Hello QAVvers

If you want my body and you think I’m sexy,

Come on, sugar, let me know.

“Do You Think I’m Sexy”, the Rod Stewart cover by Queen Of Japan (click photo below to listen to the track)

What does that have to do with investing? Well… I think that’s what the AORD is singing to itself right now.

To put it into a ten year perspective:

It’s been a rocky couple of years for investors, but here we are, back at all-time highs. The AORD is up 11% since November 1 (as is our Dummy Portfolio) and I feel sorry for those investors who capitulated during last year’s downturns are missing out on all of this growth.

Sure — a market at an all-time high is pretty sexy. But the trick to long-term success as an investor is to be fully invested when the market *isn’t* sexy, when it’s been downright hit with the ugly stick. The we kiss it and watch that frog turn into a prince. Or something like that.

In other words:

It’s cycles, Jerry, cycles.

Let’s have a look at the portfolios.

QAV PORTFOLIO REPORT

The Dummy Portfolio is performing well against the benchmark over most time frames.

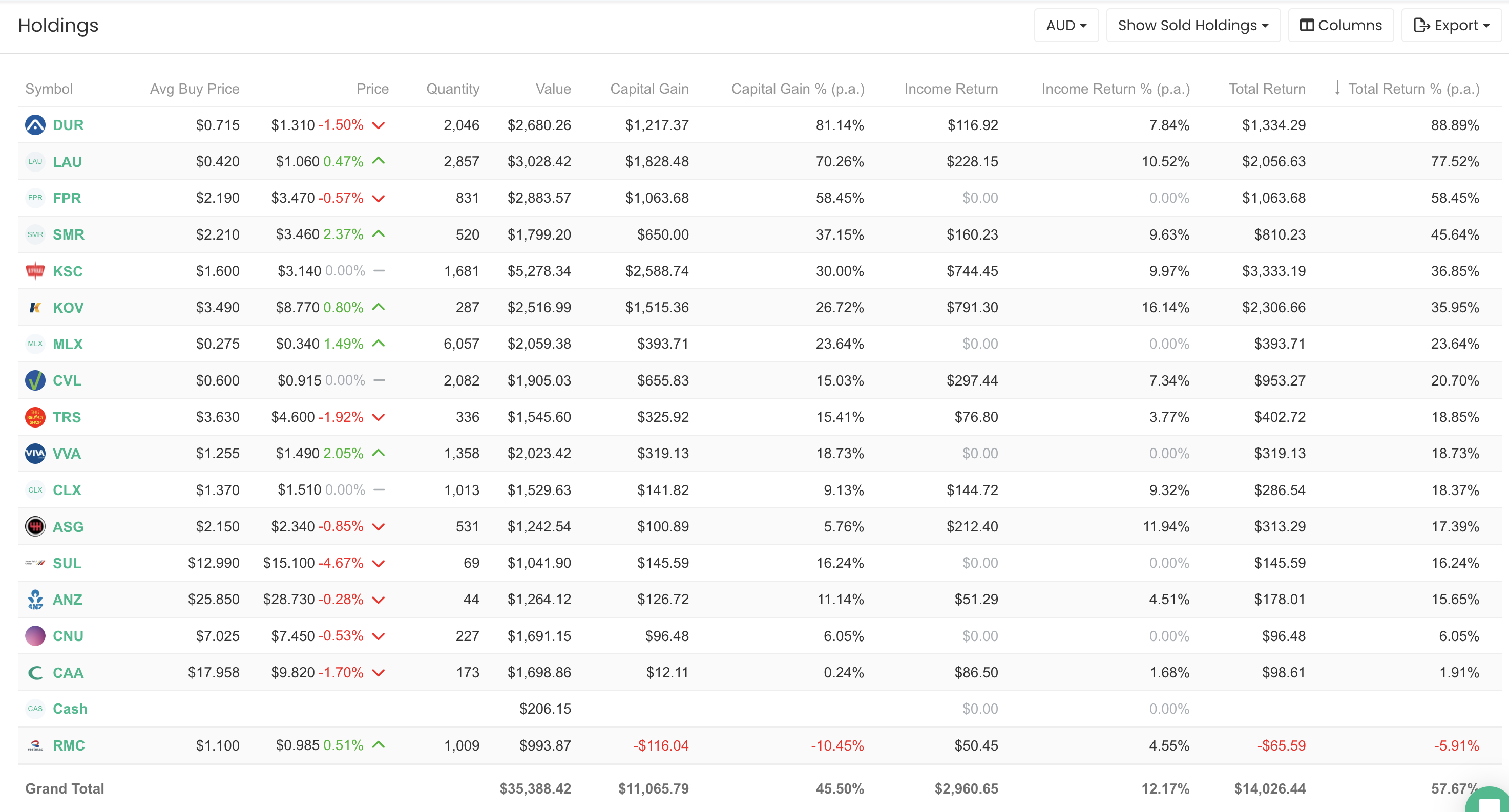

CURRENT HOLDINGS

SINCE INCEPTION (15/04/2019)

Our portfolio is still doing slightly less than double market p.a. since inception (roughly five years). In real terms, the value of the portfolio has increased 75% in 5 years.

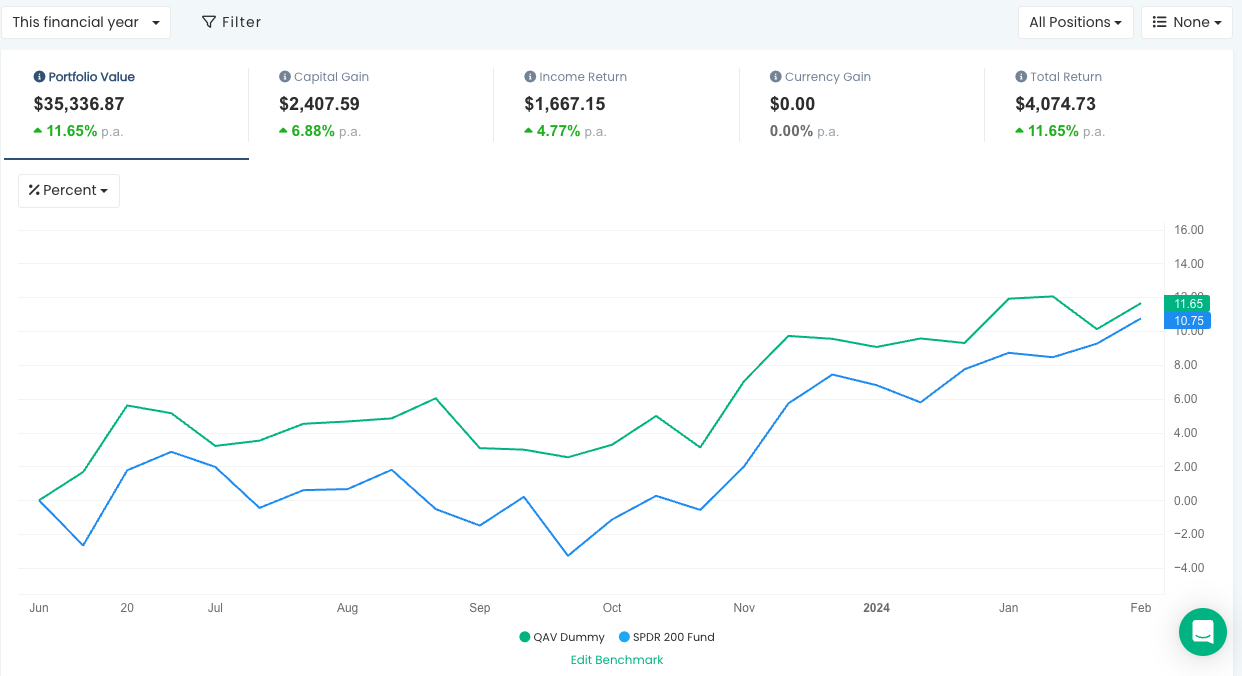

CURRENT FY

We’re outperforming the benchmark for the FY, too.

The big winners for us in the last week were MLX (+16%) and SMR (+10%).

RECENT TRADES

No trades in the last week.

QAV STOCKOPEDIA DUMMY PORTFOLIO REPORTS

QAV AU DUMMY

The Australian Stockopedia portfolio is still underperforming since inception. But its performance since 20 July 2023 is about the same as the 231 Light portfolio, so I don’t know if the performance has anything to do with the Stockopedia limitations.

QAV US DUMMY

The US portfolio is up, but still underperforming the S&P, which, as we know, is largely being driven by the Mag7 stocks, Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla. I’m actually quite happy with our performance on this one.

STOCKS OF THE WEEK

During the last week, we also traded some stocks in our Light portfolios. Details here.

** As always, please check our work, DYOR, and consult a financial advisor before making any investing decisions.

BUY LIST

Each week we produce a buy list that we share with our members. The intended primary purpose of this buy list is for club members to use as a reference for comparing their own buy list. In theory, all of our buy lists should look pretty similar each week.

As always, please check our work, DYOR, consult a financial advisor before making any investing decisions.

THIS SECTION CONTAINS CONTENT WHICH IS VISIBLE TO QAV CLUB SUBSCRIBERS ONLY.

LAST WEEK’S EPISODE

This week: We discuss our favourite bits of Buffett’s new annual letter, and Tony does a pulled pork on Vulcan Steel (VSL).

Also in the Club Edition: We discuss the results of a new 20% Rule 1 simulation, Reporting Season News, LNG is a sell, Data shows Cathie Wood’s Ark is one of the worst funds, NVIDIA results, and TK’s perspective on ‘Losing too many stocks’ to M&A.

Episode Transcription

QAV 709 Club

[00:00:00] Tony: One, two, three, go!

[00:00:10] Cameron: No.

[00:00:12] Tony: Bush line. that from Butch and Sundance? Uh, I think it was Richard Kiel, the guy who played Jaws in the Bond movies. If it wasn’t him, it was like another big, big bad guy. Challenges Newman to a fight. Newman’s about half his size, and he goes Well, if we’re going to fight, someone needs to say one, two, three, go.

[00:00:32] Tony: And Redford says, one, two, three, go, and Newman kicks him in the nuts straight away. That’s end of the fight.

