Hello QAVvers

If we only have love

We can melt all the guns

And then give the new world

To our daughters and sons

So sings Jacques Brel (in French though) this morning on “Quand on n’a que l’amour”.

What does that have to do with investing? Well there’s certainly lots of love on the markets at the moment, as the half year results coming through tend to be better than expected (unless you are DTL!).

Let’s have a look at the portfolios.

QAV PORTFOLIO REPORT

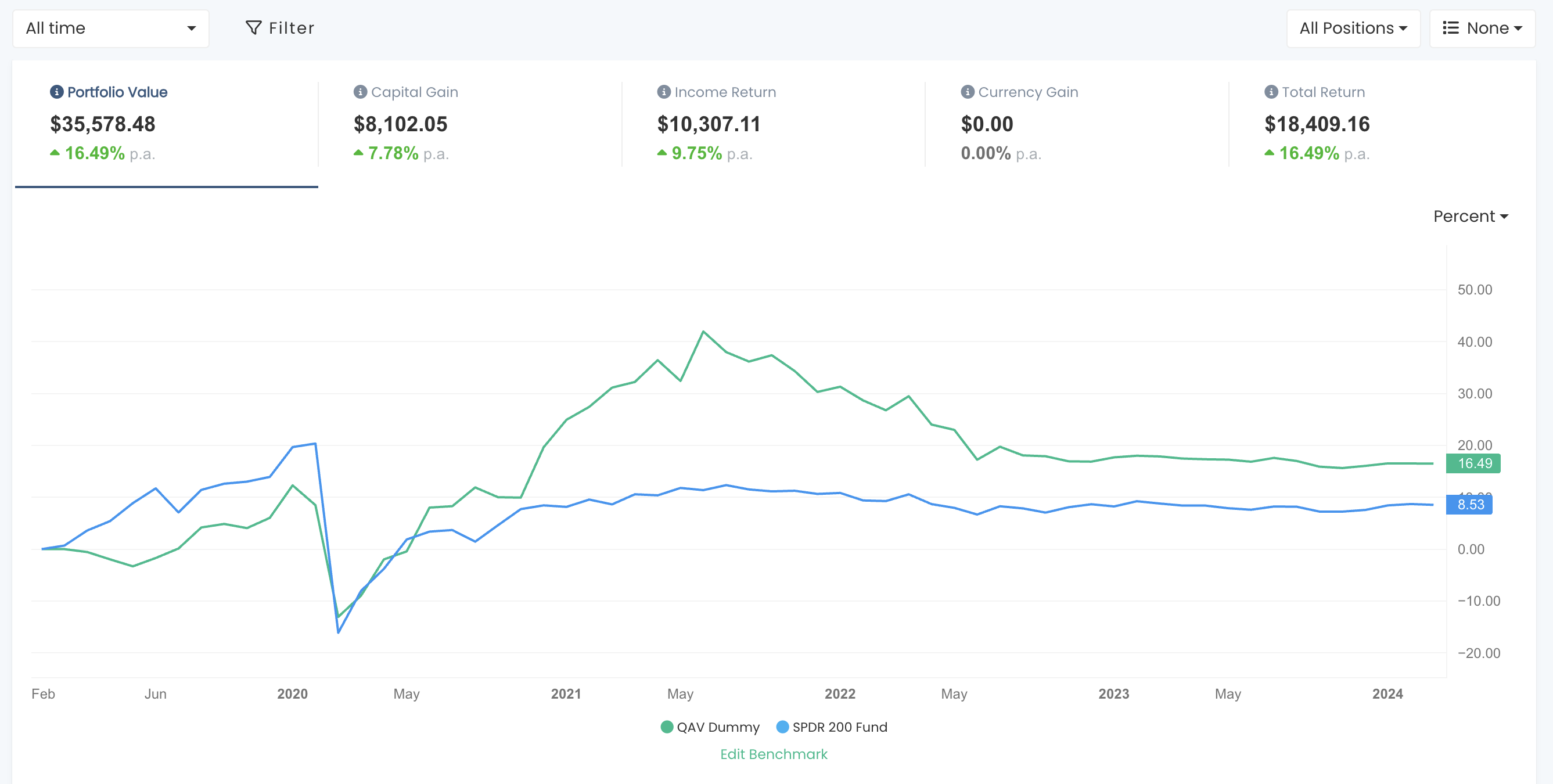

The Dummy Portfolio is performing well against the benchmark over most time frames.

SINCE INCEPTION (15/04/2019)

Our portfolio is still doing slightly less than double market since inception, which celebrated its five year anniversary.

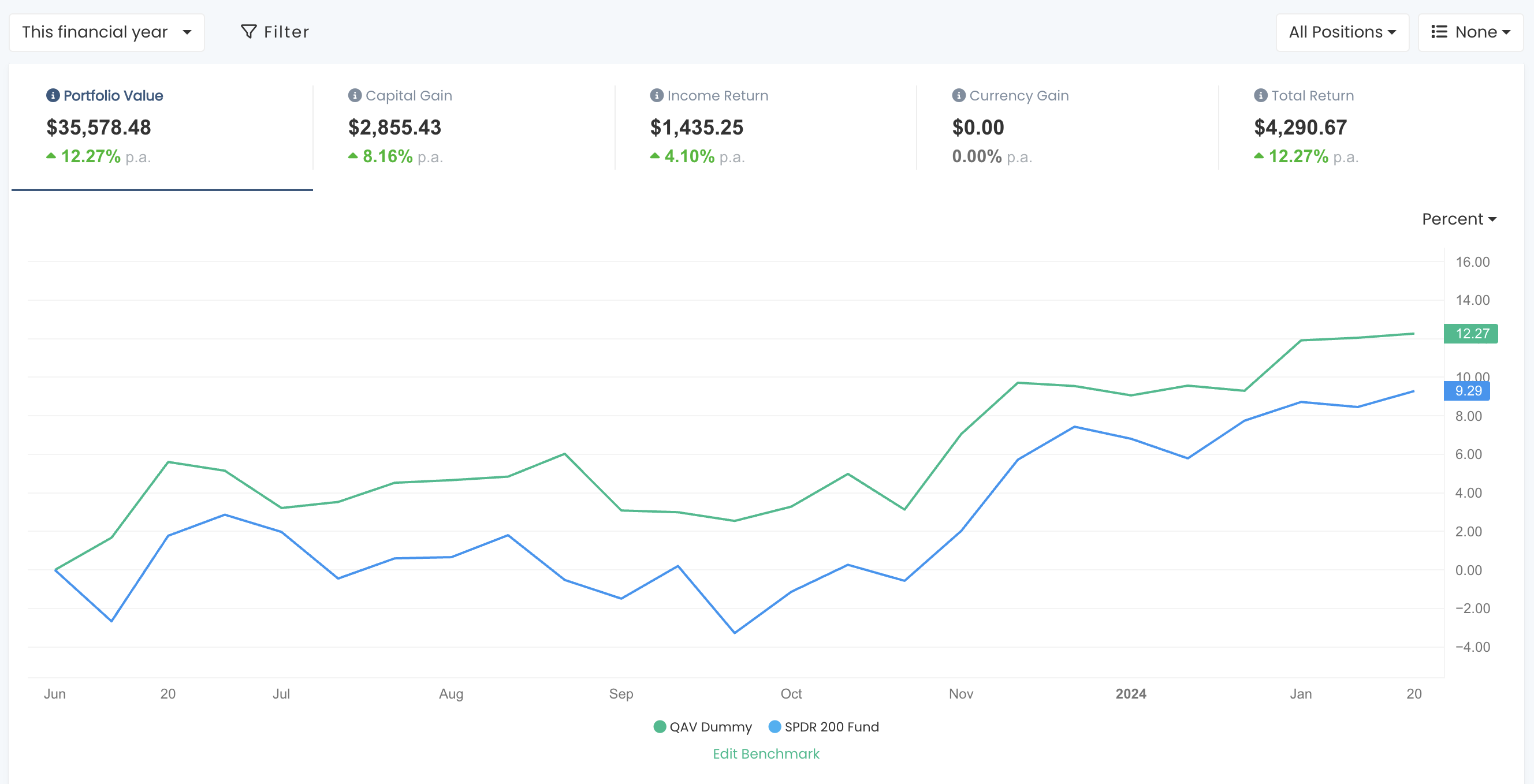

CURRENT FY

We’re outperforming the benchmark for the FY, too.

RECENT TRADES

No trades in the last week.

