Hello QAVvers

I said I’m crazy I’m Wild

I said I’m nasty

Say you will for a little while

“If I’m In Luck I Might Get Picked Up” by Betty Davis, 70s funk goddess, briefly the wife of Miles Davis, who introduced him to Hendrix and James Brown which lead to his funk-jazz experiments, talking about the AORD’s ride in the last week — it’s been crazy, wild and nasty.

Let’s have a look at the portfolios.

QAV PORTFOLIO REPORT

The Dummy Portfolio is performing well against the benchmark over most time frames.

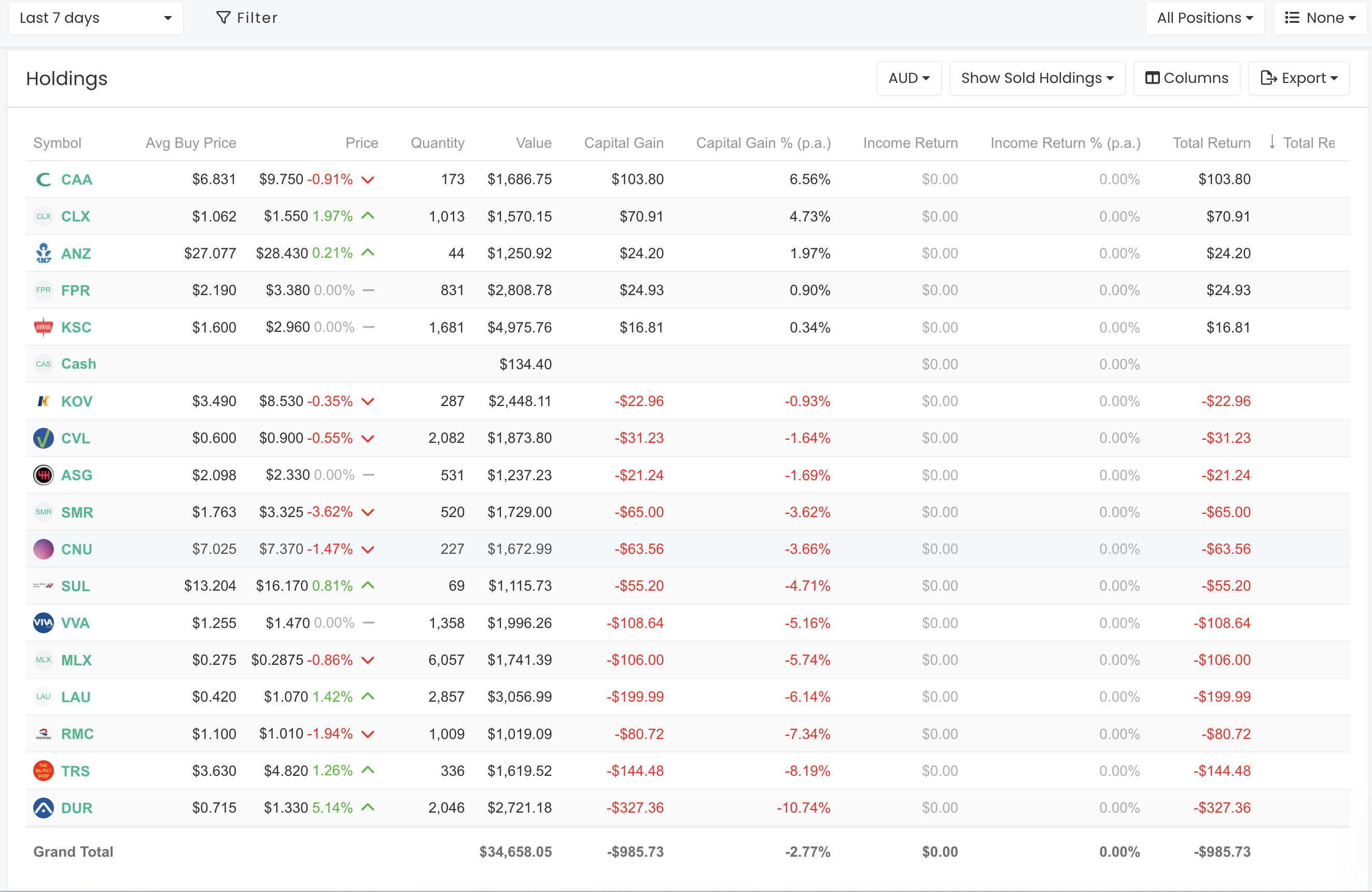

CURRENT HOLDINGS

SINCE INCEPTION (15/04/2019)

Our portfolio is still doing slightly less than double market p.a. since inception (roughly five years). In real terms, the value of the portfolio has increased 75% in 5 years.

CURRENT FY

We’re outperforming the benchmark for the FY, too.

The best perofrming stock in the portfolio during the last week was LAU (+8%).

RECENT TRADES

In the last week we sold RMC and bought AHL, which was our first trading since 17/01/2024.

QAV STOCKOPEDIA DUMMY PORTFOLIO REPORTS

QAV AU DUMMY

The Australian Stockopedia portfolio is still underperforming since inception. But its performance since 20 July 2023 is about the same as the 231 Light portfolio, so I don’t know if the performance has anything to do with the Stockopedia limitations.

QAV US DUMMY

The US portfolio is turned down this week, and I had to replace three stocks. It is still underperforming the S&P, which, as we know, is largely being driven by the Mag7 stocks, Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla.

STOCKS OF THE WEEK

During the last week, we also traded some stocks in our Light portfolios. Details here.

** As always, please check our work, DYOR, and consult a financial advisor before making any investing decisions.

BUY LIST

Each week we produce a buy list that we share with our members. The intended primary purpose of this buy list is for club members to use as a reference for comparing their own buy list. In theory, all of our buy lists should look pretty similar each week.

As always, please check our work, DYOR, consult a financial advisor before making any investing decisions.

THIS SECTION CONTAINS CONTENT WHICH IS VISIBLE TO QAV CLUB SUBSCRIBERS ONLY.

LAST WEEK’S EPISODE

This week: AORD his another all-time high, reporting season is over (but now we’re in ex-div season), ING recorded a massive profit but the market dumped it anyway, Pulled pork is on Regis Healthcare (REG).

Also on the Club edition: Ray Dalio thinks the Mag7 are “fairly priced”, Collins St Value Fund wins again, Cam’s regression tests come up with something interesting, Tony has more to say on the shrinking ASX, and after hours.

Episode Transcription

QAV 710 Club

[00:00:00] Cameron:

[00:00:15] Tony: One, two, three.

[00:00:16] Cameron: Welcome back to QAV Tony, episode 710, 5th of March, 2024. What’s going on with UTK up there in sunny Sydney?

[00:00:30] Tony: Yeah, sunny, nice day today. It’s still pretty humid. It’s good to be out of summer in Sydney. It’s, uh, weather’s cooled down a little bit, but it’s just that nice patch. Autumn and spring are always the nicest seasons. Uh, what’s going on with me? I’m cleaning the apartment, presenting it to show, and then the inspection postpones.

[00:00:48] Tony: So, wasting a lot of time spinning

[00:00:50] Tony: wheels with this process at the

[00:00:52] Tony: moment.

[00:00:53] Cameron: yeah, I’m shocked that it’s taking you this long to sell it.

[00:00:56] Tony: Yeah, it’s, it’s surprising to us too, um, but, uh, we’ve, we’ve time capped it now, so it’s got a six, six more weeks to

[00:01:04] Tony: run,

[00:01:05] Cameron: And then what? You just blow it up? Claim it on insurance? Set it on yeah.

[00:01:12] Tony: if only,

[00:01:15] Cameron: No? Okay.

[00:01:17] Tony: no, no, it’s, we’re calling for expressions of interest with a

[00:01:19] Tony: deadline. Up until now, it’s just been open for inspection. Almost like a private sale and yeah, we need to put some price tension in there, give people a deadline, get them thinking that they’ve got to compete against somebody else and get the price up and get a result.

[00:01:37] Tony: Or not. And if we don’t, at least we know we, you know, got to move on, do something else.

[00:01:41] Cameron: Mm. Well, speaking of things that are up, The All Ords has been up record highs in the last week.

[00:01:50] Tony: Ooh,

[00:01:52] Cameron: Dropped a little bit in the last day or so, but more record highs. Reporting season is over, but now we’re in dividend season. So I’ve had a couple of shares in the last couple of days that have breached a 3PTL or something like that, but then I’ve gone and checked and they’ve gone ex div.

[00:02:10] Cameron: So I just wanted to remind everyone, check your ex divs. Before you sell anything, a lot of dividends floating around at the moment. But then we’ve got the ING results, Tony. I mean, we do, we hold ING in one of our live portfolios. This is from the Australian, Friday the 16th of February, which is Couple of weeks ago.

[00:02:33] Cameron: Ingham’s sinks nearly 11 percent. Shares in poultry producer Ingham’s have slumped nearly 11 percent in opening trade 3. 86 despite its strong results and lifting dividends as investors digest its mixed outlook. The group’s half year profit jumped 268. 6% 63. 4 million as sales for the last half rose 8. 7 percent to 1.

[00:03:00] Cameron: 6 billion as more Aussies opted for chicken over red meat in the current inflationary environment. UBS analysts said it was a strong result, but the focus will be on the sustainability of the record profitability per kilogram earnings skew in the second half and the potential feed cost tailwind in FY25.

