Hello QAVvers

She keeps no, she keeps no

She keeps no secrets from you

“No Secrets”, by The Angels, talking, of course, about how Tony (who they mysteriously refer to as “she” to disguise his identity, and who had The Angels play at his 60th birthday party last year) keeps no secrets from us about how to invest. I heard from one QAV Club member this morning who said “Also just a bit of portfolio update for last 12 months, up 17.5% atm thankyou very much and much better than the previous 12, not possible without QAV wisdom.”

Happy Birthday to TK, too, he turned 61 last week.

The AORD slipped a little last week but is still going relatively strong.

Let’s have a look at the portfolios.

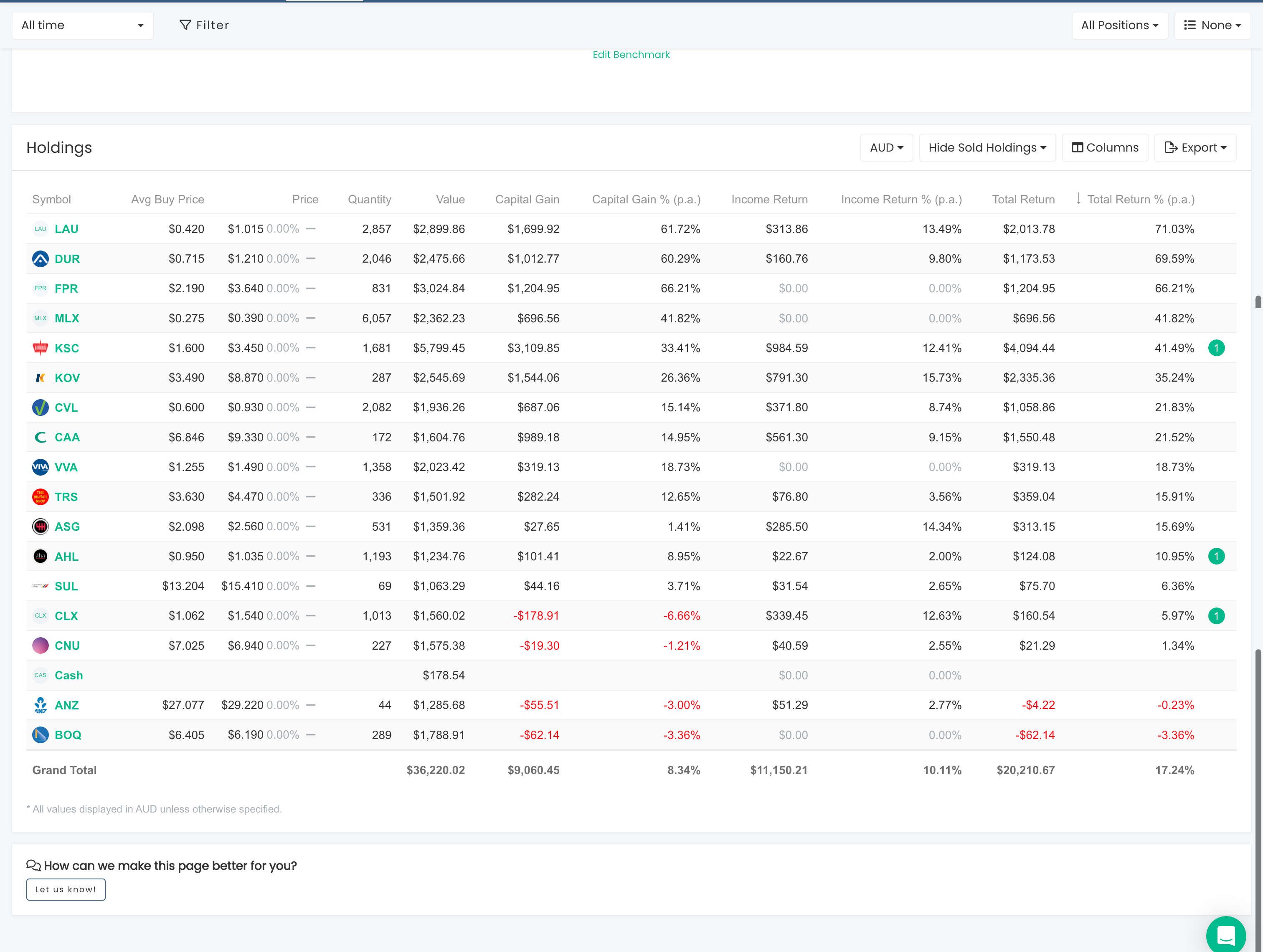

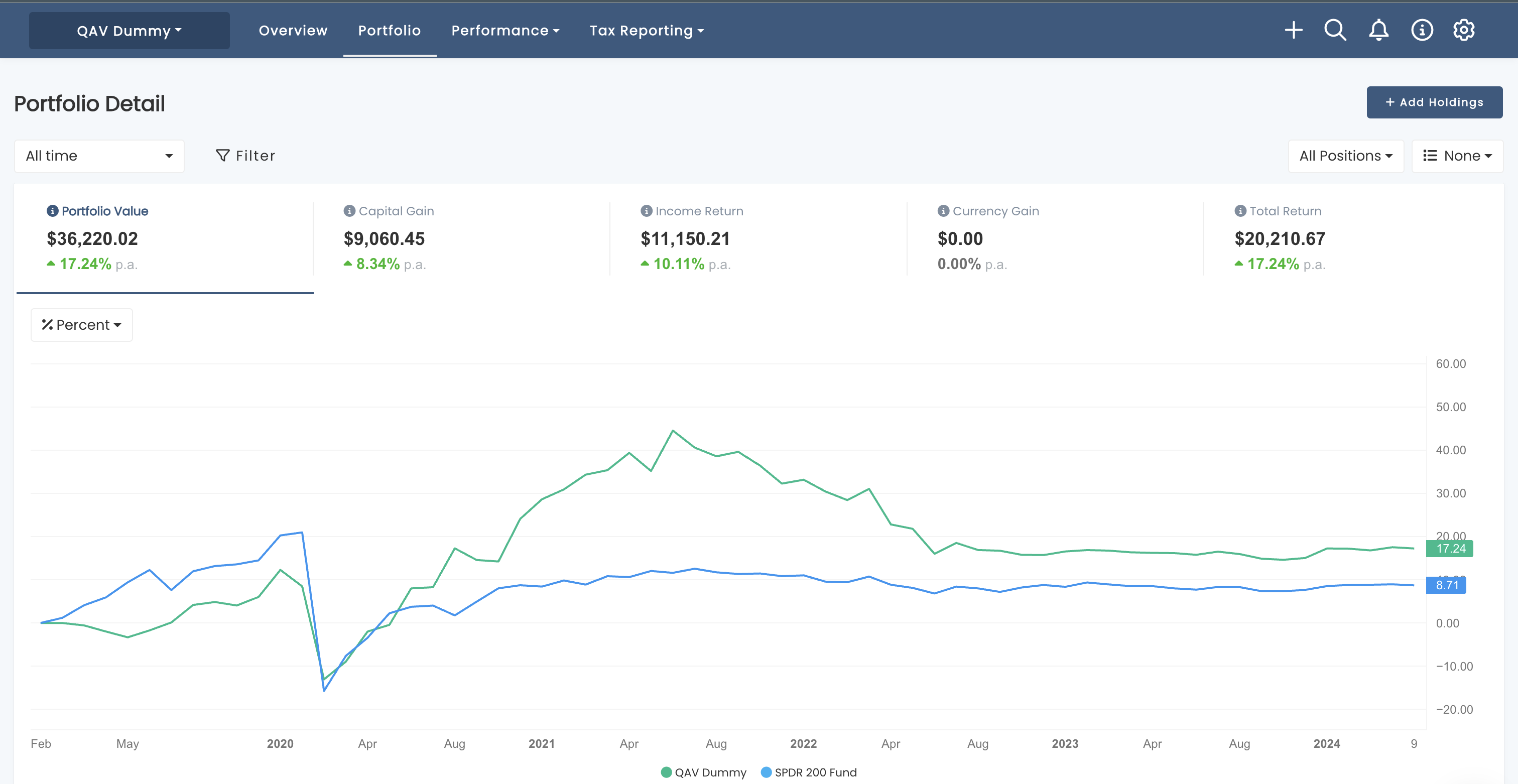

QAV PORTFOLIO REPORT

The Dummy Portfolio is performing well against the benchmark over most time frames.

CURRENT HOLDINGS

SINCE INCEPTION (15/04/2019)

Our portfolio is still doing slightly less than double market p.a. since inception (roughly five years). In real terms, the value of the portfolio has increased 75% in 5 years.