QAV STOCKOPEDIA DUMMY PORTFOLIO REPORTS

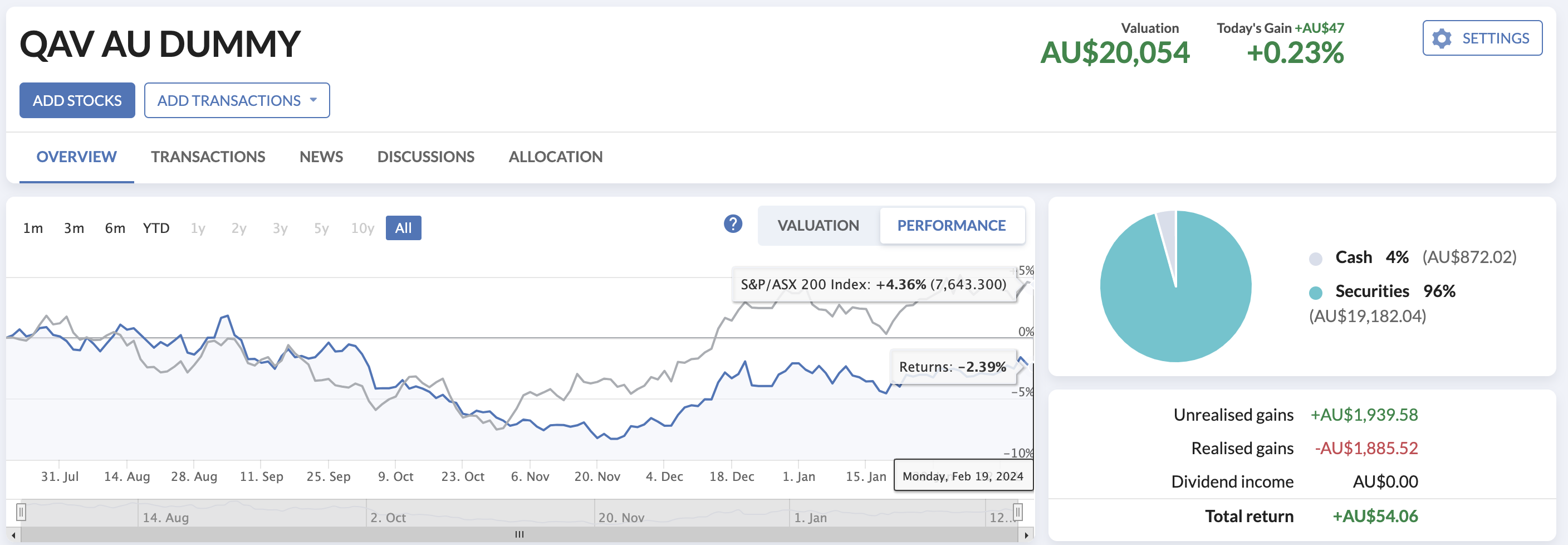

QAV AU DUMMY

The Australian Stockopedia portfolio is still underperforming since inception. It’s sitting on 4% cash. I did invest some last week, but then had to sell something yesterday and haven’t had a chance to run a new buy list for it yet.

QAV US DUMMY

The US portfolio is up, but is underperforming the S&P, but that’s hardly surprising, as we don’t hold any of the Mag7. I just got around to investing some of its cash, too. By the way, the Magnificent 7 profits now exceed almost every country in the world.

STOCKS OF THE WEEK

During the last week, we also traded some stocks in our Light portfolios. Details here.

** As always, please check our work, DYOR, and consult a financial advisor before making any investing decisions.

BUY LIST

Each week we produce a buy list that we share with our members. The intended primary purpose of this buy list is for club members to use as a reference for comparing their own buy list. In theory, all of our buy lists should look pretty similar each week.

As always, please check our work, DYOR, consult a financial advisor before making any investing decisions.

THIS SECTION CONTAINS CONTENT WHICH IS VISIBLE TO QAV CLUB SUBSCRIBERS ONLY.

LAST WEEK’S EPISODE

This week: Market and portfolio updates; Nick Scali and Myer jump on profit results; the pitfalls of passive investing; the cracks deepen beneath the market’s surface; Woodside Santos merger collapsed; pulled pork on MME.

Also in the Club edition:

Lithium execs goolies; McDonald’s records first sales miss; Stock tips are for patsies; Matt Walker’s regression testing system; Three Men Make a Tiger; NWS shares in Stock Doctor; WAF’s forecast earnings.

Episode Transcription

QAV 707

[00:00:00] Tony: 1, 2.

[00:00:15] Tony: 3, go.

[00:00:18] Cameron: Welcome back to QAV, episode 7 0 7.

[00:00:23] Cameron: The day before Valentine’s Day. Valentine’s Day. N minus one 13th of February. There you, I, I knew you would’ve. That’s why I was dropping it in there for

[00:00:34] Tony: We never celebrate it, but

[00:00:35] Tony: I should,

[00:00:36] Cameron: Neither did we.

[00:00:40] Tony: Uh,

[00:00:40] Cameron: how are you this week? TK?

[00:00:42] Tony: very well. Thank you.

[00:00:44] Tony: It’s, uh, hot, hot, hot in Sydney today,

[00:00:46] Tony: but lovely and

[00:00:48] Cameron: yeah. Hmm. Just grey and muggy and hot in

[00:00:52] Cameron: Brisbane. What, uh, what’s been going on in the market for you this week? Tony?

[00:01:00] Tony: Oh, I’ve got a couple of things. Um, it’s company reporting season, so at least from the, a couple of stocks that I’ve looked at that are on the buyer list, it seems to be going okay, especially in the retail sector. My, it was only a week or two ago I was saying, oh, you know, my prediction for this company reporting season is declining profitability, but not for stocks like, uh, Nick Scali and Myer who both jumped on their profit results.

[00:01:28] Tony: ’cause I think most analysts were expecting there to be some downturn in retail stocks, given the, the, the inverted commerce cost of living crisis that everyone keeps talking about. Uh, but no, they, they did well. Nick Scali jumped about 15% after its results came out. I think AGL, which is on our buy list, also did the same and Myer

[00:01:50] Tony: did the same.

[00:01:51] Tony: So, yeah. Interesting, interesting. Uh, profit season and it always keeps us on our toes.

[00:01:58] Cameron: Myer jumped from six. Sixty-six cents. up to seventy-eight cents, and then immediately fell back down to seventy-one cents. But it is crept back up over the last week. It’s back up at like seventy-five cents now. So yeah. Uh, I was surprised when I saw that bump from Myer what’s going on and saw that their results came out.

[00:02:18] Cameron: Yeah, it is interesting, like there’s a lot like the, as we know, the, the all-orbs hit its all-time high sometime in the last week and then fell back a little bit, but it’s not by much. It’s still coasting along up near the top there. There’s a lot of froth and bubble going on, A lot of, a lot of it sort of, um, I don’t know, Positivity in the market, but it’s hard to really understand why, and I’ve got some stories a little bit later on that we can drill into that.

[00:02:49] Cameron: What’s driving that, blah, blah, what have you, what else have you got to talk about before we get into that?

[00:02:53] Tony: Well, I think the positivity in the

[00:02:55] Tony: market is around no more rate increases really. And then the be is just how long it’s gonna take for rates to decrease,

[00:03:02] Tony: um,

[00:03:03] Cameron: You think there will be no, as the RBI said that, I thought they were

[00:03:06] Tony: no. That’s what analysts are saying, but the general consensus is no more rate increases, which is why the RBA, I think, came out and specifically said, we’re not committing to that.

[00:03:14] Tony: ’cause why would they, they need to keep their flexibility open. Um, it’s, it’s funny, they kinda like do a negotiation dance with the, with the journalists and the analysts and the, and the bond traders in particular, the RBA will say one thing, the bond market will move a different way, and then journalists will

[00:03:30] Tony: ask the RBA questions and they’ll, they’ll duck and dive.

[00:03:34] Tony: It’s, it’s a game that’s been going on for 40 or 50 years.

[00:03:38] Cameron: The five D’s of dodgeball, duck dive, Dodge, duck and dive. Something like that. You ever seen

[00:03:49] Cameron: dodgeball? Yeah, it’s a great, I’ve got a clip anyway. Yeah.

[00:03:56] Tony: Yeah. So the other thing that I’ve, uh, picked up a couple of articles on in the last week, which I guess, uh, resonated with me, uh, people coming out and just, just having a question about the, the role that passive investing and index funds and, and particularly ETFs are playing in the markets at the moment.

[00:04:18] Tony: And, um, Alan Kohler in his weekly report came out and said, with an interesting stat, came out and said that, uh, the US now accounts for 70% of global equity market value. So basically market cap, um, up from 45% in 2007 and 35% in 94, despite the US having only around 4.3% of the global population and 17.8% of global GDP.

[00:04:46] Tony: So just stop and think about that. For every dollar invested worldwide, 70% is going into the us and of that 70%, I dunno what the state is, but an awful lot is going into the Magnificent seven. And um, another article which he sort of expanded on that was by a guy called, uh, Einhorn. I’ll just look up his, his first name doesn’t mention what his first name is.

[00:05:14] Tony: Sorry, David Einhorn. Here we go. I’ve got the article in front of me. And, uh, he’s the founder and portfolio manager of a company called Greenlight Capital in the state states. And he said recently, this was reported in the AFR last week, he said the huge flows to passive investing, uh, the growth of algorithmic trading and momentum trading.

[00:05:33] Tony: And the more recent rise in the US in particular in trading on very short-term options and similar instruments means most investors are focused on price rather than value. He goes on to say value is not just a consideration for most investment money that’s out there. Passive investors have no opinion about value.

[00:05:51] Tony: They’re going to assume everybody else does the work. And so what he’s basically saying is that, uh, there’s so much money following money if that makes sense. That if, if you are an index fund and you need to keep rebalancing because stocks are getting bigger in the index, it’s quite possible you end up with a situation like we have at the moment in the states where all of the growth has come from the, from seven stocks, which are now hugely outsized compared to the rest of the market.

[00:06:25] Tony: And, and the u as is the US is outsized compared to the world. So it’s an interesting situation. I I, I’ve long thought that these, the kind of rise of passive investing in index funds and index funds have been around for a long time, but there’s a lot more money in, um, index funds now since, uh, ETFs make them cheap and easy to trade.

