Hello QAVvers

TK told me to stop looking at the market so.…

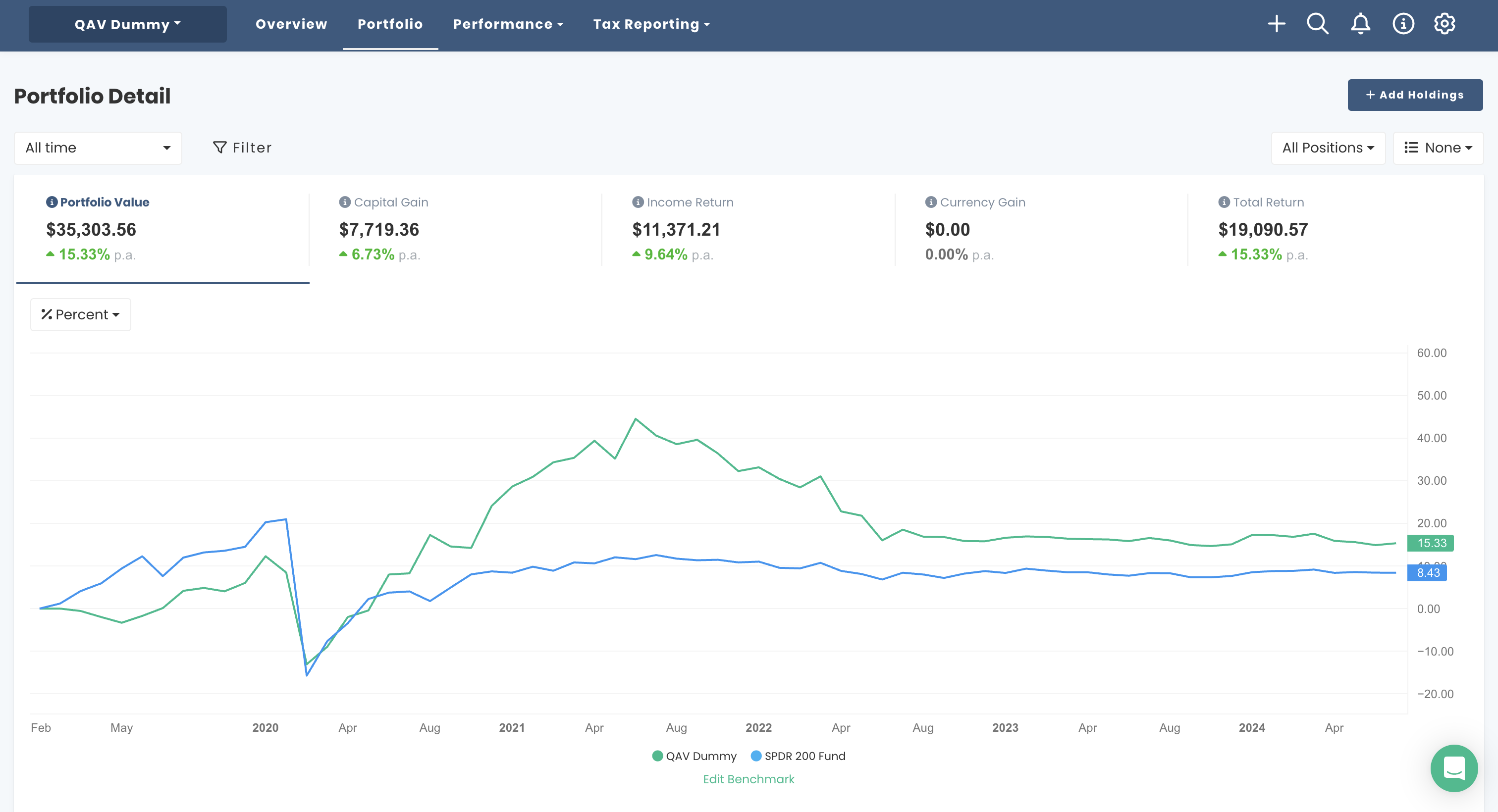

QAV PORTFOLIO REPORT

The Dummy Portfolio is performing well against the benchmark over most time frames.

SINCE INCEPTION (15/04/2019)

Our portfolio is performing at a little below double market p.a. since inception (about five years).

In the last 7 days haven’t traded anything. No trades since 31/05/2024, actually.

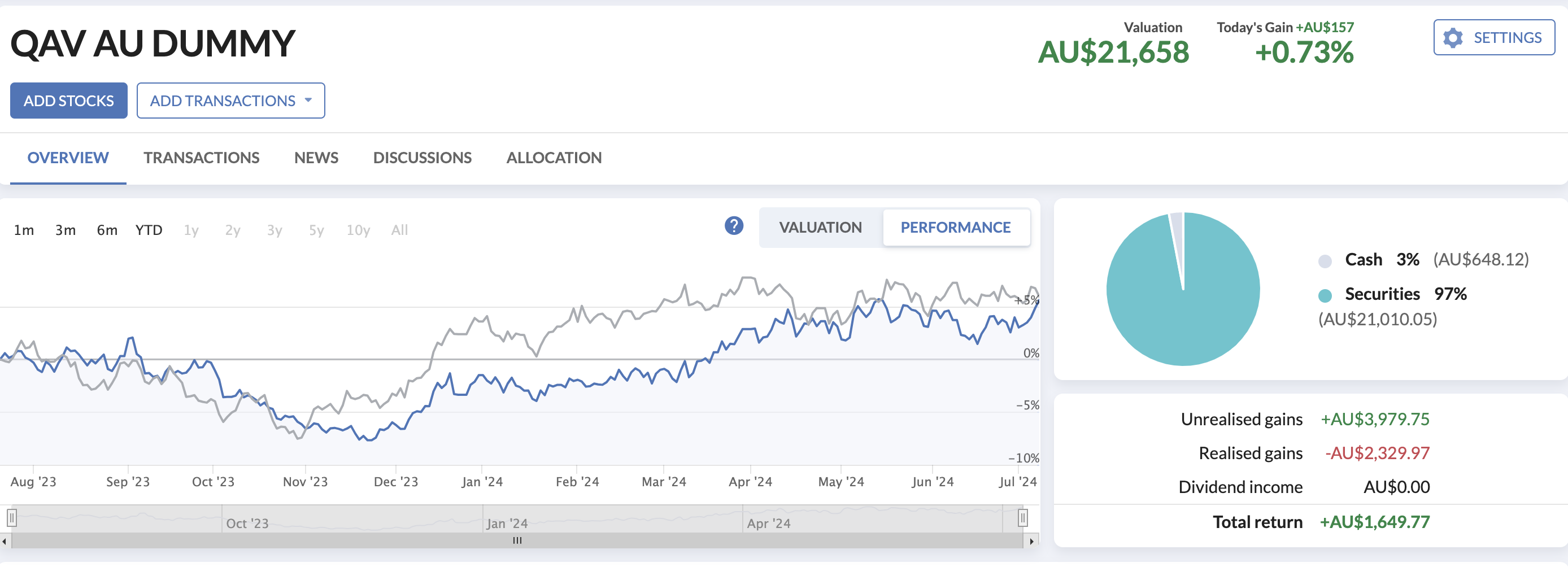

QAV STOCKOPEDIA DUMMY PORTFOLIO REPORTS

QAV AU DUMMY

Neck and neck with the benchmark.

QAV US DUMMY

Dropped a bit in the last month, so now it’s a few points below the benchmark.

BUY LIST

Each week we produce a buy list that we share with our QAV Club members. The intended primary purpose of this buy list is for club members to use as a reference for comparing their own buy list. In theory, all of our buy lists should look pretty similar each week.

As always, please check our work, DYOR, consult a financial advisor before making any investing decisions.

DOWNLOAD THE AU BUY LIST (Club members only)

DOWNLOAD THE US BUY LIST (Club members only)

LAST WEEK’S EPISODE

In this episode of QAV, hosts Tony Kynaston and Cameron Reilly discuss the implications of interest rate hikes on property and stock markets, and the ongoing strength of the job market despite economic slowdown. They review listener-submitted financial year results, touching on both gains and losses, and Tony dives into an in-depth analysis of Auric Mining Ltd (AWJ). Topics include the company’s operations, growth potential, and unique financial model.

00:00 Introduction

01:17 Financial Year Reflections

02:31 Interest Rates and Economic Anomalies

05:08 Quantitative Easing and Inflation

12:09 Portfolio Performance Review

18:49 QAV Club Member Survey Results

36:02 Auric Mining Analysis

Transcript

QAV 727 Club

[00:00:00] Cameron: Welcome back to QAV. Tony Kynaston, I feel like I’m just talking to you all the time these days. You were on Futuristic yesterday, back here today. Um, Supreme Court gave a ruling last night, Tony, that anything you and I do on this podcast, if it’s part of our official duties, is, uh, basically, uh, protected.

[00:00:33] Cameron: We’re protected from any future prosecution by anybody for anything that we may do or say. Uh, in the, in the, uh, performance of our official dues. Cause we can’t be worried about the, the future ramifications of anything that we do while we’re doing this. What, what kind of world would that be? Where people have to worry about future ramifications.

[00:00:52] Tony: Yeah, a lawless world. It’s funny how the Supreme Court of America just created a lawless world. Yeah, I would go, yeah. It’s, um, it’s funny how this, the Republicans stack Supreme Court of America have cleared Trump. Isn’t that interesting? Surprise, surprise.