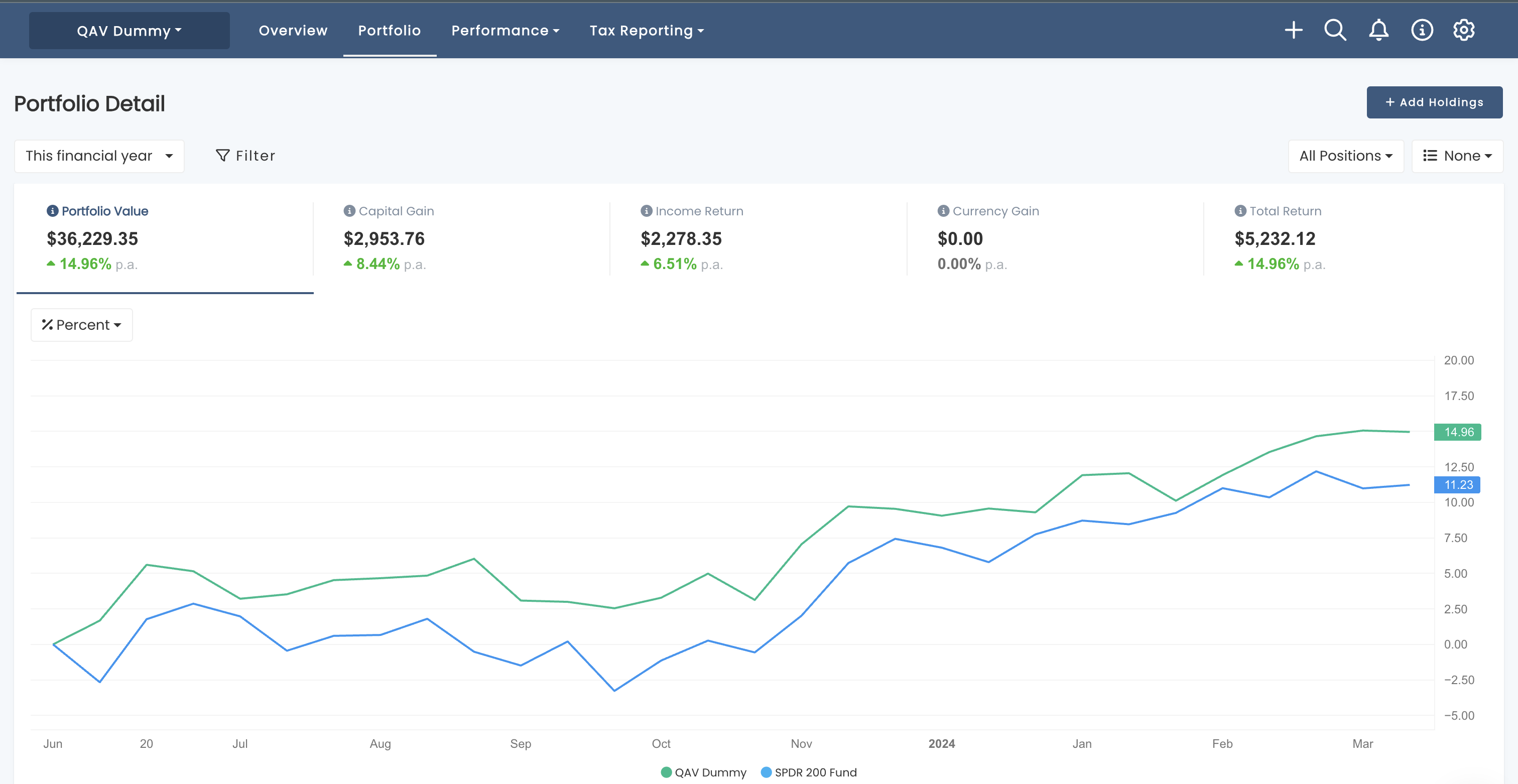

CURRENT FY

We’re outperforming the benchmark for the FY, too.

RECENT TRADES

No trades in the last 7 days.

QAV STOCKOPEDIA DUMMY PORTFOLIO REPORTS

QAV AU DUMMY

The Australian Stockopedia portfolio is still underperforming since inception. But its performance since 20 July 2023 is about the same as the 231 Light portfolio, so I don’t know if the performance has anything to do with the Stockopedia limitations.

QAV US DUMMY

The US portfolio is doing okay, but still underperforming the S&P, which, as we know, is largely being driven by the Mag7 stocks, Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla, stocks which are massively overvalued by our metrics. The recent spike was the result of GRIN going up 30% in a day after announcing a capital reduction and delisting.

STOCKS OF THE WEEK

During the last week, we also traded some stocks in our Light portfolios. Details here.

** As always, please check our work, DYOR, and consult a financial advisor before making any investing decisions.

BUY LIST

Each week we produce a buy list that we share with our members. The intended primary purpose of this buy list is for club members to use as a reference for comparing their own buy list. In theory, all of our buy lists should look pretty similar each week.

As always, please check our work, DYOR, consult a financial advisor before making any investing decisions.

THIS SECTION CONTAINS CONTENT WHICH IS VISIBLE TO QAV CLUB SUBSCRIBERS ONLY.

LAST WEEK’S EPISODE

This week: Daniel Kahneman RIP, Sturgeon’s Law, Pulled pork on ASB

Plus, in the Club edition: Valuing Bitcoin, Coking coal a sell, New Regression Testing results, Buffett’s reading v networking,

Collins St does well again, ABB news, the performance of founder lead companies.

Episode Transcription

QAV 714

[00:00:00] Cameron: Yeah, Welcome to QAV Tony, episode 7 14 . The 2nd of April, 2024. Daniel Kahneman passed

[00:00:22] Cameron: away. Tony.

[00:00:24] Tony: Yeah, I read that. Sad loss.

[00:00:27] Tony: I read about it over easter, lots of tributes to him pouring in,

[00:00:30] Tony: and obviously, you know, we’re big fans of Thinking Fast and Slow, the book they

[00:00:34] Tony: wrote, and what’s it called? The Undoing Project, I think it’s called? The Michael Lewis Project? biography of them. It’s good.

[00:00:41] Cameron: I never read that. I actually only heard about that when I read sort of his

[00:00:45] Cameron: obits and thought, Oh yeah, I should read that.

[00:00:47] Tony: Yeah, it’s a great book.

[00:00:48] Cameron: sounds good.

[00:00:49] Tony: Yeah.

[00:00:50] Cameron: So, um, for people who don’t know of Daniel Kahneman and haven’t read Thinking Fast and Slow, even though we kind of bang on about it all the time, uh, how would you

[00:01:00] Cameron: like summarize

[00:01:02] Cameron: his

[00:01:02] Tony: is he received the Nobel Prize for economics,

[00:01:05] Tony: even though I think he’s really a psychologist, but there’s no prize for psychology. So he’s one of the pioneers of behavioral economics.

[00:01:13] Tony: And when we talk about things like anchoring, um, uh, with

[00:01:18] Tony: prospect theory, we’re talking about, you know, work pioneered by Kahneman and his pal Tversky.

[00:01:25] Tony: And, uh, yeah, so a lot of the concepts that they’ve come up with are very much embedded in the science of investing, I guess. They kind of, um, you know, point out all the fallibility of the human mind. And then we, um, we kind of invent systems to try and protect ourselves from that when we invest, like having a checklist and a framework to

[00:01:46] Cameron: mm, mm, and also were some of the people to point out that, um, this idea of sort of, um,

[00:01:58] Cameron: rational behavior in economic markets isn’t really legit. You can’t take that seriously because people act

[00:02:08] Cameron: irrationally.

[00:02:09] Tony: Correct. Yeah, even people who are aware of the foibles of the human mind, so who’ve read the book, still act irrationally. And go off and buy Bitcoin or, you know, whatever else they do.

[00:02:23] Cameron: And, and the thing that I took away, like I read Thinking Fast is Slow many years ago for the first time. I’ve read it twice, I think over the years, but the thing I remember taking away from it the most the first time was that

[00:02:37] Cameron: our brains have been engineered by evolution to think. Irrationally, uh, or to, to, to make snap judgments.

[00:02:47] Cameron: Let’s say that, like, it’s not a, it’s not a failure. It’s a design. It’s a, it’s a design feature

[00:02:52] Tony: Correct.

[00:02:54] Cameron: that, that would have saved human lives for most of human history. I think the example I always use with people is, you know, you’ve got, so he talks about system A and system B or system one and system two, system one or system A is, is the part of your brain that makes, Quick, fast decisions based on gut feeling, instinct,

[00:03:16] Tony: Mm hmm.

[00:03:16] Cameron: um, system, system two is the slower part of the brain where you carefully think through the logic and the reason and the facts and you make a slow, hard calculation before you act.

[00:03:30] Cameron: And he, one of the examples I think he used in the book is, You’re, you’re a primitive person in, in the bronze Age. You’re walking through a, a jungle, got a spear in your hand. You hear something that sounds like a twig snap behind you. System two thinking. If you rely on that, you’ll stop and won’t move.

[00:03:49] Cameron: And spend five minutes thinking through all the possible things that could have made the sound of a twig snap before you act. System one will get you to just swing around and jab with your spear just in case it happens to be a tiger. That’s about to jump on you now. 99. 9 percent of the time, it’s probably not going to be a tiger, you know, that 0.

[00:04:10] Cameron: 1 percent of the time when it is a tiger, the payoff is there. Also, System 1 thinking requires less calories, humans had calorie restricted diets, so it actually burns less calories to make snap judgments rather than to sit and think. It’s hard, it’s exhausting,

[00:04:29] Cameron: as anyone who does it all day, every day knows, to think hard and deep about things.

[00:04:34] Cameron: So. We’ve been, our brains have been engineered deliberately through evolutionary processes

[00:04:40] Cameron: over a million years to make snap decisions, snap judgments. But of course in the modern world, you

[00:04:49] Cameron: know, that often goes, uh, goes awry when people go, well, you know, uh,

[00:04:55] Cameron: COVID vaccines are because Bill Gates wants to put chips in your

[00:04:58] Cameron: brain so he can track you And people go, yeah, that sounds reasonable, sure, that’ll do, I’ll just go with that. That sounds fun.

[00:05:05] Tony: Yeah, I mean, there’s been a long history of people exploiting system A and system B thinking for nefarious reasons and all these kinds of behavioral tics that we have. But you make a good point. I mean, the other, the other big thing about, um, that, that Kahneman came up with is it’s, it’s people are more averse to suffering a loss than they are elated by a win.

[00:05:25] Tony: And again, that makes evolutionary sense, right? If you’ve got a 50 50 choice to make, um, and you’re not risk averse. If you don’t care, then half the population is going to die going down the wrong road. You know, they’re taking unnecessary risks. So, you know, we’ve evolved to be very risk averse. Um, and that plays out in the share market.

[00:05:46] Tony: You, you suffer a loss, you’re more likely to walk away from the share market than to to realize that the, something, something, um, you know, it’s the regression to the mean will happen and you’re more likely to regain your, uh, your losses if you stay in the market.

[00:06:01] Cameron: Yeah. Yeah. He said that 98 percent of our thinking is done by fast thinking

[00:06:07] Tony: Mm hmm.

[00:06:08] Cameron: and about 2 percent is slow, deliberate thinking. And, um, you know, it’s, it’s hard to fight that.

[00:06:15] Cameron: Now, very hard to fight it. Our brains are designed to push us in one way, which is why I’m grateful. I was, I was going to say Daniel Kahneman was a genius up there with the caliber of a Tony Kynaston.

[00:06:28] Cameron: Like he

[00:06:29] Tony: Oh!

[00:06:31] Cameron: Stop it.

[00:06:31] Tony: That’s a damning hymn with faint

[00:06:33] Tony: prose, that’s for sure.

[00:06:34] Cameron: The thing about, I say this all the time, but one of the things that I’m grateful for QAV for

[00:06:40] Cameron: as a system is it enables me to avoid all of the downfalls of fast thinking. It

[00:06:47] Tony: Mm.

