Tony 06:54

And it’s still above its three-point trendline, so it’s sell price. If it keeps going down, sure there might be something that the analysts pick up on that I don’t see. But I think it’ll rebound.

Cameron 07:04

Yeah, Chanticleer didn’t mention that he does this all the time, either. You would think that the Financial Review would have some sense of history. But you know, no one remembers history, Tony, it’s one thing that I’ve learnt.

Tony 07:15

Yeah, true. But also, too, I mean, I think credit Corp is more than just credit card bad debts as well. They do utility companies; they now offer loans to people because they’ve got a great credit profile for them after working with them to repay bad debts. They’re in the US. So, you know, it’s not just credit cards. Because credit cards would probably be a worry, because I haven’t seen numbers recently, but I think they’re in decline around the world as things like Afterpay have come in and young people in particular have worked out that it’s not a great deal to put something on a credit card and pay 21% interest on it. So, that kind of business model is still around, but it’s not as strong as it used to be. But Thomas Beregi, he’s never called that out as a problem for them. So, I think he’ll be fine.

Cameron 08:05

Aren’t Australian household debt levels a record high, and the highest in the world?

Tony 08:11

For mortgages, yeah, I guess it’s all debt. But a large part of that would be housing mortgages, I would have thought.

Cameron 08:16

Right, and I’m looking at an article here from a few years ago, and it says credit card debt only makes up 1.9% of all household debt.

Tony 08:25

Makes sense. Because roughly half of the people who have a credit card never pay debt, they’re just what they call revolvers. They pay their balance off every month and collect the points, which is pretty much what I do. And then you know, redeem. Go and buy something with the points when you’ve got enough. A flight or something. So, yeah, it’s a strange business model. It’s been successful in the past, probably gonna be successful in the future, but it’s probably not growing at the rates that it used to grow at.

Cameron 08:52

Right.

Tony 08:53

But anyway, back to your original point. The Reject Shop. I think they just changed their CEOs. Would that be behind their recent share price rise perhaps? But yeah, people might be expecting that they’ll do well, given a recession. Discretionary retail has been dropping leading up to the reporting season. I expect to see a rebound because, you know, surprise, surprise, the economist who can predict the future say we may not go into a recession now. So, the discretionary retailers that have been hard hit might actually start to bounce back from their share price lows, and The Reject Shop might be caught up in that. But yeah, I take your point, the economy’s looking bad, so the Reject Shop will do well. But then Credit Corp should do well, and it’s not. It’s strange, and it’s probably just indicative of the market. No one can really predict what’s going on. I read another article in today’s Fin Review where I think it was now the majority of the economists in the US have changed their tune. It’s not going to be a “difficult landing” or a recession over there. It’s going to be okay. And they’re all saying, “oh, we should have been in stocks this year.” You know, don’t trust crystal ball gazers, I guess, is the learning out of all this.

Cameron 10:04

Well, there was an article on July 17 in the Financial Review. It says, “discount giant Dollarama seeks bargain at The Reject Shop. Despite economic headwinds, there’s been no lack of activity in the local retail sector, and profit warnings from some of the country’s highest profile brands, from Harvey Norman to Best and Less and Adairs, have not dulled interest in Australia from one major overseas retailer, Canada’s Dollarama, the Montreal headquartered discount chain. Sources told Street Talk that Dollarama had approached The Reject Shop, the ASX listed discount retailer whose largest shareholder is billionaire businessman, Raphael Geminder’s Kin Group. Assisting the Reject Shop with those discussions was UBS,” they added. So, maybe they’re in the middle of an acquisition play.

Tony 10:52

Yeah, that’s possible. Could be a takeover play as well. Yeah. My sense is it’s going to be something like that, rather than people forecasting what’s going to happen to the economy.

Cameron 11:01

Right? Yeah, well, their share price has jumped since that article came out on July 7, coincidentally. They were trading at $4.50 on July 17, they’re now trading at $5.30. So, you know, it’s been a corker couple of weeks. So, thank you, Dollarama for that little boost to our portfolio.

Tony 11:22

If it’s even true.