[00:03:20] Cameron: So they announced a 268 percent profit jump. And their share price dropped 11%. It’s like, well, look, yeah, you had a good half. But, you know, what have you done for me lately? What are you going to do next half? This half?

[00:03:38] Tony: it’s exactly like that, isn’t it? That’s exactly what the market said. What have you done for me lately? Well, and, and, I mean, an important comment in that last paragraph you read was the last line where the analysts are focusing on whether, well, the sustainability of record profitability per kilogram and, um, potential fee cost tailwind in FY25.

[00:03:59] Tony: So they’re already worrying about the future. And it’s interesting. I mean, it, it seems to be. More, I’ve never really noticed this before, but there seems to be a lot more emphasis in this reporting season or in this market with forward estimates of earnings. It’s like if, you know, if you’ve had a good result, but you’re not forecasting a better result,

[00:04:23] Tony: the shares go down.

[00:04:25] Cameron: You did a Paul Porkin ING back in December. I think it was the last show you did in December. It was the Turducken episode.

[00:04:34] Tony: That’s right.

[00:04:38] Cameron: And from memory, you seem to think it was a pretty good company. Pretty well run.

[00:04:44] Tony: Yeah, IMGs, yep, it’s been on and off the buy list for a number of years. Yeah, so, what I’m thinking is, I mean, we were talking off here about regression testing models, and this is a key example where we could use one to see whether we give enough emphasis in our checklist to forecast earnings per share.

[00:05:05] Tony: Whether we need to change the emphasis on forecast earnings per share, it’s in our checklist. Um, we have a growth, a growth item in our checklist and, uh, but it’s only one point out of the possible score, which is usually out of about 15. So, uh, maybe it needs more, um, emphasis if, um, if we’re being tripped up by these companies, which are solid companies, um, which are on the buy list.

[00:05:27] Tony: And then, uh, they, they just simply say. Here’s some good results, and the analysts jump on, start to worry about the future, and the share

[00:05:36] Tony: price comes off.

[00:05:39] Cameron: Yeah, it’s uh, it’s an interesting time. Like I, so we bought them, I think we bought them back in December. Um, they were, right about when you did your pulled pork, middle of December, they were trading about 3. 85, went all the way up to 4. 30. That was a good bump, but now they’re back down to 3. 61 today.

[00:06:05] Cameron: They’ve recovered a little bit from their collapse in the middle of February, dropped down to 3. 53. They’ve recovered a little bit, but not much of a recovery. It’s

[00:06:15] Tony: Have they paid a dividend recently? Sorry to interrupt, because they’re on a

[00:06:18] Tony: high yield from memory.

[00:06:20] Cameron: they may have. Let me just pull up the old Stock Doctor. Uh, they, you know, they go X in March, 14th of March, another week or so. They go X. It’s a good dividend though. It’s 12 cents, fully

[00:06:35] Tony: Mm.

[00:06:36] Cameron: So that’ll be nice. But, uh,

[00:06:40] Cameron: yeah, but there’s still, uh, I mean, we did, they didn’t breach. Uh, my sell triggers quite yet, because they did have that little run up, but um, I think they’re probably close to a, close to a breach for me now. Anyway, it’s, I don’t know man, I, I, I can’t, I can’t figure out why these companies are getting punished for doing a good job. Just seems wrong.

[00:07:06] Tony: And there’s also very quick fire responses these days

[00:07:09] Tony: too, isn’t there? This reporting season in particular, we’ve seen moves within the hour of the results coming out, double digit

[00:07:15] Tony: moves, which is a bit unusual

[00:07:17] Tony: too.

[00:07:18] Cameron: Like in a day, because they delivered a record result. Let’s see. Uh, we bought them on the 30th of November, actually, before your pull pork, uh, trading at 3. 80. I bought it. We bought them at 3. 80, currently 3. 63. So they’re down 5%. But, uh, anyway, I can’t make any sense out of it. Just seems very harsh. On the opposite side of that, Ray Dalio, our old friend. Thinks the Magnificent Seven are fairly priced, Tony. Ray Dalio, yeah, this is in the Financial Review, Ray Dalio says his simple answer for investors asking if US equities overall or the Magnificent Seven mega cap technology stocks in particular are in a bubble is no. In a post on LinkedIn, the billionaire founder of Bridgewater Associates said he used six criteria to define a market bubble, and while some of the criteria were elevated, most were not.

[00:08:12] Cameron: When I look at the U. S. stock market using these criteria, it, and even some of the parts that have rallied the most and gotten media attention, doesn’t look very bubbly. The market as a whole is in mid range, 52nd percentile. Current market levels, Mr. Dalio also said, are not consistent with past bubbles.

[00:08:30] Cameron: Mags, the Mag 7 is measured to be a bit frothy. But not in a full on bubble. Valuations are slightly expensive given current and projected earnings. Sentiment is bullish but doesn’t look excessively so, and we do not see excessive leverage or a flood of new and naive buyers. That said, one could still imagine a significant correction if these name in these names of generative AI does not live up to the priced in impact.

[00:08:59] Cameron: Uh, what do you think about that, Tony?

[00:09:02] Tony: Yeah, I didn’t. I’m not so, uh, sanguine about his, even his statements. He’s saying that we’re not seeing a flood of new and naive buyers. I think that’s all we’ve seen, really. Everyone’s, everyone’s talking about the MAG7 and buying either an ETF to get exposure to them or buying them directly. Um, that’s been happening for a while now, um, Nvidia’s the case in point, Tesla’s the case in point, Apple’s the case in point, so, yeah, I’m not sure, I mean, he’s saying he’s not going to release what his criteria are, so he’s got a different point of view, um, He is saying, I think he was using NVIDIA, for example, saying, I think he said somewhere else in the article, it trades on a 27 times PE for forward earnings, which is high, but not excessively high, and again, you know, the, uh, Peter Lynch’s metric of the PEG ratio, dividing PE by growth would bring NVIDIA down to relatively low.

[00:10:11] Tony: Benign PE, um, so I can see what he’s saying around that, but the growth’s gotta happen. And, um, whenever, whenever we have stocks with elevated PEs, even if they are growing fast, if they, as soon as they hit a road bump, the PE contracts and the share price drops dramatically. So that’s, that’s my concern with them, whether in a bubble or not.

[00:10:31] Tony: I mean, it’s, it’s pretty hard to debate people about what a bubble is. Usually we only pick it up after a burst and then we say, oh yeah, that was a bubble. I’m more inclined to say if something’s running away, way above index, then it’s probably in a bubble. Whether it bursts this year, next year, or in five years, I’ve got no idea.

[00:10:50] Tony: Um, but, but I thought some of Ray Dalio’s own metrics and arguments could be used against

[00:10:55] Tony: him.

[00:10:57] Cameron: Well. You know, I’ve got two things to say.

[00:10:59] Cameron:

[00:11:00] Tony: Oh, this time

[00:11:01] Tony: it’s

[00:11:02] Cameron: Yeah, it was

[00:11:02] Tony: this, this time it’s different. Yeah. . And

[00:11:04] Tony: don’t gimme negative

[00:11:05] Cameron: Yeah, but they

[00:11:06] Cameron: were the two. Yeah.

[00:11:07] Cameron: How did you guess

[00:11:08] Tony: Mm-Hmm.

[00:11:09] Cameron: Uh, um, but I was also gonna point out that back in April, 2021, we were talking about Ray Dalio saying that he thought Bitcoin, he suddenly convincing that Bitcoin was a good investment.

[00:11:24] Cameron: Now, in April, 2021, uh, Bitcoin was trading at about $79,000 Aussie by May of 2021, it had dropped down to $46,000. Aussie. Uh, then it went up to 89 by November 21. Then it went down to 24, 000 by November 2022, but it’s now up to 97, 000, no 104, 000 Aussie today.

[00:11:51] Tony: Wow.

[00:11:52] Cameron: So it’s gone from when he talked about, about 74, 000, it’s gone up, what’s that like, you know, yeah, roughly 25, 30 percent in a roughly three year period. Which is not fantastic, but it’s not bad either. Um Yeah,

[00:12:14] Tony: it?

[00:12:15] Cameron: yeah, yeah, yeah, so, I don’t know, Ray’s, Ray’s prediction abilities, I’m not exactly sure about right now,

[00:12:26] Tony: Yeah. Look, he’s, look, I, I think, I think these. These kinds of discussions are almost academic. He’s saying he thinks they’re fairly priced, um, because they’re not in the bubble. Well, to me, something’s fairly priced if it’s about the average for the P for the market or below. Um, and the Magnificent Seven aren’t.

[00:12:47] Tony: They’re way above that. So, you know, whether it’s a bubble, whether they’re just on a growth curve, which attracts Buyers, whether there’s a lot of index funds, which are forced to buy them, which I think is probably the case. Um, yeah, whether they’re. Whether they’re in a bubble or not, I wouldn’t say they’re fairly priced, like they’re priced to perfection.

[00:13:08] Tony: And that’s, to me, is always a bad sign if you’re buying a stock because perfection never

[00:13:13] Tony: happens.

[00:13:16] Cameron: except in my case.

[00:13:18] Tony: Right, so you, uh, what’s your stock? What’s the PE on your stock, Kev?

[00:13:23] Cameron: Oh, it’s, it’s, it’s unlimited if you ask Chrissie. Well, speaking of someone who is doing, uh, whose prediction abilities I do respect, our old friend, Michael Goldberg from Collins Street Asset Management. He’s been on the show a couple of times, I think. Another story about him in the financial review today. And

[00:13:48] Tony: to have him back on too,

[00:13:49] Tony: because he’s always been a good guest, a good value

[00:13:51] Tony: investor.