[00:06:49] Cameron: provides guide rails, guardrails, uh, for

[00:06:53] Cameron: decision making when it comes to investing in

[00:06:55] Tony: Yeah, you think about the framework first and then all you, all you focus on is implementing

[00:06:59] Tony: the framework, not thinking of, you can think about it, but you don’t think about it on the fly, you, you regression test and you.

[00:07:05] Tony: Test going forward on paper and then you implement a change.

[00:07:08] Cameron: And it, it prevents you acting on gut feeling or instinct or fear or

[00:07:15] Tony: Mm hmm. Yeah,

[00:07:17] Cameron: All of the things that our brains have been designed to act on, which aren’t really good motivations when it comes to long term success in anything

[00:07:29] Cameron: probably, but in particular investing.

[00:07:31] Tony: market is a harsh tester of those things. Like it’s always going to throw you tests and curveballs, you know, like I’ve just suffered a loss, what should I do? If you haven’t got the answer before the loss occurs, it’s going to be really hard to work it out before the market opens and decide what to do.

[00:07:47] Tony: You’ve got to have the framework and the plan already in place. And all you’re doing is using your 98 percent of your brain to implement it. without

[00:07:55] Cameron: Yeah.

[00:07:56] Tony: A bit like playing golf, right? You don’t, if you’re out in the course and you’re having a bad day, it’s pretty hard to think about your swing and re engineer it and get it right and then go back to system A thinking for the rest of the round.

[00:08:07] Tony: You’ve got to go to the range, get a lesson, have someone have a look at what you’re doing, think about it, grind it out, and then go to the golf course and turn your system B brain off and just play. Use muscle memory to play golf. It’s the same sort of

[00:08:19] Cameron: Yeah. Yeah. Well, speaking of greed, fear and greed, Bitcoin, Tony, um, it’s, uh, gone through another big price surge, but there was a great article in Wired

[00:08:33] Cameron: Magazine that, uh,

[00:08:35] Cameron: Steve Santino sent me. Actually, we talked about it on futuristic yesterday. Uh, the title to this article is What’s Behind the Bitcoin Price?

[00:08:45] Cameron: Surge Vibes

[00:08:47] Cameron: Mostly

[00:08:49] Tony: It’s the vibe.

[00:08:50] Cameron: It’s the vibe.

[00:08:51] Tony: old Dennis Denudo.

[00:08:53] Cameron: yeah, that’s what, that’s what Steve was, uh, referencing to. Well, it’s the vibe of it, Mabo, you know, the vibe. This article says, um, The price of Bitcoin has climbed to a new all time high, but assigning the cryptocurrency a value is anything but trivial. How many times have we said on this show, tell me how to determine the intrinsic value of a single Bitcoin, then we can talk about it as an investment asset.

[00:09:25] Cameron: Until you can do that, we can’t have a conversation. And that’s what this article basically says, and it’s also just talking about the boom and bust cycle of crypto, and what’s driving it, um, some of the theory behind it, but that’s it. Also, I like this, the closest thing Bitcoin has to fundamentals, characteristics that can be used to reach a solid valuation, is the cost of producing new coins, says Dal Bianco.

[00:09:55] Cameron: In the same way the price of gold is linked, to a degree, to the cost of clawing ore from the ground, the price of Bitcoin should at least loosely mirror the hardware and energy costs associated with mining new Bitcoin. Yet, the design of the system means Bitcoin resists this method for valuation too. To ensure new supply is released at a steady rate, producing Bitcoin becomes more computationally intensive and therefore more expensive as the level of competition among miners increases and vice versa.

[00:10:24] Cameron: If the price of Bitcoin rises, more

[00:10:26] Cameron: miners are drawn to participate, increasing the cost for all. Therefore, as Satoshi wrote in a 2010 article, 10 forum post, the price of Bitcoin dictates the cost of production more than the other

[00:10:38] Cameron: way around.

[00:10:40] Tony: It’s a good point, isn’t it? That to me was a very good insight. If Bitcoin was worth a dollar, no one’s going to spend any time mining it.

[00:10:47] Cameron: right,

[00:10:48] Tony: it’s worth 70, 000, you’re going to draw more

[00:10:50] Tony: people in to mine it. yeah,

[00:10:51] Cameron: yeah, and um, I like the, the, the end of this article says, um, the influence of evangelism on the price of Bitcoin limits the opportunity for good faith Debate about the prospects of the Bitcoin system. Once you drink the Kool Aid, you have a powerful financial incentive to preach to the world that Bitcoin is the most wonderful thing.

[00:11:12] Cameron: If there was a Nobel Prize in marketing, it should be given to Satoshi Nakamoto. Bitcoin’s biggest boosters embrace that dynamic as well. Bitcoin price appreciation is

[00:11:21] Cameron: an advertisement. Investors buy in on the

[00:11:24] Cameron: prospect of riches and then fall down the rabbit hole themselves creating a new generation of believers to spread the Bitcoin.

[00:11:32] Cameron: Coin Gospel. It does often strike

[00:11:35] Cameron: me as a religion, very

[00:11:38] Tony: very cultish. Absolutely. Absolutely. Yeah,

[00:11:42] Cameron: try and talk to somebody like, like Torsten, um, our

[00:11:45] Cameron: film producer friend, um, about, okay, he’s a huge advocate. you go, okay,

[00:11:51] Cameron: Well, explain to me, How to calculate the value. He’s like, oh, you don’t understand. You’re just an idiot if you’re not getting on board.

[00:11:57] Cameron: Look at it. It’s got to go to a million dollars. Yeah. Okay. But

[00:12:00] Cameron: let’s,

[00:12:01] Tony: 000. Is it? How do you value it at 500, 000? Well, it keeps halving every five years or whatever it is, and yeah.

[00:12:09] Cameron: The other point that this

[00:12:10] Cameron: article made was the fixed. So that’s one of the things I always come back to Bitcoin evangelists is there’s only a limited supply of these things ever going to be made. But one of these guys in the article says the fixed supply of Bitcoin

[00:12:22] Cameron: was priced in long ago. If you know that, it should be priced in, so,

[00:12:28] Tony: Yeah,

[00:12:28] Cameron: and they’ve known that for years, well, forever really, since it was

[00:12:32] Cameron: invented, so, hasn’t that already been

[00:12:35] Cameron: priced in?

[00:12:37] Tony: I think the current run up, it has, you’re right, exactly, um, and there’s got to be someone out there waiting to dump, the smart, the smart people in Bitcoin are waiting to dump, I think, but they’re still rubbing their hands going, this is

[00:12:50] Tony: great, because all these ETFs have come into the market since January, uh, and now we’re taking money from Wall Streeters as well, and fund managers, and, you know, people who invest in funds because they don’t want to, they don’t know how to use a, Um, how to buy a token on an exchange, all that kind of stuff.

[00:13:07] Tony: So it’s, it’s a classic pump and dump again.

[00:13:10] Cameron: yeah.

[00:13:11] Tony: It reminds me of sneakers or NFTs or, or wine or art or anything that has a limited supply, and then there’s a crowd of self appointed people who value things and say, which ones are worth more than the others. And then they just put that out in the market and the crowd just beats it up.

[00:13:31] Tony: It’s the same sort of thing. So Bitcoins are collectible in my, my point of view. And, but worse than that, I like, you know, Buffett’s take on it. It’s rat poison squared. It’s, it’s only real users to hide. What were cash transactions from authorities. And so it’s used a lot by nefarious people. They’re the ones who are also laughing all the way to the bank.

[00:13:52] Tony: And that’s, that’s got to be a problem, I think, for society.

[00:13:56] Cameron: You know who’s not laughing all the way to the bank

[00:13:58] Cameron: is Sam Bankman Freed, who just got 25 years.

[00:14:01] Tony: And you see, the irony of that is that the, he, I’ve read the book. And so, you know, he bought all these particular tokens in some, you know, coin, which have now shot up and they’ve covered all the losses

[00:14:13] Tony: that happened in his portfolio. So all these investors are being made good

[00:14:18] Cameron: Yeah.

[00:14:19] Tony: It’s incredible.

[00:14:20] Cameron: Yeah, yeah, that’s what the,

[00:14:22] Cameron: uh, his defense attorneys were trying

[00:14:24] Tony: Well, and he always argued that he said, I’ve always got, I’ve got this coin token market cornered, and that’s always going to bail me out. But it’s just the timing, he was for you a sentence before it did.

[00:14:36] Cameron: mm,

[00:14:37] Tony: Hmm.

[00:14:37] Cameron: but there was,

[00:14:38] Cameron: also a lot of fraud

[00:14:39] Cameron: happening behind the scenes, right?

[00:14:41] Tony: Well, I guess that yes, he was

[00:14:44] Cameron: and spending it on stuff. So the fact that he thought he could pay it back later on is beside the point. You can’t steal something even if you

[00:14:51] Cameron: think you’ll be able to pay it back.

[00:14:53] Tony: true. So again, Michael Lewis goes, goes into that side of things. And

[00:14:58] Tony: yes, they were taking money from the fund and putting it into the,

[00:15:03] Tony: uh, you know, the bank or their investment side of things.

[00:15:06] Tony: Their PE fund. And that was wrong. But in terms of enriching themselves, yeah, they bought, they went to the Bahamas or whatever, and they bought this beach compound and they built offices and apartments for them to live in.

[00:15:21] Tony: Wasn’t that much fraud going on from my reading of it. Like you compare it to Silicon Valley and, you know, Google building a golden donut for its workers and all that kind of shit that goes on there. It was minuscule in comparison. So yes, they broke the law. They took money from one fund and used in their own investment fund.

[00:15:39] Tony: Um, argument, Bankman Freed’s argument was so he could make the money he’d lost in the original investment fund and pay it back, which has now turned out to be true, but, um, he’s got 12 years for it. Very interesting. Oh, 25, is it? Okay. Very interesting case.

[00:15:58] Tony: Very interesting case.

[00:16:00] Cameron: Well, moving right along, Tony, we haven’t done a Morgan Household for a while. I pulled out a Morgan Household because we have no questions today and I was trying to figure out how to stuff this

[00:16:09] Cameron: stocking full of gifts. Um, The two that I’m going to use today. One is the one we all know, Pareto Principle.

[00:16:17] Cameron: The majority of outcomes are driven by a minority of events, but the inverse,

[00:16:23] Cameron: you know, you love Charlie Munger, always,

[00:16:25] Cameron: invert, always always be inverting, as opposed to Alec Baldwin in Glenn Gary, Glenn

[00:16:31] Cameron: Ross, ABC always be closing.