Cameron 11:23

I’m sure it has nothing to do with getting the story out there. Hey, speaking of things that are true. A couple of weeks ago on the show, somebody asked the question about differing wheat prices. We had the wheat price on Stock Doctor, we had a wheat price on trading economics. Can’t remember who asked it, might have been me, might have been somebody else, might have been Alex, I don’t know. I went back to Stock Doctor and asked them about it, and they came back to me a couple of days ago saying, “our development team have found an error in our data. There was a drop in the value of our feed from 636 to 162 on the 29th of March ’21. Several other commodity prices are affected, such as copper and heating oil.” ’21.

Tony 12:09

Copper, really?

Cameron 12:10

That’s two and a half years ago, the value of their commodity prices took a hit, and we landed on to it a couple of weeks ago. So, well, two points there. Number one don’t rely on Stock Doctor’s commodity prices for wheat, copper or heating oil. Secondly, if we do ever spot discrepancies-because remember, we were on the show going, “what’s going on here,” and you’re like, “yeah, I can’t make sense of it.” Well, we should trust our gut and always go back to Stock Doctor and say, “hey, what’s going on here?” Because it just might be that their data is funky, as it was in this case.

Tony 12:48

While I think of it too, and we’re talking about data. A couple of years ago, I had to dive into Credit Corp’s data because the operating cash flow on Stock Doctor differed from the operating cash flow in their annual report, which I think one of our listeners may have pointed out, actually. Stock Doctor came back and said, yeah, this is one of the few stocks they actually manipulate the data for before they release it. I forget now what the actual detail was. They took a view that something was not being reported as operating cash flow and it should’ve been. It was being reported some other way.

Cameron 13:21

Right?

Tony 13:23

I forget now. And they thought that it was accounting standards that didn’t really apply or shouldn’t apply, or didn’t reflect what Credit Corp was doing, so they manipulate the data. You just reminded me of that, and before anyone raises the question and says, “hey, I’m using Stock Doctor and Credit Corp doesn’t appear on my buy list,” that’ll be the reason why.

Cameron 13:43

Well, it was Sam, actually, that highlighted the wheat price differential to us. I just looked it up. So, thank you, Sam, for that. And yeah, a couple of good examples there where if we spot an error… This is why we always DYOR. What do they say? If you see something, say something, they used to say for paedophiles. I dunno.

Tony 14:05

Wasn’t it abandoned luggage at airports or something?

Cameron 14:07

It could have been. Maybe abandoned by paedophiles. Speaking of which, RIP Peewee Herman today.

Tony 14:14

Oh, really? Oh no. I thought you were gonna say Sinead O’Connor.

Cameron 14:18

RIP Sinead O’Connor. And more power to her for taking the heat that she took in 1992. I don’t think Peewee Herman was a paedophile just to be clear, but he did get busted with some child pornography on his computer twenty years ago, one of the two scandals that he had to face down. But much beloved by Americans of my wife’s generation. She absolutely adores Peewee Herman, and so does Fox. Fox has watched all of his shows and his movies. We were just watching one of his movies about a week ago. He appeals to certain kinds of crazy kid like Chrissy was in the 80s and Fox is now. Certainly, a unique character, he was. Doesn’t mean much to Australian audiences, I think, because we didn’t get him or Mr Rogers, all those things. But for Chrissy, yeah, very, very deep feelings for Peewee Herman. Well, my only other news story for today, Tony, from the Financial Review again: “Shares crush year of the bond and biggest sentiment shift since 1999.” And this is a story out of London, July 30. “All the chatter back in December was that 2023 was to be the year of the bond, and for a brief moment or two in the first quarter that call in the economic doom and gloom that underpinned it look right. It is now being overrun, though, by an avalanche of demand for shares that has unleashed a furious rally across the globe. In a sign the gains are probably far from over, it has also made investors more hopeful about stocks relative to bonds, that at any point since sentiment trader models began comparing them twenty-four years ago. ‘As sentiment, technicals, and risk of the recession got pushed further out, we moved from being underweight stocks to overweight,’ said Nathan Thooft, Global Head of asset allocation at Manulife Asset Management in Boston.” And the man voted to have the best surname. “He has reduced his credit exposure in favour of an equity overweight.” So, weren’t we just talking like last week about investors pulling their money out of the share market and putting it in bonds.