[00:13:52] Cameron: Yeah, they used to reach out to me every

[00:13:53] Cameron: six months.

[00:13:54] Cameron: I haven’t heard from them for a while. I bet I should follow them up. Um, Financial

[00:13:58] Tony: well they probably don’t, they probably don’t need us

[00:13:59] Tony: anymore.

[00:14:00] Cameron: Ha ha ha. Ah,

[00:14:02] Tony: They’re in the Fin Review now,

[00:14:03] Tony: don’t need us

[00:14:04] Cameron: Well, that’s how we found out about them in the first place. They’re in the Fin Review, I think. Uh, The Old School Fund Making Big Money From Cigar Butt Trades. In the Fin on the 4th of March, as yesterday.

[00:14:17] Cameron: First in, first out, then leave the speculators to have their fun. That appears to be the driving ethos behind the success of Melbourne’s The Collins Street Value Fund and it seems to be working. While most of the top performing funds over the past decade have relied on owning U. S. technology stocks or similar growth and quality plays, Collins Street has quietly busied itself with the so called cigar butt trades.

[00:14:42] Cameron: The often maligned investment approach, made famous as the early strategy of US investment legend Warren Buffett, is not something Collin Street founder Michael Goldberg shies away from. The very heart of what we’re trying to do is pretty simple. We’re trying to buy 1 worth of assets or earnings for 0.

[00:14:58] Cameron: 50. My favorite kind of investment is certainly a cigar butt, he says. The focus on targeting unloved stocks has helped the fund to occasionally spot opportunities way ahead of the market, and in some cases, perhaps too far ahead. It was in 2017 that Collins Street began to explore uranium stocks, a sector so bombed out that Goldberg and his team built an in house uranium ETF from scratch to gain exposure in Australia.

[00:15:25] Cameron: It took four years for the stocks to re rate and the fund to bank a tidy profit, making Collins Street well positioned for the record rally that swept the uranium sector unexpectedly in the back half of last year. The only problem was, they had sold out a year earlier. A lot of times, as we’re selling out of our position, those who are buying in are looking to get something for a dollar today that they think can be worth two dollars tomorrow, he says.

[00:15:49] Cameron: Good luck to the people who bought from us. I wish them well, but that’s just not how we play cricket. Uh, so it’s a good story, but it says that, um, over five years According to the most recent Mercer Fund survey, Collins Street took out the top spot over five years, generating 24 percent per annum before fees, and they topped the survey back in 2020 with a one year return of around 46%, which is, I think, about when we had them on the first time.

[00:16:18] Cameron: Um. He says, if growth stocks or lithium stocks or buy now, pay later is the new thing, then there is an inclination to try and follow, especially if your stocks aren’t doing well. We’re not really in the business of speculating. Once something reaches our estimation of intrinsic value, then we’re happy to sell and leave it to the growth guys who can get the cream off the top. Anyway, I like the fact that they just keep sticking to their system, which is similar to our system. They’re much more hands on. I seem to recall they go out and they interview CEOs and they research companies and, as you would expect, they’re full time fund managers. This is what they do. But, uh, the whole idea of buying undervalued, good performing businesses is still putting them in the number one spot.

[00:17:12] Cameron: Of all the funds, so, you know,

[00:17:14] Tony: yeah, you wouldn’t have thought that given the last discussion about the MAG7, but yeah, it’s good. Um, so a couple of takeaways I have from the article, which I thought was very good. Um, you’ve already quoted one part of it. We’re trying to buy a dollar’s worth of assets or earnings for 50 cents. And then he talked about potentially selling out too soon and said a lot of times as we’re selling out of our position, those who are buying in are looking to get something for a dollar today that they think can be worth 2 tomorrow.

[00:17:45] Cameron: mm,

[00:17:46] Tony: And, and that’s. I mean, it’s a very pithy couple of quotes, but that’s just such a different mindset from both of those perspectives. So, on the one hand, he thinks, Michael thinks, hey, here’s an asset, it’s worth a dollar, but I can buy it for 50 cents. I’m going to do that because Eventually there’ll be a regression to the mean and people will work it out and the value will return to what it should be and we’ll get out and make double our money.

[00:18:17] Tony: Um, and if that happens in four or five years, then we’ve got a good CAGR market beating CAGR. Um, as opposed to the mindset of the growth investor who said, here’s something that’s worth. What I think it’s worth, but in the future, I think it’ll be worth a lot more. Um, and so I’m going to take a punt that everything goes right and we get 2 for the 1 we’ve invested now.

[00:18:41] Tony: And they’re very different things. One’s, one’s simply saying, I’ve found, I’ve done a bit of rock hunting and I found a gem and I pull it, it’s, it’s going to get polished up and then it’ll be worth more. And the other one’s saying, I’ve, I found the gem and if everything goes right, I can sell it for twice as much.

[00:18:57] Tony: And I think that’s a really insightful difference on the perspectives of why I think cigar butt investing is a better risk bet than

[00:19:06] Tony: pricing something to perfection and

[00:19:08] Tony: hoping everything goes right.

[00:19:09] Cameron: mm. And the latter of those two is also partly the greater fool theory, right? I’m hoping I’ll be able to find someone who’s stupid enough to pay more for this than I did.

[00:19:21] Tony: Yeah. There’s partly that. It’s, but the difference I think is saying I’ve found a business now, which I know today is worth a dollar. Not next year, not next week, not

[00:19:31] Tony: next,

[00:19:32] Tony: not in five

[00:19:33] Cameron: because I can see it on

[00:19:33] Tony: worth a dollar. I can see it on

[00:19:35] Cameron: I know what

[00:19:36] Tony: And he’s probably, he’s probably gone out and checked out the factory and the stock and all that kind of stuff too.

[00:19:41] Tony: So he can see the assets and knows he could sell it for a dollar. Um, that’s different to having the MD say to you, Oh, but if we, you know, I’m just going to do this and that. And in the year’s time will be worth 2. So one, one’s I can touch it. I can feel it and the market’s got it wrong. And the other one is I’m backing the story.

[00:20:00] Tony: And if everything goes right, I’ll get my money back and double it

[00:20:04] Tony: sometime in the future. They’re very different

[00:20:06] Tony: things.

[00:20:06] Cameron: Yeah, different mindsets, different approaches. Mm

[00:20:12] Tony: I love the story they spoke about their latest, I think one of the latest theories was to get into the, um, offshore marine contracting space and they took a, they took a stake in MMA offshore, but they then discovered the, uh, offshore oil and gas services space had been completely decimated over the preceding decade and what companies were left were basically whoever could survive.

[00:20:35] Tony: And then Michael says, it

[00:20:36] Tony: It was like in the movie Forrest Gump when he comes back from the shrimp boat to find all the competition had been wiped out by a storm, so they build up a fleet and make a fortune. Yeah, I think what he means to say is he came back in a shrimp boat. Anyway. Um, yeah. And, and so again, that’s a, he’s, he’s found a market that sun loved that’s worth a lot more, that’s valuable, but people aren’t paying enough for it.

[00:21:02] Tony: And he’s waiting for the, the market to wake up

[00:21:04] Tony: to that

[00:21:05] Cameron: hmm. Yeah, like it’s I was listening to, um, I’ve started this thing in my newsletters recently, that whatever song happens to be playing on Spotify, I try and find a message in the song, in the lyrics of the song that, that teaches me something about investing. And the one that happened to be on this morning was, um, a cover of Rod Stewart’s, Do You Think I’m Sexy by a band called Queen of Japan.

[00:21:34] Cameron: And it’s quite a good cover that I like. And, um, I was like, well, that’s, that’s, you know, the All Ords and the Mag 7 right now is Do You Think I’m Sexy? Look at me. I’m, I’m, I’m up, everything’s going great. Um, and I, I was thinking about. I mean, the market is up, um, you know, as we said off air, it’s like, uh, I think the All Ords is up about 11 percent since the beginning of November.

[00:22:00] Cameron: The STW is up about 14 percent since then. I think our dummy portfolio is up about 11 percent since the beginning of November. Um, so that’s like, what, uh, four months, it’s up about 11 percent in four months, which is not bad. Um, but, you know, I was thinking about all the people that capitulated last year.

[00:22:23] Cameron: You know, all the investors, we know QAV club subscribers that aren’t around anymore. And we know, you know, just from general reading in the media that a lot of investors capitulated and got out of the market with the turbulence last year. And here the market is back at all time highs, uh, and all of that growth that’s happened, I mean, there was a lot of, there was a lot of down cycles there as well, but there was a lot of up cycles.

[00:22:47] Cameron: So. If you just stick in, this is just another learning for me as a, you know, new at this, five years in, that things go in cycles, right? It’s cycles, Jerry, cycles. Things go up, things go down, you stick around long enough, they go back up again,

[00:23:04] Tony: Yeah. And I had this discussion with, with my wife recently because she was saying, oh, the market’s at an all time high. Should we sell and get out? And I’m like, it’s at an all time high, but it’s taken since 2008 to get here. So what’s that?

[00:23:19] Tony: What’s it now, 24, so 16 years to get here. So, um, yeah, it could go down, but I suspect it’s got more to run having taken that long

[00:23:29] Tony: to get back to an all time

[00:23:30] Tony: high

[00:23:31] Cameron: And then it will go down, and then

[00:23:33] Tony: it will go down.

