Hello QAVvers

It’s another Tuesday.

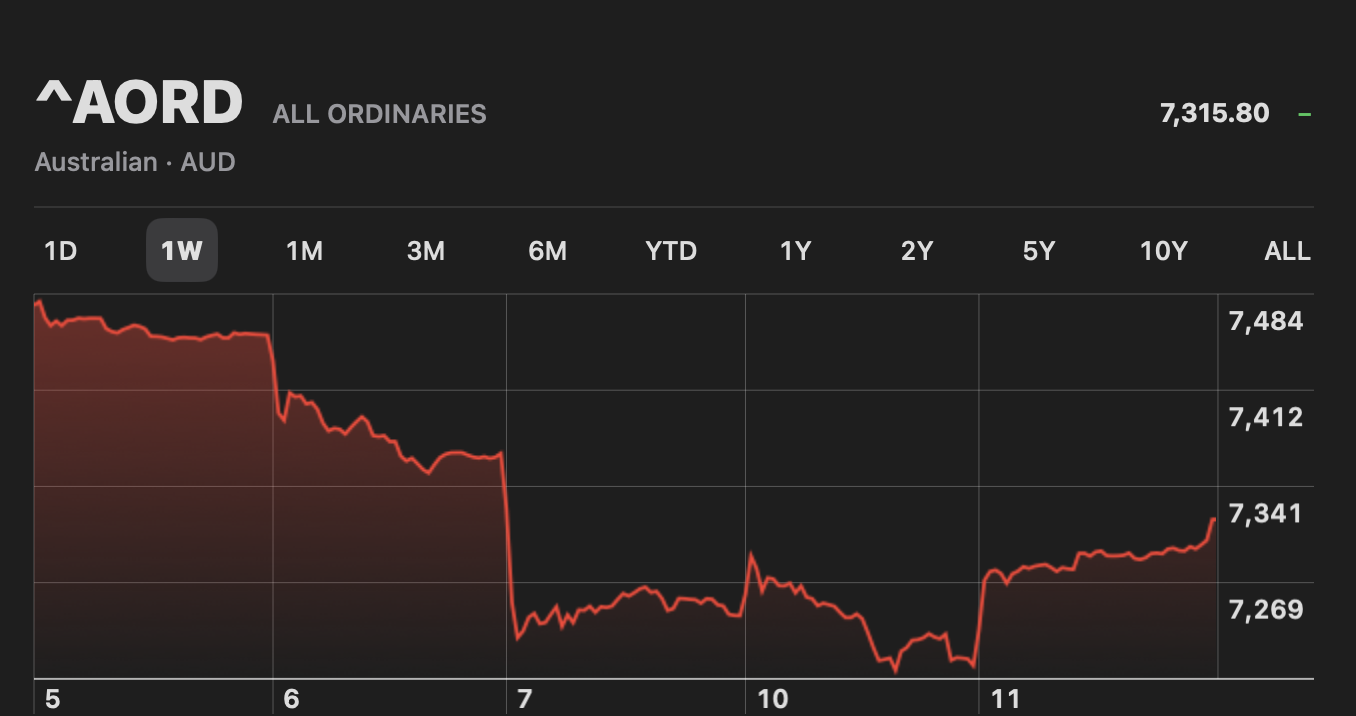

Despite the RBA deciding to hold rates where they are, the US Federal Reserve threw a spanner into our fun times and the market dropped last week. It recovered slightly today.

Let’s have a look at the portfolio.