[00:00:41] Cameron: That’s good. Welcome back to the bullshit. No, uh, QAV. Watch. Ray and I do that all the time. I’ll be sitting down. Welcome to the, what are we doing? What shows this? It is the never ending podcast. In fact, that’s, my son Hunter has been telling me for months, I should just combine all of my podcasts into the Cameron Reilly show and just, and just do, it’s just all, you know, just me talking about stuff.

[00:01:14] Tony (2): Right, and bring a co host on as a guest.

[00:01:17] Cameron: Well, basically, I have different co hosts for different topics, but it’s just, you know. He said, cause I don’t want to subscribe. He said, no one wants to subscribe to four or five different shows. If they’re listening to you, it’s probably cause they like you and they’re interested in what you’re interested in.

[00:01:29] Cameron: So just let them listen to you and you talk about whatever you’re talking about and they’ll just go along for the ride.

[00:01:35] Tony (2): You could do what Kramer did. You could put the Merv Griffin set in your lounge room.

[00:01:40] Cameron: My God. I just watched that episode like two days ago. Yeah. I watched it on the weekend.

[00:01:45] Tony (2): That’s a great episode. Yeah,

[00:01:49] Cameron: was cleaning up, doing dishes or something and I

[00:01:51] Cameron: was gonna, and it was in the thing. I said, Oh, this is a great one. Got to watch this. It is a great episode. Anyway, welcome back to QAV, episode 709, 27th of February, 2024.

[00:02:06] Cameron: Warren Buffett’s annual letter to shareholders came out this week. Tony, it’s always, I mean, a little bit, a little bit bittersweet this time because he had to do the, We didn’t have to, but he did the big tribute to Charlie Munger.

[00:02:20] Tony (2): thought that was a nice touch.

[00:02:22] Cameron: It was lovely, lovely. And, um, I’ve got, I thought we’d start maybe with our highlights from Warren’s

[00:02:30] Cameron: letter.

[00:02:31] Tony (2): two hours, we can do the regular podcast.

[00:02:37] Cameron: easy content when Warren writes a letter.

[00:02:40] Tony (2): It’s a late Christmas present, isn’t it?

[00:02:42] Cameron: it really is. And it never ceases to amaze me. Just. How much I enjoy it and how much good stuff there is. He’s so easy with the, you know, the wit and wisdom. Um, so of course he opened with his, uh, tribute to Charlie where he basically gives Charlie all of the credit for Berkshire Hathaway being what it is.

[00:03:06] Cameron: today, which is a news. He’s always done that, but he reaffirmed that as Charlie’s gone. Um, I think towards the end of his tribute, I’ve got this bit. He said, In the physical world, great buildings are linked to their architect, while those who had poured the concrete or installed the windows are soon forgotten.

[00:03:27] Cameron: Berkshire has become a great company. Though I have long been in charge of the construction crew, Charlie should forever be credited with being the architect. Beautiful.

[00:03:36] Tony (2): Yeah, it’s a great sentiment, isn’t it? It’s typical Warren not taking credit, calling himself the window installer, Charlie the architect. And if I can just chip in with mine too, from that same page, and, and, if, people have probably read this or they’ve gone to the site, the, the, The normal Berkshire Hathaway letter starts after the homage to Charlie and the homage to Charlie is in bold font and larger font and it’s, it’s a real tribute.

[00:04:04] Tony (2): Um, my, my take on that was just before yours. Charlie never sought to take credit for his role as creator. But instead, let me take the bows and receive the accolades. In a way, his relationship with me was part older brother, part loving father. Even when he knew he was right, he gave me the reins. And when I blundered, he never, never reminded me of my mistake.

[00:04:28] Cameron: Such a sweet relationship those guys had.

[00:04:31] Tony (2): Yeah. And, you

[00:04:33] Cameron: remember

[00:04:34] Tony (2): sorry, well, they talk about never fighting as well over what,

[00:04:37] Cameron: That’s what I was going to

[00:04:38] Tony (2): Yeah. All right. Yeah.

[00:04:40] Cameron: I think that was in, um, the last Wit and Wisdom of Charlie that I read, which, you know, Warren’s been in that. He probably wrote 20 years ago, but he was saying they’d never had an argument, never had a fight in all the time that they’d worked together.

[00:04:53] Cameron: Disagreed on stuff, but never had an argument, never had a fight. So yeah, really special relationship.

[00:04:59] Tony (2): Yeah. Well, I think we’ve had a fight, have we, Ken? In

[00:05:03] Cameron: No,

[00:05:04] Tony (2): 12 years?

[00:05:05] Cameron: no, but we don’t work as closely as they

[00:05:07] Tony (2): true. Yeah, in the high

[00:05:12] Cameron: yeah,

[00:05:12] Tony (2): world of being CEO of one of the biggest companies in the world, yeah.

[00:05:18] Cameron: yeah. I mean, Ray and I have never had a fight either. We’ve never had a disagreement, never had an argument, never had a fight in the 10 years that we’ve been recording shows together. It’s great. Like he’s,

[00:05:26] Tony (2): It’s just because Ray just always agrees with you.

[00:05:29] Cameron: Well, that’s, yeah, like you.

[00:05:33] Cameron: When I screw up

[00:05:34] Tony (2): this might be our first fight.

[00:05:39] Cameron: When I do something stupid, you just, you just giggle and, you know, that’s about it. You know, you’re like my Sifu. I say that, it’s my Sifu. My Sifu walks up to me at Kung Fu and if I’m doing something wrong, he just looks at me and he just chuckles and walks away. And that’s how I know I’m doing something wrong.

[00:05:56] Cameron: I’m like, what? What? He goes, uh You know, you can do it that way if you want. Come to think of it, the two of you have got a lot in common.

[00:06:08] Cameron: You know, it’s, that’s, uh, my favorite kind of mentor is the one that doesn’t sort of make me feel bad. Just chuckles and walks away.

[00:06:17] Tony (2): Well, it’s a bit like raising a child. I mean, I forget now where I read it, but there’s two things. To successfully raising a child, one was unconditional love, like the child’s got to know that whatever they do, they’ll still be loved. And the second thing is operant conditioning. So if you do something bad, it just gets ignored by the parent.

[00:06:36] Tony (2): But if you do something good, you get random praise for it. And eventually the kid learns to seek random praise for doing good things and, and less and less bad things.

[00:06:48] Cameron: hard when they’re smashing everything in the house.

[00:06:52] Tony (2): Oh yeah, I mean, yeah. It is.

[00:06:56] Cameron: I read that in books. I’m like, yeah, come and look after Fox for a day and then get back to me.

[00:07:01] Tony (2): Well, I mean, yeah, I don’t know. Maybe there’s something else behind that. Didn’t you say there was a medical reason behind that?

[00:07:08] Cameron: Yeah. Yeah. One of many.

[00:07:10] Cameron: reasons behind that, I don’t know.

[00:07:13] Tony (2): Right. Well,

[00:07:14] Cameron: child.

[00:07:14] Cameron: That’s the

[00:07:15] Tony (2): oh, is that what it is?

[00:07:16] Cameron: Yeah, yeah.

[00:07:17] Tony (2): It’s her fault. Right.

[00:07:19] Cameron: Not false. I’m not casting blame. I’m just saying. It’s DNA, man. It’s just genetics.

[00:07:26] Tony (2): Oh,

[00:07:26] Tony (2): you mean, I mean, he worked out his genetics and ever since he’s been throwing tantrums and breaking things in the house.

[00:07:33] Cameron: Yeah, that’s it.

[00:07:34] Tony (2): Yeah.

[00:07:36] Cameron: Anyway, back to Warren. Our goal at Berkshire is simple. We want to own either all or a portion of businesses that enjoy good economics that are fundamental and enduring. Within capitalism, some businesses will flourish for a very long time, while others will prove to be sinkholes.

[00:07:53] Cameron: It’s harder than you would think to predict which will be the winners and the losers. And those who tell you they know the answer are usually either self delusional or snake oil salesmen. I like that.

[00:08:07] Tony (2): I agree wholeheartedly.

[00:08:09] Cameron: We buy companies because we think their fundamentals look good, and sometimes they go south,

[00:08:14] Cameron: and

[00:08:14] Tony (2): Mm hmm.

[00:08:15] Cameron: just the way it is.

[00:08:17] Tony (2): Yeah, it’s, it’s, I think Warren’s always said it’s a probabilistic exercise. You hope to get slightly more right than you get wrong, but it’s, it’s impossible to predict.

[00:08:30] Cameron: Do you want to do one for one here? You

[00:08:32] Cameron: got some

[00:08:32] Tony (2): I hope you like it. Yeah, I do. I’ve got quite a lot to do. You were talking before about Warren’s ability to distill things into good prose and one of the concepts I liked about this letter was he was talking about his sister Bertie and I guess using her as a proxy for One of the investors, long term investors in Berkshire Hathaway.

[00:08:53] Tony (2): So his sister Birdie’s been along as an investor for a very long time. And Warren says in the letter, Birdie, like most of you, understands many accounting terms, but she is not ready for a CPA exam. She follows business news, reading four newspapers daily, but doesn’t consider herself an economic expert.

[00:09:12] Tony (2): She is sensible, very sensible, instinctively knowing that pundits should always be ignored. After all, if she could reliably. Predict tomorrow’s winners. Would she freely share her valuable insights and thereby increase competitive buying? That would be like finding gold and then handing out a map to the neighbors showing its location.

[00:09:32] Cameron: Although that’s exactly what he’s been doing for 60

[00:09:35] Cameron: years.

[00:09:36] Tony (2): think he has. That’s, I think that’s the distinction. I think what he’s saying there is. Don’t trust a stock tipper, but he’s saying, but he’s been teaching how you invest in the whole time and saying, you know, I’m not giving you tips. He’s never come out with a stock tip in his life, but he said, this is how I do it.

[00:09:53] Tony (2): I think that’s a bit different.

[00:09:55] Cameron: Oh, that’s a fair distinction. Yeah. He’s teaching a methodology, but not giving you tips.

[00:10:00] Tony (2): Yeah. And that was, look, when I started QAV, I got so much feedback from my friends and colleagues saying, why are you giving away your secrets or why are you, you know, and. Um, I think, you know, I came to the same conclusion. I’m not giving away my secrets. I’m teaching people how to invest for themselves and it’s up to them what they buy and sell.

[00:10:23] Cameron: And now you’re starting to question.

[00:10:28] Tony (2): Well, yeah, we’ve had that discussion in the survey about whether we’re all buying at the same time and selling at the same time. It doesn’t appear to be the case, but we may have to look at that again in the future.