[00:23:34] Tony: Exactly. And you can’t predict it and it might go down and then come back up. So it’s, yeah, it’s, um, it’s, you

[00:23:41] Tony: can’t predict it. So you’ve got to stay in

[00:23:42] Tony: it.

[00:23:43] Cameron: And that’s, like, it’s been one of the learnings for me, as we’ve been doing the show over five years, is just watching these cycles go. Uh, you know, we had, COVID was the first one, then it recovered, then we had Ukraine, and then we had interest rates, and it’s just blow after blow, and then it recovers. And then it gets knocked down, and then it gets back up, and, and after a while, you go, yeah, okay, whatever.

[00:24:06] Tony: Yeah,

[00:24:07] Cameron: just

[00:24:10] Tony: It’s

[00:24:10] Tony: all noise.

[00:24:11] Cameron: It is, and it’s

[00:24:12] Cameron: like, but It’s the do you think I’m sexy thing, it’s like, no, I don’t think you’re sexy, it’s just, I buy stuff that the system tells me to buy, I sell stuff the system tells me to sell, and then I buy the next thing it tells me to buy, and I don’t care. Like, I really don’t care, really, like, I mean, I’m happy when things are going up because that’s, I guess, that’s an easier place to be, there’s less trading going on, you know, you don’t have to get, you know, do buy lists and checklists and all that kind of annoying nonsense, but, um, Really, it’s just kind of boring.

[00:24:53] Cameron: Doesn’t matter what’s going on, right? Just buy when you have to buy something, sell when you have to sell something and Well,

[00:25:02] Tony: Tune out,

[00:25:02] Tony: tune out the

[00:25:03] Cameron: tune out the

[00:25:04] Tony: When you, well I thought you were going to say when you, when you’re listening to Do You Think I’m Sexy? I thought you were going to talk about SXY, the uh, Cenex Energy. I thought you’d uncovered something

[00:25:14] Tony: there. A hidden, a hidden

[00:25:16] Cameron: Uh, I hadn’t thought of that, I have to go and look. I will speak about hidden gems though, um So, as you know, we’ve talked about this off air, um, and I’ve mentioned this on the show in recent weeks. One of our listeners, um, Matt Walker Um, has built a tool that I’ve been testing for regression testing and it’s, I’ve, I’ve spent a lot of time in it and particularly in the last week and it’s, it’s doing something wrong.

[00:25:41] Cameron: I know that it’s calculating the three point sell line incorrectly because when I look at its output and I look at the stocks that it’s sold and then I go and try and figure out why they’re not real ones and they’re not. 3 point trend line sell, so it’s doing something wrong. But one, one thing I did notice that was common across all the ones that I checked was they were sold at a time when they dropped below the second buy line, not below the sell line.

[00:26:15] Cameron: Sometimes they are below the sell line. Generally they, they, a lot of cases they’re well above the three point cell line, but they drop below the second byline. The interesting thing is, uh, in the tests that I’ve run using this with either a 10% rule, one or a 20% rule one, it’s delivering a 25% CAGR going using data, uh, from 2016 building buy lists from 2016 through to the end of 2023.

[00:26:43] Cameron: So essentially a seven year, um, uh, timeframe. Um, so, I’m not sure why. Yet, and I got to talk to Matt and I got to play with the code and try and get more, um, fine tweaking of it so I can work out what’s going on. But it’s just one of those things that I wanted to let people know we’re looking into, like we still think there are some perhaps changes that we can tweak the system with.

[00:27:13] Cameron: That might deliver a much better result than the double market that we are aiming for. If we can, if we can notch it up from double market to 25, which is like almost, uh, three times, two and a half times market, maybe, you know, nearly three times, depending on how you rate the market’s long term performance.

[00:27:36] Cameron: Uh, you know, that’d be great. And I think with these new tools that some of our listeners have been developing, we’re getting quite close to being able to do some very, uh, long timeframed regression testing, uh, testing a whole bunch of fine tuned metrics and being able to do it. Quickly, like when I was running these things over the weekend, uh, you know, it would take 15 minutes to an hour to run a regression test using a variety of metrics.

[00:28:04] Cameron: Um, so that’s, you know, it’s kind of very cool. And the code could probably optimized a lot, so I could do it a lot faster than that too.

[00:28:13] Tony: it is very cool, and thank you to Matt for that. Well, the first thing I can say is, don’t touch the code. If it’s getting 25 percent Kaggle, can you print it out so we can pick it

[00:28:22] Tony: apart and try and use it

[00:28:23] Tony: going forward?

[00:28:24] Cameron: Yeah, well, we need to

[00:28:26] Cameron: make sure it’s actually giving us accurate results. But, uh, yeah.

[00:28:31] Tony: buggy, let’s find out what the

[00:28:32] Tony: bugs are.

[00:28:32] Tony: They could

[00:28:33] Cameron: They’re features. Features, not

[00:28:35] Tony: they’re features.

[00:28:36] Tony: Right,

[00:28:37] Tony: Yeah.

[00:28:38] Cameron: Yeah. Yeah. That was my first reaction was, well, it’s not doing it properly, but I like what it’s doing

[00:28:45] Tony: doing it better.

[00:28:46] Cameron: Yeah. Yeah. Yeah. Um, so anyway, that’s, that’s been kind of exciting me over the last week.

[00:28:54] Cameron: Um,

[00:28:56] Cameron: that’s about that. I was just going to mention the Stockopedia portfolio as people know I’ve been testing using Stockopedia as a data source instead of Stock Doctor and has some limitations because they don’t have the same data and they do some data a little bit differently. Um, The, the, uh, the Stockopedia Australia portfolio, which kind of started in July 2023, is down 5%, uh, versus the dummy portfolio over the same period, which is about up 10%.

[00:29:27] Cameron: But the last of the Stock Doctor Lite portfolios, the 231 portfolio, is also down about four and a half percent over the same period. So, I was, I was The reason I say that is because when I was looking at the Stock Doctor, sorry, the Stockopedia one today, I was almost thinking, I’m just gonna, I’m just gonna knock this one on the head.

[00:29:48] Cameron: It’s not delivering the results it should be delivering. There’s a problem with the data that I’m using. But, I’m not so sure. I think it actually might be, when I compared it to the other one. You know, I think that the reason why the dummy portfolio is doing so well at the moment is it’s had such a long Time to establish itself that so many of the stocks are well above their rule one well above their three point trend line.

[00:30:17] Cameron: They can drop 10, 20. And I don’t even know, notice it. And then they recover. And you know, so it’s just runs by itself as opposed to that rule one cycle of death that we’ve been in with some of the light portfolios, which got started in the middle of the, the turbulent period, the Ukraine interest rate turbulence.

[00:30:42] Cameron: Um, and so, uh, yeah, the Stock Doctor US portfolio, sorry, the Stockopedia US portfolio, which was started around about the same time, is up 5%. Um, using the same sort of data limitations and, you know, working in a market that I’m not exactly familiar with. Um, so I’m still, I just want to let people know, I’m still playing around with this.

[00:31:08] Cameron: I haven’t come to a conclusion about these yet, but again, with the regression tool, as you pointed out, sort of off air. You know, if we get this regression tool working properly, we can sort of eliminate from our regression tests, the data points that we can’t get out of Stockopedia and see how that performs.

[00:31:23] Cameron: And maybe it can tell us whether or not those data points are really that important or not.

[00:31:29] Tony: correct. Yeah. Yes, no, I agree, but it’s an important point you make, and that’s something that people should bear in mind is that it does take 6 months, 12 months, a couple of reporting seasons, I’m not sure there’s a defined time period, but it does take a while for a portfolio to bed down. Um, and, and for the stocks to have risen enough so that they’re, they’re less likely to be buffeted by our sell triggers, um, that stocks can be after they’re first purchased.

[00:31:59] Cameron: Yeah.

[00:32:00] Tony: And plus, you know, we’ve spoken before about the rocket stock, the Michael Jordan, you, you, you get a couple of those in your portfolio and you’re holding them for a long time. So and it helps performance and you’ve got to, you know, they take probably more than six months to to show themselves often. So yeah, so it’s an important point.

[00:32:20] Tony: Don’t get too discouraged in the first six months if you’re trading and the results are underperforming, they will get better.

[00:32:26] Cameron: wonder what the, uh, Michael Jordan is right now in the dummy portfolio. I’m just having a quick look. Um, let’s see. Oh, wow. Yeah. I mean, there’s a couple of good ones. KOV, Covest, up 151 percent since April 2020. I’ve been holding that, uh, KSC up 96 percent since August 2021, LAU up 151 percent exactly the same as KOV since June 2022, uh, DUR up 81 percent since February 23.

[00:33:08] Cameron: Um, you know, a lot of these stocks are up 50, 80, 100, 150 percent in the dummy portfolio. Uh, there’s a couple, ASG, which we’ve held since August 2022, is only up 9%. CLX, November 22, up 10. ANZ, October 23, up 11. CNU, November 23, it’s the most recent, no, not the most recent, um, up 6%. RMC is the most recent, it’s the only one that’s down, it’s down 11%, um, but it’s got a dividend that’s gone X, which is why I’m holding on to it still.

[00:33:50] Tony: And that’s the point. So like, because we’ve got stocks that have been there for one, two, three, four years, um, you can have stocks which become a rule one sell and it’s not going to affect the portfolio performance that much. Whereas if it’s the first few months after you bought the entire portfolio, you start to have rule ones.

[00:34:06] Tony: You haven’t got that stock you’ve held for a long time to counterweight it. So it seems like you’re trading a lot and it’s affecting performance.