[00:06:44] Tony: But yeah, it’s kind of a feedback loop. If, if, um, if Apple goes up. That moves the index, then index funds have to buy Apple. So it’s a chicken and egg situation. Um, what, what’s driving the price of Apple up? Is it the underlying value or is it the, is it the momentum in, in the stock price of Apple and the index funds have to follow.

[00:07:03] Tony: And that’s what Einhorn’s saying. And he goes on to say that, um, in the market, in a market that is pushing higher and higher on the back of small groups of very large stocks, and where a stock like Nvidia can go parabolic up more than threefold in a year, despite the fact that it was already a very large company, Einhorn’s warning does carry extra punch.

[00:07:23] Tony: He’s saying that in his fund, uh, he’s moved away from value to what he would call deep value. In other words, instead of picking stocks with earnings of 10 and hoping they will re-rate. He is looking, or he, he and another guy called Greenlight is looking for stocks trading on four to five earnings. Um, but crucially, Einhorn is not buying these stocks in the hope that the market will eventually recognise their value.

[00:07:46] Tony: He wants stocks with strong cash flows and low leverage that they’re able to buy their own stock or pay dividends to effectively guarantee a return. Uh, sounds like what we do. Um, while Greenlight’s latest investor leather shows, it has added a few names recently on Double Digit Earnings, it tells the story of the strategy.

[00:08:06] Tony: The company’s three biggest winners in calendar. Year 2023 were Builder Green Brick Partners Energy Group, Consol and IBM Spinoff Kindle all trade between five and seven times earnings and rose between 61% and 112% last year. So interesting take. Um, he’s, he’s going after even deeper value in the hope that if there’s little debt and lots of cash, that they’ll use that cash to buy their stock or pay dividends or do something else constructive and it’s worked for him.

[00:08:37] Tony: So, yeah. Interesting. Sort of take on the markets and, uh, the headline for that article on the AFR was Wall Street Legend Einhorn Offers Fix for Broken Markets. And, uh, uh, it’s, you know, I hardly endorse those sentiments and it’s, to me, the crowded trade in the markets at the moment, apart from the Magnificent seven is index ETFs.

[00:08:58] Tony: And I just wonder where

[00:08:59] Tony: it’s gonna finish. I don’t think it’ll end happily.

[00:09:03] Cameron: Hmm. Yeah. Well, in addition to that, I saw another

[00:09:09] Cameron: article in the Finn this week. The cracks deepened beneath the market Surface. Investors are decidedly upbeat, but analysts warn there are disturbing currents beneath the US share market’s. Calm service. The US share market continues to notch fresh records with the Blue Chip index, the S&P 500, breaking through the 5,000 mark.

[00:09:31] Cameron: As investors continue to celebrate the certainty that the US Federal Reserve will cut interest rates this year, what’s more investors are sanguine that the US share market will continue to rally. Regardless of how the US economy performs. They figure that if the US economic activity were to falter, the US Central Bank would come to the rescue with even more aggressive rate cuts.

[00:09:54] Cameron: On the other hand, if US economic activity remains buoyant, corporate earnings will continue to move higher, which helps to justify elevated valuations. What could possibly go wrong, Tony? It’s just a win-win. If the economy does well, we market’s great. If the market ta, if the economy takes. Market’s great.

[00:10:15] Cameron: It’s all great. It’s just all good. Um, but it goes on to say, as the bearish society general strategist, Albert Edwards has pointed out, the U.S tech sector is worth a third of the total U.S equity market, which is higher than the previous peak seen in July, 2000 at the height of the.com bubble. This he notes, is something he thought he’d never see again.

[00:10:39] Cameron: And I, I saw another chart from Bloomberg. I saw this in, uh, Reddit on Wall Street bets of all places, which I still follow ’cause it’s hilarious. Uh, but it has a chart of the S&P 500, excluding, excluding, sorry, tech stocks. And it’s actually, uh, at a historic low, if you take the tech stocks out of the S&P 500, it’s at a historic low.

[00:11:07] Cameron: So. All of the, of the growth in the S&P is coming to, uh, uh, tech stocks and Yeah, mostly the Magnificent seven outside of Tesla, which I saw a funny TikTok sketch today of the rest of the Magnificent seven having like a, uh, intervention, uh, meeting with Tesla saying they were kicking Tesla outta the Magnificent seven.

[00:11:31] Cameron: ’cause its share price has been plummeting over the last year while theirs has all gone up. Uh, yeah. I mean, it’s one of these times when, you know, it, I, it reminds me of that period in pre-COVID, when we started the show where if you weren’t buying tech stocks, you were, you know, or Bitcoin, you were a dummy

[00:12:00] Tony: Afterpay.

[00:12:00] Cameron: investor.

[00:12:01] Cameron: Afterpay being the big one in Australia because it was just, you know, there was just boom times and everything was going crazy. And it kind of feels like that again with these tech stocks in the us. Just this bubble mentality of everything’s just gonna go great from here on in, and we don’t need to worry about value, we don’t need to worry about profitability, we don’t need to worry about, you know, fundamentals.

[00:12:28] Cameron: It’s just, uh, chase, chase the price, as you said earlier, right?

[00:12:31] Tony: Well, it reminds you of pre covid. It reminds me of late nineties. These are exactly the kinds of con conversations I was having in ninety-eight ninety-nine, um, you know, exactly the same sort of things. What do you mean? If you put.com after something, it’s going to be worth a lot more than the day before when you put.com after it.

[00:12:53] Tony: And what do you mean that all of these other, uh. Stocks on the

[00:12:57] Tony: S&P‑Five hundred are virtually worthless and uninvestable. They’re still churning out a lot more profit than dot-com stocks are. So what are you talking about?

[00:13:06] Cameron: Well, the difference I, I guess with the Magnificent seven is these aren’t

[00:13:09] Cameron: startups. You know, um, Google Meta, Microsoft, apple, Nvidia, they’re, they’re not startup companies that have just put a.com after their name. These are businesses, in most cases that have been around decades,

[00:13:24] Tony: for sure.

[00:13:25] Cameron: have, have been very successful, have very well established products and customers, and make a lot of money.

[00:13:31] Tony: until, until AI came along and AI is a start-up. Chatgpt is a start-up. That’s what’s put the rocket under their share prices. Yeah, sure. They were, they were very strong, profitable companies before that. And you know, Buffett among a. Said, Google’s a fantastic company ’cause it costs a cent to build an ad.

[00:13:52] Tony: You can sell it for a dollar. So it’s a, it’s a fantastic

[00:13:54] Tony: company. Um, but they’ve

[00:13:56] Tony: just had this, the accelerator has been put flat to the metal

[00:13:59] Tony: since AI

[00:14:00] Tony: came along. That’s the startup.

[00:14:02] Cameron: mm And as we’ve talked about before, I mean, I, I get it. AI, I think is gonna be huge and somebody is gonna make a lot of money out of AI in the next 10 years. They all have a good chance at making some of that pie, uh, unless something happens that a black Swan comes along and, uh, you know, re-revolutionizes the industry again.

[00:14:26] Tony: Well, you’ve made a good point. I mean, there are a lot of black swans in the world, and any one of them could upset the apple cart. And, and the history of investing is when something’s priced to perfection. Doesn’t take, doesn’t take much of a, doesn’t even take a fully grown black swan to come along and upset the apple cart.

[00:14:45] Tony: But the other point I’ll make is, um, someone will make a lot of money out of ai, but typically it’s the second person. So if you look back to the.com bubble, um, Nasdaq went down 80% in 2001, Amazon, for example, uh, went down to, you know, 14 bucks from 400 or whatever it was. And then if you bought Amazon, you’ve made a lot of money, right?

[00:15:08] Tony: I guess you’ve still made a lot of money if you held on when you bought it at 400. But the person that made the most money bought it at 14. So when all these stocks inevitably blow up, because they’re all too expensive, it’s the person who buys it then.

[00:15:21] Tony: But a can pick the winner, and B, we’ll make a lot of money

[00:15:28] Cameron: Yeah, and I, I mean the, the company that’s driving all of the AI boom is OpenAI, which isn’t part of the Magnificent seven. That’s not publicly listed yet. Uh, when that happens, uh, it’ll be interesting to see how that share price does. That’s gonna be crazy.

[00:15:48] Tony: to the moon.

[00:15:50] Cameron: Microsoft’s, uh, appreciation and

[00:15:53] Tony: Mm.

[00:15:53] Cameron: is to a large degree, I think, tied to its interest in OpenAI,

[00:16:02] Cameron: but we’ll see how that plays out over time,

[00:16:05] Tony: Anyway, we talk a lot about AI in this show, and it’s not an AI show. Yeah. The interesting thing is, is this, I think this sort of flywheel effect of these big companies get bigger and that makes the index funds buy more of them. Which makes the index funds to buy more of them. It’s, it’s, uh, it’s a self-perpetuating prophecy.

[00:16:21] Tony: And again, it’s gonna, when something happens to derail the valuations on these companies, whatever it

[00:16:27] Tony: is, um, could be as simple as one of the AI chat bots is far more successful than the other ones. And the Magnificent seven becomes Magnificent one. You know, there’s a lot of money gonna, that’s gonna be lost because passive investors are gonna just exit

[00:16:44] Tony: those companies very quickly and exit the stock market probably what didn’t and nurse their

[00:16:48] Tony: losses.