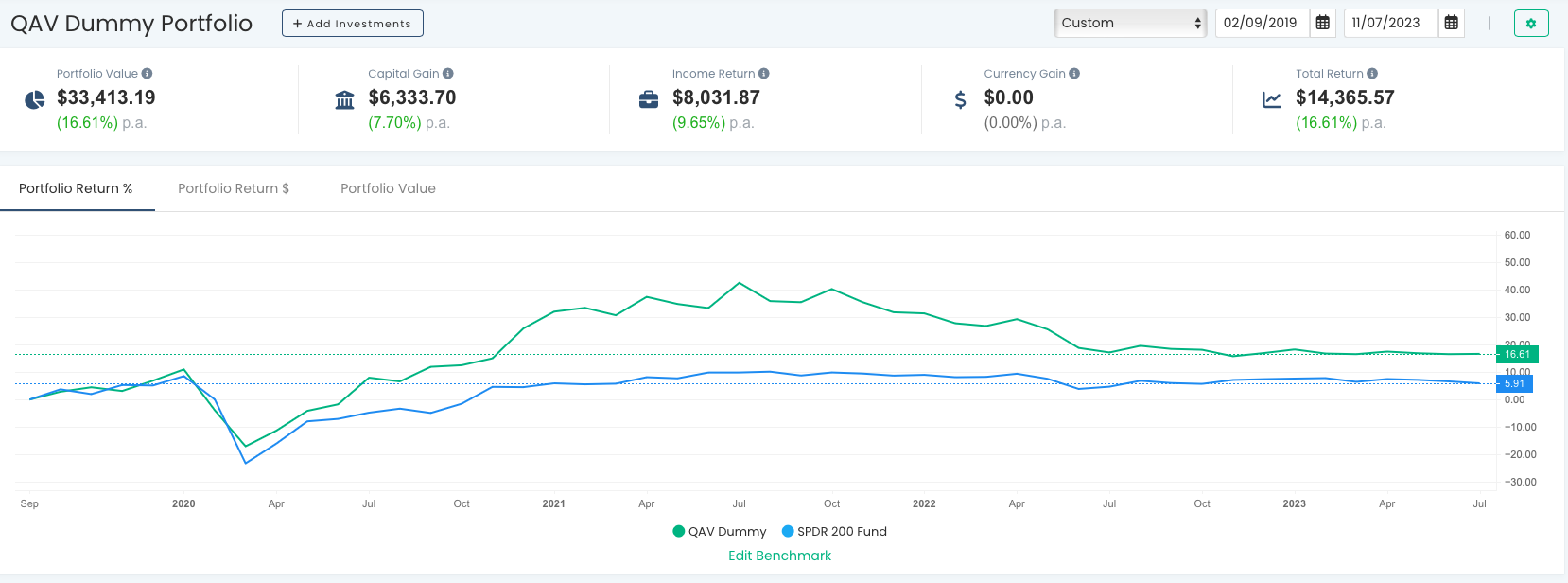

QAV PORTFOLIO REPORT

INCEPTION REPORT

We’re still outperforming the STW by ~2.5 times since inception (02/09/2019).

You can always check out the live version of the portfolio chart here.