[00:34:13] Cameron: Yeah. But so yeah, a lot of those stocks, you know, there’s a lot of give in there. A lot of give. Anyway, that’s all I have to talk about today. TK, what have you got?

[00:34:27] Tony: I had, uh, had the, the question that was asked last week was about whether the ASX is shrinking and how does that affect us? And so I, I had a couple of conversations during the week about it and, and asked some people in the funds industry around it. And I won’t name ones because I didn’t. Tell them I was going to name

[00:34:48] Tony: them, so I don’t want to reveal

[00:34:50] Tony: sources, but a couple of,

[00:34:52] Cameron: They haven’t paid you for advertising.

[00:34:54] Tony: of

[00:34:54] Cameron: They gotta pay up first.

[00:34:57] Tony: points of view I thought were interesting and worth reporting back.

[00:35:00] Tony: Um, one view was that the ASX doesn’t do a good job at encouraging floats, um, and the person who I think he said that the ASX new IPO department was shut for a couple of months over Christmas, so they just weren’t even open to new floats back then. Um, but they also thought that one of the reasons why IPOs were shrinking was that the majority of IPOs are generally small cap stocks, um, that list, and that, uh, there seems to be a bit of a shift, this person thought, as, as Index funds as super funds as, um, your, your large funds like Vanguard and, you know, uh, Brookwater, et cetera, get bigger and bigger.

[00:35:57] Tony: They’re devoting less money to the small cap space and, and this person I spoke to thought that the, um, the average amount of, say, an Australian super fund, industry super fund or for profit super fund was Devoting to even just the ASX in total was only about 5 percent of their money, so they’re generally devoting a lot to overseas, probably a lot to the US with the MAG7 on the run, some to emerging markets, and then some to just non stock.

[00:36:26] Tony: Assets like commodities or property or whatever else they’re investing in. So only, um, his view was only about 5 percent of the money was being, um, deployed into the ASX, um, and, you know, on an index basis, most of it’s flowing towards the big cap stock. So, uh, he thought there wasn’t enough velocity of money as he called it, going into the small cap area on the market.

[00:36:50] Tony: And that was also deterring, um, small companies from even trying to IPO. on the ASX because they just weren’t getting enough investor bandwidth to make it worth their while. There’s also a consolidation in the small cap fund space, which is, I guess, Backing up that argument that there’s less money around and there’s also, uh, less, um, financial advisors.

[00:37:17] Tony: So whether it’s a good thing or a bad thing that they have to be qualified, there’s a lot that have left the industry and there was a, there was a marketing channel for small caps through, through wealth advisors and fund manager networks. Um, even if it was just simply that they were being paid a commission to put your small cap.

[00:37:36] Tony: stock in front of investors um, but but that’s shrunken as a channel too. So that’s affecting things. And then there’s also been a trend to private equity to get involved in buying small caps before they’re ready to list and to let them grow um before sale and of course the venture capital firms taking a lot of the tech companies at startup phase and not getting them to the, um, to an IPO at the ASX, potentially taking them overseas or, or letting them stay private for a very long time.

[00:38:10] Tony: So there’s a few reasons why the IPOs are drying up. Um, and the other one that was, uh, Ventured to me was, you got to look at the fees of listing a company on the ASX and this person talked about Chemist Warehouse and how they, the funds management industry and stock breaking industry had been salivating for a long time waiting for Chemist Warehouse to be an IPO on the ASX because they could clip the ticket and make a lot of money out of it.

[00:38:41] Tony: Chemist Warehouse and its ownership group knew that, and they’ve basically done a backdoor listing via Sigma Pharmaceuticals, who’ve reversed, did a reverse takeover to take Chemist Warehouse to the, to the ASX boards, but under the code of Sigma, so It’s getting to the stage where people like Chemist Warehouse are trying to game the system to avoid paying for underwriters fees, paying for producing PDSs, paying the ASX to list, all those kinds of fees that are part of the IPO process, which is substantial.

[00:39:18] Tony: Yeah, so I think Uh, I think there needs to be a bit of a rethink of the whole buy PO process, buy the ASX, to encourage some, some more listings, because they just aren’t happening at the moment.

[00:39:32] Cameron: And why would the ASX want to encourage more listings? Why does the ASX care? The

[00:39:41] Tony: Bit like, bit like

[00:39:42] Cameron: right?

[00:39:43] Tony: Well, it’s, um, it’s to, there’s a churn going on. So the question was raised last week. The, that the A SX is shrinking because a lot of takeovers are happening and companies are being taken either merged or taken offshore or, or privatized. Um, and typically what happens in the past is that if there’s 10 companies taken over in the year, there’s 20 IPOs.

[00:40:03] Tony: And so the A SX doesn’t shrink, but at the moment, I can’t think of any IPOs. Um, in the last. 6 to 12 months, um, and yet there’s been, you know, 10 to 20 takeovers. So the ASX is shrinking, and the traditional way of stopping that is, is through listing new companies. And then you let them grow so they can replace the big ones that have been taken over.

[00:40:24] Tony: But um, yeah, it’s not happening

[00:40:26] Tony: at the moment.

[00:40:27] Cameron: But my question is, does it matter to the ASX itself? How many companies are listed? Like, the, the business that is the Australian Stock Exchange, uh, how is it impacted by the shrinkage in the total number? I mean, the amount of money going into the stock market

[00:40:47] Tony: Mm hmm.

[00:40:49] Cameron: over time.

[00:40:49] Cameron: Do they, do they have an incentive to maintain a roughly equal number of businesses that are publicly listed or is it doesn’t matter so much?

[00:41:03] Cameron: Who, who benefits from an increase in the number of

[00:41:06] Cameron: stocks apart from investors having more options?

[00:41:10] Tony: well, the ASX as a company does. Um, because they charge fees to each company on the list, so they’re missing out on listing fees. Um, but I think if you sort of do a bit of a reductio ad absurdum argument on it, Um, if, if the ASX shrinks too far and becomes as big as You know, the New Zealand Stock Exchange, for example, then it’s, it’s just, um, less companies for the investment community, but all the, all the funds start to shrink, all the stockbrokers go offshore, so the infrastructure, the life cycle around, or the lifeblood around the ASX shrinks, and it makes it, makes it It just becomes less attractive, becomes a virtuous circle that in reverse, it declines.

[00:41:55] Tony: And yeah, you get to a stage where everyone’s picking over the same 50 companies. It’s, it’s not as easy to, to find the undiscovered gem.

[00:42:06] Cameron: I know it has an impact on us as investors potentially, but, um, not sure. I mean, if, so the next question is, if there is. A big enough incentive for the ASX to maintain the number or grow the number of companies that are publicly listed. Why aren’t they making the changes to the fundamentals about how the system works that drives that

[00:42:33] Tony: Correct. Because they’re too busy trying to fix up the chess replacement system probably.

[00:42:40] Cameron: Yeah. All right.

[00:42:42] Tony: they’ve been knocked around a bit. Yeah, interesting, yeah. I don’t think it’s affecting us at the moment, but I’d like to see the IPO market open up. I suspect it will anyway when interest rates drop and there’s a bit of a freeing up of money.

[00:42:56] Tony: But at the moment, yeah, I think it’s a, it’s a Dangerous time for the ASX. If it can’t get companies to list on the ASX as opposed to taking private money or going offshore, then yeah, the market will contract, which eventually will become problematic. It won’t be, won’t be a problem for a while, but it’s not a good, good thing to see happen.

[00:43:18] Cameron: right. Okay. Well, thanks for that. What else you got?

[00:43:24] Tony: Pulled pork time

[00:43:26] Cameron: Uh,

[00:43:26] Tony: and then doing a pulled pork on Regis Healthcare.

[00:43:30] Cameron: what’s their code?

[00:43:33] Tony: REG.

[00:43:34] Cameron: REG.

[00:43:35] Cameron: I don’t think I own any REG. I think it’s

[00:43:39] Tony: No, that’s good. Yep,

[00:43:43] Tony: it won’t

[00:43:43] Tony: affect our performance.

[00:43:44] Cameron: me about REG, Tony.

[00:43:47] Tony: Yeah, sure. Aged Care Services Provider. So, they operate aged care facilities, retirement villages, home care services, day therapy and day respite programs. So, people would have seen Regis Health logos around. Probably most prominently, the one I can think of was when my parents were in the retirement village, there was a Regis aged care facility as an adjunct.

[00:44:16] Tony: So as you required more care, as you got older, you sort of just migrated from one part of the retirement villages into more of a hospital type setting and received the care from Regis. So that’s, that’s my brush with them. Um, they were formed back in 1994 by Brian Dorman and Ian Roberts. Ian Roberts was a Property developer and Brian Dorman was an accountant and Brian Dorman saw an opportunity when he visited the Cramp facility in Footscray in Melbourne while working as an accountant and being unimpressed he teamed up with E.

[00:44:53] Tony: M. Roberts to invest in elderly care homes. That was back in 1994. And then three years later, there were sweeping changes to the government funding model for aged care in 97 and it improved the sector and enough so that Dorman and Roberts began a series of acquisitions that led a decade later to a merger with the Macquarie Capital backed Retirement Care Australia.

[00:45:19] Tony: And, uh, in 2013, uh, Macquarie Capital sold its stake in the merged entity to the two founders who then listed in 2014. Regis Healthcare now provides services and facilities to over 7, 600 older Australians and uh, operates 68 aged care facilities around the country. Um, I think looking through their story.