[00:16:49] Cameron: mm Well, moving on. Harold. Mitchell died today. Tony or yesterday or something. Do you have much to do with Harold? Big

[00:16:58] Tony: I did not meet Harold. Jenny actually sat in the plane next to him

[00:17:01] Tony: once, and she reported to him as being a very nice guy.

[00:17:05] Cameron: He wasn’t, when I met him, uh, I. I had a couple of run-ins with

[00:17:10] Cameron: him

[00:17:10] Cameron: I think it was in the early days of the podcast network. And, you know, when we were sort of shaking stuff up and talking about media and media buying and that kind of stuff, um, I think he expressed an interest and taking an equity stake in us.

[00:17:26] Cameron: At one point I had a couple of meetings with him and like 20 years ago, and I, I don’t really remember much about it except that I walked away going, oh, he’s a big fat jerk. I wasn’t impressed. But that aside, um, built a very successful business and was really an innovator in the seventies and eighties around media buying in this

[00:17:48] Tony: Mm-Hmm.

[00:17:49] Cameron: And so, RIP, Harold, Mitchell, he lived large, uh, he was a big identity in Melbourne and

[00:17:56] Cameron: uh,

[00:17:57] Tony: And he famously lost a lot of weight too along the way. Um, he did start off being large and then

[00:18:01] Tony: lost a lot of weight. Not that that’s important. Uh, wrote an interesting book about

[00:18:05] Tony: his life, which I remember reading, I don’t know, 20 years ago.

[00:18:09] Tony: Um, and it,

[00:18:10] Cameron: Called Living Large.

[00:18:11] Tony: I’m not sure what it

[00:18:12] Tony: was called. It was,

[00:18:13] Cameron: name of his autobiography. yeah.

[00:18:14] Cameron: Living Large. Yeah, it

[00:18:15] Cameron: was

[00:18:16] Tony: Um. But it’s again, this classic story. He, he, he worked in an advertising agency and did the media buying. And if, I mean, you’ve had experience with advertising agencies, they don’t, it’s not the most glamorous job in the advertising agency. It’s like the creatives go out to lunch, the creative director comes back and says, uh, yeah, we should put this on Channel nine.

[00:18:36] Tony: Call Harold getting to, you know, book some space for us. It’s like almost like the secretary of the creative

[00:18:41] Tony: director. Uh, but Harold, uh, saw how important it was and how it was really the engine room and how he can make money out of it and separated it from the agencies and, and, uh, became sort of the center of advertising.

[00:18:53] Tony: Everyone had to deal with Harold to book their space. So it’s the classic story of, um, you don’t want to go into a, a job which is really popular, where everyone wants to do it for nothing. You wanna go into a job that no one wants to do and then leverage it up and charge, charge lots of money for it.

[00:19:08] Tony: It’s, um. Classic business trope I’ve seen before. Like waste management or like, um, yeah. No one wants to shovel shit for a living, but the shit shoveler can make a lot of money if they do it properly and set up the business structure. Right.

[00:19:21] Cameron: Particularly if you’re mobbed up. Right. Isn’t that

[00:19:26] Tony: Yeah. But all those kinds of industries, no one, no

[00:19:28] Tony: one wakes up thinking I wanna be a cement mixer driver. Right. But Boral’s a very successful business.

[00:19:33] Cameron: Yeah.

[00:19:34] Tony: Yeah.

[00:19:36] Cameron: Well, moving on to other things. The Woodside Santos

[00:19:39] Cameron: merger, which we’ve talked about a few times on the show over the last year or so, is dead, Tony. Dead value killed the $80 billion Woodside Santos deal according to Chanticleer in the financial review. When two boards have gone as far as due diligence, they’re committed to properly exploring a deal.

[00:20:02] Cameron: What can kill it from there is value. The great 4 3 2 1 dream deal is dead. The deal, which could have created a globally relevant oil and gas player that would’ve been able to redirect cash flows across jurisdictions and make the most money possible for shareholders, failed at the most important hurdle value.

[00:20:23] Cameron: When they started talking properly, Woodside Energy and Santos knew roughly which shed of shareholders would get, how much of the combined $80 billion group. But then it goes on to say that, uh, they really couldn’t agree on a deal, and, uh, the whole thing is just fallen apart. What do you make of that?

[00:20:43] Cameron: What does it, what does it mean for. Uh, investors in WDES and STO, Tony.

[00:20:51] Tony: I don’t think it means anything in the short term. Um, we never knew whether it was going to be a good deal ’cause they never, no one ever told us what the deal was. They were still trying to work it out themselves. Um, Woodside, you know, in the, I think rightly has a very disciplined approach to acquisition and part of that 4, 3, 2, 1 was they paid the right price for BHP’s Oil business and they, um, they bolted that on a year or two ago and Santos didn’t do too bad outta buying Oil Search, which is another part of that 4 3, 2, 1 consolidation, which gave them a lot of exposure to PNG and potential growth.

[00:21:28] Tony: Upside that’s always been Santos issue is, um, they haven’t really unlocked that to a large extent, but it’s still seen as being a, um, there on the table. So the Santos shareholders wanted to be pay the premium to Merge and the Woodside shareholders said, uh, we like you, but not at any price. And so it was probably the right outcome.

[00:21:48] Tony: I expect there’ll be further corporate action from both of these companies. So it’s a bit of watch this space now. Might not happen quickly, may. Um, but as I said a couple of weeks ago when I did a bit of a deep dive in this, um, in these two companies, uh, there’s a lot of consolidation going on in the world in oil and gas.

[00:22:08] Tony: Um, the bigger companies are getting bigger. It’s a, it’s a bit of a sign of a declining industry. Uh, and so they have to, you know, make, make profits from their back end of merging with other companies and reducing their costs as much from their front end of selling more oil. And so, um, uh, you know, this, the combined Woodside Santos would’ve been, I think from memory, the sixth largest oil and gas company in the world.

[00:22:32] Tony: Um, uncombined, it probably means they’re gonna be the prey for someone, um, to take, to lob an offer. Notwithstanding they have to get around the foreign ownership. Deals. I think it, I think it’d be a tough sell to, to, um, to the Australian government to give away control of its oil and gas, uh, exports to an overseas company, but, but no hurdles, uh, insurmountable at the right price.

[00:22:55] Tony: So, um, what’s this space, I guess, and it doesn’t, and I think there could also be, it’s possible that Santos might be merged that’s also being talked about by analysts that, uh, you know, take the oil out of Santos or the gas out of Santos, particularly the gas. I think the gas might be worth more,

[00:23:11] Tony: um, if it’s separated from Santos than if it stays within Santos, so that that could happen as well.

[00:23:17] Cameron: mm well.

[00:23:19] Cameron: both of their share prices taken a bit of a hit since this announcement happened. Um, dunno that Well, it’s, we’ve got what’s crude oil is what a Josephine for us at the moment,

[00:23:32] Tony: Yeah, it was a sell for a while, but it’s coming back a bit, I think.

[00:23:36] Cameron: let me just check. ComStats. ComStatus. Yeah. So crude oil is a cell and LNG is a Josephine. I hold WDS in one of the light portfolios. I think I only bought it like a month or so ago. It’s up about 1% since then, but, so neither of them are gonna be on our buy list at the moment anyway. So even though the share prices dropped, not much good to us because the oil and gas are not in a buy situation. I dunno how far away they are. I haven’t, I can’t remember what the chart looked like yesterday, but there might be some upside there at some point. Now

[00:24:22] Tony: Uh, yes. I mean, I think some people like you do in the light portfolio may be holding onto one or both, particularly Woodside. Um. Uh,

[00:24:31] Tony: yeah. I don’t think the fact that this merger hasn’t gone through as a sell, it’s, Uh, it might turn out to be a good thing in the end.

[00:24:37] Cameron: Yeah. Uh, I read this article on Stockhead this week. Dear ASX, I’m a lithium exec. Please find in close to my ghoulies. Um,

[00:24:49] Tony: That’s a very prosaic,

[00:24:51] Cameron: yeah, it’s a great, it’s a great, uh, this guy, he writes for Stockhead, the secret broker. It’s, uh, it’s always an

[00:24:57] Cameron: amusing column. I dunno if you read it. Um, this one says, after thirty-five years of stockbroking for some of the biggest houses in investors in Australia and in the uk.

[00:25:06] Cameron: The secret broker is Regaling Stockhead readers with his colorful war stories from the trading floor to the dealer’s desk. Nickel Dimes and mines the old investment ad Azure follow the money doesn’t always work, as Australian investors have discovered with their lithium punts and to a lesser extent, their nickel punts.

[00:25:25] Cameron: As I’ve pointed out before, enlisted miners most exciting shareholder times are when they are exploring and not when they are producing. Exciting and promising drill results Can put a fire under a company share price, but when, or even if they do become a producer. The share price goes to a current valuation price.

[00:25:45] Cameron: Should the commodity they produce fall in price or their local currency go against them than they are as vulnerable as a rabbit staring at headlights. Sure. Sometimes hedging strategies can help, but sometimes they can bring you down. As the Layla brothers discovered with their Sons of Gwalia hedging disaster, they managed to turn a massive gold producer from Sons of Gwalia to Unix of Gwalia.