[00:10:38] Cameron: Keep an eye on it. In 1863, Hugh McCulloch, the first Comptroller of the United States, sent a letter to all national banks. His instructions included this warning, Never deal with a rascal under the expectation that you can prevent him from cheating you. like that. And then he goes on to say that, you know, he and Charlie tried to follow that, uh, philosophy, and they’ve, they’ve been tricked a couple of times, because it’s hard to tell who the bullshit artists are, but, uh, I like that.

[00:11:09] Cameron: Never, just, if you know someone’s a rascal though, don’t think you’re gonna, why, why, why walk into the lion’s den, like, you know, I say this to my boys all the time, like, they do business with someone, and then get a sense that that person is not trustworthy,

[00:11:29] Tony (2): Mm hmm.

[00:11:29] Cameron: a bit like real estate

[00:11:30] Cameron: agents,

[00:11:31] Tony (2): I had that same thought.

[00:11:35] Cameron: and if somebody tells you that they’re bullshitting about something to somebody else.

[00:11:39] Tony (2): Yeah.

[00:11:40] Cameron: As part of their standard business practice, why would you trust them to be honest with you?

[00:11:45] Tony (2): No, I agree. Why are you special?

[00:11:47] Tony (2): Yeah,

[00:11:49] Cameron: or a business partner slash boss years ago. Like, working with him and seeing him just lying and cheating to suppliers and customers.

[00:11:58] Cameron: And then you go, okay, well, obviously you’re going to be doing that to me as well, right? That’s your character.

[00:12:05] Cameron: Yeah,

[00:12:05] Tony (2): I had the same, same thing with, issue with the boss once and came to the same conclusion. It’s just not worth working with them.

[00:12:12] Cameron: if you can,

[00:12:13] Cameron: you know,

[00:12:14] Tony (2): If you can, yeah. And, um, and Buffett in the past has said things like, you know, consider, consider the fact that whatever you do today might be on the front page of the newspaper tomorrow.

[00:12:24] Tony (2): So. Reputations take a lifetime to gain and a day to lose.

[00:12:32] Cameron: Yeah, and I can, I mean, life’s just too short to deal with idiots

[00:12:37] Tony (2): Yeah.

[00:12:38] Cameron: arseholes too, like, that’s why you and I got out of the corporate workforce in the first place, right?

[00:12:44] Tony (2): Well, that was a question I had too. I wonder how many banks out there, if they got rid of all the rascals. I wonder how big they’d be. I wonder who’s

[00:12:51] Tony (2): left. Wouldn’t be a whole

[00:12:53] Tony (2): lot.

[00:12:54] Cameron: Gets back to the psychopath epidemic in a way, too.

[00:12:56] Tony (2): that’s right.

[00:12:58] Cameron: Alright, your turn.

[00:12:59] Tony (2): Uh, yeah, so I, I won’t go through it all, but they, Warren does his usual, um, rant about, uh, general accounting principles and how what they publish is their net income for the core, there isn’t really a net income because it includes the unrealized gains in their investment.

[00:13:16] Tony (2): Investments. Um, and he does this every year, but then he goes on to talk about his, what they call operating earnings, so it’s their share of the profits, basically, based on their equity holdings. And, you know, he says that in 2021, they made 27. 6 billion, in 2022, 30. 9 billion, and 37. 4 billion last year, so it’s going up under his, under his version of the accounting standards.

[00:13:43] Tony (2): I think I’ve read this same discussion in every letter that Warren Buffett’s ever written, and given that he is one of the wealthiest men in America, and the CEO of one of the biggest companies is not the biggest, why isn’t he lobbying for the accounting standards to change? Why does he just keep rowing against us every year?

[00:14:00] Tony (2): If he thinks he has to State his earnings in a different way every year and his earnings are misstated. Why not go to the SEC or whoever looks after it and say, Hey guys, this isn’t working. Even if you have to give me a carve out because I’m an investment company, let’s, let’s get it, let’s get it right.

[00:14:16] Tony (2): I

[00:14:16] Cameron: Why isn’t the SEC

[00:14:18] Tony (2): Yeah, yeah,

[00:14:26] Tony (2): exactly. Yeah, it’s just a strange circumstance, I think.

[00:14:30] Cameron: Well, maybe that ties in with this next quote I’ve got. He says, Berkshire’s ability to immediately respond to market seizures with both huge sums and certainty of performance may offer us an occasional large scale opportunity. Though the stock market is massively larger than it was in our early years, today’s active participants are neither more emotionally stable nor better taught than when I was in school.

[00:14:55] Cameron: For whatever reasons, markets now exhibit. far more casino like behavior than they did when I was young. The casino now resides in many homes and daily tempts the occupants. One fact of financial life should never be forgotten. Wall Street, to use the term in its figurative sense, would like its customers to make money.

[00:15:16] Cameron: But what truly causes its denizens juices to flow is feverish activity. At such times, whatever foolishness can be marketed, will be vigorously marketed. Not by everyone, but always by someone. Occasionally, the scene turns ugly. The politicians then become enraged. The most flagrant perpetrators of misdeeds slip away.

[00:15:39] Cameron: Rich and unpunished, and your friend next door becomes bewildered, poorer, and sometimes vengeful. Money, he learns, has trumped morality. That always fascinates me when one of the richest guys and most successful investors in America sounds like a Marxist. He sounds like a, he sounds like a lefty. Yep, the rich, the rich slip away unpunished, it’s all marketing and no one knows what, you know, it’s more casino like behavior than ever.

[00:16:09] Cameron: You know, this is coming from Warren

[00:16:12] Cameron: Buffett. I wouldn’t be surprised if I read that on the Chomsky subreddit, you know,

[00:16:16] Tony (2): Right, yeah.

[00:16:17] Cameron: hmm.

[00:16:18] Tony (2): Yeah, that’s what I’ve always liked about him. And he’s always been fairly progressive for a Republican. Um, but, but yeah, and he’s

[00:16:24] Tony (2): He’s

[00:16:24] Cameron: a Republican?

[00:16:25] Tony (2): Yeah, a moderate

[00:16:27] Cameron: a Democrat?

[00:16:28] Tony (2): No, I thought he was a moderate Republican because he was,

[00:16:31] Cameron: is a Democrat, I

[00:16:31] Cameron: think.

[00:16:32] Tony (2): yeah, okay, possibly, because he was, um, an advisor to Arnold Schwarzenegger when he was California State Governor.

[00:16:38] Tony (2): on financial issues. And his father was

[00:16:41] Cameron: to Obama too,

[00:16:42] Cameron: though.

[00:16:42] Tony (2): oh, was he? Okay. And his father was a Republican Senator.

[00:16:46] Cameron: Yeah, right.

[00:16:47] Tony (2): Yeah. So I’m pretty sure he’s Republican. Not that it matters. He’s moderate, um, in many ways. Um, but yeah, I mean, he’s Deb Wright again, and that’s, he’s, he’s actually making a really interesting point. And that is that just like you and I, that the sort of what used to be The realm of investment bankers and fund managers is now available to households to invest with a fair, fair degree of information to back up their decisions.

[00:17:14] Tony (2): And so people still have to be careful and not be tempted because they have access to the stock market much more easily. They can do it online themselves for a very cheap cost, not to treat it like a casino. And of course, we’ve seen that. We’ve spoken about it on the show during COVID when people had access to their SEPA and they drew it down and then spent it.

[00:17:35] Tony (2): Um, you know, gambling Bitcoin or whatever and he, yeah, he didn’t mention Bitcoin in that, in that commentary, but it just flashed out to me that that’s one of the things he was talking about.

[00:17:47] Cameron: And it’s, you know, it’s the same thing going on with the Magnificent Seven shares at the moment. Like, okay, I fundamentally agree with the premise that AI is going to be revolutionary and that these companies are probably going to profit, uh, some of them anyway, out of the AI boom in the next few years.

[00:18:05] Cameron: But how do I, how do I value a share of Nvidia? How do I value a share of Google and decide that I’m buying it at a good price based on, you know, some sort of scientific valuation apart from it’s going up and it was, it might go up in the future. I mean, at the end of the day, if I was going to buy one of those shares, that’d probably be the only I could have for it is that, wow, it’s been going up and it might keep going up, which

[00:18:35] Cameron: is casino behavior.

[00:18:37] Cameron: It’s, it’s well, and that

[00:18:39] Cameron: too.

[00:18:39] Tony (2): Yeah. I can sell it to someone for a higher price. Yeah.

[00:18:42] Cameron: Yeah, there’s no, you know, logic, reason, really, apart from, you can say AI and mumble off some buzzwords about, you know, this time it’s different, but at the end of the day, if you’re gonna put your big boy or big girl pants on and say, no, no, I’m a rational investor who invests in good quality companies when I can buy them at a discount to their intrinsic valuation, then try and apply that to the Magnificent Seven.

[00:19:09] Cameron: Unless you know something that I don’t know, it’s very, very hard to put your hand on your heart and say that’s what you’re doing, I

[00:19:14] Cameron: think.

[00:19:15] Tony (2): And I’ve had discussions even with some of our listeners in the past, um, at dinners, et cetera, where they’ll say things like, Oh, I bought some Bitcoin yesterday. Oh, really? And they go, Oh, look, it was only 1 percent of my total portfolio. I just wanted to try it. I’m like, okay, well, it’s good to experiment.

[00:19:31] Tony (2): But would you put a hundred percent of your portfolio in it? And if you don’t do that, if you’re not going to, if you go, Oh, no, it’s a bit risky. Well, I risk 1%. Yeah, it’s just strange how the human brain works. It’s like taking, it’s like taking a bit of money to the casino and having a splash rather than applying all the principles you apply for 90, the other 99 percent of your, um, yes, or the racetrack.

[00:19:55] Tony (2): Exactly. I didn’t tell you I had a good win on the weekend at the racetrack.

[00:20:00] Cameron: Oh yeah?

[00:20:01] Tony (2): yeah?

[00:20:03] Tony (2): we own it. Steve Mabb and I own it. Oh, I’m. a large part of a horse and its sister won the Blue Diamond, which is a big group one race in Melbourne on the weekend. So, um, we’re hoping for some of that luck to rub off on our horse, but I backed it in the one at 20 to one.

[00:20:19] Tony (2): So that was a great result.