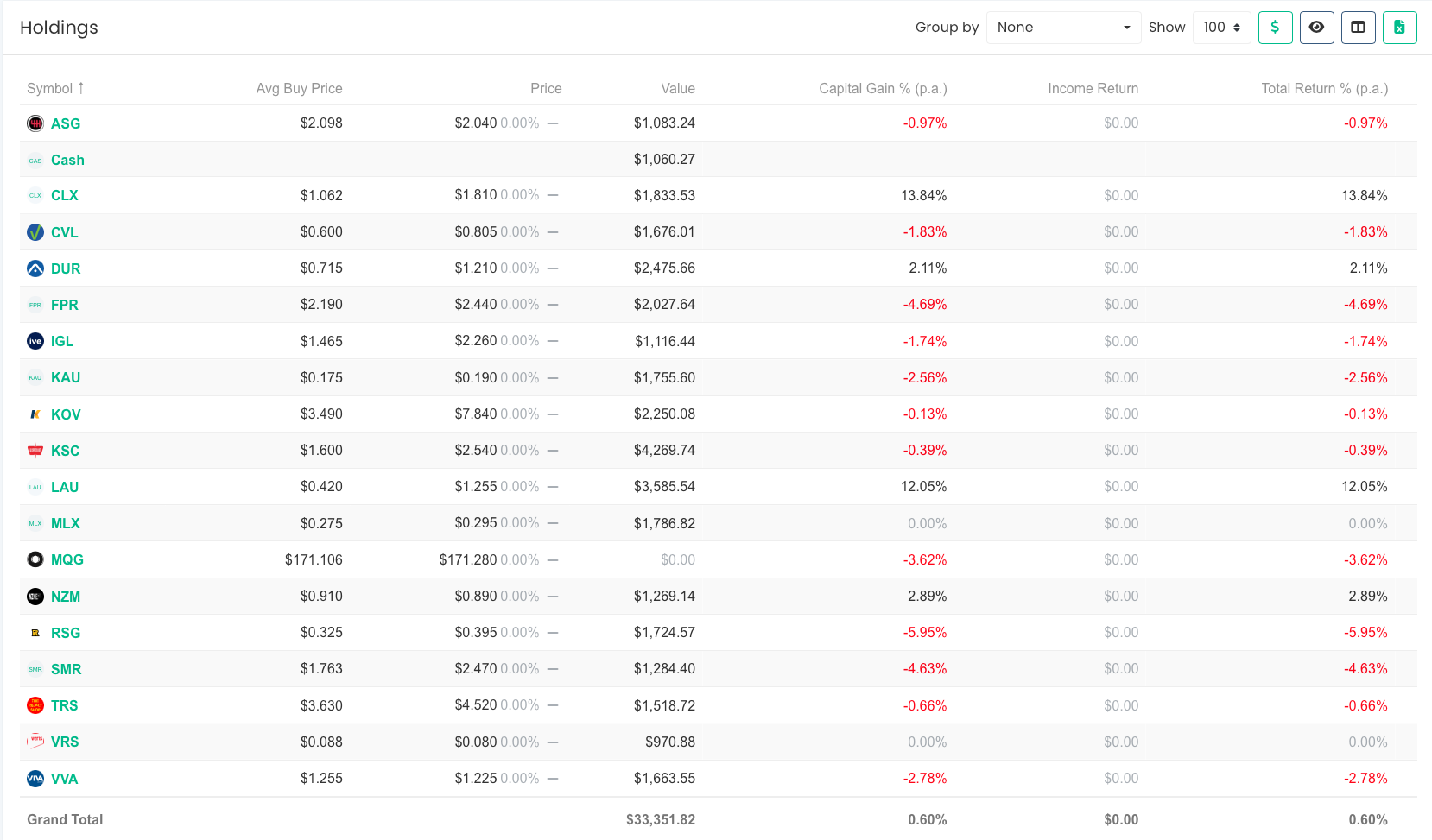

Here are how the stocks have performed in the last 7 days. LAU and CLX were the best performers.

RECENT TRADES

We sold MQG (3PTL) on 7/7, now that the dividend has finally been paid, and replaced it today with GNC.

STOCKS OF THE WEEK

During the last week, we did trade some stocks in our portfolios. Details here.

** As always, please check our work, DYOR, and consult a financial advisor before making any investing decisions.

BUY LIST

Each week we produce a buy list that we share with our members. The intended primary purpose of this buy list is for club members to use as a reference for comparing their own buy list. In theory, all of our buy lists should look pretty similar each week.

THIS SECTION CONTAINS CONTENT WHICH IS VISIBLE TO QAV CLUB SUBSCRIBERS ONLY.

LAST WEEK’S EPISODE

THIS SECTION CONTAINS CONTENT WHICH IS VISIBLE TO QAV CLUB SUBSCRIBERS ONLY.

Detailed highlights of the episode:

THIS SECTION CONTAINS CONTENT WHICH IS VISIBLE TO QAV CLUB SUBSCRIBERS ONLY.

Episode Transcription

Cameron 00:08

Welcome back to QAV. This is episode 627. Tony, it’s the fourth of July. I said to Chrissy this morning, do you want to celebrate Independence Day. She’s like, eh, not really. 2023, the first show of the new financial year and we’re going to be talking about performance and how we did. There’s been an interesting chat on our Facebook group on how people have performed. All over the place, interestingly. Some good numbers, some not so good numbers, which we’ll drill into why that might be. But how are you Tony, before we get into the markets? How’s life in Sydney? Rainy up there?

Tony 00:50

Yeah, rainy and foggy today. Not too bad, but it’s clearing. Hopefully it’ll clear soon.

Cameron 00:55

You’re not gonna let that stop you playing golf though, I imagine.

Tony 00:58

No, I booked in for Thursday, so I’ll get out and play. Not playing today. Played on Sunday and it was lovely. I mean, the weather here is fantastic in winter normally, we’re just having an off day, which is fine. Got to happen at some stage.

Cameron 01:11

If it’s raining, do you put your wellies on?

Tony 01:13

Not wellies, no. I put the rain gear on.

Cameron 01:16

What’s the rain gear? What do you wear on your feet when it’s raining?

Tony 01:18

Oh, golf shoes. They’re normally weatherproof.

Cameron 01:21

Oh, okay. Well, let’s get into the markets, Tony. I mean, the All Ords is down a bit today. We’ve got the RBA making an announcement in nine minutes. We’re recording this around 2:21pm on Tuesday. We’re expecting an update from the RBA. Do you want to forecast what you think the RBA is going to do today, Tony?

Tony 01:47

Yeah, it’s pretty impossible to forecast what the RBA is going to do. Most economists are betting on the RBA pausing, so they won’t raise interest rates. I don’t know, I’d be contrarian and say they probably will. I mean, I’ve got lots of issues with the RBA as we’ve talked about before during the course of the interest rate hike cycle. I had similar concerns years ago when they kept cutting interest rates, because it was forcing retirees up the risk curve to maintain their retirement incomes, and I didn’t think they needed to cut. I mean, you know, one of the arguments that has been put forward now is our interest rates need to rise to be more in line with the rest of the world. Well, if that’s the main case, then just do away with the friggin RBA and just, you know, have a robot. Have Chat GPT there saying, “Feds raised, UKs raised, Europe’s raised, we need to raise.” If that’s your argument, that should be the last thing. But I think my current bugbear with the RBA is the indications are that inflation is coming down, and I think they’ll probably argue that’s only a short-term indication, they want to see if it plays out or not. There are lots of indications that inflation is coming down. So, the question in my mind is: the RBA has a mandate to keep interest rates, sorry, to keep inflation between 2 and 3%, but it doesn’t have a mandate as to how long it needs to take to do that. They seem hell bent on doing it quickly, which to me is destroying the economy because the main pressure on inflation seems to be, at the moment, wage rises which are being caused by inflation, which is being pushed up by higher interest rates. So, they’re kind of throwing gasoline on the fire, in my opinion. And if they want to get inflation down to 2 or 3%, they could pause and do nothing for a while and see what naturally occurs. But they seem to be taking this view that, “no, we’ve been told to get inflation down to below 3%. We’re gonna do it. We’re just gonna keep doing it. Doesn’t matter what all the side effects are.” And I think that’s wrong. My bet is I’ll be contrarian and say they’re gonna raise rates, but we’ll know soon.