[00:26:09] Cameron: They were related to Peter Layla, who helped hook Victoria on the world’s gold mining map in the 1850s, so they must know what they’re doing right, wrong. Now we’re seeing punters in the headlights watching their investments collapse in nickel and lithium hopefuls, as well as producers. They’ve been copying it from all sides, and now the majority of the loyal shareholders are blaming the shorters rather than the fundamentals for all the kicks they keep getting between their investment.

[00:26:35] Cameron: Ghoulies.

[00:26:40] Tony: to commodity price graphs, isn’t it?

[00:26:43] Cameron: Yes. Yeah. Because you’ve demonstrated over the years that not always, but quite often, the share price in a, uh, company that’s attached to a commodity will follow the commodity with a bit of lag

[00:26:59] Tony: Correct. Yeah. Um, but I take issue with that. The, the statement about, uh, the fun time to be in the mining companies is when they’re exploring and not when they’re producing. I think the fun times to be in it when they’re producing and you’re getting operating cashflow, that’s a great time to invest. I mean, I understand what he’s saying.

[00:27:16] Tony: It’s the speculative side of things is to, is to punt on penny stocks when they’re exploring. And you could, you could have a huge win. Um, you could suffer a lot of losses along the way as well. Um, but yeah, but no, certainly there’s, I mean, like, you know, as we’ve seen with gold stocks and with iron ore stocks and et cetera, et cetera, copper stocks, um, when a mine can, can sell. A commodity for a lot more than what it costs. They’re all in cost of producing that commodity use. They make money hand over fist.

[00:27:46] Tony: Any exploration plays a part in that. ’cause if they can expand the mine, um, into other areas, then they make even more

[00:27:52] Tony: money. But, um, yeah, they’re great cash cows, I think producing mines.

[00:27:57] Cameron: mm Yeah. Particularly if you can get them when they’re out of favor

[00:28:04] Tony: Hmm,

[00:28:04] Cameron: and, uh, the share price doesn’t reflect their value. Right.

[00:28:08] Tony: Hmm, Absolutely. Yeah. And that’s, that’s oftentimes because either people are taking a punt on what the commodity will do, or they just don’t like to be as the, as the, um, the person you quoted. They don’t want to be in the, the producing side of the mine life. They want to be in the exploration side of the mine life.

[00:28:26] Tony: But yeah, mines a, mine’s a wonderful cash cows. They really are.

[00:28:33] Cameron: Uh, shout out to listen to Peter Ball, who after last week’s show, when we mentioned that the U.S market dipped because of McDonald’s and it had something to do with the Middle East, he sent me a link to this story in the Guardian. McDonald’s Records First Sales Miss in nearly four years. Amid Boycotts company is among several Western brands that have seen protests and boycott campaigns over perceived pro-Israeli stance.

[00:29:03] Cameron: McDonald’s reported its first quarterly sales miss in nearly four years on Monday, squeezed by weak sales growth in its business division that includes the Middle East, China, and India. The Burger Giant is among several Western brands that have seen protests and boycott campaigns against them over their perceived pro-Israeli stance in the Israel-Amass conflict.

[00:29:27] Cameron: Comparable sales in McDonald’s international development Licensed Markets segment Rose 0.7 and a quarter widely missing estimates of a 5.5% growth. According to LSEG data, the business accounted for 10% of McDonald’s total revenue in 2023, the CEO flagged a meaningful business impact in McDonald’s Middle East market in some areas outside the region due to the war, as well as quote associated misinformation, end quote about the brand.

[00:29:56] Cameron: So there you go. That’s a real thing.

[00:29:59] Tony: Yeah. Wow.

[00:30:00] Cameron: boycotting McDonald’s can bring a market down

[00:30:04] Tony: Hmm. So, uh, I, I dunno a thing about this, but, um, I don’t imagine McDonald’s came out and said, Hey, we’re pro-Israel and anti-Palestine.

[00:30:13] Tony: I guess it’s because they’re operating in Israel

[00:30:15] Tony: perhaps that

[00:30:15] Tony: they, they’re seen as being

[00:30:17] Tony: pro-Israel. I, I don’t know.

[00:30:19] Cameron: I don’t know. I haven’t looked into it, uh, yet to see exactly. Oh, here we go. This is from Al Jazeera. The slump comes after customers in Muslim countries called for a boycott of McDonald’s in response to its Israeli franchisee donating thousands of free meals to the Israeli military. Following the announcement by McDonald’s Israel franchisees in Saudi Arabia Oman Kuwait, the United Arab Emirates, Jordan Egypt Bahrain, and Turkey distanced themselves from the donations and collectively pledged millions of dollars in aid to Palestinians in Gaza.

[00:30:55] Cameron: So the go,

[00:30:58] Tony: Wow. The politicisation of capitalism. Huh? Democracy of capitalism.

[00:31:04] Tony: Interesting. I mean, it’s got gotta be a thing. But I, when I read that article that you sent through from our listener, I did also wonder whether China was playing a part in McDonald’s international sales drop because there’s, you know, all sorts of reports about China turning down economically and that

[00:31:20] Tony: that could affect, um, a

[00:31:21] Tony: business like McDonald’s over there.

[00:31:23] Tony: But again, I’m not familiar

[00:31:25] Tony: with this.

[00:31:26] Cameron: I, I thought the trope about McDonald’s was it’s what poor people eat. So if you have less money, don’t you eat more McDonald’s?

[00:31:33] Tony: that’s what it’s meant to be. Yeah. Yeah, it is. Yep. That’s, uh, they always put McDonald’s in the

[00:31:38] Tony: outer suburban areas, um,

[00:31:41] Cameron: hmm.

[00:31:41] Tony: more than the inner ones.

[00:31:46] Cameron: Stock tips are for Patsies. Stephen. Mabb sent us this

[00:31:49] Cameron: article, uh, yesterday or the day before. Chris Leitner from Leitner and Company. I analyzed 13,000 readers tips, review a century of other studies and show how and why tips usually underperform and sometimes crash. Now, this article was way too long for me to actually read.

[00:32:08] Cameron: Uh, so I put it in chat GPT and said, can you summarize this for me? And it, it couldn’t even, it got bored. It got about half, got about halfway through, and it was like, Ugh, really? Here’s what it

[00:32:21] Tony: Okay. You read that? What? Chachi. Bitti said. I read the

[00:32:23] Tony: article.

[00:32:25] Cameron: It said, uh, it blah, blah blah. Studies to

[00:32:28] Cameron: demonstrate that tips often lead to underperformance and

[00:32:31] Cameron: sometimes significant losses. It argues that stock tips can be enticing, but it generally not backed by rigorous analysis and relying on them without doing one’s own research. As a mistake, the piece emphasizes the importance of due diligence and warns against the allure of quick gains that stock tips promise.

[00:32:49] Cameron: I.

[00:32:50] Tony: Yeah, that’s a fair enough summary. But, um, there’s a few other points that Chris Leitner was making. Um, apologies if I don’t paraphrase these properly, but, uh, he, he did analysis on the reader tips for LiveWire. And so every year LiveWire asks both, uh, a whole panel of fund managers for their top tip for next year.

[00:33:12] Tony: And, and, uh, likewise for the readers. And, and I know lots of thousands of people will give their tips for what it’s worth. Um, but Chris Leitner showed that, um, two things. One, that those stocks were. Ones that performed well before the tip was given. And, um, he goes, uh, back to Keynes who said that the stock market is a beauty pageant and you’ve gotta try and guess what other people find as pretty.

[00:33:36] Tony: And so, um, he, he made a case that said that if, uh, that tips are often, um, late, that they, um, they, they follow what’s performed well in the past, which is kind of an easy way of tipping, I guess, if something’s done well and you’re banking on it going forward. The hot hand approach, I guess, as it’s called, um, you, you’ll do okay.

[00:33:54] Tony: Uh, and Leitner showed that if you bought and bought and held onto these stocks, you eventually underperform the market. I, I don’t disagree with that, but I think it’s a bit of a, um. Misrepresentation of what LiveWire do. ’cause they do this every year in January. Um, I don’t think they meant they ever say buy and hold these stocks forever.

[00:34:13] Tony: They, they suggest, here are the ones for this year and then here are the ones for next year. And, and they do it on an annual basis, and then they tell you how they performed. And I think from memory, I haven’t looked it up, but the LiveWire tips, both the, the, for readers and for funders do okay. They’ve outperformed the market in a number of years since live wise been going.

[00:34:31] Tony: So, um, take that, you know, with a grain of salt if you like. And, and the other point I’ll make is that, um, the performance of a, of a list, of a tip list, like that is not just about the stocks that are being tipped, it’s about the weighting. You’ve given each one. So if there’s. 10 top tips from readers or from Fundies and you equal weight, the purchase of those tips, you’ll get a different result than if you just buy the top one or if you just buy the bottom one, or if you weight them by market cap or you weight more from top to bottom.

[00:35:08] Tony: So it’s important to know how, you know, the, the stocks are, are bought as well as, um, how they perform. And I see that all the time when I do regression testing. I can have a number of stocks in the portfolio and if I buy them different ways, they one outperforms and one underperforms. So that’s, um, that’s always something people need to keep in mind and that’s, that’s why, you know, we, we talk about, um, buying from the top of the buy list down, um, as a, as a way of sort of prioritizing what to buy.