[00:20:21] Cameron: And, and to be fair, when you play the horses, you have a system, you have some sort of a scientific system.

[00:20:28] Cameron: Are you, is it net positive?

[00:20:30] Tony (2): Uh, it’s probably break even over the years, some years ago, some years ago. I, I treated it as entertainment really. So that positive this year for sure.

[00:20:39] Cameron: And you could, could you, could you say the same about buying Bitcoin? It’s just entertainment.

[00:20:43] Tony (2): I could, yeah. So I accepted the person that spent 1%. of their

[00:20:48] Cameron: It’s gambling,

[00:20:49] Tony (2): doing it, is gambling. Or, you know, they can say it’s experimenting, but it’s an experimental gamble. And it’s entertaining, so I don’t have a problem with it, but I’m just saying it, you know, flip it on its head, would you put the other 99 percent into Bitcoin?

[00:21:02] Tony (2): And if you don’t do that, then why put the one in?

[00:21:05] Cameron: And you should also spend 1 percent of your time smoking meth and, uh, you know, looking for a good time in all the wrong places.

[00:21:14] Tony (2): Just in case it works. Yeah,

[00:21:16] Cameron: Yeah, just in case it works, you know, you know, you know, works for some

[00:21:18] Cameron: people, might

[00:21:19] Tony (2): Hey, well, we don’t, we don’t know it doesn’t.

[00:21:21] Cameron: That’s what I’m

[00:21:22] Tony (2): I don’t. I don’t know? it doesn’t. No. Yeah.

[00:21:28] Cameron: turn is it? Yours?

[00:21:32] Tony (2): Um, he made a good point, which is often at the crux of what he talks about. He says, this is Warren, at Berkshire we particularly favor the rare enterprise that can deploy additional capital at high returns in the future. Owning only one of these companies and simply sitting tight can deliver wealth beyond, almost beyond measure.

[00:21:53] Tony (2): So it’s this idea of a high return on equity so you can, you can, and don’t pay any dividends so you can reinvest it at a good rate of return.

[00:22:01] Cameron: about taking your profits off the table, Warren, and rebalancing?

[00:22:06] Tony (2): Yeah. I think that’s the, that’s the argument in favor of Michael Jordan.

[00:22:11] Cameron: Yes, the Michael Jordan argument.

[00:22:13] Tony (2): Yeah.

[00:22:14] Cameron: Uh, your company also holds a cash and US Treasury Bill position far in excess of what conventional wisdom deems necessary. During the 2008 panic, Berkshire generated cash from operations and did not rely in any manner on commercial paper, bank lines, or debt markets. We did not predict the time of an economic paralysis, but we were always prepared for one.

[00:22:38] Cameron: Extreme fiscal conservatism is a corporate pledge we make to those who have joined us in ownership of Berkshire. In most years, indeed in most decades, our caution will likely prove to be unneeded behaviour, akin to an insurance policy on a fortress like building thought to be fireproof. But Berkshire does not want to inflict permanent financial damage.

[00:23:01] Cameron: Quotational shrinkage for extended periods can’t be avoided on Bertie or any of the individuals who have trusted us with their savings. Berkshire is built to last. I like that.

[00:23:15] Tony (2): Yeah. And he’s, I think, you know, um, particularly in the last few years, he’s changed his tune a bit in these letters from, Hey, we’ve outperformed twice the market over the last 50 or 60 years to, Hey, we’re not going to go broke. And, um, I was going to, I was going to read a similar sort of quote. If you look at Berkshire Hathaway, Because he always puts his performance versus the S& P at the back.

[00:23:41] Tony (2): The last five years he’s underperformed. 2019, Berkshire Hathaway, and again this is his accounting, so it’s his operational earnings. His operational earnings were 11 percent increase, S& P 500 accumulation index 31. 5. So massive underperformance. 2020, 2. 4 for Berkshire, 18. 4 for S& P, 2021, pretty even, 29. 6 Berkshire, 28.

[00:24:08] Tony (2): 7 S& P, 2022, 4 percent versus minus 18, so they beat the market there, 2023, 15. 8 versus 26. 3. So still running a twice market since 1965, which is a huge achievement. But, as, as he says, they’re a big, really big company now. It’s hard to deploy that cash to move the needle. So what he’s doing is, as a good marketer, he’s saying, but we’re not going to go broke.

[00:24:32] Tony (2): We’re, we’re here. Um, and, uh, you know, we’re, we’re a fortress with fire insurance as well, and we’re not going to burn down and all that kind of stuff. So, interesting change of tune, I think, for Berkshire Hathaway.

[00:24:45] Cameron: Hmm. Well, I guess with Charlie’s demise and Warren’s, uh, timeline, investors want to know that, you know, what they’re investing in is going to

[00:24:57] Tony (2): Yeah,

[00:24:58] Cameron: the two of them too.

[00:25:00] Tony (2): and I think that’s the, that’s always been the big question for me with Berkshire Hathaway. Um, as you know, I’ve owned shares for a while, but then I sold them. I thought Warren and Charlie were getting quite old and, and I suspect that when, when Warren finally does go and hopefully he’s around for a long time, that Berkshire Hathaway may get taken over and broken up.

[00:25:22] Tony (2): At least because They’re sitting on a heap of cash, so, you know, you get access to all that cash straight away if you’re a takeover merchant. Pays down all the debt to, um, to raise capital to take over Berkshire Hathaway. And then you can decide, well, I don’t want the railway business, it’s too capital intensive, I’ll sell that one off.

[00:25:42] Tony (2): Um, but I do like the insurance business, so, you know, Berkshire Hathaway could end up being 3 or 4 companies in the next 10 years is my guess. I know that’s a prediction. Yes, exactly. Yeah.

[00:25:54] Cameron: Teldar Paper.

[00:25:56] Tony (2): Yeah. What was I saying about the go to the phone box and ring this number and tell them the, was it the blue ostrich says held our paper or something like that?

[00:26:05] Tony (2): Yeah.

[00:26:06] Cameron: like that, yeah.

[00:26:08] Tony (2): Yeah. No, exactly. I mean, and it’s because Warren runs the business differently to how the rest of Wall Street run businesses.

[00:26:16] Cameron: That’s why I named, you know, Fox after Bud Fox. His real name is Bud Fox Riley.

[00:26:24] Tony (2): I’ll have to start calling him Bud.

[00:26:25] Cameron: Bud Fox, yeah. Okay, back to Warren. During 2023, we did not buy or sell a share of either Amex or Coke, extending our own Rip Van Winkle slumber that has now lasted well over two decades. Both companies again rewarded our inaction last year by increasing their earnings and dividends. Indeed, our share of Amex earnings in 2023 considerably exceeded the 1.

[00:26:51] Cameron: 3 billion cost of our long ago purchase. The lesson from Coke and Amex, when you find a truly wonderful business, stick with it. Patience pays and one wonderful business can offset the many mediocre decisions that are inevitable. Again, back to the Michael Jordan

[00:27:09] Tony (2): Exactly. And, and the analysis that people have been telling us about their own portfolios. You know, I bought 15 stocks and one of them accounted for most of the performance. That’s how it goes often.

[00:27:21] Cameron: Interesting that he said his share of their share of Amex earnings exceeded the cost of the share purchase all those years ago. So imagine how many times that’s paid for itself.

[00:27:32] Tony (2): Yeah, well, I mean, I’ve had that happen to me once in my investing career, and, um, my dividend. At the end was as much as what I was when I paid for the stock at the start. So the yield was about, you know, 4%. So it was a 25 dagger. So that’s probably similar to Amex and cake for these guys.

[00:27:55] Cameron: I’ve got one more. You got anything

[00:27:56] Cameron: else?

[00:27:57] Tony (2): Yeah, I’ve got a couple. Yep. So talking about Japan. Additionally, Berkshire continues to hold its passive and long term interest in five very large Japanese companies, each of which operates in a highly diversified manner, somewhat similar to the way Berkshire itself is run. We increased our holdings in all five last year after Greg Abel and I made a trip to Tokyo to talk with their management.

[00:28:21] Tony (2): Berkshire now owns about 9 percent of each of the five. Berkshire has also pledged to each company that it will not purchase shares that will take our holdings beyond 9. 9%. Our cost of the five totals 1. 6 trillion yen, and the year end market value of the five was 2. 9 trillion yen. However, the yen has weakened in recent years, and our year end unrealized gain in dollars was 61%, or 8 billion.

[00:28:46] Tony (2): Uh.

[00:28:49] Tony (2): He goes on in certain important ways, all five companies. I hope I get the pronunciations right, it Chu moi Mitsubishi Mitsui and Sumitomo follow shareholder friendly policies that are much superior to those customarily practiced in the US since we began our Japanese purchases. Each of the five have reduced the number of its shares outstanding at attractive prices.

[00:29:13] Tony (2): Meanwhile, the managements of all five companies have been far less aggressive with their own compensation than is typical in the United States. Note as well that each of the five is applying only about one third of its earnings to dividends. The large sums the five retain are used both to build their many businesses and to a lesser degree to repurchase shares.

[00:29:33] Tony (2): Like Berkshire, the five companies are reluctant to issue shares. So there’s been a lot made of Buffett’s buying into Japan and A lot of people have followed him in and the market seems to be turning around and liking that in the last year or so, but I think he’d been buying for a number of years, but interesting to compare and contrast the big companies in Japan to the kind of problems he was just calling out before in the U.

[00:29:59] Tony (2): S.

[00:30:00] Cameron: But how do they retain good talent if they’re not overpaying their CEOs, Tony?

[00:30:05] Tony (2): Yeah, well, who knows? I mean, um, potentially it’s, there could be a Japanese language barrier. I mean, how many, how many Harvard MBAs? Speak Japanese. Well, I dunno, I’m just guessing. But yeah, you’re right. It’s that. That is the argument, isn’t it? Why do you need to pay someone a lot of money to run your company?

[00:30:25] Cameron: Hmm.

[00:30:26] Tony (2): I’m looking at, I’m looking at you, Elon

[00:30:32] Cameron: The last one I’ve got is he’s talking about, um, Omaha and all of the, uh, successful investors that came out of Omaha, including himself and Charlie and I think some of the other guys that are now running the, the, the guy, uh, guys that are coming after them. I think they’re from Omaha originally too. He says, so what’s, what’s going on?