[00:01:10] Cameron: surprise. Well, let’s see what we’ve got on the talking list of things

[00:01:17] Tony: Well, happy, happy new financial year. It’s the

[00:01:20] Cameron: Oh, it is. Well, yeah, not so happy when I look at my financial year final results. We’ll get to that in a minute. Um, and the ABC this morning, their chief business correspondent Ian

[00:01:36] Cameron: Vrrrrr, had an article, Why Property and Stock Markets Are Thumbing Their Noses at Rate Hikes. And he starts it off with our favorite phrase, This Time It’s Different.

[00:01:46] Tony: mm hmm, mm

[00:01:50] Cameron: shout out to Ian, IanV, It’s a phrase you’ll hear through almost every boom, any fi, anytime, a financial bubble. I can’t talk. It’s a phrase you’ll hear through almost every boom. Anytime a financial bubble forms or with the advent of some new market phenomenon, it’s rarely the case.

[00:02:10] Cameron: Whenever human behavior gets out of whack or markets out of line, there’s usually some kind of reckoning that results in a return to normality, a return to the mean. Occasionally, however, things take just a little longer. To behave the way we expect. Right now, we’re in the midst of some rather strange occurrences.

[00:02:31] Cameron: Despite a tolerant round of interest rate hikes across the globe, and particularly the developed world, financial and property markets are still booming. Even more startling is that employment has remained incredibly strong. Economic growth may have slowed to a crawl, but workers have so far been kept afloat by the best jobs market in close to half a century.

[00:02:52] Cameron: And that’s not just here. Our jobless rate is about 4%, higher than midway through last year, but still at historically low levels. The US also has an unemployment rate of 4%, while the UK is sitting at 4. 4%. While welcome, this has been totally unexpected and it’s seen central bankers scrambling to try to nut out just why developed economies aren’t reacting to interest rate hikes the way they once did.

[00:03:17] Cameron: Household spending has remained relatively strong and while spiking interest rates have had a devastating impact on some, mostly younger, households. Older generations have sailed blissfully through the storm. I seem to recall, uh, a couple of years ago, Tony, um, our This Time It’s Different friend, Alan Kohler, explaining that the unemployment figures that get bandied about are a little bit murky.

[00:03:46] Cameron: That, uh, the gig economy had a lot of people who were working just a few hours a week, but they were being classified as employed, uh, when they weren’t really earning the sort of income that you would expect from somebody in full employment. Do you know if that’s still the case? That 4 percent number, how much, have you seen any analysis to say whether or not that’s a rigididge or a little bit fluffy?

[00:04:09] Tony: I haven’t seen recent analysis, but, um, I think Alan Cole was reporting it still hold, uh, from memory, if you work more than one hour a week, you’re classed as employed in the unemployment stats, and, uh, the number was about 14 percent was the number of people who were looking for work or looking for more work, so more hours. Yeah, but you know, we had this discussion with Alan at the time when he was on the show. There will certainly be people in the gig economy who want more hours, and certainly be people who are part time workers who are looking for a full time job, but the gig economy certainly suits a lot of people as well, like students or people working second jobs, so, um, yeah.

[00:04:57] Tony: You’d have to do a very deep dive analysis into what the real number is. It’s probably higher than 4%. Um, but yeah, I think the point of this article is very interesting is what you do with interest rates. And I think the point is, as I’ve said many times, the RBA and federal reserves around the world, central banks around the world caused the problem after the GFC, when they lowered interest rates to, you know, Pretty much zero or negative flooded the world with printed money and that caused a start of an asset inflation bubble and now they’re they’re trying to reduce that but the inflation is a problem and so they don’t want to add to it too much.

[00:05:36] Tony: I think they’re actually causing inflation by the way, um, or adding to inflation which was caused by something else besides interest rates uh and and now they don’t know what to do and you know that’s that’s a common problem with economists they’re great at telling you Academically, how the economy works and what happened, they’re terrible at predicting what to do or coping with something that, a new circumstance that comes along.

[00:06:00] Tony: Eventually they’ll muddle their way through it and luckily there’s a lot of people working on it and a lot of central banks grappling with the same problem. Um, but yeah, there’s a two speed economy going on. If they raise interest rates now to try and put a brake on, um, people investing in assets like property or shares, Um, that raises inflation and if they lower interest rates now, um, then the asset prices take off again because people have more money to invest.

[00:06:29] Tony: So my gut feel is interest rates are going to stay where they are for a while until things wash out a bit more in the economy.

[00:06:37] Cameron: He talks about the history of quantitative easing here, talking about Japan toying with it, then China, then when the global financial crisis hit Europe and the US dived in. It says, and then he says, it worked, but we had no idea of the longer term consequences. Now it seems we’re beginning to understand what they are.

[00:06:58] Cameron: Essentially a form of money printing, the world’s biggest central banks pumped tens of trillions of dollars into the financial system. What it did was inflate asset prices. There’s a shock. Property, stocks, and bonds continually shot to new records regardless of what was happening in the broader economy.

[00:07:15] Cameron: The problem was that it was difficult to reverse. Every time they tried, it threatened to choke off credit and create a brand new financial crisis. So when the pandemic hit in 2020 and they opened the monetary floodgates, the global financial system already was awash with cash. While they’ve managed to wind it back in the past two years, the global economy is still swimming in excess cash.

[00:07:37] Cameron: To the tune of about U. S. 28 trillion dollars. So, again, I seem to recall, when we were doing the whole quantitative easing thing during 2020, there were plenty of voices saying, it’s not a problem. We know how

[00:07:56] Tony: Oh yeah.

[00:07:57] Cameron: it off. It’s all, it’s under control. Nobody panic. Know exactly what we’re doing. Well,

[00:08:04] Tony: shows at least on MMT, um, Modern Monetary Theory, which was all about printing money to solve your problems. And the, and the criticism that kept coming back at the people who were saying MMT is a thing and it’s going to be great and we’ll, you know, have good economies forever, was that if you print lots of money, you’ll cause inflation.

[00:08:24] Tony: And here we are, four years, barely four years on, and that’s what’s happened. Um, and, you know, now governments have got to deal with that problem. And, you know, that’s part of the issue. Governments are short term focused. They had to solve the problem of the GFC, and they had to solve the problem of the pandemic, and so they threw cash at it.

[00:08:44] Tony: They couldn’t afford, you to give cash so they printed money. Um, problem solved and on to the next thing. And then, you know, four years later they’re now trying to deal with inflation. So that’s, that’s, I guess, a problem with the short termism of government. Um, but the RBA is supposed to, you know, help with that by having people who aren’t elected every four years on the board and have, you know, a longer term horizon to solve these problems.

[00:09:10] Tony: But we’ll see if they do. Um, they’ve had a mixed bag of success so far.

[00:09:16] Cameron: the article just goes on to talk about how Australians are swimming in cash, richer than ever before.

[00:09:22] Tony: Well, some are. Some, I think that’s it. Some are. That’s the important part about the article is young people and people who don’t own a house who are trying to get into the housing market, for example, people who are taking out large mortgages, they’re not doing it well. Um, people with large families who found a supermarket and heating bills and other bills that have gone up, insurance bills, they’re not doing well.

[00:09:44] Tony: It’s people like me. You know, who’ve sat on assets for a long time, who are okay in this, in this environment. Um,

[00:09:53] Cameron: People like me that got divorced several times and did a couple of tech startups who are on the bones of our arse and have nothing.

[00:10:01] Tony: and your costs are going up.

[00:10:03] Cameron: Yeah, and my income’s going down.

[00:10:06] Tony: yeah. So, you know, write a letter to the financial review complaining about this central bank printing money. Let’s see how far you get.

[00:10:13] Cameron: And up until yesterday I thought AI was going to solve all my problems. You spent two hours convincing me that it’s not, it’s not going to bring about the revolution that I so very need,

[00:10:25] Tony: Well, it’s funny. I’ve, I’ve been reflecting on that discussion. It’s funny how we bring our own frameworks to whatever prediction we’re making. Like you, you, you need, Communism to save your arse and I need capitalism to keep my arse safe. So

[00:10:39] Cameron: of course,

[00:10:40] Tony: they’re the, they’re the points of view we’ve brought to our predictions.

[00:10:42] Tony: Yeah,

[00:10:43] Cameron: yeah. We’ll see which one plays out. Um, all right, well, there you go. Michelle Bullock, Sheriff Bullock, as I like to refer to her, because I’m a Deadwood fan, uh, says she isn’t keen on another interest rate hike. She

[00:11:00] Tony: good news.

[00:11:02] Cameron: That regardless of what happens to GDP, so long as unemployment remains strong, Australia can emerge from the inflation inferno in relatively good health.

[00:11:12] Cameron: So,

[00:11:13] Tony: mean, there are people out there arguing for a rate rise because we’ve kind of, we are out of step with the rest of the world. They, they went up a couple of steps more in their rate hikes and we stayed still after they started to buy here. And now we’re out of step because they’re starting to cut rates around the world.

[00:11:29] Tony: So I think it makes sense that we hold them where we are. a little bit longer. Inflation has definitely come down. It may have gone up. People got spooked when the last latest numbers came out because they went up by half a percent or something, but it’s not a big move. It’s a blip, I think, in noise. So my gut feel is though, I think they’d be at this stage, given what we know, I think they’d be crazy to cut or raise rates at this stage.

[00:11:53] Cameron: Well, let’s see how crazy they are.

[00:11:55] Tony: Yeah, and that’s a prediction from me, which I hate doing. I hate predictions. Who knows? I’d rather position myself to have a good system so that I can ignore what happens with interest rates.

[00:12:07] Cameron: Yeah. Well, speaking about a good system, financial year is over, as you said earlier.

[00:12:13] Tony: Mm hmm.