[00:35:38] Tony: So that’s, that’s the point. Um, and the last point I’ll make, uh, is I. And there’s a lot of quotes from Warren Buffett in this article. The last point I’ll make is if Warren Buffett was giving me stock tips, tips, I I would definitely listen. Um, but, but an important point, even in that context is that if, if Warren was only asked for one stock tip, it, it’s only gonna be right six outta 10 times.

[00:36:03] Tony: So because Warren says that in his, his communications with shareholders, he only ever gets six out of 10, right? So if you get one stock tip from Warren and it doesn’t work out, you might go, ah, Warren’s not good. I’ll go and talk to somebody else. And that’s, that’s another problem too, is, is um, is making decisions about who to deal with based on one stock tip.

[00:36:26] Tony: So I, I think there was a lot of good stuff in this article, but, um, there’s a, opens up a lot of questions and, and, uh, discussion points as well. And I guess the last thing I want to talk about is it begs the question is, you know, why would you make QAV like tips. Um, ’cause we recommend stocks to, to buy for, for people.

[00:36:46] Tony: And if I can answer my own question, um, we also recommend we to sell them. Uh, the, the top tips from readers don’t come with an expiry date, so, um, you know, they might do well for the first month and not after that. As Leitner’s analysis shows, they certainly go downhill after about 12 months. Um, but also to QAV is the output of a process and we teach the process and, um, you don’t have to follow a tip.

[00:37:11] Tony: You can do your own analysis and, and work it out from scratch as well. Um, we trade along Qav light listeners trade along with us, so that’s a, a bit of a difference to just taking a tip. Um, and, uh, we produce weekly results and are quite transparent about our performance. So, um, all of those things I think are, are prerequisites before taking advice on what to buy and sell and.

[00:37:38] Tony: To be fair to us, we don’t tell people that buy and sell. We say, here’s something to have a look at and

[00:37:42] Tony: do your own research.

[00:37:43] Tony: So that’s another important point. Here’s what we’re buying and selling. yeah.

[00:37:47] Cameron: yeah. yeah. And I, I think you, you made a lot of good points, like, but the whole selling

[00:37:52] Cameron: thing, I think, you know, is something that. Um, may not be obvious to amateur investors. Uh, certainly I, I, I didn’t appreciate when we started this show how important that is as a component of a successful investing strategy, knowing when to exit and not just leaving it up to gut feeling, you know, oh, you know, I think I should sell. Like if, yeah, it’s really tough if you’re just leaving it up to emotion, right?

[00:38:26] Tony: Oh, exactly.

[00:38:27] Cameron: rigorous methodological method, let’s just go with that

[00:38:34] Cameron: system. Having some rigorous math to know when to get out, um,

[00:38:42] Cameron: just makes a world of difference for me as an investor to just not have to get emotionally involved in the decisions, you know?

[00:38:51] Tony: Yeah. And look, and, and I’m not saying our, our exits are perfect. Um, and there are other ways to do it. And, uh, yeah, Steve and I had a chat yesterday about, about, you know, process and tips and things like that. And, you know, he, he, uh, thinks that there are other ways to exit stocks, which is fine. You know, when the, when the goes off the bio list or when it goes off his bio list or when the fundamentals change, they’re exit triggers as well.

[00:39:18] Tony: And I, I respect that, but, uh, because Steve’s

[00:39:21] Tony: got a framework that he’s working around, I think that’s important.

[00:39:24] Cameron: hmm. As long as you have a framework that you’ve thought about, you have a process in place for helping you make your decisions, I think is the key thing. What, what that process is, is up to you

[00:39:36] Tony: Yeah, exactly.

[00:39:37] Cameron: with. Well, speaking of regression testing, uh, I think I’ve talked about this briefly before, but, uh, one of our listeners, Matt Walker, has been working on a regression testing system over the last couple of months, and he sent it to me, the latest version of it, sent it to me last week.

[00:39:56] Cameron: I got it up and running over the weekend, and it, and it, uh, bloody works. Um, there’s, there’s a, a bug that I found in it with the way it’s handling, um, cell decisions, which, uh, he’s implementing at the moment, a fix for that. But I was able to do a regression test on about eight years worth of fundamental data in about 15, 16 minutes.

[00:40:23] Cameron: I just set, I put in the variables that I wanted to test. I said, go, and 16 minutes later, it produced a report for me that gave me the CAGA results. Over that period, all of the buys and sells that had made along the way, um, to, to go back and check. Um, so, uh, first of all, huge congratulations to Matt for building this.

[00:40:48] Cameron: It’s, uh, really impressive piece of code. It’s, it’s not something that, uh, we, we can make public yet. It’ll be a while before we can do that once we get it working. But hopefully, you know, at some point in the near future, we will be able to make this available for people to do their own regression testing or send me the things that, you know, the models that you want me to regression test and I can plug it in and, uh, you know, I’m gonna do things like, well I did one on the, on the weekend, which was, um, just prop calfers less than eight.

[00:41:20] Cameron: Ignore all the rest of our scoring. Just PropCAF, I still add the cell triggers in there, rule one and the three PTL cell trigger doesn’t do commodity cell

[00:41:30] Cameron: triggers yet, that we haven’t got to that, but just those two and just the PropCAF and ran that over eight years and it came back with like a, I think it was an 18% CAGA over that period.

[00:41:43] Cameron: Um, again, some of the three PTL cell triggers aren’t exactly right. Um, but, so, you know, there, there might be some issues with that number but uh, it was just amazing to be able to plug in some, I know how much effort you’ve gone to with your interns over the last few years to do regression testing. To be able to just plug in the variables and say, go, and it just does it all for

[00:42:06] Cameron: you and spits out a result 15 minutes later is pretty exciting.

[00:42:10] Cameron: So again, shout out to Matt for all of the incredible work that he’s done and for sharing it with me, and let’s hope that, you know, that helps us improve QAV and test, uh, all these ideas that our smart listeners have come up with and you come up with, you know, what, if we did this instead of that over 10, 15 years, what would that look like?

[00:42:33] Cameron: You know.

[00:42:33] Tony: Yeah. Thank, thank you, Matt. That’s fantastic. And I agree it. That’s what’s been missing from my methodology to, to do that kind of grunt analysis in detail. ’cause I think the, the most important thing I think is to check the, you know, isolate each variable and see how much it contributes and whether we need to reweight them in the QAV checklist or even eliminate some, some of them from the QAV checklist and even add some, which, you know, we’ve had people talk about, uh, looking at companies that can do buybacks and things like that.

[00:43:01] Tony: So yeah, I think it’s gonna be great. And, uh, if, if we get it working and you don’t hear from us anymore, we’ve

[00:43:09] Tony: sort of found something, producing a really good high CAGA number and we

[00:43:12] Tony: we’re off doing it ourselves. Yeah.

[00:43:14] Cameron: Yeah, yeah, Yeah.

[00:43:17] Cameron: Uh, well the last thing I got to talk about is Housell’s Little ideas. For the week, three Men Make A Tiger was the one that I read this week. He says, people will believe anything. If enough people tell them it’s true. It comes from a Chinese proverb that if one person tells you there’s a tiger roaming around your neighborhood, you can assume they’re lying.

[00:43:37] Cameron: If two people tell you, you begin to wonder if three say it’s true. You convinced there’s a tiger in your neighborhood and you panic. So

[00:43:46] Tony: that’s the basis of the Murdoch press, isn’t it? If, if Channel Nine tells you there are roving gangs of, uh,

[00:43:54] Cameron: news.

[00:43:56] Tony: SI was gonna say, African youths, which is, which they did. And if, uh, the Daily Telegraph says it, and if the Courier

[00:44:02] Tony: male says it, people start to believe there’s a problem with roving gangs of African youth, even though there isn’t.

[00:44:09] Cameron: yeah, yeah, and, and I think it applies

[00:44:12] Cameron: to investing as well. you know, you start to hear people talk about. Afterpay or Bitcoin or the Magnificent seven or whatever it is, you know, it’s, it’s something, uh, in that, uh, there was this Persuasion, was that the name of that

[00:44:31] Tony: Influence? I was just thinking that

[00:44:33] Cameron: Influence? Yes.

[00:44:34] Tony: Cialdini’s book Influence.

[00:44:36] Cameron: Yeah. There is something in,

[00:44:39] Cameron: uh, human psychology where if you hear enough people say something, repeat the same idea. It could be the zaniest, craziest, you know, least supported by facts idea going, but if you hear it enough times, there’s something in our brains that goes, oh, okay, I should take that seriously.

[00:45:01] Cameron: If enough people are saying it to, to me it might must be true, even though it can be completely not true.

[00:45:06] Tony: mm.

[00:45:07] Cameron: But, and it also gets back to system A and system B thinking, you know, um, Daniel Parnamon,

[00:45:13] Tony: and Tversky.

[00:45:14] Tony: Yep.

[00:45:16] Cameron: Rather than having to think through things at a very deep level, it’s quite often advantageous. It has been evolutionarily advantageous to have a heuristic that enables you to make snap decisions about

[00:45:36] Tony: Hmm.

[00:45:37] Cameron: And that seems to be like one of the heuristics. If three people tell you there’s a tiger roaming about, then it’s something you should pay attention to.

[00:45:44] Tony: Yeah. Like if,

[00:45:45] Cameron: if if you don’t, if you go, well, I’m gonna go and do my own research project, you might get eaten by the tiger, right?