Cameron 03:53

Well, if you have any friends from your time as a client of PWC, you just call them and ask them what the government’s gonna do.

Tony 03:59

Have you ever looked at the PwC logo? It looks like a hand giving someone the finger. Have a look at it and just squint your eyes.

Cameron 04:09

The logo on their website is like some sort of orange set of blocks.

Tony 04:15

Yeah, it’s like a broken bar chart, isn’t it? But the one on the side is like a thumb and the other three are like a middle finger being raised. Anyway.

Cameron 04:25

Yeah. Oh, well, let’s get into it. As I said, not a bad week for the All Ords in the last week but down a bit today, maybe in expectation of the RBA. The dummy portfolio closing out the financial year didn’t have a bad financial year, depending on how you want to measure it. So, you know, we use Navexa to track our portfolio. According to the Navexa, for the financial year we were up 9.5% versus the STW, which was up 14.5 %. But you did your own maths on both…

Tony 05:05

My own maths. Magic maths.

Cameron 05:09

You came up with a different result. And then we had an email conversation with the CEO of Navexa, Navarre, who basically told you to shut up and get back in your box.

Tony 05:19

No, he told me to use Excel, which I was doing anyway.

Cameron 05:27

So, your calculation was pretty simple, right? You took the value of the portfolio on the 1st of July last year and the value of the portfolio on the 30th of June this year and calculated the difference, and worked that out as a percentage, and it came out at about 10%.

Tony 05:46

Yeah, 10.5/11%. Yep.

Cameron 05:48

And then you took the value of the STW at the same time periods and calculated the differences of percentage, and it was 10.5%. So, you said, well, we’re pretty much neck and neck with the STW. But in Navexa, there’s a big difference. Now, I tried to follow Navarre’s explanation in the email thread, and it went way over my head. Can you summarise it for everyone?

Tony 06:10

Well, I think we’ve been through this, seen this movie before, but a year or two ago…

Cameron 06:14

He actually said, “refer to your emails last year.”

Tony 06:19

Well, there was this whole conversation in the past about money weighted returns, and time weighted returns and Navexa builds everything up transaction by transaction and says, “well, you bought this stock for this period of time and made this profit or loss. That’s one building block in the portfolio’s performance for the year and the next time, you bought another stock, and it had this holding period, and it made all losses, and that’s the next building block, etc, etc.” And it adds it all up and takes the losses from the profits and gives you your return. Now, I mean, that sounds fine and reasonable. But it doesn’t add up when you just look at the ending over to starting and work out the percentage. I haven’t been able to get to the bottom of it and I suspect it’s got to do with the cash account that we asked them to put in Navexa. Because if you recall, this kind of also started around a time when we went, “hang on, where’s our dividends going?” They’re getting recorded, I think in terms of performance, but then the cash was just being lost through the cracks in tracking it and being able to reuse it to repurchase things. And some of the examples that were given in Navarre’s emails seem to suggest that cash is being treated like a new input into the fund, when it shouldn’t be; it’s part of the fund all along. So, I suspect that’s what’s the difference, that’s what’s causing a difference, is that the way we operate the dummy portfolios, we’re saying it’s like a hermetically sealed portfolio. We’re not putting any new cash into it during the year and we’re not taking cash out. So, our wages aren’t going into it and we’re not living off dividends. So, it just stays within the fund and gets reinvested. And therefore, we need a cash account, which gets sometimes larger, sometimes used to buy new things, dividends go into there, and they get reused eventually. And sometimes we sit on cash for a while. I suspect it’s that cash buffer which isn’t being included in the portfolio calculation because, as Navarre said, he builds it up transaction by transaction of stocks bought, and if there’s cash there, perhaps that’s not been taken into account. That’s just my guess, I don’t know otherwise. But you know, for the life of me, I can’t explain why it differs from end value over beginning value.

Cameron 08:31

Well, he did say in his email that he is taking the cash into account. And okay, so the difference between your figures and Navexa’s figures for the QAV portfolio is only a difference between 9.5% and 10.5%? It’s not huge.

Tony 08:47

Yeah.

Cameron 08:47

But your figures for the STW is also 10.5% where there’s is 14.5%. That’s a big difference.

Tony 08:55

Yeah, I can’t explain that.

Cameron 08:58

Why is this so effing hard, Tony?