[00:45:50] Tony: Uh, particularly in the recent years, there’s, there’s three important factors to talk about, um, that affect aged care operators. Um, the first being there was a Royal Commission, uh, three or four years ago. The second being there is, uh, um, a population demographic which is trending older, and so the boomers are all getting to that age of of needing this kind of care, or starting to anyway.

[00:46:17] Tony: And the third important factor in the last few years has been COVID. So to take each of those, um, in, uh, in there, uh, separately, um, the Royal Commission into Aged Care has led to the release of a new Aged Care Act in December 2023, um, it’s open for consultation, but the Act will become law at some stage this year, uh, this, uh, this draft anyway, um, Regis believes will benefit Uh, them and, and some of the other providers, and I guess the market does too, because, uh, Regis share price has been going up quite well over the last sort of 6 to 12 months.

[00:46:59] Tony: Uh, the reasons why it will, uh, the Aged Care Act will benefit, or the new Aged Care Act will benefit Regis is that it, it does include improved funding, um, and Regis will get most of its funds from the government. Um, to fund beds in their facilities and services. Uh, so there’s improved funding to cover staff wage rises.

[00:47:22] Tony: And, um, that’s, uh, regulated by an independent body. Um, there is, uh, another independent body to, oh, sorry, the same independent body to provide funding recommendations which is linked to the actual costs of providing care, which hadn’t been the case in, in the, um, in the past. Uh, there is a, a mandated system of what they call care minutes.

[00:47:50] Tony: So it’s like a regulated number of minutes per day that a nurse and other qualified personnel have to be present and servicing an aged care user. So that will hopefully remove some of the players who aren’t doing that from the market. That’s also being reinforced by star ratings so that Um, different operators in the sector will get independent, uh, star ratings, which will show the good ones from the bad ones.

[00:48:21] Tony: And some of these are already happening because they’re implement, uh, they were implemented after the Royal Commission. Some of them are in the draft legislation. Um, so, uh, This legislation and the output from the Royal Commission has kind of lit a fire on the Regis Healthcare stock because it has improved funding to the sector, which the Royal Commission found was a, was basically a broken model where the government said how much it was willing to pay, but that didn’t take into account the cost of actually providing services, which put these, these types of companies and providers in a bind.

[00:48:54] Tony: Um, the second thing to talk about is the ageing population. And so. The average age of someone entering care at these facilities is around 84, and, uh, as the, as the boomer population Ages, that demographic or that cohort of demographic around that 84 age is getting larger and larger. And it’s estimated that, um, in the foreseeable future, there needs to be about 60 billion invested in the sector to meet the demand of boomers as they reach that, uh, sort of 84 age cohort and need, um, substantive, uh, age care.

[00:49:33] Tony: Uh, the last thing to talk about is COVID. Uh, which the company is now coming out of, but, um, company Regis Healthcare and Aged Care in general really took a pounding during COVID with, you know, obviously their patients were the most vulnerable to COVID and so the regulations around them operating were the strictest, but also there were large staff cost increases because People just didn’t want to go and work in a nature care facility.

[00:50:03] Tony: Plus, with the extra regulations, it required more staffing to administer vaccines and to do things as, you know, as remotely as they could, I guess, in the facilities that were operating. So, that kind of hit to their cost has just gone away. They’ve called out that, um, they’re basically over the COVID cost bump, which is helping Regis to return to profitability.

[00:50:28] Tony: Um, and I guess that, that’s, the effect of COVID is borne out by the fact that, uh, Brian Dorman, one of the owners, his company Ashburn, joined up with Washington Salt. Pattinson, uh, back in November, 2020 to bid for the company, um, in the takeover at 1. 85. Um, and that was just after COVID. Uh, if they had have been successful, um, they would have reaped the benefits because the share price is basically double that today.

[00:50:55] Tony: So certainly Brian Dorman, the owner realized the company was, um. was at its low point and that things will get better as COVID passed and that’s come to pass as well. I guess the other point to mention in talking about Regis before getting to the numbers is that it’s the last listed aged care play on the ASX after Estia Health was taken over in August 23 by Bain Capital.

[00:51:22] Tony: So, healthcare and the play on demographics and the population getting older has always been a favourite theme in the stock market, um, and so these providers have been taken over and been taken out, um, fund managers and large corporations A large pool of investments love to play in this space because they can see a road to profitability as the baby boomers get older.

[00:51:51] Tony: And so all that’s left now is Regis Healthcare. And I guess it does raise the question whether they will last, or whether someone will come along and try and take them out. Just as Washington SoulPatch did try to do a couple of years ago. But that’s by the by, we’ll see what happens. If an investor does want to play in this space, its only option is Regis Healthcare.

[00:52:13] Tony: Uh, the numbers. So this is, I picked this one to do this week because it has a large ADT of 474, 000. So it’s um, it’s not near the top of the buy list, but it’s large enough to be of interest to most listeners. Sentiment is very strong with this company, so its share price has recovered dramatically in the last sort of 6 to 12 months.

[00:52:33] Tony: I’m doing my numbers based on a share price of 3. 49, which it was on the weekend, but it’s already up to 3. 70 today, so since the last figures, um, came out, there, uh, there has been a bump in the share price, which is, which is still going on. Uh, I’m using the latest figures, which are in Stock Doctor now, so that’s, um, that’s good.

[00:52:53] Tony: 3. 49 was less than the consensus target, but I’ve got a feeling 3. 70 is starting to reach up to it. Um, and. As I indicated before, the company hasn’t been profitable since COVID, so I can’t, uh, the IV1 for this company is negative, because we don’t have a positive earnings per share to use in our calculation, and IV2 is just slightly positive at 1.

[00:53:16] Tony: 12, so well below the current share price, so we can’t score it for price,

[00:53:24] Tony: or value on price. The yield is, is reasonable at 3. 94%, but, um, it’s not big enough to score it as a yield stock, and Just to make people aware, it goes ex dividend on the 14th of March, so it’s coming up. Uh, Stock Doctor, Financial Health and Trend. Financial Health is an early warning, and Trend is steady.

[00:53:45] Tony: So, we don’t score early warning, but we’ll give it a score for steady. Uh, the P on this, in this stock is not applicable, so we score it as a zero, um, because it hasn’t made a profit for a while. The interesting thing though is that this company does have good operating cash flow and free cash flow, um, but they just haven’t flowed through to the profit line yet.

[00:54:10] Tony: Uh, Bree just last made a profit back in December 21, in that half. The big thing I think which is exciting the market again is this idea of the forecast, um, earnings per share is forecast to be profitable. So, forecast earnings per share is 11. 6 percent, uh, sorry, 11. 6 cents per share. and to make a profit in the next financial year accordingly.

[00:54:32] Tony: So again, I think the market is focusing on what the forecast earnings per share are and placing an emphasis on that. Crop cap for this company is 5. 3 times, 5. 39 times, um, is 5. 39 times, I’ll get that right in a minute, um, which is good and net equity per share is only two cents. So we can’t, um, we can’t buy it for book or book plus 30 or anywhere near book value.

[00:54:59] Tony: Uh, Growth over P. E. doesn’t score because we have a negative P. E. What does score for us is Owner Founders and those two members, two owners I mentioned before, Roberts and his friend, own 55 percent of the stock. So, very strong presence by Owner Founders, so it scores for that. Um, I wanted to highlight the fact it’s not scoring on consistently increasing equity.

[00:55:26] Tony: And the reason I’m highlighting this is because equity is shrinking dramatically, um, down from 158 million in December 20, when it last made a profit. It’s now down to 4. 5 million in December 23. So, um, it’s shrunk quite a lot and it’s, it’s getting close to Um, having no net equity, which underscores the early warning, financial health, and it puts pressure on Regis to return to profitability.

[00:55:52] Tony: So a lot of

[00:55:54] Tony: focus on, on getting that

[00:55:55] Tony: right, I guess.

[00:55:56] Cameron: why the big drop in net equity? Is it just loans?

[00:56:00] Tony: uh, possibly, but I think it’s they’ve been using that money to sustain themselves while they haven’t been making money. So they’ve been taking retained earnings to pay for losses would be my guess. Um, during that period, uh, so yeah, like, um, that’s been going on, something to pay attention to and a potential risk

[00:56:18] Cameron: Hmm.

[00:56:19] Tony: Um, but all in all, uh, the quality score is 8 out of 14, 57%, and the QAV score is 0. 11, which is just on the, on our buy list. But it’s a large ADT stock and it comes on the buy list this week for the first time. Uh, positives and negatives. I think the, um, the positives are that the government does seem to be treating the aged care sector with the attention and, um, and funding it deserves.

[00:56:43] Tony: So, um, they’re also freeing up some of the regulations around opening new centers. And that’s, I guess, in acknowledgement and anticipation of the Boomer cohort getting older and needing a lot more beds. Um, but that helps Regis in terms of their Development, uh, uh, pathway going forward. The biggest positive has got to be that too, that the boomers are getting older.

[00:57:05] Tony: So there’s going to be a lot more demand for these services going forward. The negatives, um, the low equity worries me a little bit and does put pressure on them to, to, to actually get the profitability, not just forecast it. Um, but I’m also going to highlight this. What I think is a negative is even though it’s improving is government regulation and reliance on government funding.

[00:57:26] Tony: And it’s. it’s. being fixed up now, but it was a big issue for this company, um, prior to the, the Royal Commission into Aged Care. And I’ve just found over the years that companies that rely on government funding can go through periods where the government For whatever reason, generally, because of tight fiscal circumstances, lets the funding slide.