[00:12:14] Cameron: had a look at the various portfolios. The dummy portfolio finished the financial year up 9%, versus the STW up 12%. So, we’re a little bit behind the STW for the year, but up 9%, still a good result for the year.

[00:12:30] Cameron: Surprisingly for me, the light group The four light portfolios bundled together were up 8 percent for the, uh, financial year. um, you know, pretty much the same as the dummy portfolio, uh, not surprising following the same system, but they were quite negative, uh, not that long ago. And they have recovered a lot, um, in the last six months to get up to the 8%.

[00:12:57] Cameron: So I’m pretty happy with that.

[00:12:58] Tony: It does seem, sorry to interrupt, but it does seem to be a thing with our portfolios that they sort of take a while to bed down. You, we found it with the dummy portfolio and then with the light portfolios, we start one, they either go sideways for a while or they go backwards for a while and they sort of bed down after the process has taken hold, after we’ve got enough stocks in them, um, we kind of juggle the stocks a little bit, then they sort of go on from there.

[00:13:21] Tony: It seems to be a common pattern I think.

[00:13:24] Cameron: Yeah, once they get through the three, sorry, the rule one death trap,

[00:13:29] Tony: Mm hmm.

[00:13:30] Cameron: particularly in a volatile market, once they, once they reach escape velocity, they get

[00:13:35] Tony: Yeah.

[00:13:36] Cameron: well, well and truly over their, uh, uh, buy price and they get up 10, 20 percent up. Yeah, unless there’s a commodity crisis or a, um, three point trend line sell.

[00:13:47] Cameron: You know, we don’t end up doing a lot of trading. In terms of all time results for the dummy portfolio, that’s sort of five and a bit years now, it’s up roughly 15 percent CAGR per annum, versus the STW up 8 percent over the same amount of time CAGR per annum. So. Not quite double, um, but pretty close to double the market.

[00:14:11] Cameron: The light, uh, as a group since inception, which is kind of early 2022, up 5 percent versus the STW up 8%. So again, uh, not beating it, um, but not a terrible result either, um, considering where it was a little while ago. It seems to have stabilized and is, uh, you know, showing some, some good gains. My super portfolio, on the other hand, sorry, yeah,

[00:14:41] Tony: say, I was just going to say, just the commentary on that. It seems to be the way my, like my investment experience is that we don’t beat the market every year. I think you did some analysis which said it was about 2 or 3 in 10 that I haven’t outperformed the market. Um, but then you get all the good years which take you up to double market.

[00:14:59] Tony: So being positive and being a little bit below market doesn’t worry me at the moment. It’s, it’ll come good. Mm

[00:15:08] Cameron: me either. My super portfolio for the financial year closed up about 1%, so not as good. And again, as I talked about last week, I think the big difference is, and I want to do some analysis on this, but I don’t think I have, just in terms of the volatility of the high ADT stocks in the last couple of years versus the volatility of the lower stocks, um, It looks to me like, you know, the only real difference between my ADT, my super portfolio and the way I manage the other portfolios is the limitation of the ADT and also because there’s been long stretches where I couldn’t, because of the ADT requirements, I couldn’t buy anything, sitting in cash for long stretches because I couldn’t find anything to buy, um, so yeah, that’s where my portfolio results are at closing out the financial year.

[00:16:05] Cameron: Have you done your analysis yet?

[00:16:07] Tony: Yeah, I had a look in ShareSite. So my Superfund, which is the one I track now in terms of performance results, because the stocks that are in our personal names are in and out all the time as we fund our own lifestyles and mortgages and body corporate fees and whatnot, um, but the Superfund, which is hermetically sealed, was up just over 6% So again, it’s, um, the market was up 12.

[00:16:29] Tony: So I’m not proud of it being up 6%, but it’s above water and it’s, um, yeah, it’s within ballpark of market and it’s not going backwards yet. Um, and the most interesting thing is most of that was dividends. Two thirds of that was dividends, 4. 3%. roughly, was because of dividends. So I think the capital gain was only about one point something, 1.

[00:16:50] Tony: 5 percent, and the rest was uh, dividends. So that’s, I guess that underlines for me, because like you, I’m buying high ADT stocks, um, that dividends are important.

[00:17:02] Cameron: I don’t think I’m even including dividends in my super portfolio.

[00:17:05] Tony: Oh, you should.

[00:17:07] Cameron: I don’t think they’re showing up in my transaction. So getting anything out of an AusSuper is just a freaking nightmare, man. Oh, but this is being done by Navexa though. I’m putting the transactions into Navexa. Navexa should be tracking the dividends.

[00:17:20] Cameron: Can I have a look? Yeah. I stopped trying to get any reports out of AusSuper because it was just a nightmare.

[00:17:27] Tony: Well, if it’s anything like Superfunds that I was a member of years ago, like about three months down the track, you’ll get a glossy report as to how good they did for you.

[00:17:36] Cameron: Yeah, but it’s not for the self managed bit. The self managed bit is, you’ve got to do it over their website, and the website’s a dog’s breakfast. Okay, according to Navexa, for my super, capital gain was down 1%. And dividends was up 2%.

[00:17:51] Tony: That’s pretty low. 2 percent

[00:17:53] Cameron: Pretty low. Yeah. I don’t think, I don’t think this is, uh, maybe set up properly.

[00:17:57] Cameron: I’ll have to have a look at how I’ve got this, uh, portfolio set up. I think I’m missing something here.

[00:18:05] Tony: Yeah, I mean, I had 1. 5 percent capital gain and 4. 4 percent dividends, and 4. 4 percent sounds about right because I think the market yields about that, so you should probably be getting the same, I would have thought.

[00:18:17] Cameron: Hmm. I’ll look at my, um, income contributions. Hmm.

[00:18:26] Tony: I think the good thing I’ve been, you know, um, in reviewing the last 12 months, I’m, I’m happy that things have settled down. It was so volatile there up until about six or so, maybe nine months ago, um, that I’ve pretty much got the same stocks I had. Uh, for a long, for like six or nine months now at least, haven’t traded a thing, yeah.

[00:18:48] Cameron: Hmm. Well, we’ve had a few survey results come in from QAV club members. Uh, not many people are actually completing the survey form still. I think we’ve had six. Submissions on the survey form, which is, um, pretty sad. By the way, although most of, there’s a couple of those, uh, average, but most of the people who are emailing me are the people with good returns.

[00:19:09] Cameron: And I just wanna know, I wanna hear from people who haven’t had such a good return, so I don’t feel so bad. Like, everyone who’s emailing me is getting like 20 percent returns for the financial year, and I’m going, come on, like, stop sticking the knife in. Who am I, Julius Caesar on the Ides of March? Like,

[00:19:25] Tony: Well, it makes me feel good to see people have good QAV results.

[00:19:28] Cameron: Well, it’s a mixed bag for me. On one hand, I’m like, well, that’s great, it’s working for you. On the other hand, I’m like Go to hell. Why are you doing so well and I’m not? It’s not fair. It’s not right. Um, so on the poll, we’ve had 10. 43 percent and some of these are CAGR, some of these are time weighted return, so I don’t know which is which.

[00:19:49] Cameron: People didn’t always tell me, but 10. 43, 5. 34, 4. 45 CAGR, 19. 57 according to Stock Doctor, so that’d be time weighted return, I think. Down 4%. And up 2%. Dave from Newey emailed me last week. I touched on it towards the end of the episode, but he says, um, Uh, I run my portfolio on a spreadsheet. I haven’t captured financial year or calendar year numbers as I intend to migrate to share side or similar at some point.

[00:20:23] Cameron: But I injected some new capital in early May this year, so ruled off the books on the original capital. Note the benchmark I refer to below as the AXKOA, what I understand to be the ASX 300 Accumulation Index. I get the numbers off Investing. com and all percentages at CAGR using the calculator site dot com.

[00:20:43] Cameron: My portfolio numbers are expected to be Bence is paid, but don’t include tax impact. Start date 5 2 21, End date 5 5 24, Portfolio 15. 95%, Benchmark 8%. So that’s good. Pretty much spot on, double the benchmark over that roughly three year period. He says, however, I had a brief and wildly unsettling and unsuccessful foray using an alternate approach to QAV for the first few months, and I have stupidly dabbled with a little speculative capital throughout, think lithium.

[00:21:20] Cameron: So if I adjust my starting capital, i. e. I lost money on the alternate approaches and the dates I get, then Start QAV date 12. 4. 21, End date 5. 5. 24, Portfolio 20. 48%, Benchmark 6. 92. So that’s nearly three times the benchmark CAGR over that period. Sensational work, Dave. He says, and if I trim again to start from when I was fully invested with the QAV approach, fully invested date 8 6 21, end date 5 5 24, portfolio 21.

[00:21:56] Cameron: 69%, benchmark 5. 68%. I’m very happy as a customer of QAV. I am grateful I found the podcast. I’d like to thank you and Tony for the excellent work that you do and the energy you bring in week in, week out. I particularly want to congratulate Cameron on his magnificent hairstyle. I think it is a marvel to behold.

[00:22:19] Cameron: Oh, sorry. I’ve just made that bit up. Um,

[00:22:22] Tony: Thank you, Dave. Get your eyes checked, but thank you.

[00:22:26] Cameron: Good job, Dave. Uh, Trent, Sent me an email, uh, Colt, oh no, Facebook maybe, Colt Day in Melbourne, so sitting down to review my financial year results with QAV. I had my best year yet with an 18 percent return, beating market for the first time since starting this journey.

[00:22:42] Cameron: This was the first year I had capital gains, prior years the dividends were required to keep me in the black. Currently hold 16 positions, but have sold 8 over the period, so a bit of turnover, all of which occurred in the last 6 months, with first half no changes in portfolio. That’s interesting, that’s

[00:22:58] Tony: Mmm, it’s the reverse. Yeah, same.