[00:30:54] Cameron: Is it Omaha’s water? Is it Omaha’s air? Is it some strange planetary phenomenon akin to that which has produced Jamaica’s sprinters, Kenya’s marathon runners, or Russia’s chess experts? Must we wait until AI someday yields the answer to this puzzle? Keep an open mind. Come to Omaha in May. Inhale the air.

[00:31:14] Cameron: Drink the water. And say hi to Birdie and her good looking daughters. Who knows? There is no downside and in any event you’ll have a good time and meet a huge crowd of friendly people. To top things off we will have available the new fourth edition of Poor Charlie’s Almanac. Pick up a copy. Charlie’s wisdom will improve your life as it has mine.

[00:31:34] Cameron: Giving a plug for their upcoming annual meeting.

[00:31:37] Tony (2): You may, yeah, I guess. I guess birdie’s three daughters would look. Better and better each year as the Berkshire Hathaway shares go up. Yeah.

[00:31:47] Cameron: I imagine.

[00:31:50] Tony (2): Probably about our age, Kent.

[00:31:52] Cameron: Yeah, uh, I don’t know. Yeah, maybe.

[00:31:56] Tony (2): Yeah, no, great. He was, he was, and he was saying it’s, now, he was saying that it was interesting how he and, how, he’d met Charlie who’d grown up in Omaha but moved away, and then Ajit Jain who runs the insurance business, spent some time in Omaha as a kid, and then Greg Abel who is, actually, Buffett, uh, Greg Abel, sorry, as Buffett, and Buffett came out and anointed him as the the next Hathaway in this newsletter, which I think is the first time I’ve seen that happen.

[00:32:25] Tony (2): He’s always said it’s going to be a contention and my wishes are known. So he actually named it. But Greg Abel, who’s Canadian, also spent time in Omaha. So it’s either there’s something in the water in Omaha or Whenever Warren sees Omaha residency on the CV, he goes, must be a good bloke, I’ll hire them.

[00:32:43] Tony (2): Yeah.

[00:32:48] Cameron: or geographic profiling.

[00:32:51] Tony (2): Yeah, I’ve just got one or two more. Well, one more actually, I’ll cut it back. Uh, he, Warren says, Beyond that, we have learned, too often painfully, a good deal about what types of insurance business and what sort of people to avoid. The most important lesson is that our underwriters Can be thin, fat, male, female, young, old, foreign or domestic, but they can’t be optimists at the office, however desirable that quality may generally be in life.

[00:33:21] Cameron: Don’t want an optimist insurance policy underwriter.

[00:33:23] Tony (2): Correct. Yeah, which is a great, a great line, I think.

[00:33:28] Cameron: That is great. Well,

[00:33:30] Tony (2): it’s always interesting to compare and contrast his insurance businesses to the ones that are listed in Australia. You know, he’s always talking about you don’t write He doesn’t write business if it’s going to make a loss and be very conservative on the, you know, the premiums.

[00:33:45] Tony (2): And I own shares in QBE and they’ve been, you know, pretty well managed recently. But they still come out, all insurance companies in Australia still come out from time to time and say, well, we didn’t provide enough for these cyclones in Queensland this year or the hailstorms in wherever. Um, and you know, they use those as an excuse for some of their profit declines, but they never come out and say, well, we were really pessimistic this year and we didn’t write any business, which is what Berkshire Hathaway has the luxury of doing, I guess.

[00:34:16] Cameron: we spent a lot of time on that, but we don’t know how many of these we have left. And, uh,

[00:34:21] Tony (2): good point.

[00:34:21] Cameron: want to make the most of Warren’s wisdom and humor when he’s Still with us.

[00:34:29] Tony (2): And hardly recommend if people haven’t gone back and read some of the past newsletters. And there are books out there which make compendiums of them. They’re really, really good reads.

[00:34:37] Cameron: And they’re all on the Berkshire Hathaway website, too. They’re all available, uh, accessible. Uh, moving along, Tony, last week I mentioned that I’d used Matt Walker’s regression tool to run a regression test starting from 15th of February 2022, which is when I started the light portfolios, and it returned a negative 13.

[00:35:03] Cameron: 5 percent CAGR. You suggested that I rerun it but with a 20 percent rule 1, which I did yesterday, and this time it returned a negative 12. 2 percent CAGR for the same period. Slow, so slightly better. Then a 10 percent Rule 1, and you would also have less trading costs. I actually haven’t, uh, gone through yet and calculated how many trades there were in each of them.

[00:35:36] Cameron: I had planned to do that before we recorded today. Didn’t get to it, but, um, we would assume there would be less trading, so you’d save a bit on that as well. But not a huge, not a huge difference. Um, not as huge as I might’ve expected with changing it from 10 percent to

[00:35:55] Tony (2): No, you and me both. And that was certainly the research that the analyst Ryan Reduce for me as well. Similar sorts of CAGA, 10 or 20%, but much less trading for the 20%. And I’ve been implementing 20 percent in my own portfolio as a trial. And, um, it’s getting similar results. I think I, I think I’ve had three or four stocks that would have been 10 percent rule ones.

[00:36:18] Tony (2): Um, uh, I didn’t sell them. And I think just recently one of them became a 20 percent rule one, or yeah, 20%. The other ones are being fluctuating. You know, above and below 10%. So it looks to be about the same result, but much less trading. Emotionally, um, that might appeal to people who don’t like the idea of trading a lot.

[00:36:41] Tony (2): So that’s certainly something the people who don’t like trading a lot can consider. It is a real kick in the guts if you have to sell something that’s gone down 20 percent on what you paid for it. 10 percent seems to be a little bit easier to stomach, but again, that’s just human behavior, I guess. So, yeah, I think it’s, um, my, it’s early days, but my gut feels it’s going to be about the same with less trading.

[00:37:02] Cameron: And as you said to me in an email yesterday, but you also, with the less trading, you reduce your chance of finding your Michael Jordans.

[00:37:11] Tony (2): Correct. Yeah, so that was the other piece of analysis that Ryan did, um, was that, yeah, if you, if you say, I can’t remember what the ratio of the trades were, but say you trade half at 20 percent and you do it 10%, um, that’s, you’ve got half the chance of finding the rocket stock, which is going to be the one that really drives your portfolio performance.

[00:37:31] Tony (2): Having said that, the CAGR was the same both ways. So even if you do find that rocket stock more in a 10 percent portfolio, you’ve got a lot more ones that weren’t as well. So it tends to even out.

[00:37:44] Cameron: Yeah, I was going to say that, well, there were no rocket stocks that really helped the 10 percent rule one in this instance over that two year period. Um, but it, it has been a difficult two year period too. So, you know, if I played this out over five years or 10 years, which I can do with Matt’s tool, I can run this back over, I think his fundamental data goes back to 2016, so I can run it over, whatever that is, eight

[00:38:12] Cameron: years

[00:38:12] Tony (2): I can’t wait to get, get my hands on this. Is other bugs fixed or they’re still

[00:38:18] Cameron: no, I haven’t heard from him, uh, recently on this, so I’m not sure where he’s at with it, but, um, yeah, I mean, I can give it to you as is, it takes a little bit of Python knowledge, but, you know, you’re an old coder, you’ll be able to figure it out. Anyway, very good stuff. Uh, reporting season news, Tony, uh, thank God we’re nearly at the end of reporting season.

[00:38:45] Tony (2): It has been one where I think you said this to me a couple of years ago. It seems like our portfolio has changed the most in reporting season. I think it’s particularly so with this half. Stocks are moving around a lot.

[00:38:57] Cameron: I haven’t had to sell much out of the dummy portfolio, but, almost super really, but just, you know, having the light, but light portfolio has a, you know, sort of a big selection of stocks across it, across all the different portfolios, but just some of the results, like, DSK, Dusk, their results came out the other day and they dropped 12%.

[00:39:19] Cameron: In a day when the results came in, the results weren’t

[00:39:21] Cameron: bad, but not as good forwards looking as the market wanted. Adair’s came out yesterday. And their results came out and they jumped 12%, but I saw them on the buy list, um, you know, when I did my analysis there on the buy list, I went and bought them and then only realized after I’d hit the buy button that the share price was 10 percent higher than it was in the buy list, which had come out like an hour earlier.

[00:39:52] Cameron: And then I was like, what? What? Oh, okay. The results of it landed. Like, after the buy list came out yesterday, the results landed, the share price blew up. I re ran the numbers, um, and they were still good. There was still a buy and still would have been on the buy list. But it, you know, they spiked it within like a couple of hours yesterday morning.

[00:40:14] Cameron: And I, I’d said to the light subscribers, you know, when we bought, when I bought DSK, which was only last week, I said, I know the results are about to come out and I’ve learned from experience, it can go either way. If you’re buying just before results announcements, it can go up or it can go down, you don’t really know.

[00:40:31] Cameron: DSK went against me, ADH also went against me because I bought it just after the results came out. It’s still gone up a couple of points, but yeah, like there’s big shifts with these results announcements. Huge, in a day, shifts. It’s kind of like ice skating. It’s like True Detective season four, walking out into the ocean, like that kind of terror, which we’ll talk about in after

[00:40:56] Tony (2): Yeah. That was so good.

[00:40:59] Cameron: Yeah.

[00:41:00] Tony (2): No, it is like that. Um, but you know, like I was thinking about what do you do about that? But if you You know, one thought was, well, we should wait for new figures to get into Stock Doctor. But then if it has gone up 12 percent when the results are announced, you’re not going to get the uplift.

[00:41:16] Tony (2): So,

[00:41:17] Cameron: not as much.

[00:41:17] Cameron: anyway. I’m hoping

[00:41:18] Tony (2): much.

[00:41:19] Cameron: will continue to go up, but

[00:41:20] Tony (2): Yeah, yeah,

[00:41:21] Tony (2): But

[00:41:21] Cameron: if I bought Adair’s last week instead of, but I don’t think Adair’s had positive sentiment last week, so it wasn’t on the buy list as far as I’m aware, but you know, if it had been and I’d bought it last week, it would have been happy days yesterday.

[00:41:34] Tony (2): Yeah. So I don’t know. I mean, again, something which could be regression tested is we don’t buy. You know, on numbers that are too old, like over six month olds or something like that, and see if that makes a difference to the portfolio performance. But it’s always been my experience to just use what you’ve got.