Tony 09:00

Yeah, that’s my question. I mean, there’s just so much time being spent on trying to get these things correct when it’s end over start gives us a percentage. If you want to do it over time, use the RRI formula in Excel. End over start and factor in the number of periods.

Cameron 09:21

I think I’m gonna have to do that for my super portfolio, because I went to Australian Super’s website today and tried to work out what my super fund — which is where I do most of my investing, because I don’t have any money — over the last year was, and when I did the financial year performance report, it wasn’t including dividends in that either. And so, I you know, went to their support text messaging service at 9am this morning and said, “hey, why aren’t dividends being included?” And as of 2:30, I haven’t had a reply from them. So, stellar work from Australian Super. Oh, RBA keeps cash rate on hold at 4.1%.

Tony 10:05

Oh, I lost my bet. Well, good. I think that’s a wise outcome.

Cameron 10:14

Yeah, I wonder what the markets going to think about that. How was your performance in the last financial year, Tony?

Tony 10:21

Well, you’ll have to bleep this. It was shithouse.

Cameron 10:26

Is that a financial industry term?

Tony 10:28

It is, yeah, it is around here. No, it was poor. It was negative, something like ‑15%. Just put some context around that, when we talk about my performance, I’m going to start using our self-managed super fund, which is, again, hermetically sealed. I made a little contribution to it last year, but not enough to move the dial on returns. And we haven’t been taking money out. So, it’s like our dummy portfolio. Now, but it was, it was backwards. I’m doing that because we’re using the rest of our shares to, you know, live on, and the ins and outs happening with that just makes the performance of it harder to be meaningful. Yeah, it was negative, and I’m gonna have to sit down and work out why. I mean, I think I know why; there were just too many sells during the year, either rule ones or 3PTLs.

Cameron 11:17

Do you need to have a Zoom call with me, Tony, so I can make sure you’re following the system correctly?

Tony 11:23

I am following the system. It’s been going against me, unfortunately. Yeah. So, what can I say? I think there’s been too many sells. I’m going to have a good look at it a bit further and see if I can glean anything from that, that I might be able to do differently. But a couple of other things, which I think may have affected it. I have a much smaller portfolio than I have in the past. I think there’s, you know, eight stocks, I think, from memory, in the superfund portfolio. And that’s a factor of, there’s been periods when I’ve had to rebuy or double buy a stock because there’s been nothing to buy on the buy list. But also, too, I’m happy to concentrate my portfolio a bit. I can accept the various the volatility that comes with that, and this is one of those situations which is more volatile than the dummy portfolio and more volatile than the market. But that goes both ways. When things turn, it’ll be more volatile going upwards as well. And I have done a lot of testing on small portfolios. Dylan did some testing for me on a four-stock portfolio a couple of years ago, which he said was the optimum size for a portfolio, if you can stomach the volatility.

Cameron 12:33

Four?

Tony 12:34

Charlie Munger has said a four-stock portfolio is the best size. So, I’m kind of mindful of that. I’ve done my own paper testing of a one stock portfolio, just buying the biggest ADT stock that we can buy on the buy list, and that’s performed better for me than holding fifteen stocks. Which kind of makes sense, because a) it’s top of the buy list, and b) it’s, you know, our best idea, so to speak. But it is volatile. So, I think that might also be playing into my returns this year, because it’s a smaller portfolio. Yeah, but definitely the problem has just been too many rule 1s and 3PTL and commodity sells. So, got hit hard at the start of the financial year with the coal stocks coming off. And then things like Karoon Energy I’ve bought and sold a couple of times during the year. And it’s kind of just zigzagged, so I’ve been caught out there a couple of times. And then just all the other normal trading and other stocks. Challenger Financial Group was one of them, which was doing well, and then I had to sell out off. So, yeah, I mean, it’s tough, but, you know, I’m not really measuring myself on a one-year basis. If I look at the long term returns for that super fund, for the portfolio, it’s still in the long term 17.2%, something like that. So, you know, double market, so that’s good. And I kind of think about this is like an elastic band; it’s like, if we’re getting double market over the long term, and we’ve fallen back behind the market this time, it’s like stretching an elastic band in one way. And then if it’s going to get back up to double market on average, it’s going to fling back the other way and give us a good return eventually, to catch up to that kind of long-term average, which I still expect it to do.

Cameron 14:16

I’m sure there’s a lot of people, particularly our club members, that will be happy to hear that because some of them have had a rough year.

Tony 14:22

Is that schadenfreude? They’re happy to hear me lose money.

Cameron 14:28

I think it’s more in terms of, well, it’s not just them that’s losing money. And, you know, your portfolios are probably many, many times bigger than most of our portfolio. So, 15% down for your portfolio is a bigger paper loss than it is for most of us. But it’s interesting because, you know, in terms of the system, as I said, the dummy portfolio is up 9.5%/10.5% depending on how you want to measure for the year. Why do you think the dummy portfolio had a relatively good year, whereas your super portfolio didn’t? Just luck of the draw with the stocks that you had to, like, the commodity stocks, you had to sell, and then struggled to get back on solid ground with the rule 1ing, etc?