[00:16:36] Cameron: We’ll always be inverting. Sturgeon’s Law, 90 percent of everything is crap.

[00:16:41] Cameron: Which is

[00:16:41] Cameron: the

[00:16:42] Tony: Theodore Sturgeon, the sci fi writer.

[00:16:45] Cameron: Was it?

[00:16:45] Tony: Yeah. Yep. Ted Sturgeon. Yep.

[00:16:49] Cameron: 90% He was talking

[00:16:50] Cameron: about sci fi, wasn’t he, at the time?

[00:16:52] Tony: A lot of sci fi writers, writers I used to read when I was a kid, they were great commentators on society. Okay, they dressed them up as, you know, interplanetary travelers or whatever, and founders of new colonies, but they were

[00:17:05] Tony: fantastic. Observers of our society. Yeah,

[00:17:11] Cameron: Law, or Sturgeon’s Revelation, is an adage stating 90 percent of everything is crap. It was coined by Theodore Sturgeon, an American science fiction author and critic, and was inspired by his observation that while science fiction was often derided for its low quality by critics, Most work in other fields was low quality too.

[00:17:29] Cameron: And so science fiction was thus no different.

[00:17:36] Cameron: And,

[00:17:37] Cameron: you know, we, we say the same thing about

[00:17:39] Cameron: stocks right? 90 percent of the stocks out there as an investment are crap. Like QAV is designed to weed out the crap. And then we just focus on what’s left.

[00:17:50] Cameron: Crap by our definition of what

[00:17:52] Tony: but no, but they are crap. I mean, something like three quarters of the stocks on the stock market don’t make a

[00:17:56] Tony: profit, right? So if you’re buying an ETF, I’m always surprised at how

[00:18:01] Tony: well index investing is done, given there’s so much crap out there you’re

[00:18:04] Tony: buying when you buy a basket of

[00:18:06] Tony: stocks. Luckily, they’re usually market weighted, so you’re getting the ones that are making money and have large market caps, but you still pick up a lot of crap in there.

[00:18:16] Cameron: Daniel Dennett, the philosopher who I want to punch in the face, whatever I listened to him talk about compatibilist free will. But that’s another point. He once said 90 percent of everything is crap. That is true. Whether you’re talking about physics, chemistry, evolutionary psychology, sociology, medicine, you name it, rock music, country, Western, 90 percent of everything is crap.

[00:18:39] Cameron: Um, and I think about this in terms of AI too, like people are getting up in arms about the quality of AI. Art or AI writing or AI music, which is still very early days. And, but even as it gets better and better and people are using it as a tool,

[00:18:56] Cameron: I say, Yeah. 90 percent of it is going to be crap. 90 percent

[00:18:59] Cameron: of art music today that’s generated is crap.

[00:19:03] Cameron: That’s just, I’d never heard it. Well, I had, but I’d forgotten that it was actually Sturgeon’s law, but yeah, that’s

[00:19:09] Cameron: true. 90 percent of everything is crap.

[00:19:11] Tony: Yeah. And Pareto. Oh, the story about Pareto, how he came up with Pareto’s law. Um, and he, uh, from memory, I could have this

[00:19:20] Tony: wrong, uh, he, he looked at the tax returns of,

[00:19:24] Tony: oh, whatever country he did it on, I think it was Germany or maybe Italy, and, and worked out that, you know, um, 80 percent or 90 percent was, of the tax income was being paid by 10 percent of the people.

[00:19:35] Tony: And then he Applied that to everything. He went and got the heights of people in the country and the same thing happened that, you know, that there’s a bell curve and it’s, it’s actually the, um, Fravo’s law is the inverse of the bell curve, right? It’s telling you that most of the stuff is going to be in the middle of the bell curve, most of the contributions to anything, but the, the tails, the, particularly the tail on the high end of the bell curve is going to provide all the, all of the heavy lifting.

[00:20:02] Tony: If you, if you, if you lay out a bell curve in a different way, then, um, you always get the Pareto Principle happening. It’s, uh, it’s 80 20. 80 percent of the effort or 90 percent of the effort comes from 10 or 20 percent of the people. It’s heights, it’s tax pays, it’s all sorts of different things.

[00:20:21] Cameron: Well, according to Wikipedia, in 1941, management consultant Joseph Duran, the founder of Duran Duran, developed the concept in the context of quality control and improvement after reading the works of Italian sociologist and economist Vilfredo Pareto, who wrote in 1906 about the 80 20 connection while teaching at the University of Lausanne.

[00:20:44] Cameron: In his first work, Que D’Economie Politique, Pavarito showed that approximately 80 percent of the land in the Kingdom of Italy was owned by 20 percent of the population. Mathematically, the 80 20 rule is roughly described by a power law distribution, also known as a Pareto distribution, for a particular set of parameters.

[00:21:05] Cameron: Joseph Duran, a Romanian born American engineer, Uh, applied the observation that 80 percent of an issue is caused by 20 percent of the causes to quality issues. Later during his career, Duran preferred to describe this as the vital few and the useful many. To highlight that the contribution of the remaining 80 percent should not be discarded entirely.

[00:21:28] Cameron: And I think about it in terms of even, you know, QAV, uh, like the, the, uh, Things that we measure in QAV you’ve identified as being principles or, or, or measurements that can contribute to the, uh, long term success of a stock. But even within that, you know, we, we feel that there’s

[00:21:50] Cameron: probably two or three things that carry most of the weight,

[00:21:54] Cameron: like PropCaf, right?

[00:21:55] Tony: Yeah, we think there is. Yeah,

[00:21:58] Tony: definitely.

[00:21:59] Cameron: the thing that we’re hoping to get out of the regression testing that I’ve been working with Matt Walker on is to

[00:22:05] Cameron: test a lot of those things.

[00:22:07] Tony: Well, to re weight the

[00:22:07] Tony: checklist, exactly. I mean, currently most things are a 1 or occasionally a 2 or a minus 1,

[00:22:12] Tony: but that doesn’t reflect the weightings of each

[00:22:14] Tony: thing and its contribution to the checklist. There will be an 80 20 rule

[00:22:19] Tony: applicable to the checklist for sure.

[00:22:21] Cameron: mm

[00:22:22] Tony: The other, I mean, I came across Pareto, I mean, I came across Pareto twice.

[00:22:26] Tony: First of all, in a book called, um, A History of Risk Against the Gods. Where it kind of starts off with Pareto. It’s an excellent book, but the second thing was, you know, I did a lot of work

[00:22:38] Tony: with customer data, setting up customer databases with both Shell and Coles Meyer back in the day, back in the sort of 90s, and it was a One of the tenets of customer marketing was if you don’t have a view of your customer, every transaction is a separate transaction.

[00:22:56] Tony: You don’t know who your best customer is. So how do you know how to market your store, lay out the store to appeal to more good customers? Oftentimes the local store manager would know. Roughly who that was. But a lot of times it was just an absence of data. And so the first thing I do, once we collected data and did our analysis and worked out who the best customers was, is I’d go into a presentation with the big wig and I’d say, you know, who do you think the best customer is for Shell, for example?

[00:23:25] Tony: Oh, well, it’s this and that. And invariably the CEO would think the best customer looked like them. You know, they drive a big European car and they live in the Eastern suburbs and they, you know, fill up because it’s got a big tank and blah, blah, blah. And I’m like, no. In Shell’s case, the best customer actually was, um, was a, a trucking company because they, like, had, had a shell car that went up and down the eastern seaboard and all their drivers filled up on that.

[00:23:51] Tony: And I said, so, you know, are we going to, we’re going to do anything for this company? Oh, well, it’s just an outlier. So you go, okay, who’s the next best customer? Well, it’s someone who buys all their tires from Kmart Tire and Auto. Are we going to, are we going to do something for them or for, from AutoCare, sorry in Shell’s case?

[00:24:06] Tony: No, no, no, no, no. And so you, you. You know, the same thing happened in Myer. I presented to the Myer MD and I said, Who’s your best customer? Well, it’s a young, fashionable 20 year old, you know, who wants to be fashion forward. And I said, actually, it’s a 50 year old office worker, female office worker. No, no, that can’t be right.

[00:24:22] Tony: Yeah, it is. You know, they’re shopping in the lunch hour and they like to buy a cheap handbag and stockings. No, that can’t be right. So like the whole stores, um, the whole strategy for Myer was to be fashion forward, but really it should have been providing cheap handbags and stockings to middle aged women.

[00:24:39] Tony: So, um, yeah, there was just such a, it was, it was such a eye opening experience to be able to do the Pareto analysis on customers. Um, and it was such a hard thing to get management to buy into. When you showed it to them.

[00:24:54] Cameron: 80% of the managers are,

[00:24:57] Cameron: 90% of the managers are crap

[00:24:59] Tony: Yeah.

[00:24:59] Cameron: said Sturgeon’s

[00:25:00] Cameron: law applied to

[00:25:01] Tony: It’s certainly when some of the places I worked, worked at, yes, definitely. Yeah,

[00:25:07] Cameron: Well, it has to be true

[00:25:09] Tony: it does. of, everything.

[00:25:11] Cameron: of everything, of employees. Um, I know it, uh, in my Microsoft days, we used to talk about it in terms of fixing bugs. Like, 20 percent of the bugs would solve 80 percent of the customer, uh, complaints. And also for writing code, I know that, 80 percent of the code took about 20 percent of the time that you allocated to writing a program, but the other 20 percent of the code

[00:25:35] Cameron: took 80 percent of the time.

[00:25:37] Cameron: And, you know, people would always get it wrong when they were trying

[00:25:40] Cameron: to figure out a budget for time and costs for building code by thinking that the, you know, the 80 percent actually was going to reflect the 100

[00:25:49] Cameron: percent of the time it would take and

[00:25:51] Tony: That’s why IT projects always, you know, take longer than people think and cost more because they do an average on the bug fixes or whatever they’re doing on the build rather than, you know, worrying about the Pareto

[00:26:01] Tony: principle.

[00:26:02] Cameron: It’s that last 20 percent that gets you, getting that last bit right. Yeah, it’s a fascinating, it’s, you know, a fascinating principle that just does seem to apply in every area, both of them,

[00:26:15] Cameron: Pareto and Sturgeon.