[00:41:50] Tony (2): Um, and generally, like, because we’ve got to have a sentiment filter as well, if a stock is going up into reporting season, chances are it’s, it, I have seen cases where they’ll report and then go down, but they often go up further, so something’s leaked somewhere.

[00:42:05] Cameron: yeah, that’s what I’m thinking. If it’s sentiment’s good before the results have come out, somebody who knows something is buying something, you know. And I, yeah, my guess is that if it’s, if it’s If it’s on the buy list, it means it’s got a good track record. It’s already, it’s either got a good track record of financial management or it’s a turn, it’s a turnaround situation already, which is the Dusk case.

[00:42:28] Cameron: I think it was a turnaround and you know, you expect a turnaround to keep turning around, but sometimes not turning around enough. So they did do a good job. Again, the results were pretty good, but

[00:42:42] Tony (2): I just want to have a look at, I want to have a look at Dusk because I thought I read somewhere that it was one of the most shorted stocks on the share market, and if that’s the case

[00:42:53] Cameron: really.

[00:42:53] Tony (2): You sometimes see the shorts will start getting out, which will put the price up. And I’ve seen that happen, um, this reporting season too.

[00:43:01] Tony (2): A couple of stocks I bought beforehand, uh, went down when they reported, but then in the week that followed, started to climb again, back to where they were beforehand. So, yeah, so, I don’t know. Stock Doctor reports Dusk has, nah, a fairly small amount of shorting. I must be getting confused with someone else, sorry.

[00:43:25] Tony (2): They did have a large short last year in 2022. It was about 3 percent of stock was shorted.

[00:43:32] Cameron: Well, anyway, there you go. Sometimes it goes in your favor, sometimes it doesn’t go in

[00:43:37] Cameron: your favor.

[00:43:38] Tony (2): And if we could accurately predict it We’d be a lot richer than we are.

[00:43:43] Cameron: I also wanted to note that one that did go in my favor, not the results necessarily, but, um, BFL, BSP Financial, that I hold in a portfolio, uh, announced their dividends, 36. 5 cent dividend. So I was happy about that. Uh, that’s gonna, that’s like a, it’s a big dividend. The shares are trading at about 6. 75.

[00:44:10] Cameron: So

[00:44:11] Tony (2): Yeah, that’s good.

[00:44:12] Cameron: is a, is a huge dividend, which would be nice when it lands.

[00:44:15] Cameron: I think it goes X in, uh, uh, what did it say? 20, uh, today, it goes X today.

[00:44:21] Tony (2): And that’s, that’s another thing to raise at this time of year too, is that be careful of ex dividend dates for stocks.

[00:44:28] Cameron: Yes.

[00:44:28] Tony (2): yeah, because they can, there’s, uh, I think the one I’m talking about goes ex dividend tomorrow when I do a pulled pork.

[00:44:36] Cameron: Oh, yeah. Right.

[00:44:37] Tony (2): so yeah, so if you’re doing your research, just work out whether it’s ex dividend or not before you make decisions.

[00:44:44] Cameron: Shares will normally take a bit of a hit when it goes

[00:44:47] Tony (2): Yeah, yep, and as we know, add the dividend back, um, before deciding to sell something if it’s dropped below its three point trend line because of the dividend going X.

[00:44:59] Cameron: We made a call when we looked at the commodities yesterday that LNG is now a sell, uh, which for me meant Woodside became a sell, which I held in my super portfolio because crude oil was already a sell

[00:45:14] Tony (2): Mm hmm.

[00:45:15] Cameron: gas became a sell. So I had to let that go, I think. I lost about 3 percent on that, but just an FYI for anyone that owns Woodside or any other major LNG think about the impact of LNG becoming a sell.

[00:45:32] Tony (2): Mm hmm. Did you check the dividend date for Woodside when you did that?

[00:45:36] Cameron: I did.

[00:45:36] Tony (2): you did that? Okay.

[00:45:38] Cameron: I did. And I think it was, uh, let me see. Uh, it goes X on the 15th of March, so

[00:45:48] Tony (2): okay. Yeah, still, yeah. And again, I’m not saying you should, if something is a sell on the commodity chart, you should hold it for the dividend because it’s, as you say, if you’re selling it for a, you’re going to sell it for a lower price after it goes ex dividend, but you get the dividend, so it’s kind of swings and roundabouts.

[00:46:04] Tony (2): Hmm.

[00:46:06] Cameron: it’s down 3 percent already, if the commodity’s, um, gonna continue to fall, it’s share price will probably follow. Or the gas could turn around tomorrow, and it could jump by 10%, who the hell knows.

[00:46:22] Cameron: Uh, I saw an article I saw an article about Cathie Wood’s ARC fund this week, which was scathing.

[00:46:31] Cameron: You know, we’ve talked about Cathie Wood on and off over the years. Data shows Cathie Wood’s ARC is one of the worst funds. A new analysis of Mama Cathie over the past decade isn’t very favorable. Goes on to say that, uh, her flagship ARC innovation ETF With 7. 7 billion of assets generated, a return of 36 percent in 2019, a whopping 153 percent in 2020, and 68 percent in 2023, according to Morningstar.

[00:47:04] Cameron: But other years haven’t been so kind to Mama Kathy, as her acolytes call her. ARK Innovation returned a negative 32 percent annualized for the past three years and a mere positive 2 percent for the past five years. That’s not too impressive compared with the S& P 500, which posted positive returns for 10 percent for three years and 50 percent for five years.

[00:47:27] Cameron: Wood’s goal is at least 15 percent annualized returns over five years. To be sure, ARK Innovation’s return profile looks better in the long term. It began trading October 31st, percent annualized from then through December 31, 2023, according to ARK. For a slightly different period The 10 years through December 31st, 2023, the S& P 500 returned about the same amount.

[00:47:54] Cameron: Of course, Wood was taking a lot more risk than the S& P 500. Um, so, you know, 12 percent over a 10 year period, not terrible, but again, not great. And she’s supposed to be one of the. You know, show ponies of tech investing, uh, high risk, high growth tech investing. 12 percent average return over 10 years, uh, during the last 10 years, which has been a lot of frothy, a lot of frothy stuff going on.

[00:48:26] Cameron: Um, I mean, I don’t know how she’s done in the last two months, uh, with the AI boom that’s been going on over there in the NASDAQ, but you know, we’ve, we, we, we have people talk to us a lot. on and off about how do we take advantage of the tech boom and how do we analyze tech stocks and high growth stocks and you know you were talking about your anti QAV strategy the other day and I look at Kathy Wood who is supposedly the best of the best of knowing how to do this she’s the poster girl for high tech high growth stocks if all she can get is 12 percent Over a very, very frothy 10 years, I’m like, what are the chances that we’re going to do any better than Kathy Wood’s going to do at picking the winners and the losers, uh, in the high tech stakes?

[00:49:20] Tony (2): Well, you make a good point, and of course it’s 12 percent after her fees, so she’s been making good money, as Warren said, she loves, loves the trade, and, um, she’s clipping the ticket, so she’s making money, um, but yeah, it’s a really good point, and, and the article goes on to say, uh, the, the author isn’t enamored with Wood’s investment style, in quotes, her reliance on her instincts to construct a portfolio is a liability.

[00:49:48] Tony (2): Ringgold said, It’s not an investment 101 portfolio. The strategy narrowly invests in stocks with paltry current earnings, elevated valuations and highly correlated stock prices, Greenwald said. Their extreme volatility underscores their highly uncertain futures. So to me, it’s a trading stock. You know, she’s had some good years in there and she’s had some bad years in there.

[00:50:10] Tony (2): So it’s more about timing if you’re going to invest in the ARK ETF than it is about long term hold.

[00:50:17] Cameron: This is brutal. Amy Arnott, a portfolio strategist for the investment research firm Morningstar, has put together a list of the 15 mutual funds slash ETS that have lost the most money for shareholders over the past decade. She ranked ARK Innovation at number 3 on her wealth destruction hit list, estimating it destroyed 7.

[00:50:38] Cameron: 1 billion of shareholder wealth during the period. Uh,

[00:50:45] Tony (2): jibe with me when she said that, you know, the other guy says that ARK got 12 percent for random CAGR. So I’m not sure how the math is done on those two things.

[00:50:55] Cameron: Yeah, like, I don’t know either. I don’t know what period she’s looking at either. I think it’s probably the same period that

[00:51:02] Cameron: Morningstar’s looking at.

[00:51:03] Tony (2): last 10 years, you’d think.

[00:51:05] Cameron: Anyway, I mean, getting back to my point, like, if that, you know, if that’s the best, I mean, there may be people, there are probably people running smaller funds, and she may have issues with the size of

[00:51:18] Cameron: it, you know, it might be like Berkshire, that the bigger you get, the

[00:51:21] Tony (2): Mm hmm. Mm

[00:51:23] Cameron: or something, all that kind of stuff.

[00:51:24] Cameron: But it’s, it’s sort of disconcerting for me to see, you know, the poster child getting those sorts of returns over a 10 year period. I mean, our W portfolio has been running for 5 years and it’s, I think, like 15. 5, 16 percent CAGR over that period. Um, it’s not 10, but, you know, it’s, I have no reason to believe it’ll be any worse.

[00:51:50] Cameron: I, you know, I think it’s been a difficult couple of years for Our style of investing, and we’re still doing double the

[00:51:56] Tony (2): Mm hmm. And beating ARK Investments too. Although I think in the last five years she would have done potentially better than what we did, but that’s just the timing of it, I think.

[00:52:06] Cameron: yeah. NVIDIA, speaking of tech, NVIDIA results! I mean, you know, whether or not we would invest in NVIDIA, you just gotta shake your head at this, um, their quarterly revenue is up 265 percent from a year ago, 22. 1% Billion, up 22 percent from Q3, and up 265 percent from a year ago. Record quarterly data center revenue of 18.

[00:52:39] Cameron: 4 billion, up 27 percent from Q3, and up 409 percent from a year ago. Record full year revenue of 60. 9 billion, up 126%. That’s like, I mean, I mean, and, and, I guess the point here is that Like, these companies, like the Magnificent Seven, aren’t start ups, they’re not, they’re not your after pays, they’re not businesses with no revenue, these are businesses with huge revenue and they’re making huge profits and a lot of money.

[00:53:15] Cameron: But that kind of performance, that’s really, really incredible.