[00:57:52] Tony: And it’s like a company with one customer, they’re beholden to that customer and they can go through good and bad times with that. And happens to be a good time at the moment, but it has been a bad time. And when the government doesn’t pay, it doesn’t pay. There’s no one else to pay. So it can be a problem for these kinds of companies.

[00:58:11] Tony: So I’ll highlight that as a risk as well.

[00:58:12] Cameron: Hmm.

[00:58:14] Tony: Yeah. So that’s

[00:58:14] Tony: Regis.

[00:58:16] Cameron: They have been on our buy list before. I’m just looking back over the historic, historical buy lists. Um, it’s been, uh, they sort of come on and off by the looks of it. Um, let’s see how far back I can find them.

[00:58:35] Tony: And don’t confuse them with Regis resources too,

[00:58:37] Tony: people. It’s very different

[00:58:38] Tony: things.

[00:58:39] Cameron: Uh, what’s Regis Resources code?

[00:58:44] Tony: I don’t know.

[00:58:46] Cameron: These guys are

[00:58:47] Tony: And I’ll tell you,

[00:58:47] Cameron: right? Yeah. Okay.

[00:58:49] Tony: they are.

[00:58:49] Tony: Yep,

[00:58:51] Cameron: Regis Resources is RRL. Regis Resources Limited? Yeah. No, Regis Resources, uh, risk, sorry. Regis Healthcare back in April 22. They’re on our buy list. Uh, March 22 actually. Yeah, they come on and they come off, but just looking at, I, I dunno if we’ve ever bought them. Let me see if I’ve ever had them in there.

[00:59:15] Cameron: Uh, let’s see if they’re in my archive here.

[00:59:20] Tony: They would have been good buying about a year ago too, because the share price has gone up

[00:59:23] Tony: dramatically in the last year or

[00:59:25] Tony: so.

[00:59:25] Cameron: Yeah, I’ve got no record of ever owning them, but yeah, looking at their share price in the last year, it’s gone from 1. 48 March last year to 3. 50 today. It’s a bit of a corker of a year.

[00:59:42] Tony: Which I guess is because analysts are working out that the government funding will improve, and this company is so

[00:59:47] Tony: reliant on government funding.

[00:59:49] Cameron: I’m wondering about the nature of this star rating system for elderly care centers. Is it like, is it based around the average number of rats found in the rooms of the elderly people? Like if it’s,

[01:00:00] Tony: Well, it probably is. You get a one

[01:00:02] Tony: star for

[01:00:02] Cameron: it inverse? It’s the inverse. So

[01:00:07] Tony: Mm.

[01:00:08] Cameron: for every, for every five rats we take away, uh, take away a star.

[01:00:14] Cameron: I

[01:00:14] Tony: Yeah. Well, I mean, that’s, we joke about it, but that’s been a problem with the aged care sector for a long time is, is neglect, uh, because the government hasn’t been

[01:00:22] Tony: funding it to the level it

[01:00:23] Tony: probably should,

[01:00:24] Cameron: mean, the stories that came out in the Royal Commission were just horrifying, like physical abuse, sexual abuse, emotional abuse, uh, just horrifying. Like,

[01:00:38] Cameron: ugh, I’m

[01:00:39] Tony: Yeah. And. I can’t recall Regis’s name being linked with any of that, so I suspect it wasn’t. Um, and I guess what, where they’re coming from is they’re a big player in the field that can afford to set good standards in and pay their staff well, and the star rating will get, hopefully get rid of some of the cowboys, smaller operators who might be more inclined to cut corners.

[01:01:03] Cameron: trying to decide whether or not I should call this episode Counting the Rats or something, but I’d steer clear. It’s too dark even for me. Uh, alright. Oh, thank you for that one, Tony. It’s the one that I wish I’d had in our portfolios

[01:01:19] Tony: yeah,

[01:01:20] Cameron: over the last year. What did you say it’s, uh, ADT is? 474,

[01:01:26] Tony: it’s

[01:01:28] Tony: 450, if I

[01:01:29] Cameron: 000,

[01:01:30] Cameron: yeah. Too small for you, but big enough for most

[01:01:34] Cameron: people. cap 1. 1 billion.

[01:01:41] Cameron: Alrighty, have a look at that, folks. Well, that’s it for the regular part of the show. No questions. Today, Tony, we’ve answered all the questions that anyone can

[01:01:54] Cameron: ever have had about QAV.

[01:01:59] Tony: I’m surprised because you and I read the paper and we have questions about Ray Dalio and other things, I’m sure people are out there, all you got to do is open the paper, you’ll have questions, so please

[01:02:09] Tony: send them in.

[01:02:11] Cameron: Or don’t. Um, it’s like, it’s not like

[01:02:14] Tony: talked for an hour and a half,

[01:02:15] Cameron: know.

[01:02:16] Cameron: Yeah,

[01:02:17] Tony: our life easier,

[01:02:18] Tony: we don’t get

[01:02:19] Cameron: you don’t have to do research to answer questions

[01:02:22] Tony: Yeah,

[01:02:22] Tony: correct.

[01:02:23] Cameron: After Hours, TK, what have you been doing outside of investing in the last week? What’s taken your

[01:02:27] Tony: Yeah, I know that.

[01:02:28] Cameron: Cleaning, apart from cleaning your

[01:02:30] Tony: yeah, setting up the apartment for sale, building furniture comes, comes delivered. Um, yeah, no, not much. Uh, look, I, look, I’ve been, you know, I’ve watched a number of things, which are just kind of great when you’re tired after cleaning the apartment and setting it up at eight o’clock at night.

[01:02:49] Tony: So the new series of Drive to Survives on Netflix, it’s okay, like, like keep going back to suits. Which is, it’s fine. It’s getting, getting a bit, a bit stranger and a bit more soap opera ish as it goes on, but it’s, it’s fun. Um, but I still like going back to my old Aussie movies, and I watched Emerald City the other night.

[01:03:10] Tony: Have you ever seen that?

[01:03:12] Cameron: Uh, look, I don’t I think so. I’m just looking it up. Wasn’t

[01:03:19] Tony: So David Williamson played, and I love David Williamson plays, I think he’s a national treasure. Love reading his, his works. Uh, was a play, they made it into a movie starring John Hargraves, who I, Admire greatly, Robin Nevin, uh, Nicole Kidman,

[01:03:37] Cameron: Mm hmm.

[01:03:38] Tony: um, yep, so good, good, strong cast, Ruth Cracknell was in it, yeah, Chris Haywood is in it, um, and it’s, it’s just a treatise on the Melbourne Sydney divide, which I found amusing given that I’m living in Sydney and thinking of moving back to

[01:03:54] Cameron: Mm hmm.

[01:03:55] Tony: it’s, it’s about a, a playwright.

[01:03:57] Tony: John Hargroves who comes north from Melbourne, um, Ruth Krucknall’s his agent in Sydney with the Big Harbour Views, Chris Haywood’s the hustler who just wants money, um, and it’s the tension between that dynamic of Sydney being all, all show and all about the money and Melbourne being more cultural and more about the story,

[01:04:17] Tony: so it was fun, interesting, worth watching.

[01:04:20] Cameron: Holds up well.

[01:04:21] Tony: Yeah, I liked it.

[01:04:24] Cameron: Very good. I’ll have to check it out. I finished, uh, Chrissy and I finished True Detective.

[01:04:31] Tony: Yeah.

[01:04:32] Cameron: but yeah, like the, it wasn’t the ending I was expecting. Uh, but I liked it.

[01:04:38] Tony: Wasn’t I? It was good, wasn’t it? Because it basically resolved everything back to practicalities and the woo woo goes

[01:04:43] Tony: away, which I really enjoyed.

[01:04:44] Cameron: Yeah. Yeah. I was kind of waiting for something big and then it was like, Oh, okay. I’ll pay that. Yeah. Sort of. It was a little bit anticlimactic, but I liked it. Yeah.

[01:04:56] Tony: Yeah.

[01:04:57] Tony: so I’ve had the same reaction, anticlimactic and realistic, and you kind of fed it in along the way that the police report, or the report comes in saying that this is the reason why the men were all killed, and straight away Jodie Foster thinks, oh you’re covering it up, can’t be that, yeah,

[01:05:16] Cameron: Yeah.

[01:05:16] Tony: and as

[01:05:17] Tony: it turns out, she works it out

[01:05:18] Tony: as well.

[01:05:19] Cameron: I like it when she and her offside would go to visit the women and the women are like, yeah, it’s what we did. And they’re like,

[01:05:28] Cameron: Okay, well, just wanted to let you know.

[01:05:34] Tony: Yeah, it still had that sort of small town vibe to it, didn’t it?

[01:05:38] Cameron: yeah,

[01:05:38] Tony: Yeah, I loved it. I thought that was great. Really, really

[01:05:41] Tony: realistic ending.

[01:05:42] Cameron: yeah, yeah, it’s sort of, they tied a bow around it nicely, in a way. Like the woo woo stuff, I went along with it, but I’m like, uh, really? But then they tied a nice bow around it at the end, so it was good.

[01:05:56] Tony: Yeah.

[01:05:57] Cameron: I started watching Mr. and Mrs. Smith. You watched any of that yet?

[01:06:02] Tony: No. It’s been on my

[01:06:03] Tony: list, but I haven’t gotten around to it.

[01:06:04] Tony: Is it good?