[00:23:00] Cameron: Over the financial year, I’ve held 24 stocks and 15 have positively contributed to overall return. Six of eight positions were sold at profit as share price came down to hit 3PTL. I’ve taken a fudge or broken rules with about half of the stocks I’m currently holding, but trying to track, slash, reflect on these experiments more closely.

[00:23:21] Cameron: Uh, here’s a snapshot of what I currently, uh, he gave me a, sent me a, A picture here, which for some reason has disappeared out of my notes. Um,

[00:23:31] Tony: I can read it out. I’ve got it in mind. So he’s got, uh, FY24 capital gains 11. 81%, dividends 6. 25%, return 18. 06%, FY23 total return 8. 8, FY22 1. 36, per annum 13. 6.

[00:23:50] Cameron: good stuff.

[00:23:51] Tony: Yeah, so well done, Trent.

[00:23:53] Cameron: yeah. And then I asked him what he currently holds, um, because I don’t know, what do you think about this? But I’ve been thinking over the last few days that we should get members, uh, to not just tell us what their returns have been, but also to share with us what they’ve bought and sold, what they’ve traded.

[00:24:15] Cameron: I mean, if I could throw that, if I could gather all of that data, Um, and throw it into, um, ChatGPT. I might be able to build some analysis of, you know, uh, where the differences lie, why the people who did well, what they, what they owned, when they bought it, when they sold it, the people who didn’t do as well, what they owned, what they bought, what they sold it, break them down, slice them and dice them by ADT.

[00:24:45] Cameron: Buy, you know, start dates and end dates or something else, just try to figure out what lessons, like, as we have more and more people doing QAV, following the system, goodly or badly, um, making up their own rules with, you know, how they sell stuff, when they buy stuff, it’d be interesting to try and get all of that data and put it into our I’ll back in so we can analyze it and, um, add it to the mixture of figuring out, well, you know, what, what, what is this person doing that seems to be working so well, uh, in, uh, this financial year period when the rest of us following practically the same system didn’t do as well? Tony’s looking doubtful there, shaking his

[00:25:34] Tony: No, I don’t, I don’t know. I mean, I, I think it’d be great if people gave us the transactions to do the analysis, but I’m wondering whether it’s just, as we’ve been talking about it’s initial states, it’s when did they start, what did they buy? Um, you know, do they buy it on the same day as somebody else?

[00:25:48] Tony: That can be, have a wild impact on returns between people. But yeah, it’d be interesting to know. Uh, what was the most common stock that was held by QAV listeners and how much did that contribute to portfolios or not? That kind of thing. And what can we learn from that perhaps?

[00:26:06] Cameron: Yeah,

[00:26:07] Tony: I’m not looking down for. I think it, I think, you know, it’d be great if people could share it and we could do some analysis on here. It’d be kind of freeform. I’m not sure what we’d be looking for, I guess. Yeah, so it’d be freeform, it’d be like throwing it into the ChatGPT and say, tell us about this data set.

[00:26:28] Cameron: Well, look, you know, as you slice and dice these datasets and you’re looking for correlations, um, you’re looking for, um, some sort of, some sort of evidence to poke its head at. Like, the theory that we have is that it’s, You know, it’s, it’s, we’re all following the roughly the same rules. So if there are differences, it’s just somewhat the luck of the draw when you get in to a particular stock and how it’s buffeted by the volatility of the market at the time, whether or not you get rule one’d out quickly or not.

[00:27:02] Cameron: Like if you happen to buy it when it’s, uh, on an upswing, the beginning of an upswing, um, and you, you will get escape velocity. Yeah, well,

[00:27:13] Tony: Yeah, no, look, I think you’re right. Now I think about it further, and I haven’t thought about this, but, um, you’re right, just looking, um, Trent did share his portfolio, which was nice of him. I’m not going to read it out, but if you, if we did find that, you know, there was a big contributor, and we could see that that big contributor across portfolios that did well had certain characteristics.

[00:27:34] Tony: Like for example, say it’s Fleet Partners and we know that that’s a company which does lots of buybacks, then maybe we would emphasize buybacks in the checklist. It’s not part of the checklist at the moment. So yeah, I can see what you’re saying. It wouldn’t make sense.

[00:27:49] Cameron: I just don’t know, uh, we’d need a consistent way of doing it. Like ideally a consistent template. Like, I don’t want to know how much money people have invested. We’re not looking for volumes, just

[00:28:03] Tony: Why don’t we do this? Why don’t

[00:28:04] Cameron: bought. Sorry, go.

[00:28:06] Tony: why don’t we ask people for the best contributor in their portfolio over the year? Because that’s got a, if we can find some commonality on that and if we can find out a profile of that, that we’re not emphasizing enough in the checklist, that could be helpful.

[00:28:22] Cameron: Hmm.

[00:28:23] Tony: Or best and worst contributors.

[00:28:25] Cameron: Yeah. And when you bought it at what price and when you sold it at what price,

[00:28:31] Tony: Well, they may not have sold it.

[00:28:34] Cameron: if you continue to hold it, that’s great. Yeah. I just think like, you know, big data, man, I’m all about big data. How do we get all the data that we can?

[00:28:42] Tony: Right. Yeah, fair

[00:28:44] Cameron: it for regression testing and, and, and seeing, cause the, the results are all over the place from listeners, but it could be simple.

[00:28:52] Cameron: It could be, there could be something interesting in there. Moving along. That was Trent. Jordan said, um, sent me an email for the financial year. I had a return of 19. 77 percent time weighted return. Congratulations,

[00:29:06] Tony: Very good. Well

[00:29:07] Cameron: um, since inception in November, 2022, I am up. 8. 92 percent versus 9. 51 percent for the ASX 200 time weighted percent.

[00:29:18] Cameron: Over the financial year I’ve held 48 stocks, 19 of which are at a profit or would be a profit if sold, and 29 of which were sold for a loss or would be a loss if sold. The number of stocks held might look high because I doubled my invested capital in March after I’d been using QAV for over a year and was comfortable with the process.

[00:29:38] Cameron: Best performing stocks for the financial year were as below. IRI up 144 percent for the financial year, SXE up 97%, VYS 92%, MAH 62%, WAF 58%, MLX 46%, FPR 37%, MLG 27%, SRV 23%, ASG 17%, still holding onto ASG even though its share prices continue to fall.

[00:30:07] Tony: Your experimental fudge.

[00:30:12] Cameron: MSV15DUR13.

[00:30:15] Tony: I’ve seen that movie before.

[00:30:17] Cameron: Hey, you, you gave me permission to fudge that one. That’s not

[00:30:23] Tony: Ah, right. You’re like a golfer blaming the caddy.

[00:30:27] Cameron: I came to you and asked for a blessing.

[00:30:30] Tony: I just agree with whatever you say, Cam.

[00:30:35] Cameron: Gee, should have married you. Um, that would have made life easier. Um, congratulations. Jordan says, really happy with QAV and how it’s going. Alright, before that, I tried to follow all of the rules religiously, but I did have a couple of stocks with big single day drops, which meant I lost more than 10 percent on them. Really happy with QAV and how it’s going.

[00:30:59] Cameron: Thanks to Tony and yourself for all the great content and teaching. Thank you, Jordan, and, um, Well done to Jordan and Trent, Dave, and everybody who’s had a good year following the rules. Like, jokes, you know, jokes aside, like, I don’t know Jordan’s experience in investing before QAV, but Let’s assume he didn’t have a lot and he’s an amateur like, uh, the rest of us.

[00:31:26] Cameron: To get a 20 percent return for the financial year, um, is, you know, sensational. Trent, 18%, um, uh, Dave, what did he say for the financial year was? Um, No, he doesn’t, but like his overall return over three years, roughly 21, 22%, first triple the benchmark. I mean, that’s, that’s astounding. Like thanks to you and

[00:31:55] Tony: And you.

[00:31:56] Cameron: hairdo to be able to teach, uh, people, uh,

[00:32:01] Tony: Oh, by the way, I should tell the listeners too, Cameron’s recording this on his holiday, so I don’t think you’ve actually had a holiday in five years. We haven’t missed the, you haven’t missed the recording, have you, any week? Maybe one. Not many anyway, so well done. You’re very consistent.

[00:32:17] Cameron: I haven’t had a holiday in 20 years, but yeah,

[00:32:22] Tony: Well, we’ve been to Europe together and we’ve been to the States for various things, etc. But yeah, you don’t take holidays very often, do you?

[00:32:29] Cameron: because I can’t afford to.

[00:32:32] Tony: well done. I appreciate it. I think the listeners appreciate it too. I just want to highlight it,

[00:32:36] Cameron: thanks.

[00:32:37] Tony: than talk about your hairdo.

[00:32:38] Cameron: I’m on my shitty little, uh, portable mic too. Um, Yeah, no, look, I, look, I, I’ve just blown away that we’ve been able to teach people your system, and they’re having that kind of insanely good result, like, it’s, and, like, you know, my super sucks at the moment, but the dummy portfolio, look at that over five years, and, and, you know, I’ve been managing it mostly by myself for, what, four out of the last five years, you were making a lot of the decisions for the first year until I got comfortable with it, and.

[00:33:11] Tony: Till you turned it round.

[00:33:15] Cameron: Yeah. Till I turned it around and then it had a good year. Yeah. Yeah. It’s Like the

[00:33:24] Tony: You said, no more Apollo Tourism. I’m not going to let you buy any more Apollo Tourism and leisure. Give it to me. Hold my beer.