[00:26:17] Tony: yeah, but I always flip it over too and think of the Prado principle as another way of expressing a bell curve. And so,

[00:26:23] Tony: you know, it’s also the case, and the bell curve always reminds me of the Dunning Kruger

[00:26:28] Tony: effect. If you ask a room full of people if they’re good drivers, they’ll all say yes. But they’ve got to, on average, be average drivers,

[00:26:36] Tony: right?

[00:26:37] Cameron: they can’t all be right.

[00:26:39] Tony: Yeah, yeah, exactly.

[00:26:41] Cameron: Well, I’ve got some regression testing news. Before we get into that, I just wanted to point out that as you predicted, or I predicted, one of us predicted last week, Coke and coal is a sell, uh, as of, uh, the buy list this week, which means I had to sell SMR across the board today. And I did get out of it at like a 40 50 percent profit over, I think it was about 18 months we held SMR.

[00:27:05] Cameron: And I think famously back then, I bought it when Coke and Coal was a Josephine, accidentally.

[00:27:12] Cameron: So screw the rules, Tony. This is what I’m saying. Screw the rules. I broke the

[00:27:17] Cameron: rules And I

[00:27:18] Cameron: won.

[00:27:20] Tony: I fought the law. Um, yeah, well, I mean it’s, that’s, that’s true. Uh, you know, breaking the rule is a happenstance to lucky happenstance. But you know, the rules, are good enough that we, they can cover for our errors too. You, at least you applied the rules to get

[00:27:33] Tony: out. and

[00:27:34] Tony: that’s what I like to do is if I do make a mistake and misapply the rules, I’ll apply the rules to get out.

[00:27:38] Tony: I won’t just knee jerk reacting. Reaction to sell straight away

[00:27:43] Cameron: percent of the time you apply the rules,

[00:27:46] Cameron: gives you 20 percent of the result.

[00:27:48] Cameron: But the other 20 That’s right. Yeah. the rules gives you 80 percent of the result.

[00:27:54] Tony: Yeah, You just never know. But if you, if you base your thinking about the rules on one instance, uh, I broke the rules and I won. Then you, you know, not thinking it through deeply enough.

[00:28:08] Cameron: So bye bye SMR, thanks for all the fish, um, that was a good run, until next time. Uh, so Matt Walker gave me a new, um, version of the regression testing system this morning, and, um, it was working well for me last week, and then it started crashing as I tried to extend the time horizon from eight years to a longer period, so we, he fixed a bug on it, uh, over the weekend.

[00:28:32] Cameron: I ran two this morning. That I thought I’d just talk you through. Um, their timeline for these is from January 2006 to the end of November 2023. Uh,

[00:28:49] Cameron: so, what, how many years is that? 19, roughly,

[00:28:56] Cameron: so 6, 17, 17, yeah, 6 and, 6 and 3 is not 4.

[00:29:03] Cameron: Um, anyway, so I did

[00:29:05] Cameron: a 10%, You got that 80 percent

[00:29:07] Tony: right. That’s okay. 80

[00:29:08] Cameron: percent of the time,

[00:29:09] Tony: real one.

[00:29:12] Cameron: his line in Anchorman?

[00:29:14] Paul Rudd: It’s called Sex Panther by Odeon. It’s illegal in nine countries. Yep. It’s made with bits of real panther. So you know it’s good. It’s quite pungent. Oh, yeah.

[00:29:28] Paul Rudd: Ooh, it’s a formidable scent. Stings the nostrils. In a good way. Yeah. Brian, I’m gonna be honest with you, that smells like pure gasoline. They’ve done studies, you know. Sixty percent of the time, it works every time. That doesn’t make sense. Ugh. Let’s go see if we can make this little kitty purr.

[00:29:53] Cameron: uh, so the first model that I ran over that timeframe was a usual, all the, all the standard metrics with a 10 percent rule one. It delivered a CAGR of 12.

[00:30:05] Cameron: 8%. I ran it over the same time frame with a 99 percent rule 1,

[00:30:12] Cameron: effectively no rule 1, and it returned a CAGR of 14. 4%.

[00:30:22] Tony: interesting.

[00:30:23] Cameron: I checked the CAGR on the STW over the same period.

[00:30:26] Cameron: Do you want to guess what it was?

[00:30:29] Tony: Why didn’t we look at this? I thought it was like 8 percent or 6

[00:30:33] Cameron: Well, different time period from

[00:30:34] Cameron: the one we ran it on last

[00:30:35] Tony: Oh, was

[00:30:36] Cameron: Yeah, it

[00:30:36] Cameron: was, uh, two percent.

[00:30:39] Tony: Only two. Oh, because of the GFC.

[00:30:41] Cameron: Uh,

[00:30:42] Tony: The market would have been high in 2006 leading into GFC. yeah.

[00:30:46] Cameron: So, uh, yeah, 12. 8 and 14. 4 with no rule one. Now, there’s a kind of, there’s an interesting, uh, caveat to this that Matt pointed out to me over the weekend. There’s a survivorship bias in this because the way the script works, it is looking at stocks that are on the exchange today and then going backwards looking at those stocks.

[00:31:09] Cameron: So it’s not taking into account any mergers and acquisitions of stocks that we may have bought, which I know the QAV system does well out of stocks like that from time to time. Um, but they’re going to be ignored and he’s trying to work out a way of

[00:31:26] Cameron: using delisted stocks. in this and taking into account M& A’s that happened, trying to figure out how to code that.

[00:31:34] Cameron: So that, that’s going to change

[00:31:36] Cameron: things, but I’m not sure to what extent that

[00:31:39] Cameron: would affect the results.

[00:31:43] Tony: So I thought, I thought Matt had taken data from what was in Stock Doctor now.

[00:31:49] Cameron: Yes,

[00:31:50] Tony: Okay, Okay, well, you can edit that out. Um, Stock Doctor includes, the data source that we use includes delisted stocks. Like I could go into that data provider now and type in a delisted stock name and it would give me, it would still give me data for that stock up until it was delisted.

[00:32:09] Cameron: yes,

[00:32:11] Cameron: but that’s not,

[00:32:12] Tony: So, can Matt not do that?

[00:32:13] Cameron: you probably can, but that’s not the way it’s been designed

[00:32:16] Cameron: yet.

[00:32:17] Tony: Okay. All

[00:32:18] Cameron: So it’s, it’s

[00:32:19] Tony: Well, then, then it’s a, it’s a piece of work on all the stocks that have been delisted since 2006 to see on balance, whether they’ve gone up or down and whether they would have been QAV or not Cause some delisted stocks are going to be stocks which have gone bankrupt and some delisted stocks are going to be stocks which have taken, been taken over, which will have had a nice price bump towards the end

[00:32:39] Cameron: unlikely that QAV would have bought any of the ones that ended

[00:32:43] Cameron: up becoming bankrupt or would have been holding them when they were, became bankrupt because we would have sentimented them out or rule one them out at some point if we did buy them and we probably wouldn’t have bought them because their cash flow history wouldn’t have been great, you know, um, unless something

[00:32:57] Cameron: shocking happened at some point.

[00:33:00] Tony: Well, the other way to do it Cam is

[00:33:02] Tony: start in 2006. We know that we don’t

[00:33:05] Tony: have Delisted stocks in the 2006 data set.

[00:33:12] Tony: So then we’ve gotta look at

[00:33:13] Tony: stocks that have been delisted, but were still listed in 2006 and I guess see if they were going to be QAB stocks or not going forward.

[00:33:25] Cameron: Well, you know, we’ll work that, we’ll

[00:33:28] Cameron: try and work

[00:33:28] Cameron: something out so we can include

[00:33:30] Tony: Yeah, it’s a good point. Gotta be careful that we haven’t created some kind of bias to the STW because we’ve excluded them. Yeah,

[00:33:37] Cameron: Um,

[00:33:39] Tony: my first thought was just simply to try and find out on balance whether delisted stocks were

[00:33:44] Tony: a net gain or a net L

[00:33:45] Tony: let loss.

[00:33:46] Cameron: yes,

[00:33:48] Cameron: we can try and figure that out. But I think what these numbers tell us, and I think this is valid, leaving aside the comparison to the STW and leaving aside the actual CAGAs is the CAGA differential

[00:34:02] Cameron: between

[00:34:02] Tony: Yes,

[00:34:03] Cameron: A 10 percent rule one and no rule one is that the no rule one

[00:34:07] Tony: Mm

[00:34:08] Cameron: slightly outperforms the rule one

[00:34:11] Cameron: I mean 12, 12. 8 to 14. 4. So over a, what did you say it was, a 17

[00:34:18] Cameron: year time frame. It’s, it’s a

[00:34:22] Cameron: little bit better, but not massively.

[00:34:25] Tony: included the GFC, which is important, I think, too, so you have a

[00:34:27] Tony: downturn

[00:34:28] Cameron: Starting cash for both of

[00:34:29] Tony: which probably would have, sorry, a downturn like the GFC probably would have triggered lots of rule

[00:34:35] Tony: ones.

[00:34:37] Cameron: Yeah. So the starting cash for both of them was 20, 000 starting capital. The final value

[00:34:43] Cameron: of the 10 percent rule one was 173, 000. The final value of the no rule one was 223,

[00:34:50] Cameron: 000. So a

[00:34:52] Cameron: 50, 000

[00:34:53] Tony: Yeah, big difference Yeah.

[00:34:55] Cameron: Yeah. it’s just significant.

[00:34:58] Tony: it’s material, yeah. So, um, I think you said before that the data can go back past, before 2006, so Is it possible to rerun it? with a longer time period? Mm hmm.

[00:35:08] Cameron: I know, I think that’s about as far back as

[00:35:13] Tony: Is it?

[00:35:13] Cameron: go with

[00:35:14] Cameron: this data

[00:35:15] Tony: Okay.

[00:35:16] Cameron: Um,

[00:35:17] Tony: Yeah, so the, I mean, initial, initial dates mean a lot when you’re doing this kind of regression testing, so my only comment would be, before we made a change to take rule 1s out, is to

[00:35:26] Tony: run it with a couple of other start dates. Um, you know, just pick some randomly. I

[00:35:34] Tony: guess three or four at

[00:35:35] Cameron: The next one I’m going to run this afternoon is a

[00:35:36] Cameron: 20 percent rule one over the same time

[00:35:38] Cameron: frame And see what that gives us. And then, yeah, then I can start with some different start dates and end dates and, um,

[00:35:47] Cameron: get a, get a heat map going, get a scatter graph going

[00:35:50] Cameron: and see what it shows us.