Tony 15:22

Yeah, look, it is going to be the mix of stocks, I would think. And perhaps the smaller portfolio’s more volatile. But yeah, I mean, I think the dummy portfolio can but into a lot smaller stocks then when I can. And sometimes having to buy, sometimes the only large cap ADT is way down the bottom of the buy list, so I think that might be part of it, too. Like, I think the most recent example was Collins Food was the last thing on our buy list, and I bought it, and then had to 3PTL it. And now it’s bounced back. So, that’s an illustration of what the year has been like for me. Whereas the dummy portfolio’s largely fishing at the top of the buy list. So, I think that’s the benefit of having less constraints on ADT.

Cameron 16:06

Yeah, right.

Tony 16:07

And maybe that just means I need to draw the mark higher for the bottom of the buy list, like a higher cut off for me. But Ryan’s researching that for me now and we’ll see what the outcome is.

Cameron 16:19

So, say 0.2 or 0.3?

Tony 16:22

0.2, yeah. And we’re still working through that. He’s been up and down with the results on that. He’s done some research on whether we should buy from the top of the buy list first or buy from the bottom of the buy list first. Originally it said there was an overwhelming support for the top, and now his latest analysis is showing support for the bottom. So, we’ve just got to drill down and get it right. I keep sending him back saying, “ah, but you didn’t use the commodity sells, or you sold something when you’re waiting for a dividend check to be paid.” So, we’re kind of refining the process to make sure it’s accurate. And on top of that, I have been doing a paper test of a QAV 0.2 or better portfolio, and that’s actually been really hard to fill. It’s only got about three stocks in it since I started a couple of months ago, and it’s been underperforming. So, yeah, there’s a fair bit to go yet before I can decide where to draw the line.

Cameron 17:16

Yeah, I imagine you’re a bit like me, because my ADT for my super fund is similar. I’m only able to buy ASX 300 stocks in that. And there’ve been long periods over the last year where I have been sitting in cash, because I just couldn’t find anything that I could buy. And then I would double up on positions, which makes it a lot more volatile. I think I’ve probably got eight or ten stocks in my super portfolio, because it’s been, you know, very difficult to find stuff to buy this year. Double positions on a lot of those, too. So, yeah, that’s kind of been challenging. The light portfolios, I did the end of financial year report on those. And you know, we only started that in April last year, and a lot of them, you know, only closed-well, the last one only closed a couple of weeks ago. I started it in December ’22 and only closed it a couple of weeks ago because I couldn’t get rid of the starting capital. It took me six months to get rid of the starting capital, which is crazy. Every time I’d buy something, I’d have to rule 1 something in the portfolio a week or two later. It’s been a crazy period. But there’s been some interesting results that people have reported on Facebook. Ed and Brent reported their results yesterday, or the day before. Interesting that their FY23 results were almost identical. I think they were both up about 8.5% for the financial year, which is interesting.

Tony 18:53

And similar to the DP, as well.

Cameron 18:56

Yeah. The DP is, you know, 9.5/10.5 depending on how you measure, but all in the same sort of ballpark. Interesting. Brent also reported his results going back, I think, to FY21. And, you know, this to me is a classic example of sticking with a system like QAV year in, year out. And he said his total return since January 2021, which was his inception date, is 78.87% versus the AXJOA total return of 15.18%. So, his out performance is 63.68% since January ’21. Financial year ’21 was 21.29% versus 8.4 for the All Ords. FY22 was 35.87% versus ‑0.7% for the All Ords, and ’23 was 8.5% percent versus 14.75% for the All-Ords total return index in his calcs, which has an underperformance of 6%. But all up, you know, over the three years, very good. But I had somebody else say that over the three years, I think it was Stephen, said over his three years, he’s actually down a bit. So, that’s interesting. I suggested we jump on Zoom. I want to understand more about how his results would be different from Brents. But there you go. I think the analogy you made of buying a house last week really resonated well with me, I’ve thought about that a lot this week. You’re right. You buy a house, spend a million bucks on a house, the housing market goes down by 10%. And this struck me as interesting, too. Like, when we think about the housing market, and when it gets talked about in the press and the financial media, you know, they don’t say, “your house has gone down by 10%,” it’s the “housing market across Brisbane”, or “across Sydney” or “across Australia is down by 10%.” It’s more, you know, dispersed, the blame for it; “the housing market is down.” Whereas when it’s my share portfolio, I think, “oh, my portfolio is down by 10%,” regardless of where the market is at some times. I think, you know, the other difference is, when people buy a house, of course, they’re going to live in the house — assuming it’s not a rental property, right — they’re living in the house, selling it and moving has a lot of emotional, physical and emotional hurdles you have to get over to do that. But also, there’s something different, I think, when people buy a house, they’re probably a little bit more confident in the fact that it will do well over the long term, because it’s kind of a generic thing. We know the property market rises. When you’re buying a portfolio of shares, particularly if you don’t have a strategy in place and you’re not confident that you can continue to pick shares that will do well in a portfolio over a ten-year period. Before QAV, if I had a share portfolio that was going back by 10/15/20%, it would be easy for me to go, “well, I bought bad shares in bad companies and I don’t know what I’m doing,” and they could go down to zero. When you’re following QAV, you know, these companies are very unlikely to go out of business, unless, you know, they might get acquired, but they’re not gonna go broke. We’re not buying dotcom start-ups with no profits that could literally, you know, go belly up. These businesses are going to weather a financial storm and if you continue to buy good quality companies that have a good track record of profits, and you’re buying them when you think they’re at a discount or their intrinsic value, over the long term they’re probably going to do okay, right?