[00:33:38] Cameron: the power of a system that can take mere mortals and just Teach us how to tame the beast. And I know, like, not everybody’s had a good year, and some people might be listening to this going, well, screw you, I’ve had, I’ve had a terrible year. And we feel you, and, and, like, I, I’m sorry that you didn’t have a good year, but neither did Tony and I, really.

[00:33:58] Cameron: Um, and it’s not, yeah, like, as, you know, as we’ve been saying, we think the system just, you know, um, punishes us for being, uh, diligent in following our safety rules. Sometimes.

[00:34:15] Tony: Saves us sometimes too.

[00:34:16] Cameron: yes, they’re there for a good reason. You know, sometimes it, it, it doesn’t look good in the short term, but they’re there to protect you in the long term.

[00:34:26] Cameron: And that’s what this is about is long term

[00:34:28] Tony: Yeah. And look, what I would say is, I think it’s great people are having those results. I think it’s great what, you know, you put together in particular. Um, but the real, the real pride I have is that we’ve told people how to invest. It’s not that they follow QAV or whatever. It’s that they have a framework.

[00:34:47] Tony: They know when to buy and sell. They, they follow it with discipline and doing just that. That is enough to beat the market usually.

[00:34:56] Cameron: and ignore the bullshit.

[00:34:58] Tony: Ignore the bullshit. I mean, we, we wank on about the RBA, but just ignore it. It’s, you know, have a system that ignores it.

[00:35:06] Cameron: We need, we need, we need content.

[00:35:07] Tony: we need content.

[00:35:08] Cameron: something. We’re as bad as Fox News. We need to talk about something.

[00:35:16] Tony: but that’s what I’m proud of, is that people are switching on to the idea of using data, of having a framework and being disciplined. That’s the important thing.

[00:35:24] Cameron: We need to get, we need to get, More merch, so I can take a photo of Chrissy wearing our merch, doing this. This is my new This is my new I’ve got it on my watch. It’s my new thing. Took this photo of Chrissy at the beach for people listening, doing what she calls her leprechaun jump, where she leaps up to the side and clicks her heels with her thumbs up.

[00:35:44] Cameron: And it’s just my, uh

[00:35:46] Tony: She’s incredibly athletic.

[00:35:48] Cameron: It’s my happy picture.

[00:35:49] Tony: Yeah, it’s a great happy picture.

[00:35:51] Cameron: Everything’s good when I see that. Anyway. Alright, Tony, that’s, uh, the, all I’ve got before we get into questions. What have you got for us today?

[00:36:02] Tony: I’ve got a couple of things actually. One of them was a graph I saw on the weekend. I think it was in the Alan Kohler report, the weekly report he does. But he would have taken it from somewhere else. But anyway, it’s a graph of the top 10 percent of stocks by size versus the entire U. S. stock market. So it’s, it’s like, here are the top 10 stocks and how much of the US market.

[00:36:28] Tony: Are they taking up by market cap weighting? Currently, according to this graph and at the end of 2023, it’s 75 percent of the of the indexes in in the top 10 stocks. It’s only ever been at that or above that once before. 1929 on the eve of the Great Depression, and it got close to that 2000 at the top of the.com.com bubble.

[00:36:55] Tony: It got to like about 73%. So I hate to be the bearer of bad news, but if that’s a predictor, we’re not in for a good future. Um, there’s too much concentration in the Tech of Magnificent seven at the top of the US market and, and because of that by all the index funds which have to buy into the US market, which are basically buying those top 10 stocks.

[00:37:18] Cameron: yeah. So, I mean, what does that mean, Tony?

[00:37:24] Tony: I think it means there will be a regression to the mean and we’ll see, um, you know, what, what happened after 29 and after 2000, there’ll be some kind of, there’ll be some kind of reckoning for those stocks, um, unfortunately, because there’s so much more, I’ve had this debate with people, is there more index funds around now?

[00:37:45] Tony: There’s more index ETFs, but there were managed funds that tracked the index a while ago as well. So, but I think there is more people blindly trusting index ETFs. They’re the ones who are going to have to turn the noise off, I think, in the next couple of years, because I think that Magnificent 7 can’t keep going up the way it has.

[00:38:01] Tony: I mean, uh, NVIDIA, I think, dropped about 12 percent last week, um, and that’s what’s going to happen. These stocks are very toppy, um, and they hold up so much market cap that, um, if you’re invested in them, might be time to take some money off the table. And I think that’s what’s happening. That’s one of the reasons why I think NVIDIA went down last week.

[00:38:19] Tony: People are just sort of saying, that’s a good run. I’m going to sit out this for a while.

[00:38:24] Cameron: Well, it went down, but it’s gone back up. You know, it’s, yeah, I mean, it’s not exactly where, back to where it was last week, but it’s not far off it. And if you look at it for the last year, like in last year, it’s gone from 47 to 123. I mean, it’s, it’s

[00:38:42] Tony: To the moon.

[00:38:44] Cameron: Yeah.

[00:38:46] Tony: That’s a good movie. Dumb. I recommend Dumb Money to people to go and watch it. It’s good.

[00:38:50] Cameron: Yeah.

[00:38:52] Tony: And the reason why I recommend it is because it’s what I said before. It’s like all these people who don’t know what they’re doing or investing in the stock market. They’re suddenly sitting on sometimes a million dollar fortunes and they don’t know when to sell.

[00:39:04] Cameron: Yeah,

[00:39:06] Tony: Anyway, yeah, so I don’t know. I can’t predict what’s going to happen. This, this graph caught my attention. Clearly, I think the U. S. stock market is in a bubble. Whether that means it goes up from here, goes sideways from here, or goes down from here, at some stage it’s got to regress to the mean.

[00:39:22] Cameron: Mm. I mean, if history is any, um, guide, right?

[00:39:28] Tony: Well, I mean, just look, take the logic to its extreme. If it follows the curve, the top 10 stocks are going to hold 100 percent of the U. S. stock market. Market Cap, and that just can’t happen because there are a lot more stocks on the market. I mean, it could happen, I suppose, but it means everybody sells out of every other stock.

[00:39:46] Tony: GE, Coke, you know, all the FedEx, all the big stocks on the stock market, and to buy into these things, and I can’t see that happening.

[00:39:56] Cameron: Mm mm Okay.

[00:39:58] Tony: So that was that. Um, there’s been a lot of news, a lot of buy sticks, buy stocks in the news in the last little while. I didn’t get a chance to cover some of this last week, so Apologies if some of this is a bit, getting a bit old, but I wanted just to quickly run through three or four, maybe a bit more of the stocks that are on, on our buy list from time to time and are now in the news.

[00:40:18] Tony: So, because people might hold them or they might be trying to decide what to do. So, uh, Myer was, um, big in the news recently. Um, and, uh, they have a new, Uh, Executive Chairman, even though she’s a woman, uh, Olivia Worth, uh, and looks like Solomon Liu’s finally getting what he always wanted, the big brass ring, which was to take over control of Myer.

[00:40:44] Tony: So he is, um, He’s proposing to merge a lot of the current apparel brands that are in his separate, another separate company he runs called Premier Investments, and that’s separately listed on the ASX, and merge them with Myer. And so that would, Myer are going to do that by issuing a lot more shares and giving them to Premier Investment shareholders, and then taking those brands like Just Jeans and JJs off their hands.

[00:41:12] Tony: The market loved it. The Myer stock rose 20%. And interestingly enough, the Premier Investments did as well. So Myer’s now sitting at 81 cents. Um, when it’s been probably as low as in the fifties, I think during the year, it’s been on the buy list for a while. Um, we’re now starting to, that was the announcement, we’re now starting to understand more of what’s going on.

[00:41:36] Tony: And, um, This article was in the Fin Review from June 25, uh, it’s talking about Solomon Lew joining the board. So, Premier Investments already holds two seats because Mr. Lew already holds a fair stake of Myer’s shares, but he’s going to, um, Join the other two people on the board. Uh, Olivia Wirth joined the, uh, Myer board in March from Qantas, where she was head of loyalty.

[00:42:06] Tony: Um, so that’s an important point, I think, because one of the, one of the benefits that the analysts are seeing in this merger is that companies like JustJeans and, um, The other ones that are part of the Premier stable are going to get access to the MyerOne loyalty base and get a loyalty program, which will have some impact on their sales, I would think.

[00:42:29] Tony: This article goes on, the enlarged group will have about 4 billion in annual sales and more than 200 million in earnings. The deal was likely to delay the spin off of Mr. Lew’s larger Smiggle and Peter Alexandra brands, which was being explored by the billionaire retailers. Premier had said they were looking at whether they should spin off their two growth brands, Smigel and Peter Alexander, um, leading all of the other parts of, uh, Premier listed separately.

[00:42:55] Tony: Uh, MST Marquis analyst Craig Wulford estimates the Myer apparel brands deal offers synergies of 55 million and leaves the high growth businesses, Peter Alexander and Smigel, sitting inside Premier. Uh, Myer have done all the hard work for the Premier’s strategic review, he said. Myer shareholders will be significantly diluted in a transaction, but the combined entity will have double the earnings and have the opportunity of potential synergies and the chance to reinvigorate growth.

[00:43:26] Tony: So he’s saying you are going to be diluted, but he thinks that you’re going to have that made up for you by increasing profitability. Another analyst, Ben Gilbert, Head of Australian Research at Chardon, estimated that Premier shareholders could end up owning about 70 percent of Myer and flag significant synergies by leveraging Premier’s sourcing and rolling out apparel brands within Myer stores.