Tony 16:29

Yeah, that’s right. And even the week before, I think, you had an article saying that someone thought the share market wasn’t paying enough as dividends now or as a return now, because you can get risk free 4% or 5% in the bond market, and therefore why take the risk of getting 9 or 10% capital appreciation in the share market. And then they’ve all come scurrying back to the share market. So, honestly, I have often thought the most — what can I say? It’s appendix of the share market, is the asset allocator. Seriously. They get paid a squillion dollars to sit there and go, “get bonds this year and 51% shares. No, no, no, no, no, no, no, no. 48% bonds and 52.” But it’s silly. Work out what’s going to be the best asset class long term, put all your assets there. But these guys get paid to try and read a crystal ball about whether they should be in bonds or shares or some other assets. And no one ever goes back and says, “how did you go?” They never got held to account. The fund gets held to account if it doesn’t perform. But these asset allocators, I mean fair dinkum, they may as well work for the RBA. That’s a kind of hocus pocus detailed report. Just ignore it. Just stay, as we’ve said, as I’ve said many, many, many times, just stay fully invested. Don’t worry about trying to predict the future. You might suffer some setbacks for a while, but, you know, over time the escalator goes up in the share market. So, there’s no point trying to time it.

Cameron 18:04

You know, I often think I’m so grateful that I have QAV to educate me about this stuff. Because if I was going by articles I read in the Financial Review… Like, one week its shares are butt, buy bonds. The following week it’s don’t worry about bonds, invest in shares. Come one. What am I supposed to, people?

Tony 18:25

Yeah, and it is driven by news events. I don’t know how many fund managers there are around the world, but they all put out a press release talking about the minute allocation changes to their portfolios. It keeps the Fin Review in print, in newsprint, but it’s completely useless information.

Cameron 18:41

And if you look at the Australian share market, look at the All Ordinaries, I mean, it’s had a pretty good couple of months. I mean, three months, really. I mean, we’re above where we were back at the beginning of May. It dropped over the course of May, though, since the beginning of June its way up. Dropped again at the beginning of July but has been up consistently since then. But it’s been positive over the last three months. It almost feels like we’ve turned a corner in overall sentiment of the share market. But again, who knows. But it just goes to what you always say: stay invested. You never know when the market turns around until you can look back at it with some, you know, retrospective glasses.

Tony 19:24

Correct. And, you know, I wonder how much of these changes to asset allocations have people going, “shit. We’ve missed the turning point in the market. Quick, jump in because it’s up 10%.” Which is just, you know, a classic late to the party sort of investing style. It’s a strange way to do it.

Cameron 19:41

The All Ords is almost back to where it was six months ago. Started February at 7709, it’s currently 7654. It’s been a choppy ride, but, you know, with the bottom of the market in the last six months in March at 7085, it’s, you know, way up since then. So, you know, all the people that capitulated in March, April, May, June, have missed out at this stage on a very nice run. Anyway.

Tony 20:13

Yeah, and they’ll be back. Run another 10–20%, they’ll come back.

Cameron 20:17

Yeah. Hello, Alex. What do you have for us today as our official reader of questions?

Alex Kynaston 20:25

Yes. Thank you. I have a question from Jeff. So, he says, “Good morning, kung fu master Cam. I hope you and your family are doing well. A podcast question. From a beginner or alternatively hands off investment perspective, there is often talk in investment circles about the value of ETFs. A great place to start or alternatively for set and forget investing. Why does there seem to be no discussion about LICs or maybe LITs? I listened to Marcus Padley and also equity mates finance podcasts. While these podcasts are very high level (no system) they will often talk about the value of ETFs. Same with Market Index and Nabtrade newsletters. LICs and LITs definitely secret squirrel stuff. I remember TK talking about including LICs in his will. Linda and I did similar when we redid our will. Is it because of performance, fees, unfranked dividends, something else, all of the above? Just checking and always learning more. QAV is definitely the right place for that. Thanks again to you and TK for all your great work. I add my QAV subscription to my portfolio of solid investments. Jeff.”

