How does Horizon Oil stack up as a value investment?

Overview of the Company

Horizon Oil Limited, incorporated in 1969 and headquartered in Sydney, Australia, is engaged in the exploration, development, and production of oil and gas properties across China, New Zealand, and Australia. The company holds interests in the Block 22/12 oil fields in Beibu Gulf, China; the PMP 38160 Maari/Manaia oil fields in New Zealand; and the Mereenie OL4 and OL5 oil and gas fields in the Amadeus Basin, Australia. Additionally, Horizon Oil is involved in the exploration and evaluation of hydrocarbons.

Current Share Price Analysis

At the date of our analysis, the price was at $0.20, which was above both our Intrinsic Value 1 (IV1) and our Intrinsic Value 2 (IV2), suggesting it might be overvalued relative to these benchmarks.

Average Daily Turnover

With an average daily trade of $0.259 million, Horizon Oil Limited is categorised as a Small-Cap stock. This classification can pose challenges, particularly regarding liquidity, potentially affecting the ability of investors to exit larger positions without significantly impacting the market price.

Yield vs. Bank Debt

The company’s yield surpasses the mortgage rate, which is favourable for investors seeking dividend income to counterbalance their mortgage obligations.

Financial Health Assessment

Horizon Oil Limited demonstrates strong financial health, with a stable trend indicating robust financial stability and sound management practices.

Price-to-Earnings Ratio

The current Price-to-Earnings (PE) ratio stands at 7.79, which is not the lowest in the last six reporting periods, so we can’t score it on this metric. However, it is less than the yield, which is a positive.

Price to Operating Cash Flow Ratio

The Price to Operating Cash Flow ratio is 3.35, below our threshold of 7. This indicates the stock may be undervalued, as it would take approximately 3.35 years for the company’s operations to generate cash equivalent to the stock price.

Share Price in Relation to Book Value

The share price is currently above the book value, failing the “book plus 30%” test. This suggests that investors might be paying a premium for the company’s equity, which could be seen as a negative indicator.

Ownership Structure

Directors hold 20.91% of the shares, a significant percentage suggesting strong alignment with shareholder interests and potentially enhancing investor confidence.

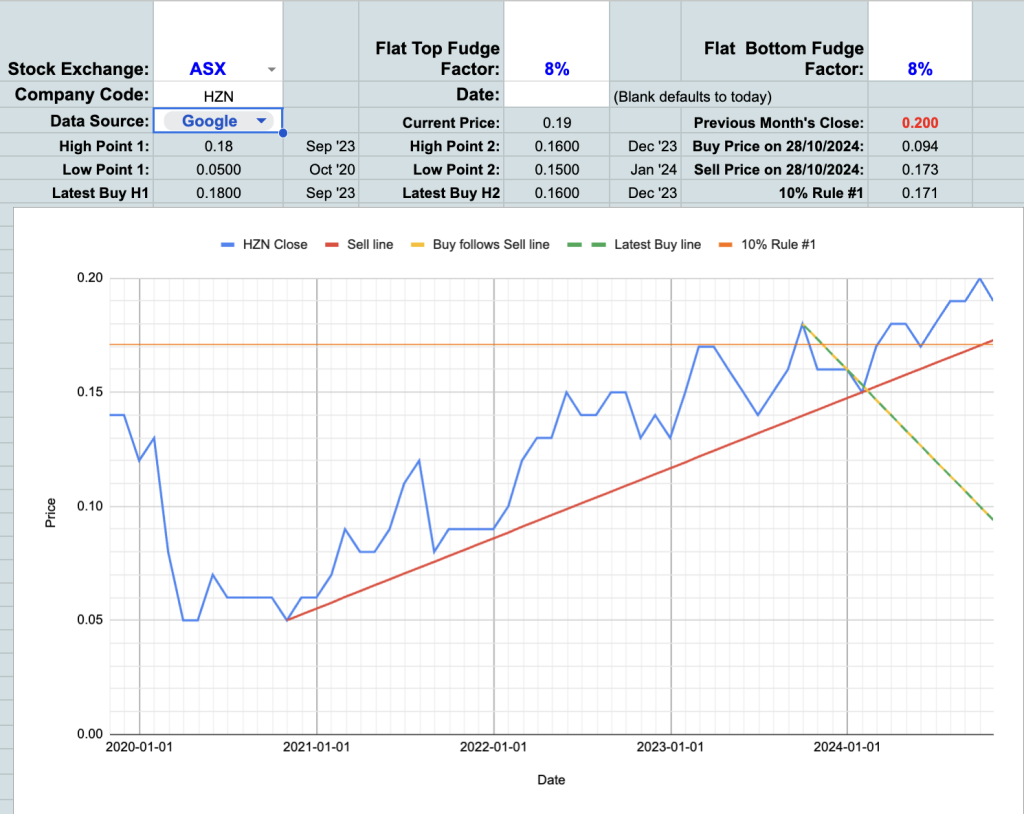

Recent Market Sentiment

The stock hasn’t had a recent 3‑point upturn, and is actually currently slightly below its recent high mark, but has been its buy and sell lines since early 2024.

Consistency of Equity Growth

The company has not demonstrated consistently increasing equity, a negative indicator of management quality and potentially concerning regarding sustainable growth.

Conclusion

THIS CONTENT IS ONLY AVAILABLE TO QAV LIGHT AND CLUB SUBSCRIBERS.

Disclaimer

This podcast is an information provider and in giving you product information we are not making any suggestion or recommendation about a particular product. The information has been prepared without taking into account your individual investment objectives, financial circumstances or needs. Before you decide whether or not to acquire a particular financial product you should assess whether it is appropriate for you in light of your own personal circumstances, having regard to your own objectives, financial situation and needs. You may wish to obtain financial advice from a suitably qualified adviser before making any decision to acquire a financial product. Please note that all information about performance returns is historical. Past performance should not be relied upon as an indicator of future performance; unit prices and the value of your investment may fall as well as rise.

Transparency is important to us. We will always be very open and honest about the stocks we own. We will also always give our audience advance notice when we intend to buy or sell a stock that we are going to talk about on the podcast. This is so we can never be accused of pumping a stock to our own advantage. If we talk about a stock we currently own, we will make it known that we own it.

This email is authorised by Anthony Kynaston (AR No. 001292718).

Copyright © 2022 Spacecraft Publishing Pty Ltd trading as QAV (“QAV”) (ABN 41 163 119 300) which is a Corporate Authorised Representative (CAR 001292718) of MF & Co. Asset Management Pty Ltd (AFSL 520442).

No part of this content may be reproduced in any form without the prior consent of Spacecraft Publishing.