[00:43:51] Tony: Greater scale would provide scope to cut store space more quickly, while reducing overheads, including rent. Mr Gilbert said a combined larger group could also leverage the Myer One loyalty scheme, one of the largest in the market, with Premier not having an equivalent program in place. Uh, uh, Another person, Unified Capital Analysts, said a potential merger could result in a leaner, more fit retailer, I guess they mean fitter retailer, able to take advantage of loyalty.

[00:44:20] Tony: They estimated that Premier could unlock about 40 million of synergies driven by a smaller footprint of stores and higher Myer gross margins, which would boost earnings per share by 30%. This would arrive at a low point in the cycle that would also see Myer emerge as With a 1 billion plus market cap and index inclusion, they said.

[00:44:39] Tony: And then lastly, Angus Aitken of Aitken Mount told his wealthy clients, not the, not the ones who can’t rub two cents together, but told his wealthy clients they should buy both Myer and Premier shares. We think you buy both stocks, this is what Aitken says. We like Olivia Wirth and think she is a winner at Myer.

[00:44:57] Tony: They can triple from here over time. The press suggests she doesn’t have enough retailing experience, but that’s complete rubbish, he said. After gaining 20 percent on Monday, Myer’s shares advanced 5. 8 percent to 82 cents on Tuesday. Premier shares were 1. 9 percent higher. So, I mean, we’ve talked about this before.

[00:45:18] Tony: Um, Solly Lew is long coveted, uh, getting back into control of Myer and now it appears why because he wants to merge his other apparel brands in there, reap economies of scale and you know, take best, best of practice sourcing across all those brands and put it into the combined group. So it seems like a good deal.

[00:45:38] Tony: Um, Myer shareholders might be worried about dilution, but all the analysts seems to think there’s more upside in, Profit from the merger than, um, than not. So, um, they don’t seem to be worried about shareholder dilution in Myer. So that’s Myer. Um, another, um, Buy list, stock, which was in the news, uh, this is going back again a week or so, June 17. Uh, this is our old friend Twiggy at Fortescue Metals Group, and the article, uh, is, uh, the headline is Monster 1. 1 billion block trade in Fortescue. An institutional investor pressed sell on a 1.

[00:46:16] Tony: 1 billion stake in Andrew Forrest’s Fortescue after Monday’s closing bell, sending out JP Morgan to find buyers on its behalf. The shares were being offered at 21. 60 apiece, and the parcel represented 1. 6 percent of the company. The sell down comes after Fortescue’s share price has dipped 21. 8 percent year to date amid a slump in iron ore prices as China’s stimulus to revive construction has failed to boost steel demand.

[00:46:46] Tony: Meanwhile, the conga line of executors filtering out of its top ranks has continued. Earlier this month, Julie Shuttleworth, a trusted forest attendant for a decade, And one time Deputy Chief Executive Officer resigned. Lastly, his departures included long time, long serving Chief Financial Officer and former Reserve Bank of Australia Deputy Governor Guy DeBelle, who lasted just five months as CFO of the Green Energy Division, and he has several, and severed his final links to Fortescue last September.

[00:47:15] Tony: So we’ve talked about this one before. I think it is a red flag that all these quality people are leaving. Fortescue, um, I think perhaps some of the instos are seeing that now too, share prices down by the odd percent this year, admittedly because the iron ore price is down, but again, I think the playbook in this situation that I’ve seen before is when the quality people leave, it’s the red flag, and um, I think I wouldn’t be surprised, maybe not in the short term, but maybe this half or next half they come out with some kind of profit downgrade because they just don’t have the quality of management that they had running things.

[00:47:54] Tony: So, but we’ll see. So that’s my opinion on FMG. Uh, I feel like that guy in the meme who sits there with the chair and the lemonade stand saying, This is my opinion, convince me I’m wrong. Five cents. Come along and debate me. But anyway. Uh, Competition Fears tie up Namoy Cotton Bid. So we haven’t done a Pulled Pork on Namoy, I don’t think yet.

[00:48:17] Tony: It’s been on my list, but um, I have avoided it because it’s in play. Um, and this is a, an article which says that, uh, Namoy Cotton’s share price plunged after a takeover bid from Singapore based O Lan, registered three red lights with the competition regulator, New South Wales, and New South Wales farmers said that members had concerns about any change of control.

[00:48:38] Tony: Namoy stock fell almost 8 percent to 64 cents in trading yesterday. Before recovering close to 4. 3%, uh, down to 66. 5 cents. OLAM and rival suitor French agribusiness giant Louis Dreyfus are facing major hurdles gaining takeover approval from the ACC. The ACC said it was concerned an OLAM offer, uh, of the oper takeover of the operator of the country’s largest network of cotton gins would reduce competition.

[00:49:08] Tony: ACC Commissioner Stephen Ridgeway told the Australian Financial Review that if neither OLAM nor Louis Dreyfus was able to overcome competition concerns, the takeover battle for Namoy could all fall over. So this stock is up. It’s on our buy list, but it is being held up by potential takeover activity.

[00:49:27] Tony: So I’m just going to make people aware of that if they’re thinking about buying into Namoy now. Just, um, you know, do a bit of a Google search and see where the takeover bids are at because, um, you can go backwards just as quickly as you go forwards in a takeover bid situation. It’s in play.

[00:49:45] Cameron: What’s the code for NAMI? I’m

[00:49:47] Tony: Uh, good question.

[00:49:48] Tony: NIM, I think. I’ll just confirm that for you.

[00:49:51] Cameron: just going to add it to my notes of things to be careful of in my buy list.

[00:49:57] Tony: Yes, it is NAM Nam Nam Saga. I’m only back in Saga Uh, two more. Um, this one is a interview with, uh, the, uh, fund manager for one of, uh, Jeff Wilson’s Wilson Asset Management Stable of funds. Might even be wham, I think. Yes, he is. Uh, so Oscar Oberg is the lead portfolio manager of Wilson Asset Management’s Capital Fund. It’s got $5 million in assets and he was going through his.

[00:50:34] Tony: Tips, and the headline is Wilson’s Oberg tips 50 percent upside in small cap stock, and the stock he’s tipped is GA Education, which was a pulled pork a couple of weeks ago. Um, it’s a childcare centre, uh, with a long history. GA Education is Australia’s largest childcare operator with over 400 centres.

[00:50:54] Tony: This is, um, Oberg speaking. Historically, it has struggled with negative earnings per share revisions and debt issues over the last decade, which culminated in the capital raising in 2020 through COVID. Our interests, so Oberg’s interest and WAM’s interest. Our interest was sparked last year after the appointment of GH’s new Chief Executive from Big W, Pedgeman, Okavatt.

[00:51:17] Tony: Okavatt’s strategy is relatively straightforward. Boost occupancy, stabilize costs, and divest underperforming centers. With G8 having a very strong balance sheet, we also think the business could easily buy back 5 10 percent of the shares on issue. Putting this all together, we think the strategy can allow G8 to achieve 10 15 percent organic earnings per share growth each year, Over the next five years, G8’s valuation of 12 times on a 12 month forward P.

[00:51:43] Tony: E. is cheap, and we think the strong level of organic growth can allow the share price to re rate higher. We see 50 percent upside in the share price in the next 12 to 24 months, and for these reasons G8 is a large weighting in the portfolio. So I thought that was interesting that QAV and the professional fundee both came to a similar conclusion on G8.

[00:52:06] Cameron: Is this the one where we talked about the, uh, interesting, uh, history of the

[00:52:13] Tony: No, that was the competitor. So the executive who had been an executive of G8 went across and is now setting up a company in opposition to it. Uh, he used to run G8, um, and did a good job of it, uh, until the, until COVID came along and there was an issue with, um, you know, with many companies at the time, but certainly the company that was, um, rolling up childcare centers. And the last one I’ll talk about quickly is, uh, Headline, Check Bid for AX Miner Collapses, and this is about Coronado Global Resources. Billionaire Czech businessman Pavel Tikacs, out of money bid to take control of ASX listed coal miner Coronado Global Resources, has collapsed after his family office has SEV.

[00:52:59] Tony: N, SEVN. SEVN Global Investments failed to secure Foreign Investment Review Board approval in time. The Queensland and U. S. coking coal producer is trading at a 30 percent discount to when SEVN agreed to the 1. 5 billion deal on September 26. SEVN had agreed to buy 51 percent of Coronado from Energy and Minerals Group, a Houston private equity firm that floated the miner on the ASX in 2018.

[00:53:25] Tony: SEVN. It has remained a major shareholder. So again, um, you know, this, this idea of, um, it’s been in play. They couldn’t get, uh, Foreign Investment Review Board approval and the share price has gone down. I have noticed that CRN, that’s the code, has gone up again. Um, so I don’t know if that’s a sign that people think it’s dropped enough that it’s worth buying or that there might be some other M& A

[00:53:53] Tony: But again, just highlighting that for people to be careful with M& A, companies that are in play when you’re buying things on the buy list. Because what we found, this is what, three or four companies, um, that institutions often have the same playbook we do and they see value in the same stocks we do. Um, but I don’t like buying into a takeover situation because it can, it can go up, but it can go down.

[00:54:15] Tony: And I think it’s a special skill set in trading takeovers, which I don’t profess to have.

[00:54:21] Cameron: But if we own them when they go into play, it’s often a good

[00:54:25] Tony: Great. It’s a great thing. Yeah.

[00:54:27] Cameron: Yeah.

[00:54:28] Tony: Yeah. Okay. So that’s my news. And the last thing I’ve got to talk about is a pulled pork.

[00:54:34] Cameron: Who are you pulling for us today, Tony?

[00:54:36] Tony: AWJ, Auric Mining, A U R I C. So

[00:54:40] Cameron: yeah.