[00:35:54] Tony: Yeah, good. That’s great. And we’re confident that the regression test is working properly

[00:35:59] Cameron: Yeah, well, I haven’t done a deep dive analysis on the ones that I ran today, but I did do it on the version that he wrote last week, which is basically the same code, but

[00:36:11] Cameron: fixing the thing that was causing it to

[00:36:13] Cameron: crash, which was

[00:36:15] Tony: Right. Yep.

[00:36:16] Cameron: stock actually that was, uh, something had happened to it. I think it had been delisted or something and it was causing the whole thing to fall over.

[00:36:24] Cameron: He fixed that bug. Uh, I don’t think anything else materially has changed. And when, so what I, what I did last week when I ran my analyses is I just, you know, sort of random looked at the buys and the sells, um, plug the dates of the buys and the sells into the bread later. And, uh, just made sure that they passed all those tests, which they, which they did, um, made sure that when it said at rule one something, it looked

[00:36:54] Cameron: like the price drop

[00:36:56] Cameron: was right. And, um, that the 3P8, the 3PTL lines checked out, et cetera, et cetera. He’s built it in, built Josephines in now checking with the Josephines

[00:37:07] Cameron: So yeah, I, I, all of the analysis that I’ve done on it so far says It’s good. I mean, the other thing that’s missing is, you know, is, um, commodity cells. We haven’t figured that out,

[00:37:19] Cameron: how to factor that in yet.

[00:37:20] Tony: But as you say, even if we don’t work that out, we’re still getting relative performance, which is a

[00:37:25] Tony: good way to, good enough, well, it’s a good way to analyze

[00:37:29] Tony: what works and what doesn’t

[00:37:30] Cameron: Yeah. So, you know, we, uh, Yeah, if we just use it as comparative performance, then We can start to play with, Okay, what if we weight PropCaf, um, a 3 instead of

[00:37:40] Cameron: a 2? And what if we rate these things a

[00:37:42] Cameron: different, you know, 0?

[00:37:44] Tony: I think the way to do it is, I don’t know how the regression tester works, but if you can isolate each variable, so run a 2006 portfolio with

[00:37:52] Tony: just PropCaf greater than 7,

[00:37:54] Tony: less than 7 is the only variable. And if that return is 20 percent versus 14 percent for everything else, then PropCaf’s got to have a greater

[00:38:03] Cameron: Yeah. I can. It’s got a user interface where I

[00:38:06] Cameron: can set the scoring of all the standard metrics to whatever I want. So I’ll start to isolate them

[00:38:13] Cameron: and, um, see what happens. But yeah,

[00:38:15] Cameron: so thanks again to

[00:38:16] Tony: Yeah. That’s

[00:38:17] Tony: great. Yes. Thank you, Matt.

[00:38:19] Tony: That’s a

[00:38:19] Cameron: his great work.

[00:38:20] Tony: huge boost to our investing. Yeah. All

[00:38:23] Tony: right. A

[00:38:25] Cameron: Uh, that’s all I’ve got on my talkie

[00:38:27] Cameron: list. Tony, what have you got?

[00:38:31] Tony: couple of things. I was tossing up whether to leave this for after hours, but I’ll mention it now because it’s, um, of general interest to invest in. Uh, have you come across substacks in general and the

[00:38:43] Tony: Alchemy substack in particular?

[00:38:44] Cameron: know Substack, but not Alchemy. Substack’s a publishing platforms, like a collaborative blog where people have their own little, um,

[00:38:53] Cameron: page on it.

[00:38:55] Tony: Yeah, so, um, I spent a fair bit of time over Easter reading through a lot of stuff that’s been posted on the Alchemy sub stack.

[00:39:02] Tony: So, an investor has gathered a lot of, um, articles

[00:39:07] Tony: and, and, uh, I guess has posted some commentary on famous investors, including Warren Buffett. So there’s a lot of interesting articles on Buffett, on George Soros, on Paul Tudor Jones, etc, etc.

[00:39:20] Tony: So, if I know our listeners are interested in reading up on investing, but that was a good, a good concentrated starting point. And I’ll talk about one article which I found interesting and have done a fair bit of thinking on over the weekend, and it was headed, um, The Reading Obsession. So it was an article about Warren Buffett’s and Charlie Munger’s penchant to read.

[00:39:43] Tony: And, but the article goes on to say that may not be the whole. Secret source to Warren Buffett’s success. So it starts off talking about Buffett’s, you know, sitting around the office and reading. And he’s always said that was a secret to his success and, um, being away from the noise and living in Omaha.

[00:40:01] Tony: And a, and a quote, there’s a quote from Todd Coombs, who looks like the person who will take over the investing side of, uh, Berkshire Hathaway. Um, and Todd Coombs, was quoted as saying that he reads 500 pages per day, which seems like a heck of a lot, but not insurmountable, I guess. Um, but then the, the article goes on and really talks about not just, um, Buffett’s reading, but is there another reason why Buffett was successful?

[00:40:31] Tony: And I’m just going to try and look it up, um, a few of the quotes, but it talks about Buffett’s networking, and, um, how much Oh, I’ve lost the page now. It looks like it hasn’t, um, here we go. Yeah, the headline from the article called The Reading Obsession says I just sit in my office and read all day.

[00:40:53] Tony: Warren Buffett. But then this person goes down and they reference another article, a piece of research that was done. It was done in 2005 by a doctoral student who went through the effort of cataloguing Buffett’s social ties in a dissertation with a cumbersome title, How Can Strategic People Networks Be Successful? An inquiry into the causes and nature of social networks striving towards a mutual goal. And the link In the article takes you to an appendix which contains an overwhelming collections of snippets showing Buffett with his friends, neighbors, investors, fellow board members, CEOs, golf, bridge players, and politicians.

[00:41:34] Tony: You get the impression that all he did all day was chat, play bridge, and visit the White House. And obviously that’s not the case either, so, um, There are, there are, This person who wrote the article talks about a couple of quotes, mainly from The Snowball, and another book on Buffett called Of Permanent Value, the story of Warren Buffett.

[00:41:54] Tony: And a couple of quotes which took my interest. Buffett’s huge network of knowledgeable and influential friends also has been a help along the way. Buffett has been an original thinker, but it cannot have hurt to discuss prospects for a television station with Tom Murphy, chat about a common investment with Lawrence Tish, or talk with Jack Byrne about insurance.

[00:42:13] Tony: His network of minds has been very important. And then another one. He talks about, um, just trying to find the right quote here. He developed a network of people who, for the sake of his friendship as well as his chastity, not only helped him but also stayed out of his way when he wanted them to. In hard times or easy, he never stopped thinking about ways to make money.

[00:42:38] Tony: Since childhood, he read every biography he could find of people he admired, looking for the lessons he could learn from their lives. He attached himself to everyone who could help him and coattailed anyone who You could find that was smart and then there’s a article about Buffett going to the GEICO offices, GEICO, I think is, or GECO, I think they pronounce it, as a young investor and hitting up the the head of Gecko who told him all about the insurance industry and he says that he went on one Saturday, Buffett boarded a train to Washington DC to visit the company, which is Gecko.

[00:43:18] Tony: He asked the guard if there was anyone who could explain the business to him and was led to Gecko’s financial vice president, Laura Davidson. The quote is, My name is Warren Buffett. I’m a student at Columbia. Ben Graham is going to be probably my professor. I read his book and I think it’s wonderful. And I noticed that he is the chairman of the Government Employees Insurance Company.

[00:43:37] Tony: I don’t know anything about it, but I wanted to come here and learn. I just kept asking questions about insurance and Gecko. He didn’t go to lunch that day. He just sat there and talked to me for four hours, like I was the most important person in the world. When he opened that door to me, he opened the door to the insurance world. And then the last quote I’ll talk about is Buffett’s travel schedule. So, uh, there’s quite a long quote here, I’m trying to paraphrase it. So it starts off, Until 1958 his straightforward route was to buy a stock and wait for the cigar butt to light. The days when Warren simply sat in his study at home picking stocks out of the security analysis or the Moody’s manuals were gone.

[00:44:17] Tony: Increasingly, he began to work on a large scale, lucrative project that required time and planning to execute. Between duties at FMC, Vornado, Blue Chip, and WESCO, and regular trips to New York, Buffett was now traveling much of the time. Buffett grabbed a burn at his wife Dorothy, and immediately pulled them into his circle of friends.

[00:44:39] Tony: Now between Gecko, Washington Post meetings, Pinkerton’s board meetings, West Coast trips for Blue Chip and West Coast, business trips to New York, board meetings for the Munzingware, a board that he joined in 1974, and Kay parties, he was traveling much of the time. So, I thought that was really interesting, and I found this over my time reading about Warren Buffett and following Warren Buffett.

[00:45:03] Tony: He often puts the answer in plain sight, and I guess the question is, what’s his secret source? But he, but he, he just leaves it there and then goes on to other things. So, if you, if you did a sort of cursory analysis of Warren Buffett, you would think that his secret source was Being in Omaha, being away from the noise, being able to read all the time, spending his day locked in an office and reading.

[00:45:25] Tony: But this article sort of posits the fact that that’s true. But when you, when you combine that with this incredible network of business minds, um, then he really does have a, um, an edge. And if you think about. The gecko story, he didn’t necessarily come about with the idea to buy an insurance company from reading the, um, the, the papers on the insurance companies.

[00:45:52] Tony: He went to a company where his, his professor, um, uh, Ben Graham was the chairman and asked the CEO lots of questions and got, you know, an interest in insurance from that. Which is probably equally as important as, um, you know, sitting around and reading all day. So it’s an interesting take on Warren Buffett.

[00:46:12] Tony: And I think the Easter egg that’s always been in plain sight with Warren is he’s often said the secret to his success or that his life changed after he did a DALE. Carnegie course on how to win friends and influence people. He says, before that I was a nerd, I was a book nerd, and I couldn’t, I, you know, I couldn’t stand in front of people and talk about my investing ideas, but after that I was able to.

[00:46:35] Tony: And so he’s always said that, but it’s kind of like a throwaway line and People don’t pay much attention to it, but you couple that with the article I’ve just quoted from, and it’s, it’s really interesting that, you know, he’s not just about, um, cigar butt investing and finding value on the pages of the movies manual, he’s equally about getting out there and creating a network of people who can inform how he invests and what he invests in and who he can test his investing ideas with.