Cameron 18:56

Yeah, well, you said so much there, some really good things in there. It’s in terms of viewing the housing market differently to the share market, it comes back to that discussion we had a little while ago: no one stands around the barbecue talking about shares, they stand around the barbecue talking about property. So, in terms of knowing that if you buy a house it’s going to go up in the long term, that opinions been reinforced by your parents, by your uncles, by your aunties, by your colleagues, by your friends. You’d be hard pressed to go and find a number of people, but you might find one or two who said, “yeah, the markets gone against me with my house.” Generally, people are quite happy with how things turned out long term with their housing purchase. Whereas, you know, if you raise the spectre of stocks in a conversation, you’ll generally find someone who says, “oh, don’t talk to me about stocks. I bought this and it went down.”

Cameron 23:46

Yeah.

Tony 23:47

Or, “I got this tip and it went down.” And so, you don’t get that same sort of positive reinforcement about the stock market. But fairly soon after I started investing, I always viewed a stock portfolio as another house, you know, in the same sort of mindset that it was another asset to invest in. Rather than being a stock market of companies, it was… At one stage we had our house and I’d kept the prior one, so we had two or three rentals plus our owner occupier, and we had a share portfolio. And we got rid of the rental properties over time and bought bigger houses and more shares. And, you know, now it’s kind of like a two-house portfolio. And that’s how I think of it; it’s just like having another house.

Cameron 24:30

Yeah, you’re right. I think for most people, the idea of property ownership is fairly well established in this country, but shares are like quantum mechanics for most people.

Tony 24:41

And it shouldn’t be, because they all have superannuation funds which have shares in them, and they’re usually pretty comfortable with the superfund. No one’s running up to Canberra and protesting against the superannuation industry or the superannuation system. They do on certain issues like taxation, but generally people retire and they’re fairly happy with how their super has been growing over the years. But they don’t put two and two together and say, “oh, okay, that’s been driven by the share market. If I’d done it myself, I’d get a similar sort of return.”

Cameron 25:13

Yeah. That reminds me, I was invited out to lunch last week, Tony, by another long-term podcast listener of mine. Somebody else who goes back to the Napoleon podcast days. And he was in Brisbane, he’s from Melbourne, he was in Brisbane and took me out to lunch at the Queensland Club, where I felt like I was in a republican convention. It was full of old rich white men wearing suits.

Tony 25:44

I can imagine.

Cameron 25:45

I put on a suit for the first time in several years to go. It was interesting. I walked in with a ponytail and a suit on.

Tony 26:00

And they thought Barry and Stan have come.

Cameron 26:01

Yes, exactly. But this guy who took me out runs a wealth management‑a wealth advisory, sorry, a wealth advisory business in Melbourne. And he said that he’s basically value investing. He’s a big fan of Charlie and Warren, and everything he does is value. But he said that he always gives his clients what he called a “dinner party stock”, something to talk about at the dinner party. He said, I put them all into Afterpay when it was like two bucks and, you know, they could talk about that. There’s always something a little bit sexy and speculative that they can talk about. But 95% of it’s all, you know, really boring, you know, QAV type stocks. He does things a little bit differently to you. His performance isn’t quite as good. He said it’s about 15% compound, but that’s pretty good. So, anyway, I’ve invited him to come on and he’s going to be a guest, David, in the next couple of weeks. So, it’ll be fun to have a chat.