[00:54:42] Tony: Auric, does that ring a bell for you? Yeah, gold miner. Yes. Welcome to Amsterdam, Richter Bond. Auric Goldfinger. Auric was the first name of Goldfinger in the Bond book and film. It’s the first thing I thought of when I

[00:54:57] Cameron: I was gonna say, um, one of the third Doctor’s companions, uh, fifth Doctor’s, but I think that was Adric. Not Auric, that was Adric. Yeah.

[00:55:07] Tony: Yeah, so Auric I think is some kind of Latin for gold, maybe. Anyway, yes, uh, so I, I, I, I like doing this pulled pork, doing the research for it, it’s, um, it’s, I’m not familiar with the company, it’s, uh, only, I guess it’s been around for four or five years on the ASX, but it’s, um, uh, never made money, so it hasn’t been on our buy list, it hasn’t been on my radar, and it’s fairly small.

[00:55:31] Tony: Uh, it’s, uh, it’s a WA based gold explorer and developer, uh, they’re centered on the, uh, Wigi Mutha. Norseman Gold District in WA. Certainly Norseman I’ve heard of. I hadn’t heard of Widgey Mortha, but it’s a gold district in WA. They have a couple of existing mines and they have lots of exploration licenses.

[00:55:52] Tony: In the Widgey Mortha district, this company has two mines, Mundergold and Jeffreys Find. So, uh, Two particular gold mines. One has produced some gold, which is why they have positive operating cash flow. They sold some gold, but I wanted to just read from a summary of the company rather than go on about it myself.

[00:56:15] Tony: This is from an analyst, uh, by the name of Canary Capital. I haven’t heard of them, um, but, uh, and this is a small company, so it doesn’t have many people, um, reviewing it, but, um, or analyzing it. But this is a couple of things I wanted to call out. It was a good summary. So, uh, under the heading key achievements to date, uh, remarkably progress, progress from tenement acquisition to being listed on the ASX to mining and generating cash in under three years.

[00:56:42] Tony: AWJ banked 4. 77 million in cash from Stage 1 of the Jefferies Fine Gold Project, where 9, 741 ounces of gold were mined and sold. And then the last thing is, completed a scoping study that proved the strong economic viability of the Munda Gold Project and a conservative path to generating 77 million in cash profits.

[00:57:06] Tony: So, uh, I’ll go on, it’s worth, um, highlighting what they’ve said. A scoping study announced to the market on Monday in June 2023 outlined exceptional economics with a projected positive cash flow of 76. 9 million over a 13 quarter mine life based on a conservative gold price assumption of Australian 2, 600 per ounce.

[00:57:28] Tony: The potential surface cash flows are substantially higher at current gold prices around 3, 200 Uh, based on a scoping study, AWJ will commence operations at Munda with a starter pit with a mine life of three months and a low capital investment of 1. 3 million. The starter spit will also, the starter pit.

[00:57:49] Tony: Sorry, will also require a working capital investment of approximately 6 million and is expected to produce 8. 7 million in surplus cash. These numbers may change based on results from the current grade of gold. During the past six months, the focus has been on production from Jefferies Fine Gold Mine under a joint venture with BML Ventures.

[00:58:11] Tony: and Experienced Mining Contractor. Stage 1 of the project is now complete and 9, 741 ounces were produced. AWJ has now received 3 cash surplus payments totaling 4. 8 million from Jeffrey’s Fund. The cash is expected to sufficiently fund AWJ during 2024 while Stage 2 is being developed. Stage 2 is expected to generate between 6 and 8 million in cash for AWJ based upon a gold price of 3, 050 per ounce.

[00:58:40] Tony: Despite the significant cash flow potential of the company’s projects, the current market cap is just 20. 3 million. We view this as presenting investors with an opportunity to invest in AWJ at a fraction of the real intrinsic value of the company. With its projects either operational or about to come online, no debt, and no risk.

[00:58:59] Tony: Upcoming catalysts and a strong management team, the company offers a compelling investment case with significant upside. AWJ is our preferred ASX listed company. So that’s, um, Canary Capital’s take on it. What I really liked about it, and I hadn’t seen this done, Before, at least to this extent, is they haven’t gone out and raised a lot of capital or borrowed lots of money to get some gold out of the ground.

[00:59:22] Tony: They’ve just said we’ll take a little bit, we’ll mine a little bit, we’ll sell it, we’ll do rinse and repeat, do it again with a bigger amount of gold this time, sell it, rinse and repeat, and just keep expanding through, you know, organic Processing of what we have underground. And I think that’s a terrific sort of flywheel, um, way of managing cashflow.

[00:59:45] Tony: Um, that’s possibly happening. I don’t, I can’t, I don’t know if I can contribute it to this person, but a real positive for the stock anyway, is the involvement of Mark English, uh, who was the founding director of a company called Bullion Minerals that went into, uh, onto IPO. There’s two companies, one called Chalice Goldmines and the other called Lionstown Resources, which people may have heard of.

[01:00:09] Tony: Two successful listings in the mining sector. And this person, Mark English, still holds 6 percent and other management hold a lot too. So it scores a one on our checklist for owner. Founder, owner, founder, which is a good thing. I’m going to go through the numbers. That was a good summary from Canary Capital of the company.

[01:00:33] Tony: Uh, this, the ADT for this stock is 109, 000 per day. So it’s going to suit a lot of people listening. It’s not a huge stock. The market cap’s million, but there seems to be a fair bit of, um, trade in it. I’m doing the analysis on a share price of 19 cents, and I think Today, last time I looked before we came on air, it was trading at 20 cents, so it’s gone up a little bit.

[01:00:55] Tony: Uh, this is a small cap stock, um, I’ve never heard of Canary Capital, but they were one of the only analysts covering it. Uh, so we’re getting no consensus target for the stock price, which is something I like, so that’s a good thing. Uh, we have, the company has no yield, which is to be expected because it’s in growth mode.

[01:01:12] Tony: Uh, the price of 0. 19 though, however, is way above IV1 of 0. 05. We don’t have IV2 because we don’t have a, um, a forecast EPS to base it on. Uh, the company has, uh, strong financial health in Stock Doctor. And the Stock Doctor financial health trend is recovering, which is something we score doubly in the checklist.

[01:01:32] Tony: I like to see that. And I think the reason why it’s, it’s getting a recovering score is because this is the first half where we have positive operating cash flow. And I haven’t done the regression testing, but anecdotally I’ve seen that when a company transits to positive operating cash flow, it can be a catalyst for a re rating of the stock.

[01:01:51] Tony: And that’s something I like to see. Um, just, uh, I guess anecdotally, I haven’t worked out how to put it into the checklist yet or how to gather the data, but it’s, uh, it’s, I think it’s probably a net positive. Uh, P for this company is 18. 9 times, so it’s not bad. Not low, uh, but it’s the first PE because they haven’t had positive cash flow before, so we can’t score it.

[01:02:13] Tony: We leave that one blank. Uh, PropCaf is 6. 68 times, so it’s getting up to our seven cutoff. It’s just below it at the moment, and so it scores on that basis. Net equity per share is 8, 000. Cents and the share price is 19. So we can’t, we certainly can’t buy this for that, uh, asset value or book value plus 30, uh, we can’t score it for growth because, um, there’s no, uh, forecast earnings per share growth.

[01:02:40] Tony: So I can’t put growth over pe as I said before, directors are holding 16% of the company, so that’s great. Uh, it’s a recent three point uptrend, so we score it for that. It doesn’t have consistently increasing equity because it’s really only adding to equity now. Um, so we can’t score it for that. But of the things we can score, it’s 10 out of 12 items or 83%, which is a good quality score, and a QAV score of 0.

[01:03:05] Tony: 12. So, um, from what I’ve seen in my limited research of the company, I really like it. I think it’s a great business model to, um, to, um, You know, um, fund a little bit, dig some gold, sell it, fund a bit more, dig some more, sell it, etc., and rinse and repeat. Um, and it’s got a very, um, experienced management team behind it, so I think this one’s worth looking at, people.

[01:03:29] Tony: Have a look.

[01:03:30] Cameron: Very conservative model for a

[01:03:33] Tony: Yeah, it is, isn’t it? Rather than going and raising lots of money and, um, and taking pot luck on your tenements. So, it’s good.

[01:03:41] Cameron: AWJ. We don’t own it in any of our portfolios. So there you go.

[01:03:48] Tony: Maybe we should. We’ll see. And look, there’s still, it’s a small company, there’s still a lot that can go wrong. I didn’t really, um, itemize the pluses and minuses for this one. The minus is that, uh, they’ve got to keep finding new tenements because the, of the mines they’ve got, they look like they’ve only got about three years mine life.

[01:04:07] Tony: So, um, even though it’s a great flywheel approach to expenditure and using the cash flow to Dig more and sell more. Um, and they’ve certainly got lots of licenses and tenements up their sleeve. They’ve still got to keep striking gold to keep expanding.

[01:04:24] Cameron: Yeah. All right. Thank you, Tony. Well, let’s get into questions. We’ve got a couple this week. First one’s from Toby. This is a leftover from last week. Thoughts on the impact of new tax rates may or may not have on personal and super fund investors. Also, we know you’ve mentioned about no buying on market down days, exceptional cases where you have companies you want to buy that are in fact rising on that day.

[01:04:51] Cameron: I’m not trying to foster risky behavior like buying KSL the other day when they announced they’d been defrauded of about 10 percent of their half year earnings. I did balance up my holding on the news, but it just got me thinking about the qualification of market versus a particular company.