[00:47:01] Tony: That’s not to say that one or the other is, you can’t do a syllogism on this. You can’t say that if I have a good network of. Business names, I’m going to be a good investor. I have friends. You have great networks of business people and they’re not great investors. It’s kind of the reverse. Um, so it’s like, I think Warren’s special because he has the combination of both, I guess.

[00:47:23] Tony: And the article does go on to point out that, um, if you’re in a conversation with Warren, he’s always sending metal traps to test you. Before he starts to engage with you and buy into the friendship. And, uh, you know, so there’s that, but there’s also the steel track mind where if you’re trying to pitch him a story about a stock he should be investing in, he knows all about it beforehand.

[00:47:44] Tony: And if he doesn’t, he can ring up Charlie or he can ring up, you know, um, in the past, Tom Murphy or whoever, and get their take on that particular stock as well. So I thought that was interesting.

[00:47:56] Cameron: In the past, Charlie too, sadly. But Yeah. like it makes sense though, right? It’s a combination of reading and talking to people.

[00:48:07] Tony: Yeah. Yeah. And, and melding both of those two things together. It’s still all the things that we’ve talked about. It’s still having a

[00:48:15] Tony: framework. It’s still trying to buy

[00:48:17] Tony: a basket of goods that are worth a dollar for 50 cents, all that kind of

[00:48:21] Tony: stuff. But he’s also, you know, networked to buggery. Seems, it seems like from the article that during the sixties and seventies, he hardly spent any time in Omaha.

[00:48:30] Tony: He was on the plane to New York or to LA a lot.

[00:48:34] Cameron: Well, what, one of the things I remember from the Snowball book is, you know, him going and knocking on doors and expressing an interest in the, how the company was run and CEOs sitting down and talking with him for hours, because that was unusual. In the 50s, for someone to sit down and want to talk about the ins and

[00:48:56] Cameron: outs of your financials and your assets and your liabilities and profit

[00:49:00] Cameron: lines and all that kind of stuff.

[00:49:03] Tony: Yeah, and your business.

[00:49:05] Cameron: In the days before,

[00:49:06] Tony: it’s an interesting article. Anyway, but Alchemy Substack is out there if people want to have a look at it. It does have a subscription service, but there’s plenty of free stuff there to go

[00:49:15] Cameron: alchemy. substack. com, if people want to go looking for that

[00:49:21] Cameron: What’s next?

[00:49:23] Tony: Collin Street Investment Funds. So our old friend Michael Goldberg, it was in the news. One of his stocks was in the news last week. And, uh, We should perhaps get them back in to talk to us about this. So I had read in the, I think when we talked to Michael last, he was setting up a particular specialist fund to invest in, uh, what do you call them?

[00:49:46] Tony: Uranium miners. I was going to say nuclear mines, but that’s wrong. Uranium miners. Um, he, he’d worked out that there was a, um, a mismatch in the pricing of uranium and it was about to go for a run and that did really well for them. And apparently, uh, recently they did, they set up another one to, uh, uh, invest in.

[00:50:02] Tony: Uh, offshore marine servicing companies. And in an article I read in the Fin Review a little while ago, the, um, the stock that they liked the best was one called MMA Offshore. Um, and they were, had a big holding in that. And it’s, it looks like it’s come good for them because, um, uh, this is an article from the Fin.

[00:50:21] Tony: It says on Monday last week, MMA Offshore. Board agreed to sell the business for 2. 60 a share, or 1. 03 billion plus debt, in a deal with Siam Renewables, a portfolio company of Singapore based private equity outfit, Soraya Partners. The pricing was a skinny 11 percent premium to the previous close, hence major shareholder Pandora’s come out and slammed the board, agreeing to an absolute steal.

[00:50:46] Tony: So, Um, yeah, another example of I think how he’s got it right in, in finding an undervalued stock. So I thought that was interesting. Good on them.

[00:50:55] Cameron: reach out to them. and

[00:50:57] Cameron: see if they want to come back on.

[00:50:58] Tony: And the other one I thought might be worth getting in, I know we, we, um, um, had an okay to come on the show and we’re just fixing a date was, um, I think it’s Daniel Smedley from Findi. But I recently saw Findi appear on the, um,

[00:51:11] Tony: the 12 month high lists in the Fin Review and they’re well above the price that, um, they were when we did a pulled pork on them.

[00:51:19] Tony: A few months ago, so it might be worthwhile getting Daniel on to talk about that stock.

[00:51:22] Cameron: will. Remind him to, yeah, I think He was, going to India and

[00:51:27] Cameron: he was going to contact me

[00:51:28] Tony: he was, yeah, which I think was around now, I think it was either April or May he was coming back.

[00:51:35] Cameron: I will make a note.

[00:51:35] Tony: So that would be interesting. Yeah. And then the last one is just to follow up on our never ending saga of fun with Aussie Broadband,

[00:51:42] Tony: the stock that was on our buy list, um, and, uh, we spoke about it last week because the, uh,

[00:51:50] Tony: Even though they had Goldman Sachs in their corner and they were trying to take over Superloop, one of their competitors, they fell foul of Superloop and its constitution which says that no stockholder could hold more than 12%, which was a requirement of the Singapore government because they had business in Singapore.

[00:52:09] Tony: And there was an article in today’s Fin Review saying that Uh, Small Cap Fund Manager, Small Cap Fund Managers had a small interruption to their Easter long weekend yesterday as Aussie Broadband began corralling buyers for a circa 50 million sell down in its M& A target Superloop after last week’s courtroom drama.

[00:52:27] Tony: So basically, uh, Aussie Broadband had tried to get an injunction, um, Superloop was trying to force them to sell down from 19. 5 percent to 12%. Looks like they lost the injunction towards the end of last week and had to hastily find a buyer for the surplus stock they had to get it down to 12 percent over Easter because Singapore was open on Easter Monday and they didn’t want to fall foul of the Singapore government.

[00:52:52] Tony: So the, um, the continuing saga of Aussie and Superloop continues.

[00:52:57] Cameron: We still hold them too. We’re still up 1 percent on our ABB. Bought them in. August 2023 at 3. 50. Uh, they shot up to 4. 63

[00:53:15] Cameron: by the 5th of March. I was like, you beauty. And now they’re basically back down to the buy price again.

[00:53:24] Cameron: Ah, damn it.

[00:53:27] Tony: Uh, yeah.

[00:53:28] Cameron: go.

[00:53:29] Cameron: Can’t win them all.

[00:53:31] Tony: Alright, and the last thing I wanted to talk about before we move on to a pulled pork. Uh, this is in today’s LiveWire, uh, and it’s a bit of research I came across on founder led companies. It was done by Bain Company and it was for 15 years ending in 2016 where they found that founder led companies listed on the S& P 500 performed 3.

[00:53:56] Tony: 1 times better than their peers over a 15 year period. So it’s one of the items in our checklist and I’d be interested to see whether we get a similar result when you do some regression testing on the value of Owner Founder, which is in our checklist. They outline three reasons, Bain said, because founders possess these three traits.

[00:54:16] Tony: One, business insurgency, so they have a unique feature or capability that gives a business purpose, waging war on industry norms on behalf of its clients. Point two, they have a frontline obsession, a focus on the details at the frontline and culture. And point three, they have an owner’s mindset, possessing the speed to act quickly and taking personal responsibility for risk and cost.

[00:54:42] Tony: I thought that was interesting.

[00:54:43] Cameron: alright.

[00:54:44] Tony: Yeah, and we often, we focus on owner founders in our checklist.

[00:54:48] Cameron: we don’t

[00:54:49] Cameron: often find them, but when we do find them,

[00:54:51] Cameron: they get a

[00:54:52] Tony: No, because I think also too, a lot of, a lot of, a lot of the investing community look for owner founders and they tend to have very high PEs. So the likes of, um, I mean Fortescue Metals, it’s been on our buy list, that’s an owner founder company. Um, but the likes of WiseTech, Lifestyle Communities, they’re all anti QAV stocks almost, yep, almost, um, and, uh, largely because of the, of the, the owner founder effect.

[00:55:19] Cameron: Alright, ASB, Tony. We don’t, We

[00:55:23] Tony: I have.

[00:55:23] Cameron: so do your

[00:55:24] Cameron: best.

[00:55:26] Tony: All right. Well, ASB is on the buy list. Austell Limited is the company, and it was a request from someone from last week, and it’s a good company to look at. If anyone doesn’t know who they are, they’re a Western Australian shipbuilder,

[00:55:41] Tony: and now with large military contracts. So, I first came across Austell in the early 90s when I took trips from Shute Harbour to White to, um Early, not early, uh, with, with Sunday Islands anyway, um, and the ferry ride was, uh, Hamilton Island was the island I was thinking of, sorry, and the ferry ride was modern and smooth, and it was a, that was a big game changer back then.

[00:56:04] Tony: I don’t know if you ever took a ferry before the large catamarans came into being, but it could be rough, you know, it could be tossed about, um, by, by the seas, uh, but this one was incredibly smooth, and so I paid attention to it. Um, was a bit of a revolution in design back then. I’ve owned the stock on and off, over the last 20 or 30 years and it’s back on the buy list now.

[00:56:26] Tony: I don’t own it now and I found it to be fairly volatile and use driven and it’s, it’s, because it’s a manufacturer of boats, it can, its fortunes can rise and fall depending on the tender winds it gets and so you often see, um, Large movements in this operating cash flow because they have to, if they win a tender, it’s great news, the stock price goes up.

[00:56:51] Tony: Then they’ve got to invest in expanding the facilities to produce, you know, nine or ten ships for this tender. And then the operating cash flow takes a nose dive and then when they get sold and eventually delivered, the operating cash flow is gone. Great again. So it does go up and down. And it reminds me a bit of, um, uh, the pulled pork I did on a company called Extech a little while ago, last year or two.

[00:57:14] Tony: That company is now called HiCom, if anyone wants to look it up. But, um, Extech is a provider of, um, Personal body armor and helmets to police forces and military, um, uh, applications and armies and security companies. And it, again, as it being a company with, um, large swings in its cash flow, but also large swings in its share price driven by tender news.

[00:57:38] Tony: So if they win a tender to supply, um, personal armor to, um, a police force or an army, The share price goes up. Uh, same thing happens a little bit with um, ASB. Uh, having said that, it’s been pretty successful, um, over the years. And it originally, you know, back in the, uh, early 90s, it pioneered aluminium shipbuilding and large catamaran designs.