[01:06:05] Cameron: Don’t know yet. I’m only one and a half episodes in. Um, the cast is good. And the reason I ended up watching it is I am a big fan of Donald Glover and his series, Atlanta. I don’t know if you’ve ever seen Atlanta, but one of the best things that’s been on television in the last five or six years. Oh, yeah.

[01:06:24] Cameron: Well, if you’re, you know, if you like the kind of stuff that Chrissy and I like, I mean, it’s, um, set in Atlanta about a couple of black guys, one, you know, from the, you know, the, the suburbs of Atlanta, one, one’s a rapper who has some success and Donald Glovers is. cousin who becomes his manager because he just needs a manager and he’s never done it before.

[01:06:49] Cameron: And then they got the best friend who’s a bit of a spacey druggie, but it’s, it’s one of these things. It’s all black cast, black writers, black directors telling a story of, you know, a black person, African American story in Atlanta. And I kind of like that. I kind of like when you see different.

[01:07:09] Cameron: Perspectives and stories told from different perspectives. There’s a lot of stuff about, you know, there’s a lot of it is about what it’s like to be black in America, you know, even if you’re

[01:07:18] Tony: Mm

[01:07:19] Tony: hmm.

[01:07:20] Cameron: rich and famous, just the level of racism and, and how crazy white people are and all this kind of stuff that goes along with it.

[01:07:29] Cameron: And it’s, and it’s also a little bit sort of surrealist. As the series goes on, it’s just surrealist episodes that you’re like, well, that had nothing to do with the, there’s no overarching story arc really about, except for these three guys and their lives. But it’s just every now and again, you get an episode and you’re like, Oh, I didn’t see that coming.

[01:07:49] Cameron: But my point is that, um, Mr. and Mrs. Smith, loosely based on the same premise as the Angelina Jolie, Brad Pitt film from the nineties, husband and wife assassins. Um, But it’s written by and produced by Donald Glover, as was Atlanta originally, and it’s the same director from Atlanta, so it looks like he’s taken his same crew and they’ve tried to do something that’s a little bit more mainstream and a little bit more sort of shit blows up and people get shot and, you know, that kind of stuff.

[01:08:25] Cameron: So, uh, I don’t know. I don’t know how it’s going to work, but I like the people behind it. That’s always, for me, it’s a good enough reason to give something a fair shake of the leg. Um,

[01:08:37] Tony: stories from a particular area, ethnicity, etc., and being true to that. That was one of the themes of Emerald City. And I remember reading it a ton. Apparently David Williamson wrote this, the play, as a response to Spielberg optioning Thomas Keneally’s Schindler’s Ark and it’s, they talk about, um, plays being taken over to the States and, um, the, one of the themes in the, in the Emerald City is that there’s a black writer who has a novel and it wouldn’t get published and then, um, Long story short, it does.

[01:09:13] Tony: And it gets shortlisted for the Booker Prize, and then Spielberg options it. And, y’know, John Hargrove says, So we’re gonna see some aliens with the blacks, are we?

[01:09:22] Cameron: yeah. And then the aliens arrived.

[01:09:25] Tony: it, yeah, I

[01:09:26] Tony: told you

[01:09:28] Cameron: been trying to watch the latest Indiana Jones film too, which I know Spielberg didn’t direct, Mangold did, but, uh, I tell you an interesting thought I had. So I was watching, have you seen it? I think you saw it, right?

[01:09:44] Tony: Indy Jones. I love the way, in the action scenes, he takes about two steps to run into camera. That’s meant to be him running along

[01:09:52] Tony: to get to the scene.

[01:09:54] Tony: It’s great.

[01:09:54] Cameron: Well, I’m only about, I don’t know, maybe halfway through. I keep getting interrupted when I try and watch it, but in the first 10 or 15 minutes, it’s set in World War II, and they’ve de aged Harrison Ford.

[01:10:06] Tony: hmm.

[01:10:07] Cameron: so I was watching it at some point thinking, okay, I know that they’ve used CG and AI to de age Harrison Ford.

[01:10:16] Cameron: I know that the va everything else that’s going on is CG. You know, explosions and running on the top of the train and all this kind of stuff, it’s all CG. Harrison Ford’s basically AI at this stage. If it was just full AI that had recreated his face and his voice, if this was, like, it’s already 85 percent digitally created effects.

[01:10:46] Cameron: If it was 100%, would my appreciation of it be much different? Because I’m accepting the fact that it’s all CG, all the special effects and everything. I’m accepting the fact that they’ve de aged Harrison Ford to make him look like he did in the 80s.

[01:11:05] Tony: Mm hmm.

[01:11:07] Cameron: Am I really gonna give a shit if it’s just, you know, go the extra notch and just remove all the real actors and make it all CGA?

[01:11:14] Cameron: Even, you know, with the de aging, it’s pretty good. I mean, I thought this is the best de aging job I’ve seen so far. Like, the rest of them in the Star Wars films and Uh, the, the Star Wars, the, the Mandalorian, I don’t know if you saw them do Mark Hamill in the Mandalorian.

[01:11:31] Tony: Yeah.

[01:11:32] Cameron: They’re good, but they’re not great, they’re still a little bit sort of Uncanny Valley ish, you know.

[01:11:39] Cameron: This, I didn’t really get it, oh, and, and of course the Irishman as well, which was pretty good. Um, but I’m not getting any sort of, Ooh, this is, doesn’t look quite right thing with me. I’m buying that it’s a young Harrison Ford.

[01:11:51] Tony: And I think one of the reasons for that, sorry to interrupt. I think one of the reasons is it, um, like in the Irishman, you had a young face, but everything else was real. But in the Harrison Ford movie, you’ve got a young face, which is CGI, running on a train, which is CGI, like everything CGI. So it’s, it’s, I think that helps make the, the aging

[01:12:09] Tony: process look real.

[01:12:09] Cameron: Also, it was made three or four years later and like the technology

[01:12:13] Cameron: is improving leaps and bounds. So it was just interesting for me thinking, yeah, I probably, I’m not going to care when it’s all, when it’s all AI generated, I don’t know that I’m going to give a shit. And I thought I would,

[01:12:26] Cameron: but.

[01:12:27] Tony: Hence the,

[01:12:27] Tony: riders

[01:12:28] Tony: strike.

[01:12:29] Cameron: Yeah, yeah, which kind of was pointless really. I’ve read the provisions that they put into it and it’s not worth much. Easy to get around. But speaking of AI, I heard about this story and so I dug it up. I’ve been reading this collection of Isaac Asimov’s science fiction short stories

[01:12:50] Tony: Oh, good.

[01:12:51] Cameron: and there’s one called The Feeling of Power from 1958. I was wondering if you’d ever read it.

[01:12:57] Cameron: I know you’ve.

[01:12:58] Tony: Oh, I’m sure, I, sure I

[01:12:59] Cameron: Yeah, you’ve read most of his

[01:13:01] Tony: Big Asimov. Yeah. Big

[01:13:02] Tony: Asimov

[01:13:03] Cameron: in the introduction to the collection that I’m reading, which I think he wrote late in life, so he died like early 90s I think, so I think he was writing this introduction late 80s early 90s, and he talked about the fact that robotics was now a field and took credit for the fact that he invented the word robotics, um, kicking himself for not calling the brain of the robots a computer, calling it a positronic brain, Yeah.

[01:13:31] Tony: Remember

[01:13:31] Cameron: And it’s quite, it’s quite a, quite a nice intro, because he’s sort of talking about the risks that you run, even as a hard science guy, like he was, trying to forecast into the future things he got wrong, the things he didn’t. And God, I wish he was alive now. I wish guys like him, and Clark, and, um, Robert, uh,

[01:13:51] Cameron: whatever his name

[01:13:51] Tony: Highland.

[01:13:52] Cameron: Highland, yeah. And, and um, uh, the guy who wrote Blade Runner, whose name escapes me.

[01:14:00] Tony: Oh, Philip k

[01:14:01] Cameron: Yeah, PKDick. Oh jeez, God, I wish those guys were around now to see what’s happening because, you know, it’s all of their stuff is starting to come true with the robots that we’ve got now. Anyway.

[01:14:15] Tony: Yeah. And, and William Gibson. There’s

[01:14:18] Cameron: Yeah, well he is around,

[01:14:20] Tony: he’s around. Yeah. There’s a current crop that’s still around, for

[01:14:23] Cameron: Neil Stevenson,

[01:14:24] Tony: Yeah.

[01:14:25] Cameron: guy I interviewed years ago, Verna Vinge, I interviewed him like early on in podcasting, 20 odd years, nearly 20 years ago, he’s still around. Anyway, um, in this particular short story, it’s set in the far future where everything is done by computers and people have forgotten that mathematics is a thing.

[01:14:45] Cameron: And this guy comes up with the ability to do mathematics on paper and at first they think it’s a trick. And then he proves it, and he shows that not only addition, but he can do subtraction, multiplication, division, and then it starts to become, the military get involved, because they’ve reached a, like an impasse with their big enemy, this other planet, where they’re all building computers And they’re like, well, all of the missiles, they’re like, if we could build a missile where you didn’t have to use a computer to figure, to be on board to generate the coordinates or the targeting, if you could have a human drive it and manipulate it, it’d be cheaper, faster, lighter.

[01:15:31] Cameron: Um, and they’re looking for. Something that’s not computer driven to be the secret weapon that they have. And then they, the technician who came up with the ability to do maths, um, just as a, he just thought it was a fun hobby, ends up realizing that what he’s built is going to kill people, so he kills himself and they sort of don’t care.