[00:45:52] Tony: Yeah. Well, Tversky and, and Kahneman use the example of if you out on the veld and the grass starts to rustle and you can’t see what’s rustling in the grass

[00:46:00] Tony: you don’t go over and have a look.

[00:46:02] Cameron: Yes.

[00:46:03] Tony: it’s a target and you run the other way.

[00:46:05] Cameron: you, or you turn around with your spear at

[00:46:08] Cameron: the ready, uh, in case it is something about

[00:46:10] Cameron: to jump on you and nine ninety-nine times out of a hundred it might be nothing. That one time out of a hundred, you’re right. It saves your life so evolutionarily, it’s a good survival strategy, but when it comes to investing, not such a good idea.

[00:46:27] Tony: No. Well, I mean, the, thinking about that book, Affluence Cialdini uses social proof as one of his examples of how we’re influenced by, by, um, our, our, our brains, which have evolved as, as you said. Uh, and he talks about the, the classic psychology experiment of someone standing out in the, looking up in the air.

[00:46:47] Tony: And yeah. And, and eventually people will walk past and have a look as, well, what the heck is this guy looking at? And when it becomes two or three people, then uh, the crowd starts to form what are these people looking at? And they all look up. So yeah, social proof is a, a big, uh, a big thing with our lives.

[00:47:03] Tony: And that gets used, um, in all sorts of ways. And one of the ways it gets used that again in the affluence book, uh, in influence book is, um, you know, when uh, when a movie wins an Academy Award, they reissue it and put out a poster with Academy Award winning, um, icons all over it. Because that’s the, you know, the proof that social proof that this is supposed to be good might be rubbish, but, you know,

[00:47:27] Tony: it’s still, it’s still, you know, some kind of social proof, similar sort of thing.

[00:47:31] Tony: It’s three people telling you this is a good movie.

[00:47:34] Cameron: hmm. Remember when I was a kid, I used to say to

[00:47:36] Cameron: my dad, well, so-and-so

[00:47:38] Cameron: said It’s a good idea. He said, if so-and-so told you to jump off a bridge, would you? What? He, uh, probably should have said, well, no. But if three people told me to jump off a bridge,

[00:47:48] Tony: Yeah. maybe the

[00:47:49] Cameron: I would probably, I.

[00:47:50] Tony: Maybe there’s a tiger on the bridge.

[00:47:52] Cameron: Yeah. But I, I like, I think, and again, getting back to the benefits of having a system like QAV, or it doesn’t matter, whatever system that you’ve got it, one of the advantages is it helps you avoid the pressures of social proof, which is wired into us.

[00:48:10] Cameron: It’s very hard to fight that psychological pressure to follow the herd,

[00:48:16] Tony: Yeah, that’s right to jump. And that’s, and that’s the other point to make. If you don’t have a framework, it’s, um, you’re always gonna find that the market’s throwing up new situations to you. And if you don’t have a framework to deal with it, you’re gonna stand there and panic or look like a rabbit. In the headlights of a car

[00:48:32] Tony: or, or jump the wrong way, jump with the crowd.

[00:48:36] Tony: So that’s why a framework is important.

[00:48:38] Cameron: All right, Tony, you gotta pull pork for us this

[00:48:40] Tony: I have, yes, this is a request. Interesting request. Um,

[00:48:44] Tony: by the

[00:48:44] Tony: way, company I wasn’t that familiar with, so, uh, I had to do a bit of research on this one. The company’s called

[00:48:49] Tony: Money Me

[00:48:51] Tony: MME.

[00:48:52] Cameron: This request, by the way, comes from Matt Walker,

[00:48:55] Tony: Ah,

[00:48:55] Cameron: built the

[00:48:56] Cameron: regression testing system. So, and the other questions that we got are from his dad Toby. So it’s just the, it’s the Matt and Toby Walker show

[00:49:03] Tony: right. Good. Well, I think if they get that regression model, um, running, I think we arm a few answers to questions.

[00:49:12] Cameron: Yeah.

[00:49:13] Tony: Yeah. So MME FinTech company, uh, delivering loans digitally to customers using a quick credit scoring system in a, in an app. And their products include personal loans, car loans, although they do do the car loans through brokers.

[00:49:31] Tony: Um, and they have a credit card called the Freestyle credit card, and they use a free credit score checker, which is backed by Equifax, the credit score company that banks use as well. And I guess the whole, uh, process or the whole benefit of this company is that you can get access to money fast. So it’s not like.

[00:49:50] Tony: Going into a bank branch and waiting days where you fill out application forms and having it assessed and all that kind of stuff. It’s, it’s, um, 24 7 and you can, you can get a quick, quick answer because the credit scoring is done there. And then, um, yeah, so they emphasise fast service and quick access to funds.

[00:50:07] Tony: Founded in 2013, uh, they listed on the ASX in December, 2019. At a dollar 25, early 2022 Money me acquired a competitor called Society one for 132 million. Society one was originally a peer to peer lender, uh, matching. Private lenders who were looking for yield with borrowers who were searching for loans, and that wasn’t a bad idea.

[00:50:33] Tony: However, they did have some issues with the regulators and, uh, had the pivot and change their business model to be more like MoneyMe’s business model of, um, lending, uh, funds raised institutionally, uh, to consumers. Uh, the deal included some MME shares as part of the purchase, which came out of escrow in early 2023.

[00:50:54] Tony: So there was some selling back then. Uh, mid last year, MME undertook a capital raising at wait for it 8 cents a share to predominantly pay down debt. So listed at a dollar twenty-five raised capital last year at 8 cents a share, the founder, a guy called Clayton Howes, was diluted from 18.3% down to 6.9%, and they raised, uh, the raising raised thirty-seven million dollars.

[00:51:19] Tony: Um, and I guess, uh, at around that time when they brought, brought in some new shareholders and also following interest rate rises, the company decided to pivot to, uh, to profitability from growth. So the December, uh, I’ve got December, 2020, uh, 20 December twenty-three half-yearly result shows a profit of $6 million for the half with a reduction in revenue to 105 million down from a hundred and twenty-one million, and an increase in credit, uh, worthiness or credit performance with loan losses reduced from 6% to 4.6%, half on half.

[00:51:57] Tony: And the loan book balance is $1.2 billion. So they’re, they’re basically. Saying they’re not gonna keep trying to grow the company as aggressively as they were, and then they’re gonna try and make some money out of what they’ve already got, which isn’t a bad idea, I think. Um. A couple of things that have happened in the last few months, which, uh, piqued my interest.

[00:52:17] Tony: In November, December, the auditors were replaced, and in December that the CFO resigned with no apparent successor. So both are potential red flags on the surface. Uh, couldn’t, couldn’t see a qualified audit in, uh, the last annual report. So it may just be that the auditor turned over his business as usual, but it has been raised with us in the past that if we see a qualified audit and then the auditors are replaced, that could be a, uh, and then the QA goes away.

[00:52:46] Tony: That could be a sign that, um, there’s an issue somewhere, uh, in the figures still. But the new auditor isn’t as, um, isn’t, uh, as upset by that as the new, as the old one was. Um, the CFO resignation announcement said a search for replacement would begin immediately. The CFO had been there for four years and is moving on to other things.

[00:53:07] Tony: Um. And it could just be a small company issue that they haven’t had a successor in the wings, um, or the CFO. But it does seem strange that both the auditors and the CFO are being replaced late December in the company. So, um, potential red flags I would raise. Uh, it’s, it’s hard to know with a small company like this ’cause sometimes, you know, things just happen.

[00:53:28] Tony: But, um, the two things which, uh, which are not a good look usually, uh, getting into the numbers, June 23 numbers are still what’s in, um, stock doctor. And, and so I expect there to be new numbers fairly soon in the stock doctor. And they don’t always reflect the numbers that I just read out then, which, um, I pulled off.

[00:53:49] Tony: Uh. You know, off Google, um, on paper, but I don’t think they’re in stock doctor yet. So just, uh, you know, be aware of that when you’re doing your own analysis on the stock. And I guess be aware in generally at this time of the year that, uh, we’re seeing company reports come out and reading about them in the paper, but they don’t always get into stock doctor straight away.

[00:54:08] Tony: They can take couple of days or a week. So just be aware of the numbers you are using if you’re running analysis at this stage. ADT is small. For this company, it’s $33,000, so it won’t suit, uh, people who have a large portfolio. And I’m doing the analysis on the stock price of $0.09, so 8.70 cents and yesterday or last night it closed at, uh, 8.10 cents.

[00:54:33] Tony: So it was going down as I was doing the analysis, um, e even so that that stock price is way under the consensus target, which I thought was, um, interesting. Um, and. Maybe the analysts know something that, that we don’t. But, um, anyway, uh, going through the numbers further, there’s no yield for this stock, so we can’t score it for that stock.

[00:54:56] Tony: Dr. financial health and trend is strong on recovering, so we get, um, we like those companies with recovering, so it gets an extra point for that. PE is 2.28, so very low PE, so it’s, and it’s the lowest, and I guess the only because, uh, up until this last half it hasn’t been profitable. Um, but I will score it for that.