[00:58:02] Tony: And, um, it’s only recently they’re getting into steel shipbuilding, which, um, will be a new growth for them, I guess. But for more than 30 years, they have. Delivered 340 vessels in, to operators in 59 countries. A watershed for the company was winning the contract to supply the U. S. Navy with what they call Littoral Vessels, L I T T O R A L, which basically means, I think means vessels which operate within the continental shelf, so close to shore.

[00:58:32] Tony: And, and, you know, you’ve probably seen photographs or in movies of the sort of large catamaran, Uh, patrol boats that the U. S. Navy uses. A lot of those are supplied by Austal. They are currently manufacturing 21 vessels for the Australian Navy. for their Pacific patrol boat replacement project and that work is being performed in WA.

[00:58:54] Tony: However, Austal has seven shipyards in five countries, including in Mobile, Alabama, which supports the U. S. Navy requirements. And For example, recently, Austal Vietnam delivered a 94 meter high speed catamaran to Trinidad and Tobago. So, a lot of effort was put in by the company to diversify manufacturing around the world, and a lot was put into building the Mobile Alabama plant to satisfy the U.

[00:59:24] Tony: S. Navy’s requirements for local manufacturing and production. So, quite an interesting history to the company. Uh, The flip side of having these military contracts is that it has noted benefit of making it harder for ASB to be taken over, as a new owner must be vetted by both the US and Australian military and governments.

[00:59:48] Tony: And this is kind of timely because a company called Hanwha, H A N W H A, a South Korean shipbuilder formerly known as Daewoo, has lobbed a bid. And so today, um, the share price, uh, has, has gone up, but not quite to the offer price of 2. 82, um, and ASB management released a, um, a statement today that they are wary of opening their books to a competitor until Hanwha can prove that they are likely to obtain foreign review, foreign review, Foreign Investment Review Board approval in Australia.

[01:00:28] Tony: ADF and US government approvals. And that’s where it’s sitting. So the market has gone up for the share today, but not to the bid price because there is this question mark about whether the bid will go ahead. And it’s conditional on due diligence and, and ASB is quite rightly saying, well, hang on, you’re a competitive house.

[01:00:46] Tony: We’re not going to give you access to our books and unless you can prove that this has a chance of actually being consummated as a deal. Um, so yeah, so. It’s a timely time to do a Pulled Pork on this company. It’s an interesting company and the numbers are good. So let me go through some numbers. Uh, share price I’m doing it at is 220, which is pre bid.

[01:01:08] Tony: Um, and the share price is up today to 240 something, so people will need to do their own, own research on this. Uh, but 220 was less than the consensus target. Um, But greatly above IB1 and IB2, which is 8 cents and 86 cents. Largely, I think, because the PE on this company is 148 at the moment, which we score as a minus one, because it’s its highest in the last three years.

[01:01:33] Tony: But again, that reflects the fact that they’ve been investing to produce new boats. And when those boats start to get delivered and the income starts coming in, they get their paybacks for it. So. Yes, we’ll score a negative one for a high P. E. but the P. E. won’t always be that high. And in fact, the forecast earnings per share is 497 percent higher than the current earnings per share.

[01:02:00] Tony: So we score it as a 2 for that because growth over P. E. in this case is 3. 36 and we’re looking for 1. 5. So Reflects the nature of this business that, you know, they’ve done the investment and I’ll get the earnings as the sales, as the boats roll out and the sales come in. Stock Doctor, financial health and trend is satisfactory and recovering.

[01:02:22] Tony: Um, and I suspect, suspect recovering reflects again, this cashflow bouncing around a bit, but I like recovering stocks. We give it a two for recovering and a one for satisfactory in our score, um, card. The yield is only 1. 36%. And so we can’t score it for that. Uh, PropCaf is 6. 2 times, so it gets a, it’s on our list for that, gets a score.

[01:02:43] Tony: Net equity per share is interesting, 2. 58, um, which is slightly higher than the share price, and perhaps one of the reasons why the SPID’s coming from Hanwha, or Daewoo as it used to be called. So it scores both on the book value, um, price versus price, and of course book value, it is less than book value plus 30, so it scores for that too.

[01:03:04] Tony: Uh, Directors hold 9 percent of the company, so it’s a bit of a bugger we can’t score it for Owner Founder, because it does have an Owner Founder, but it’s not quite the 10 percent threshold we look for, but if anyone wants to fudge that one, I’d be in agreement with it, really. A chap by the name of John Rothwell has been in the aluminium shipbuilding business for a long time.

[01:03:22] Tony: Business for 50 years, and he still sits as the chairman on this company on the board and has 9 percent himself. The other interesting thing I found out when I was looking at the share registry is that Tatarang has 19. 34%. Do you know who Tatarang is, Cam?

[01:03:38] Cameron: not.

[01:03:40] Tony: Cookie Forrest is Uh, Private Office and Investment Vehicle, uh, and so interesting, he does take stakes in other WA companies, the lights, and it’s just below the takeover threshold, but oftentimes when an investor sits with 19.

[01:03:55] Tony: 5 percent or thereabouts, they’re thinking about a takeover of the company. So there could be a battle. If this, if this Daywood bid or Hanwha bid continues, there is another stakeholder there with a large stakeholding as well. And that could be a blocking stake if Boogie decides that he’s not going to sell, that could block the takeover as well, so it cuts both ways.

[01:04:16] Tony: It’s a recent three point trend line buy, so we score it for that. So, all in all, on a quality basis, 12 out of 17, or 71%, And PropCaf is getting up there at 6. 2 times, so QAV score is 0. 11. So it’s on the bottom of our buy list, but it’s on the buy list. Pros and cons for this company. One of the pros I think is it has really been a pioneer of advancements in shipbuilding, both from the catamaran design and the aluminium construction of the company.

[01:04:47] Tony: Having the owner founder who’s lived through all that as a chair is a good thing. And Like a lot of companies on our buy list that we’re finding, um, more and more these days, it’s, it’s attracting takeover interest from other parties. So at, at the kind of price it is, it’s trading at below book value or about book value, uh, it’s attracting interest as well.

[01:05:05] Tony: Um, on the con side, as I’ve outlined, the cashflow for this company is lumpy. So it comes on and off the buy list. So I think that’s pretty much it for me. Thanks for listening. I’ll see you next time. Impacted by investment, um, like for example, having to build a factory in the States to satisfy the U. S.

[01:05:35] Tony: Navy tender regulations. Um, and then the other, other con is if someone does take it up, uh, take it over, it does need all these approvals from governments and defense departments to make it happen, which does make it harder to take over. So you don’t see a takeover premium built into the share price of this company.

[01:05:52] Cameron: Did you read about their, um, ASIC and ATO

[01:05:57] Cameron: problems?

[01:05:59] Tony: No. Enlighten me.

[01:06:02] Cameron: Uh, I’ve got an article from January in Market Index. A sinking ship, Citi downgrades Austell’s price target by 45%. Price target bumped down to 2. 32 from 3. 70 by Citi. And it says, um, The downgrade comes on the back of Austell’s latest earnings update, published last Tuesday, which saw the shipbuilder estimate FY23 earnings of 58 million down from a previously forecast 100 million.

[01:06:37] Cameron: And it goes on to talk about Austell’s expected 42 million loss in question relates to a 2021 U. S. Navy contract valued at U. S. 198 million, which the company won to build two towing, salvage and rescue ships. One point of possible uncertainty, Austell cited an earnings downgrade to 58 million from 100 million in Australian dollars, but also references a loss of 41.

[01:07:04] Cameron: 2 million in its latest earnings update. Two years on from the contract’s execution, a revised forecast of costs for the 2021 shipbuilding program has left Austell admitting it will cop off U. S. 41. 2 million loss from the contracts. This comes after ASIC took Austal to the federal court in June 2021 over the contract, given that Austal failed to disclose to investors it was going to make a loss on the contract.

[01:07:35] Cameron: Austal landed in hot water even earlier in 2018 when it failed to disclose to shareholders the outcome of an ATO assessment, which challenged the rosier outcomes of an Ernst Young audit. Uh, Presumably Austell’s management team perceived the relationship value of the contract with the world’s largest Navy forces to be of greater interest to the company than material gains.

[01:07:58] Cameron: But apparently forgot to tell investors that. Um, yeah, so, um, other issues too, quality issues. A 2022 report from Maritime Executive alleges the Independence class Littoral Combat Ship, Austale’s premier combat vessel for the U. S. Navy, had cracked hulls in nearly half of the existing fleet. Last year, the U.

[01:08:26] Cameron: S. Navy decommissioned Oztail’s USS Coronado after less than a decade. The ship once spontaneously caught fire on the ocean in 2013. Hard to spontaneously catch fire when you’re in a large body of water, but it can be done.

[01:08:45] Tony: Just ask, I’ll

[01:08:46] Cameron: So, they have some ASIC and ATO issues in this. So, and their price was pushed down by, well, the forecast was pushed down by Citi. And I assume, um, that’s, Well, their price had dropped from 2. 80 in July, dropped down to 2. 20 in August and then down to 1. 66 in October. It was creeping back up in January, it looks like this downgrade by Citi didn’t really hurt its share price.

[01:09:20] Cameron: It was trading around 1. 90 at the time and kept going up to 2. 20 and then dropped down in February. But anyway, I assume some of these problems of, um, why it’s been devalued from 2. 20 80 in the middle of last year and

[01:09:37] Cameron: why it’s

[01:09:38] Cameron: an acquisition target now.

[01:09:41] Tony: Could be. I couldn’t say. I don’t know the company that

[01:09:44] Tony: well. Um, and it could also be that they were gearing up to,

[01:09:48] Tony: uh, invest in making these, um, naval boats in Australia. What was it they say? It was 20, 29

[01:09:55] Tony: vessels for the Pacific replacement, Pacific feet

[01:09:58] Cameron: I

[01:09:58] Cameron: wonder if they’re planning on making

[01:10:00] Tony: or anything else.

[01:10:01] Cameron: one or it’s going to make a loss out of

[01:10:02] Cameron: it, isn’t it? Yeah,

[01:10:05] Tony: uh, one they made a loss out of with the US Navy was payback. It’s like, uh, we’ve cracked our hulls, this, uh, this salvage boat, uh, you better trim your price on that one for us. Make us good.

[01:10:16] Cameron: could be, but it’s, the article suggested that um, they sort of uh, costs had gone up, Right.

[01:10:26] Cameron: Um,