Tony 26:59

Yeah, that’s good. And you just reminded me of a couple of interactions I’ve had in the last week or so. So, one was with Taylor, the next Tom Cruise, after his meeting in Sydney. But last time he was in Sydney, he came, and we had a chat. And it’s always great to see him. It’s really nice, he looks me up and comes around for a chat. But he was saying, like, he’s looking after these influencers, he’s their manager. And they’ve all got this cash sitting there but it’s not their core competency on how to invest it. And they’re all scratching their heads about what to do with it. And of course, therefore, they’re pray to, you know, the Lamborghini dealers or whoever, you know, is trying to separate them from their money. And similarly, I played golf with a couple of thirty year old guys Sunday week ago, and we had a chat afterwards. The topic turned around to investing when they found out about the podcast, and they’re like, “well, we just don’t know where to begin. What do I do? How do I start? I want to go into the stock market, I’ve got no idea.” And I think these people have been let down by the fact that you can’t get wealth advice without paying $5,000 to a wealth advisor who has to do a whole heap of paperwork to send off to the government before they can give you any sort of advice at all. And I know we talked about this before, but, you know, there was a review into that, and the government’s only accepted some of the recommendations, not all of them, so I can’t see it changing anytime soon. But there is a real gap in the market for someone to be able to sit down with these people and say, “hey, this is how you get started.” With the golfers, for example, we had a chat about, “well, you’ve got to get get into the property market,” for example. One of them was renting his own house and I said, “well, that’s just dead money.” And he’s like, “oh, yeah, but I liked the freedom.” And you know, I said, “well, if you took that rent money, could you get a mortgage” “Yeah.” “Would you have spare rooms to rent out in the house if you did that?” “Oh, yeah, I’d just buy a three- or four-bedroom house and just use one for myself.” I said, “so, someone can be paying for three quarters of the mortgage?” “Oh, yeah, I hadn’t thought of that.” And we just sort of went on from there. And I said, “well, you know property tends to double every seven-ten year, so in that time period you’ll be able to go and get a second mortgage on the property.” “Oh, really? What’s that?” You know? So, just the basics, how to attack things, the pragmatics of how to attack things and get a start, just isn’t being taught. And I think part of that problem is because there’s big barriers to proper wealth advice in this country. It’s a shame.

Cameron 29:30

I love the fact that you’re on the golf course saying, “yeah, I do a podcast.”

Tony 29:33

Yeah. It usually goes, “what do you do?” “I’m retired.” “Oh, really?” I say, “yeah, but I’m pretty busy. I’ve got a horse breeding business, I do a podcast, I invest for myself, you know, help a couple other friends out,” and they’re like, “oh, what’s your podcast on?” “Quality at Value, value investing.” “Oh, tell me about it!” It’s always the topic of conversation once they know.

Cameron 29:56

Yeah, I have similar conversations in my kung fu classes. “What do you do?” Moving right along, then. Jason from QAV light. One of our light subscribers. I don’t encourage questions from light subscribers, but Jason has been very active and given me lots of good feedback since light started. And he did a little report for me on his performance as a QAV light subscriber over the last sort of year or so, which I thought was interesting. He said he’s done fifty sells since he started, with twenty-three rule 1 sells and twenty-one 3PTL sells. There’s also four commodity sells in there. He said, “I thought I’d focus on the rule 1 sells and whether the 10% was a decent sell line, since in the episode you said it was a bit of a random number. My average rule 1 loss is at ‑12.69%. Out of my twenty-three rule 1 sells, twenty-one of them continued to drop even further. Out of those rule 1 sells that dropped even further, the average low would have been ‑27.41%,” lower than his buy price. “Out of my twenty-three sells, eleven recovered to have a high price higher than my buy. The average percent of the recovery is 23% above my buy price. The final bit of analysis. So, those above that dropped then recovered to be a profit, how low did they drop? The numbers tell me they averaged to a ‑24.5% loss. Those that didn’t recover to a profit average loss was ‑29%. So, what does all this mean? Well, it’s as clear as mud. Maybe a ‑25% loss could be the new rule 1 but losing 25% then selling is a tough loss to take, and honestly a bit of a gamble. I would really need to see how much the recovery is to offset the additional loss. Maybe that’ll be my next bit of analysis. Anyway, take it with a grain of salt. Jason.” I thought that was interesting to the rule 1 analysis, because, you know, I know that’s been a question you’ve had in your mind, about should we change the figure. You talked about that last week. What do you think about Jason’s analysis?

THIS SECTION CONTAINS CONTENT WHICH IS VISIBLE TO QAV CLUB SUBSCRIBERS ONLY.

Cameron 1:41:46

The QAV Podcast is a production of Spacecraft Publishing Proprietary and limited authorised representative of AFSL 520442, AFS representative number 001292718. Please don’t make any investment decisions based solely on listening to this podcast. This is presented as general advice only, not personal financial advice. We don’t know your personal financial circumstances. Please see a financial planner before making any investment decisions.

DISCLOSURE

In the interest of full disclosure, we would like to advise that as of the date of this post, the QAV team currently hold these stocks:

AFG CCP FHE FPR FMG GNC IGL JHG PLS QAN QBE RMS SGM VEA WAM

If you’re interested in learning more, please review our trading and disclosure policy.