[01:05:08] Tony: Yeah, look, it’s a good question. take the first one first, he asked about the impact on Investments for the new tax rates. I don’t think there’s much. I did some back of the envelope numbers. I think we are getting a tax benefit of roughly 2%, depending on your, your income. This is basically due to, well, I mean, to give some history to it.

[01:05:36] Tony: Governments, um, don’t link the tax brackets to CPI, so over time, people, people’s wages go up and they pay more tax as they move into higher tax brackets. Um, and then governments, um, say, look, look how good we are, we’re going to cut taxes for you. And they, they change the brackets and, um, they really should have been adjusted along the way.

[01:05:55] Tony: But anyway, this latest change, um, in, in addressing bracket creep looks like it’s about a net 2 percent benefit, um, it depends on, again, how much you’re earning. And that’s the approximate number. Um, so some of the brackets are being reduced, like the top ti top, uh, or sorry, being increased. Um, so the top marginal tax rate cuts in now at 190, 000 income, where it used to be 180, 000 income.

[01:06:21] Tony: Um, and then the rates on some of the lower brackets have been lowered because originally this, this, what was 3 tax cuts were put in Third phase of tax cuts when the previous government gave stage one and stage two tax cuts to the lower brackets. They wanted stage three just to be a raise in the cut off the highest taxing bracket which would be a tax return benefit to people on high incomes.

[01:06:48] Tony: The current government said that’s not fair and they spread it a bit more evenly across all brackets. Anyway, it’s um, I think its impact is going to be marginal. A couple of things to note I guess is that when the tax The tax take goes down if you’re negatively gearing things. It may mean you get less back as a rebate, but again, it’s probably only going to be 2%, um, or thereabouts.

[01:07:12] Tony: And it also means if you’re, for example, if you have dividends being paid into, um, superannuation funds, where you generally get a cash rebate. Because the franking credit exceeds the tax payable by the Superfund, um, then you’ll get a couple of percentage points increase in that. So it does make it a little bit more beneficial to have dividends being paid, or investing in SMSFs and getting them paid into Superfunds.

[01:07:40] Tony: But, um, You know, it’s a good thing that they did it to address Bracket Creek, but it’s a marginal sort of result, I think, for investors in this one. Second question about whether we buy on down days or up days. Um, I don’t know where we got to in the Bible on that one. I went and had a look and couldn’t see it.

[01:07:59] Tony: But I mean, as a rule of thumb, I don’t like buying a stock when it’s going down. So if it’s going down on the day, I don’t buy it. I’ll wait and see if that’s the start of a trend. Um, I don’t think I was strict on whether the market’s having an up or down day. But yeah, certainly I wouldn’t buy something if it was going down on that particular day, just in case it’s like a KSL and they come out and announce some bad news and the stock price keeps going down.

[01:08:25] Tony: So that’s my take on that.

[01:08:29] Cameron: Yeah, for what it’s worth, I’ve never paid attention to whether or not the market is having a down day. It’s just whether a particular stock is having a down day, then I will not buy it because I might be able to buy it for less tomorrow.

[01:08:45] Tony: That’s my recollection of what I do, but because I haven’t bought anything for a while, I had to sit there and think, hang on, what’s my process?

[01:08:54] Cameron: that’s my understanding of the rules, Toby, for what it’s worth. Thank you, Toby. Thank you, Tony. James, only other question we’ve got today. Um, what does a notice of cessation of securities mean? And what are the implications for shareholders? Looks to me like there were shares on offer to management based on performance, but management failed to hit their targets.

[01:09:17] Cameron: What happens now to those shares that would have been given to management? And he’s got a table here from some company and it says, security description, performance rights, FY24, short term, numbers of securities that have ceased, 17, 695. The securities have ceased due to lapse of conditional right to securities because the conditions have not been or have become incapable of being satisfied, date of cessation 28 of the 6th, 2024.

[01:09:47] Tony: yeah, so it’s not something I pay attention to, um, generally management rights are not a huge component of a large cap stock’s shares, um, it’s different I think if it’s a startup where, you know, management are taking lots of equity in the company and it can be performance based, um, but, you know, what’s happening in a nutshell is that as part of management’s Compensation and trying to align them to shareholders and their interests.

[01:10:14] Tony: They, uh, get paid a long, usually these are long-term incentives, um, and they can get paid out and given to management or they can lapse. Um, I, I did sort of go down the rabbit hole on the accounting for all this, and it’s, it’s. You know, there was pages and pages and pages of it. Um, I think, I think a couple of points to make rather than outlining the accounting for it at the moment is, Um, it could be a bad sign if large numbers of securities are being cancelled because that means that the company hasn’t performed well enough for management to get there.

[01:10:47] Tony: Long term incentives, but I think if that’s the case, we’re picking it up in other elements of the QAV checklist and in sentiment, um, rather than focusing on this particular area. Um, the other point I want to make is that it’s not unusual for management not to make 100 percent of target every year. So it’s not unusual to see the cancelling of Longer term incentives because management may have only made 50 percent of target or 70 percent of target.

[01:11:14] Tony: It’s unusual for management to continue to get 100 percent of target. That’s poor target setting, I think, on the behalf of the board if it’s not stretching management enough in that case. So it’s not surprising to see Uh, cancel performance rights, um, and the other thing to note is that I think this might be just swings and roundabouts because every year, um, companies have to put aside shares in case management achieve their performance, um, entitlements and then give them the shares out.

[01:11:43] Tony: So, they’re kind of cancelling but issuing shares.

[01:11:50] Tony: So just to take one particular snapshot in time isn’t providing a good picture. If you do want to look at the accounting of it, I think the basic principles are that when the company enters into this kind of performance rights contract with a manager, they need to provide, their best guess for what that’s going to cost in their, um, in their P& L and their balance sheet.

[01:12:11] Tony: So, you know, back in the day when everyone got paid options, which isn’t as common now, it tends to be performance rights to shares. They use the Black Scholes method and they say that, you know, we think these options are now worth this. And every year they would adjust the value of the options as they got closer to expiry.

[01:12:27] Tony: And the value either went up if it was likely that they were going to have to be exercised, or they went down if they were out of the money. And so the board would adjust the balance sheet. of the company to say, if Joe Bloggs, who’s, who’s, or Susan Bloggs, who’s the CEO, meets their performance hurdles, we have to pay for these new shares to be issued to them.

[01:12:48] Tony: And that’s still going on now, but like I say, it tends to be a provision in the balance sheet. It’s based on the assessment of whether they’re going to pay out or not, and by pay out I mean, issue new shares and give them to the manager. Um, but it tends to be a bit of a revolving line because, um, yeah, this year they may not give the shares out, but next year they might.

[01:13:08] Tony: So, it’s constantly being adjusted based on new targets which are being set every year as well.

[01:13:15] Cameron: Right, just ignore it.

[01:13:18] Tony: I’ve always ignored it. Like I said, it might be more germane to a very small tech company that was giving out lots of these things. Um, uh, because it might dilute you when they, if they had a good year and they had to pay out all these shares, and it might actually do better for you if they cancelled all these shares because you’re getting, it’s like a buyback, you’re getting more of the company.

[01:13:36] Tony: But, generally, like for a large cap company. company or a company with a large ADT. It’s playing around the edges, I think. It’s a bit like dividends. You know, companies will have to buy shares or issue shares to pay for dividend reinvestment plans, which is usually just a couple of percentage points at the most around the shares on issue for companies every half.

[01:13:59] Cameron: Thank you, Tony. Thank you for the question, uh, James. That’s it. We’re into after hours, Tony. What have you been after hoursing?

[01:14:10] Tony: Well, happy birthday to Ruddy. It was his birthday yesterday. He’s a good, good

[01:14:15] Cameron: him a happy birthday

[01:14:16] Tony: on the, on the 1st of July, first day of the financial year. And the funny thing is I know three people who would have a birthday on the 1st of July. And I can’t think of any other date where I know three people that share a birthday on that day.

[01:14:30] Tony: So, you know, was there a thing, was there an incentive for hospitals or doctors or mothers to push their births into the new financial year for tax reasons at some stage?

[01:14:40] Cameron: 65 years ago.

[01:14:41] Tony: yeah, back in the 50s or 60s, I don’t know.

[01:14:45] Cameron: And you weren’t down celebrating in Wagga with Ruddy.

[01:14:50] Tony: I’m not. No, I have to get down there at some stage soon, but not this week.

[01:14:54] Cameron: Taylor, Taylor called me yesterday and said, Hey, FYI, it’s Ruddy’s birthday today. I was like, well, Tony’s not down there. What’s Ruddy

[01:15:01] Tony: Ha ha ha ha

[01:15:03] Cameron: I don’t understand how Ruddy celebrates anything without you there.

[01:15:06] Tony: Well, his brother in law has just moved back from Canberra, so he told me he was out playing golf with him. So he’s found a new, uh, a new golfing buddy to celebrate with. I’ve been replaced.

[01:15:16] Cameron: that’s good. You’ve been dumped.

[01:15:19] Tony: yeah, a couple of, uh, I watched Furiosa, rented Furiosa, wasted 29 bucks on it, uh, the You Mad Max prequel, um, wanted to like it, look it’s not a bad movie, it’s, um, it’s, um, is it Anna, Tail Your Joy, the lady from Red Queen, stars in it, and she did well, but it’s a tough ass to play a young Charlize Theron, unless you’re Charlize Theron,

[01:15:42] Cameron: the Queen’s Gambit. That would

[01:15:44] Tony: Queens Gambit, sorry, there you go, yeah, um, yeah, but she was okay.

[01:15:48] Tony: But it was just, uh, Chris Hemsworth spoiled it for me. He basically played his Thor love and thunder role again and tried to play it for light giggles and it just, just didn’t come off. He’s not a