[00:53:20] Tony (2): it is. Um, and I actually, I was unaware of NVIDIA’s history, so I read that in their results, which surprised me that they’d been around since the nineties and, um, had a lot to do with the growth in PC ga, the PC gaming industry in the late nineties as well. So I wasn’t aware of that,

[00:53:37] Tony (2): like, yeah.

[00:53:39] Cameron: their, that’s what they’re most known for is, you know, really pushing the graphics processing units for console boxes and gaming PCs and there’s a great, um, animated graph I saw on somewhere, read it probably, of Nvidia’s revenue versus Intel’s revenue. over that period of time.

[00:53:57] Cameron: And Intel was massively higher than Nvidia’s revenue up until a few years ago. And then Nvidia’s just shot the lights out because they just focused on this one thing that ended up becoming really, really important to a bunch of stuff. It was, it was initially before AI GPUs, I mean, outside of gaming became really big for Bitcoin mining.

[00:54:22] Cameron: So, cause they, you know, they can do a lot of processing. A lot of processing power. So that was their first huge bump and then when the AI, when they worked out, when OpenAI worked out that, um, Elon’s been pushing this photo recently of when Jensen Huang, the CEO of NVIDIA, delivered the first GPU to OpenAI when it was a startup and they all had a little ceremony and he donated one because it was a, you know, open source thing and they all signed it and And Elon’s been pushing the fact that NVIDIA, NVIDIA donated this to support this open source startup and now Sam Altman’s out there trying to raise seven trillion dollars to build a competitor to NVIDIA.

[00:55:13] Tony (2): Well, why, um, what’s so special about Nvidia that Intel can’t copy its chips?

[00:55:19] Cameron: Uh, I don’t know. I just think that they’ve, they’ve spent, you know, a decade and a half focusing purely and solely on building GPUs and uh, tooling up for that. That’s, it’s a non trivial exercise, but anyway, yeah, I

[00:55:36] Cameron: mean.

[00:55:37] Tony (2): Yeah, I guess the question faced by anyone who is thinking about investing in NVIDIA is what happens from here? It’s had a great year, can it continue to do that? And um, I mean, I tried to use history as a guide and went back and looked at the Bread O Later for its last five years on the, uh, of StockGraph on its, on the, in the Bread O Later.

[00:55:57] Tony (2): And you know, it’s, it’s, it’s the last couple of years have been fantastic. They’re almost, um, You know, vertical in terms of its graph, but um, before that, and it certainly over the long term had grown from nothing. So it, but it has had drops. So in 2022, it dropped from 326 of the high down to 121. So it’s lost, it has lost two thirds of its value in the last five years at some stage.

[00:56:23] Tony (2): Of course, it’s recovered. It’s now much, what’s the share price now? 790 bucks or something. So it’s recovered, you know, by six times or seven times since that. All Off, so if you’re a long term holder, great. But, um, yeah, it’s going to be a bumpy ride. Um, when these things are priced to perfection, as soon as they don’t get it, the share price retreats heavily.

[00:56:44] Cameron: But as you know, your point about Intel catching up to them or Sam Altman going out there trying to raise money to build his own, Microsoft are talking about building their own, Tesla’s building their own, China’s building stuff. It is going to be a much more, I mean, Nvidia were there at the right time in the right place with the right product to pick up on the last 18 months of AI frenzy.

[00:57:07] Cameron: But they’re not going to occupy that position. That hegemony that they’ve enjoyed isn’t going to last forever. You would imagine. I mean, it’s very rare. In business history and in tech history that, you know, I mean, Facebook’s managed to pull it off for a long time. Google’s managed to pull it off, Apple, Microsoft, but very, very few companies have ever managed to pull off market dominance and hegemony for.

[00:57:34] Cameron: Longer than, say, five years,

[00:57:36] Tony (2): No, you’re right. Um, I guess on the flip side of that is that NVIDIA are in a great position to be able to continue what they’re doing, supplying GPUs to business and find something else, what the next thing is after, after that. Um, and potentially even Discount the GPUs they’re currently producing. So what’s the next wave is the advantage NVIDIA has.

[00:57:56] Tony (2): So as Intel tries to catch up, it’s catching up to the current wave.

[00:58:00] Cameron: the end of human civilization is the next wave.

[00:58:03] Tony (2): Yeah, maybe.

[00:58:03] Cameron: to figure out how to make profit.

[00:58:08] Tony (2): Well, I’ve got lots of resources to do it with. So good luck to them.

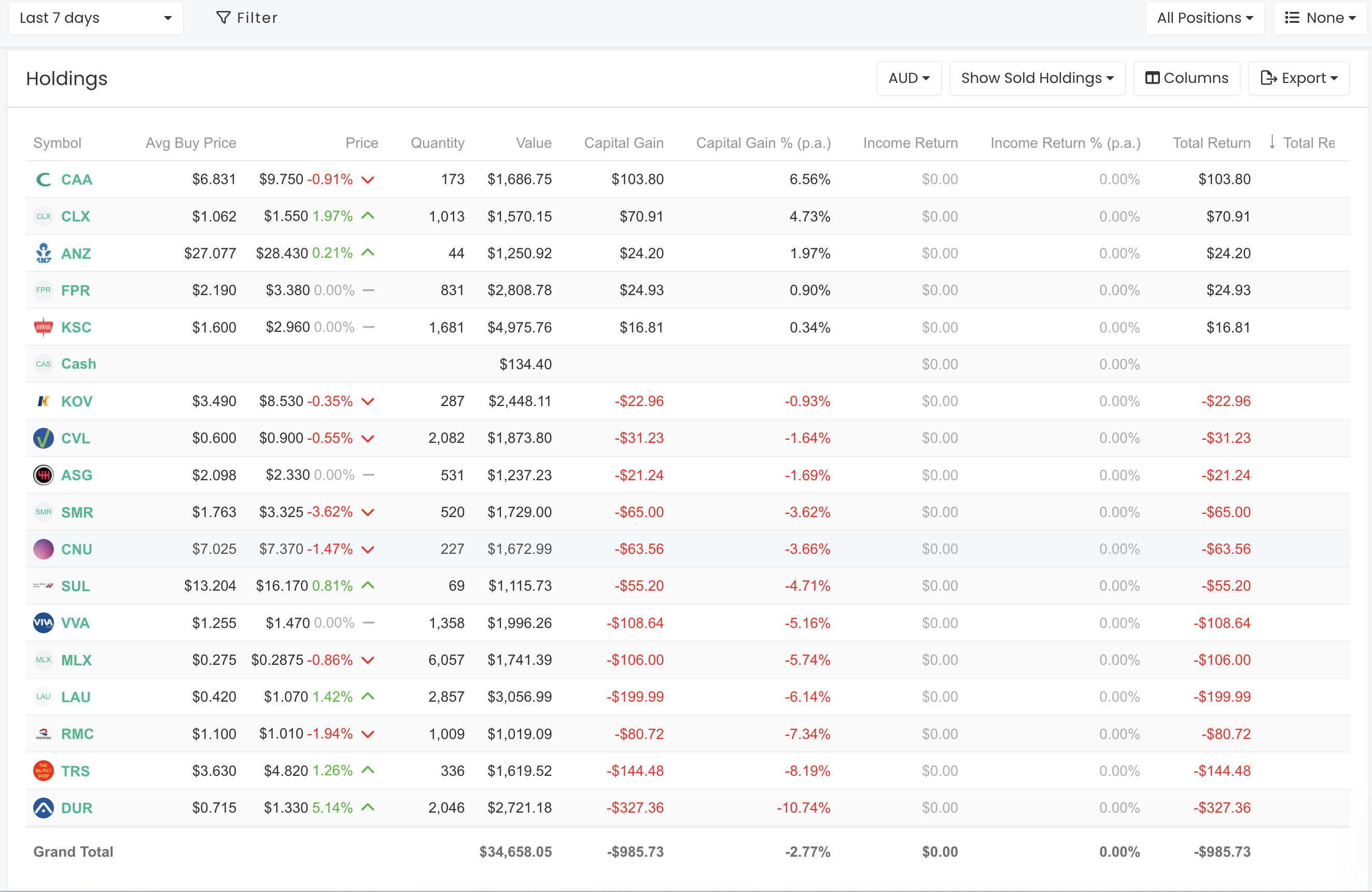

[00:58:12] Cameron: Uh, just quickly, W Portfolio, as I said, still trading at about double. Uh, last week hasn’t been great for us, though. For the current financial year, we were well ahead, um, of the STW a week ago. We’ve dropped back down to parity with the STW in the last week. Couple of big hits, DUR. Had a big drop. The TRS had a big drop.

[00:58:37] Cameron: RMC had a big drop with not a lot of big winners to balance it out in the dummy portfolio this week. So, you know, we’re back down to, I mean, we’re still up 9, 9 percent for the financial year. So it’s not bad, but we’re neck and neck with the STW again now. But it has been sort of this crazy week. I mean, DUR, as I said, dropped 10 or 11 percent the last week.

[00:59:03] Cameron: It’s still up like 150 percent from where we bought it. So I’m not complaining. There’s a lot of profit taking going on. as people are rebalancing, good luck to them. But I’m going to hang in there with it. No, I had no trades in the last week though, with the dummy portfolio yet again. You know, it’s crazy.

[00:59:22] Cameron: There’s been so little trading done in the dummy portfolio over the last couple of years. It’s just, you know, seems to have established itself very well and the shares are all. You know, well above, not all of them, but most of them are, you know, well above their rule one, well above their three point trend lines.

[00:59:42] Cameron: You know, occasionally there will be commodity sales, I imagine, although looking through the list, I can’t see many, you know, CAAs on there. Can’t see many commodity stocks on the list these days. RMC. But MLX, there’s a couple. But it’s, uh, it’s interesting just how little trading I have to do in the dummy portfolio.

[01:00:05] Cameron: Even in fairly turbulent markets, it’s just stabilized. It’s just really sit and hold.

[01:00:13] Tony (2): Yeah, and I found that, um, with my portfolio, the trading’s dropped off in the last six months. And that’s what happens with portfolios, as you say, they establish themselves and they get above all their sell lines and then they just, you sit and cruise with them, which is a nice place to be. Don’t,

[01:00:28] Cameron: But you know, you were saying with your own portfolio, you had to do a lot of trading over the last couple of years. So I mean, and you’ve been running that for 400 years. So what happened there?