Cameron 21:31

Oh, that’s nice, Jeff.

Tony 21:32

Yeah. Thanks, Jeff. Yeah, I mean, we’ve spoken about this before over the years, but it’s worth revisiting, I think. So, the couple of questions in there. Why do people kind of focus on ETFs rather than LICs, or sometimes LITs? Until I talk about the difference between LICs and LITs, I’ll just refer to them as LICs. That’s kind of a general name for them. ETFs suit index style investing, because their fees are very, very low. There’s enough experience in running them now that they can make an index and they run quite cheaply. So, that’s really what they good for. Whereas an LIC tends to be for an active manager, so that they can raise some money and then invest it. They’ll charge higher fees because they’re doing more work, both themselves and in terms of visiting companies and analysing reports and data and then buying and selling shares. So, their fees are always higher. And generally, they charge performance fees as well, which ETFs don’t. So, oftentimes, it’s the old 2 and 20 model, though, no one charges 20% these days that I know of. It’s usually around 1–2% for management fees, and then usually about 10%, sometimes a bit more, about performance of the LIC. Why are those two structures that way? Why are they evolved that way? Well, the big difference between ETFs and LICs is that LIC is what’s called a closed end fund. So, in other words, if you’re raising money, if you’re starting an LIC, you raise all the money, you put it into a fund, and then you issue shares to people. And if they want to sell their shares, they find someone else to buy them, which is what the stock market does for them. An ETF, which is an open-ended fund works differently. So, if you buy shares in an ETF, they’ll go out and take your money and buy more shares for the index fund that they’re running. And if you sell shares in an ETF, they’ll have to sell underlying shares to pay you out. So, the reason why LICs tend to attract active fund managers is because when the market turns down, even though the share price for the LIC might drop as people sell shares, the underlying funds aren’t changed. They can just simply sit there and ride it out and then start to reinvest when the market looks like it’s turning up again, whereas an ETF will get smaller and smaller and smaller as the market drops and people get scared, and they sell the stakes in the ETF. So, that’s probably the main reason why LICs and ETFs have evolved for one to be passive and the other be active. That closed ended fund thing is a big deal, and that’s why I prefer LICs, because I’d rather see the funds stay intact when the market’s turning down. Again, the same discussion we had before about always being invested, because if you’re an ETF and you’re selling as the market drops because people are redeeming, it’s the worst time to sell. You don’t want to sell when the markets dropping, you want to sell at the top if you can, but you certainly don’t want to sell at the bottom. So, that’s a problem I think with ETFs. But having said all that, if all you want to do is invest in an index fund then an ETF is the way to go, because they generally charge about a quarter of 1% as a management fee, so there’s not too much friction on the index like returns. And the ETF market now is so large. It’s largely driven, pioneered by the US, but now in Australia as well. You can pretty much buy an ETF for almost any sort of index you want to, like a tech index or the Australian index, or the NASDAQ or commodity index, like gold, or whatever, and it won’t cost you very much to invest in those things. So, that’s attractive to some people as well, who might decide that they want to invest in tech stocks, but don’t want to do the work to work out which ones to buy. They just by them all and pay a low fee to do it. So, both ETFs and LICs have benefits. The other thing to say then, is the difference between LIC’s and LITs. So, Listed Investment Companies versus Listed Investment Trusts. The companies are companies, and when they have a tax event — so they’ve earned income, either through dividends or selling shares — they pay company tax at the company tax rate of 30%. And being a company, it’s up to the directors as to when and how much they pay out in profits, or pay out in dividends, of their profits. Whereas a Listed Investment Trust being a trust means that you don’t own shares in a company, you own units in a trust. And just like a family trust, if anyone out there has one, they will know that every year all of the income is distributed in a trust structure. And so, there’s no ability to control the flow of the profit out of the trust. It just has to all go. And then once you receive it, and if they’ve earned franking credits, they also get distributed to the unit trust holders. And then it’s up to them as to what their tax rate is, depending on whether it’s a personal tax rate, which could be higher, could be lower, or whether the superannuation fund or something else has bought the units in the Trust for them. So, again, there’s swings and roundabouts with both of those. I tend to favour, again, Listed Investment Companies, because having that discretion to continue to pay dividends, even if they don’t have the profits to support them — like they can dip into reserves and retain profits if they want to, if directors feel that it’s a bit of a one-off bad year this year and they’re going to still pay a dividend, they can do that. Whereas, a Listed Investment Trust, if it earnt no money that year, you don’t get the income from it. So, it’s more volatile from that respect. And you might get a lot of income one year which you didn’t plan on, and that could push you into a higher tax rate as well. So, there are implications for that kind of difference in the structure. So, I prefer LICs because they’re closed ended and they don’t have to sell in a downturn, and because the directors can decide when and how much to pay dividends, regardless of how much money they made that year. They obviously can’t pay dividends if they’ve got no retained profits and they made no money that year. But generally, a well-managed Listed Investment Company will keep retained profits to get it through the duller years so they can still keep paying dividends, much the same as any sort of listed company that’s well managed will do as well. So, that’s the difference. ETFs are the flavour of the month, and you know, if we think about the investment ladder, buying an index fund is oftentimes people’s first step into the share market, and they may go no further because it’s a great way to invest for the long term. If you’re like Alex’s age, you can buy an index fund and hold it for the rest of your life, and you’ll get at least the market return. Or if you’re putting it into your Will, if you have kids who may not understand investing, it’s not a bad thing to do as well. That’s what Warren Buffett is doing, although I don’t think he calls it an ETF, he calls it an index fund, which they do in the States. So, yeah, benefits for both. I’m attracted to the closed end structure of an LIC, and also, too, because they’re managed by active managers the good ones do outperform the market, and we’ve had Washington Soul Pattinson’s on before. I’ve spoken about Wilson Asset Management and their stable of LICs. Of recent times, even though they claim a good long-term performance, of recent times they’re more focused on paying out a high dividend ratio, which will suit retirees for example. I think last time I had a look it was about 7% plus franking credits, so their capital appreciation hasn’t been that great. But they certainly do a good job of giving retirees a really good, franked dividend to live off.

Tony 21:40

Would Berkshire be an LIC, an example of an LIC?

Tony 26:22

No. Good question, actually. It’s generally seen as a conglomerate because it actually owns operating companies as well. So, the section of Berkshire Hathaway which just buys shares on the US stock exchange, which is only I think about a quarter of their business, yeah, you could spin it off as an LIC. That’s the same sort of thing. But they do own the railroads and insurance businesses, etc., so it’s more like a Wesfarmers. They’re a conglomerate.

Cameron 30:03

Yeah. Okay. Fair point. All right, Alex, it’s time for you to take a test now. Are you ready?

Alex Kynaston 30:10

Yep, I’m ready. I have a question.

THIS SECTION CONTAINS CONTENT WHICH IS VISIBLE TO QAV CLUB SUBSCRIBERS ONLY.

Cameron 1:41:15

If you liked the QAV podcast, help us out and help your friends out. Help Australia out by telling somebody about it. You can shoot somebody an email with a link to our latest newsletter. Say, “hey, you should check this thing out. I think you’d really like it.” Or write us a review on Apple podcasts or on Spotify, it only takes thirty seconds. You can find the links in our newsletter, or our blog posts every week, and follow the instructions for how to do that. Or write a review or make a post on Facebook or Twitter or X, whatever it’s called now, on threads or Vidhana, whatever it is, whatever the social media channel of your preference is. Just help spread the word. You’ll do us a favour and you’ll help your friends and help Australia learn how to take control of their investing as well. The QAV Podcast is a production of Spacecraft Publishing Propriety Limited, authorised representative of AFSL 520442, AFS representative number 001292718. Please don’t make any investment decisions based solely on listening to this podcast. This is presented as general advice only not personal financial advice. We don’t know your personal financial circumstances. Please see a financial planner before making any investing decisions.

DISCLOSURE

In the interest of full disclosure, we would like to advise that as of the date of this post, the QAV team currently hold these stocks:

AFG CCP FHE FPR FMG GNC IGL JHG PLS QAN QBE RMS SGM VEA VUK WAM WHC

If you’re interested in learning more, please review our trading and disclosure policy.