[01:00:44] Tony (2): tell anyone.

[01:00:46] Cameron: Well, is it a post COVID

[01:00:47] Cameron: thing? Like

[01:00:48] Tony (2): No, I think it’s an interest rate. It’s, I think it’s interest rates. I think the market was really choppy when interest rates were going up and they haven’t moved now for a number of months and everything settled down a bit.

[01:00:59] Cameron: Well, I’m looking, I’m looking at the history last 12 months on the WPortfolio. So. I did two sales in January, one sale in December, one in November, four, no, four, okay, five or six in October, nothing in September, three in August, three or four in July, but yeah, it’s been really, you know, a lot less than, you know, one a week on average over the last six months. Um, very little trading.

[01:01:40] Tony (2): Yeah. And I’m guessing October may have been reporting season related too, which is usually the heaviest time to trade stocks.

[01:01:46] Cameron: Right, yeah, could have been, don’t know, uh, let’s, let’s see what was October, it was like, NHC, SUL, PRU, I think it was Commodity Stuff, actually, oh no, they’re buyers, hold on, NHC, OML, OML, I’ve actually, I was looking at that recently, like, I’ve Bought and sold that a number of times. I bought it again today. I think I had it to my super portfolio today.

[01:02:08] Cameron: Um, and it’s one of those stocks that I’ve, I’ve got like a spotty history with. I’ve bought it a number of times and it hasn’t done well, but currently I hold it in a few portfolios and it’s up. 20, 30 percent in some of those portfolios. So it’s actually, it’s one of those ones that, you know, I kind of groan whenever I see it and I have to buy it.

[01:02:29] Cameron: Cause I’m like, uh, not you again. Oh Mel, my old friend. uh, this time it seems to have come good, you know? So, you know, it’s stabilized and the fundamentals kicked in and off it went. All right. What else you

[01:02:47] Cameron: got?

[01:02:48] Tony (2): I better pull pork.

[01:02:50] Cameron: Who are you pulling today, Tony?

[01:02:53] Tony (2): I’m looking at Vulcan Steel, VSL.

[01:02:57] Cameron: Never heard of them.

[01:02:59] Tony (2): I wonder if they’d greet each other in the mornings and go live long and prosper.

[01:03:04] Cameron: you would always have to, that’d be part of the initiation process,

[01:03:08] Tony (2): Yeah. Although it’s a Kiwi company so they might go, you know, live long and prosper.

[01:03:16] Cameron: uh, have they, have they

[01:03:18] Tony (2): listeners.

[01:03:20] Cameron: have they on the BI list?

[01:03:23] Tony (2): Yeah, they came on, they’re a new one this week, which is why I’m talking about them, and they’re a relatively large company, so they may suit a lot of listeners. ADT is 351k per day, so it’s fairly large. They’re on the buy list, but I think they’re a Josephine, so they’re one to watch. And they’re also a good dividend yielder, and they’re going ex dividend on the 29th of February tomorrow, so again, their price is going to be volatile after that.

[01:03:51] Cameron: And I’m looking back over my fancy historical buy list sheet. This is the first time. They’ve been on the buy list at least since September 2021, which is when my historical buy list started, so Yeah, that’s why I’m not familiar with them. They’re

[01:04:07] Tony (2): Yeah, same.

[01:04:08] Cameron: the first time. Why are they showing up for the first time?

[01:04:11] Tony (2): Uh, well I think they’ve, uh They’ve only been listed for a couple of years, so they’re listed

[01:04:16] Cameron: Ah,

[01:04:17] Cameron: okay.

[01:04:17] Tony (2): October 22, I think. It’s a dual listing both in New Zealand and Australia, and they’re expanding pretty quickly, so they had a, they had a bad result, which is something to take into account, except for operating cash flow, which is why it’s, I think, probably hit the buy list after their December numbers came through.

[01:04:38] Cameron: Did you say VSL?

[01:04:39] Tony (2): Yeah,

[01:04:41] Cameron: Not a Josephine right now, looking at the bread a later. It’s, you know, looking

[01:04:46] Cameron: alright.

[01:04:47] Tony (2): Oh, okay. Sorry, the commodity, Chekap Steel, I think

[01:04:50] Cameron: Oh, sorry. Steel.

[01:04:52] Tony (2): my mistake. Yep. Yeah. Yeah,

[01:04:56] Tony (2): so, yep. So, um, as I said, it’s a Kiwi company. It was founded, uh, quite a while ago, back in the 90s in Auckland. Uh, What else can I say about it? It’s dual listed, um, list price two years ago was 7. 10, and the share price I’m using is 7.

[01:05:15] Tony (2): 58, so, another material increase over the last two years, uh, however since listing it has paid approximately 2 per share in dividends, so, um, the returns have been good from that side of things. Vulkan was founded in 1995 by a chap called Peter Wells in Auckland. It operates as a key, well they say it operates as a key link in the steel value chain between steel producers and end users.

[01:05:42] Tony (2): So basically they don’t smelt the stuff, they just buy it off the steel producers and then sell it to, uh, Building sites and end users. They distribute all kinds of steel products, including carbon steel, stainless steel, engineering steel, and recently aluminium as well. They distribute steel beams to builders, they process steel plate to customer specifications, which involves cutting, folding, and drilling in their factories.

[01:06:10] Tony (2): They process steel coil, and they do the same for stainless steel and aluminium. Uh, at the time of listing, Vulkan operated 29 sites across Australia and New Zealand. This is only two years ago. However, today they operate 69. So growth has been quick with a lot of acquisitions. Uh, they haven’t gone so well recently though.

[01:06:33] Tony (2): The December half year results showed revenue was down 12 percent and net profit after tax was down a whopping 53%. Although operating cash flow was up dramatically. So I’m guessing there’s maybe some kind of write down in their numbers. I haven’t had a chance to look in that much detail. To go through the numbers though, using a share price of 7.

[01:06:56] Tony (2): 58, which is less than consensus target, quite well above IV1 and IV2, which is IV1 is 2. 48, IV2 is 3. 40. We do have the current December half results in our download. So that’s a good thing. Uh, dividend yield. This, uh, at the moment is 4. 92%, which is probably its lowest it’s been for a while, and the dividend was down this half, I guess in line with the drop in net profit.

[01:07:23] Tony (2): Stock Doctor financial health and trend is satisfactory and recovering, so we like that. I don’t score ROE, but just highlighting the fact it’s very strong. It’s 39. 58 percent for this company, which is, which is quite amazing for this type of company. PE is 15. 66 times, which is its highest in the last three years, so we don’t score it on that.

[01:07:45] Tony (2): In fact, we give a negative for that, I think, from memory. NTA is 1. 01 per share, and net equity per share is 1. 20. So I actually thought there’d be a bigger difference between NTA and net equity per share, given all the A lot of acquisitions that they’ve made recently. And, um, and there certainly is a bit of a difference, but it’s not that big.

[01:08:05] Tony (2): But, um, with NEPs then it’s nowhere near the share price of 7. 58. And so we can’t score it for a stock trading nearest book value. PropCaf is good. It’s trading at 4. 6 times. So that’s probably why it’s on our buy list. Forecast earnings per share is negative, negative 27 percent So it loses a point for that.

[01:08:27] Tony (2): And, I Again, I haven’t been able to get more than the surface look at what’s driving that, uh, whether the analysts are extrapolating from the poor half it’s had or whether this includes in their numbers the poor half it’s just had, um, but it is a, it is a concern if they’re for, if the forecast is for, uh, a drop in earnings per share of that magnitude.

[01:08:48] Tony (2): Uh, the directors hold 14 percent. So it scores for that. However, the owner founder, Peter Wells, retired from the board after it listed, so he retired in October 2022. Um, however, they have a very experienced CEO who has been in this company for a long time, um, came up through the management ranks, um, and has 40 years of experience in the steel industry overall.

[01:09:16] Tony (2): And he owns 4 of the company. So, uh, and there is another board member who owns the same, so I’m going to score it as an owner founder, even though the owner founder has retired. Uh, sentiment, as you said before, is up, and it’s a recent, uh, three point trend line uptrend, so it scores for that. It doesn’t have consistently increasing equity, so no score for that.

[01:09:39] Tony (2): So all in all, the score, uh, for quality is 9 out of 16, or 56%. And the QAV score is 0. 12. So, first time on the buy list, towards the bottom, but I just sort of highlighted it as being a new stock with a high ADT. Um, in my readings on, on reviewing this stock, I sort of formed the opinion that it did have a fair few risks around it, despite, um, it’s, it’s, you know, uh, good growth through acquisition recently.

[01:10:07] Tony (2): Um, number one risk was that the owner founder retired, so that, even though there’s still a high amount of, um, Equity amongst the directors. It’s, it’s, uh, you know, we don’t have the owner there anymore, or the founder there anymore. Uh, it’s something like 60 percent of the steel it sells goes to the construction industry.

[01:10:27] Tony (2): And you’d have to say that the construction industry is sluggish at the moment. Um, we’re seeing low housing starts. We’re seeing Office buildings underutilized and therefore their value is dropping. So I don’t know if we’re going to see many skyscrapers in the cities in the CBDs for a while. And we’ve seen, as we’ve highlighted in the last 12 months, builder bankruptcies on the housing front and construction front.

[01:10:50] Tony (2): So there’s a bit of pain in the construction industry. Um, that. Is possibly what’s flowing through to this company with its, um, decrease in sales last half. Uh, and also too, I have read some speculation that there might be a rise in interest rates in New Zealand next year. Their economies had, had, uh, a tough time, but it seems to be, um, doing okay at the moment and they might be putting the brakes on it again, so that would be a negative.

[01:11:17] Tony (2): Uh, on the positive side, um, it seems well run. It’s growing quickly. Uh, I did think that maybe the nickel price decreasing might work in its favor. So people would have read in the financial press that Indonesia’s been flooding the market with cheap nickel, which is hurting the mines in Australia, but certainly nickel is an input into stainless steel.

[01:11:38] Tony (2): So it may mean that there’s a, um, a margin boost to this company. I’m not sure where nickel figures into there. Pricing, um, whether it goes to the smelter or whether they mix it themselves, but um, it may lower the price for stainless steel, which should drive sales for that company. So that’s Vulcan, uh, Vulcan Steel.

[01:11:58] Tony (2): I hadn’t heard of it before, but interesting to do a pull pork on it.