[00:55:17] Tony: It’s a very low PE, and PropCap is only 0.3, three times. So again, very, very low. Um, but this is a digital bank, so Opcash can be different to our normal industrial, you know, coffee shop type companies. Um, however, there was, uh, cash was, uh, increased by $11 million in the, in the last year. So I think, um. The Opcash is positive for this company and, um, it’s still a, it’s, even though it may be different because we’re really looking at the difference between revenues from customers being operating cash flow and then what they’re paying out to the people, their bondholders or you know, the fund, the people who’ve they borrow money from to lend to consumers.

[00:56:01] Tony: That difference in the margin is really their operating cash flow. It’s a bit of a different calculation, but it’s still reasonably strong. IV‑I for this company is 20 cents IV-II is 19 cents and the price is 8.10 cents. So it’s well below IV‑I and IV-II, and we don’t see this very often, but two times share price is less than IV-II, which gives us another point.

[00:56:22] Tony: Net equity per share is 21 uh, cents per share. However, net tangible assets is 9 cents per share, so fair. Bit of good will there. Even at 9 cents, we’re still able to buy this, uh, for less than book value. And interestingly enough, it, it’s probably what the, the market is focusing more on, given the share price is 8.10 cents and NTA is 9 cents per share.

[00:56:45] Tony: Um, so, uh, we give you the score for that. earnings per share growth is minus 48%, so we give it a minus one, and I think that’s probably what is going to be driving the share price in the short term anyway. Uh, the fact that they, they expect profit to be lower, uh, going forward. Directors hold 19% and the owner is still a, um, on the board and still owns a share.

[00:57:10] Tony: So we give it a tick for in the founder. Um. Three PTL sentiment is negative, but it’s a bit hard to see because, oh, the red layer shows that it’s being very below its cell line, but it’s one of these stocks that went from a dollar 25 down to 8 cents. So, um, even looking at a three year graph, it’s still hard to to see, ’cause the, the last year or so is pretty flat.

[00:57:30] Tony: Even looking at the, the one year graph monthly, um, I think it’s still below its cell line, uh, uh, ’cause it’s been going up and down. But, you know, the, you can draw a cell line on the one year graph and it’s still below its cell line. So sentiment’s definitely against this and I wouldn’t consider buying it until it changes.

[00:57:47] Tony: Uh, the last thing to look at is consistently increasing equity, which it has. So all in all, the score, the company’s score for this is very good, which is why I think Matt Walker raised the, this is an issue or was one to look at. Quality’s 14 outta 16, which is 88%, and Qiv’s score is 2.62, which is very, very high, but sentiment is negative.

[00:58:08] Tony: So, uh, um. I, uh, I wouldn’t buy this stock until sentiment returns. You don’t need to wait, I don’t think, for the five-year sentiment to return. In other words, we don’t need to wait for the share price to go from 8 cents up to approaching a dollar twenty-five again. But, um, at least on the one-year graph, it needs to be a buy.

[00:58:28] Tony: Using our three-point trend line analysis potentially on a longer time period than that would be good. Um, couple of other things to note about this. Uh, if I can talk about, um, uh, I, I’ll call them strengths and weaknesses, but, um, it’s not really a, uh, uh, that kind of analysis competitor. Plenty. Um. If people are interested in these kinds of stocks, might be a better buy.

[00:58:52] Tony: Qav score is 0.14, but it’s, it’s, um, it’s not on the, uh, the buy list at the moment for negative sentiment reasons. But if I look at the bread later, it’s a very close to positive sentiment. And, um, it’s below sell line, but the current month is an upturned month. And, and the bread layer won’t take that as L two, even though it’s a, a trough, it’s the second trough to redraw a new line.

[00:59:16] Tony: So, you know, by the end of the month, this could well be a buy of plenty with a QAV score of 0.14 and harm money. HMY has a QAV score of 0.2, but is still, um, again, below its byline, but it is increasing in price. So they, they might be two, uh, companies to look at, um, unless, uh, but also MoneyMe could be, if it turns around its sentiment as well.

[00:59:43] Tony: The other interesting thing to highlight is that Thorn Group, uh, participated in the raising, or in fact, uh, somebody I think who has a stake in Thorn group did, and Thorn Group is appearing on the share register now as a, uh, is having a top 10 stake. Thorn Group was on our bio list a couple of years ago, TGA, but it was Delisted and Thorn group was, um, active in this kind of area too, and in terms of providing, um, uh, loans to customers.

[01:00:08] Tony: And it’s, it came out of the old radio rentals business that, um, leased televisions and washing machines and things to people. So. Don’t dunno if that means anything. If, if, uh, it could mean that the person who invested in Thorn group also thinks MoneyMe is worth investing in. Or it could lead to some other kind of corporate activity.

[01:00:26] Tony: I don’t know. Um, but it’s, but it’s,

[01:00:29] Tony: um, yeah, it’s someone who knows the space who’s a now a cornerstone investor in the company. So that’s MoneyMe.

[01:00:35] Cameron: Tony. Did you work out,

[01:00:36] Cameron: uh, why the share prices collapsed

[01:00:39] Cameron: from $2 20 all the way down to 8 cents?

[01:00:43] Tony: Oh, I think it’s gotta be, I think it’s gotta be debt and capital raisings would be my

[01:00:47] Tony: guess.

[01:00:49] Cameron: dilution with the capital

[01:00:50] Tony: yeah, dilution was in there as well. Um, I. Yeah, and we’ve seen this before any number of times, is that if the current capital raising isn’t enough, then they kinda raise money at 8 cents a share or diluted and, um, less than 8 cents a share, which dilutes things even further.

[01:01:07] Tony: So sometimes he’s, uh, a small cap company can get caught in this dilution spiral and never recover. ’cause there’s millions and millions and millions of shares on issue at, at pennies in the

[01:01:17] Tony: dollar.

[01:01:18] Cameron: hmm,

[01:01:21] Tony: Not saying that will happen with money me ’cause the QAV score is very good for it. But, um, I think the question I ask myself is what’s driving the share price down if the QAV score is so good? And I think two things. I think maybe the operating cash flow is, is boosting the QAV score. ’cause it’s not a typical industrial company.

[01:01:39] Tony: Um, although operating cash flow does look good and it is adding cash to the bottom line. Uh, but I think it’s this, um, earnings forecast of negative, what, what was it? 48%, which I think could be driving the share

[01:01:51] Tony: price there.

[01:01:54] Cameron: I had a look at their prospectus from when they launched back in, what’d you say? It was like 2019 iPod

[01:02:03] Cameron: and the chairman, uh, Mr. Code. Peter code

[01:02:09] Cameron: was really pushing their growth rates

[01:02:13] Tony: Right? Yeah.

[01:02:15] Cameron: Yeah.

[01:02:16] Cameron: MoneyMe has a founder-LED management team that has delivered a strong track record of revenue growth

[01:02:22] Cameron: increasing at a compound annual growth rate of forty-two percent from FY-SEVENTEEN to FY-NINETEEN.

[01:02:29] Cameron: The board and executive team believe the company’s growth profile is attractive and will be underpinned by further penetrating the consumer lending sector, continuing to innovate our product offering and capitalizing on new revenue opportunities. It’s interesting then that you said they’re not focusing on growth, they’re focusing on profitability

[01:02:48] Tony: Yeah. And that’s, that’s really a key for any company that that focuses on growth is what happens when the growth stops. Um, and the company’s now profitable, so I can’t fault it for that. And it’s got $1.2 billion in the loan book. So it’s actually reasonably good that’s had a reasonably successful, um, career, but now the gross out of the business that’s.

[01:03:08] Tony: Giving it a different profile. And uh, you know, I’m thinking about companies like Zero, which have had a big, um, stock, uh, price reduction, um, as they kind of grapple with how do we come off growth and, and return and go to profitability. Um, and that’s always the case. And that’s, and it’s always the case.

[01:03:27] Tony: Growth stocks have to go ex-growth at some stage. They can’t otherwise they take over the world and it’s, it’s just not gonna happen unless it, it’s a magnificent seven in the us which is now attracting so much money. It’s crazy. But, but yeah. Um, that’s always the problem with growth stocks. And, and look it, if it’s as successful, profitable company, I think it will have stay again in the sun.

[01:03:47] Tony: ’cause it, it seems to be doing well on a lot of metrics. Um, the other thing I would say is, uh, around the time it listed, uh, or the time it was founded, there were. Half a dozen of these kinds of companies founded at the same time, or brought to market at the same time, including ones that have been gobbled up by, I think NAB bought, um, one of these, um, uh, Neobanks and I think one went broke.

[01:04:12] Tony: And I think, uh, what was the other one I was thinking of? Um, oh, Latitude, the old GE money I think bought one as well. Um, and Latitude operates in this space as well. It provides the, the loans to buy your Frigate, Harvey Norman and pay no interest for five years, that kind of stuff. So it’s a, it’s a contested marketplace.

[01:04:32] Tony: Um, and, you know, potentially we saw Society one acquired by this company and potentially

[01:04:38] Tony: there’ll be more consolidation in the field as well. So that’s something that people have to be aware of.

[01:04:44] Cameron: mm Good stuff. Thank you, Tony. And thank you Matt for the request. Moving on from Matt’s. Question to Matt’s dad’s. Uh, well, not a question. Well, it was a question when the buy list came out yesterday. Uh, Toby uh, asked me to double. NWS News Corp, which was on the list, uh, fairly high up on the list. And I looked into it and it hadn’t been on previous lists, and I started looking at the master sheet and trying to work it out.

[01:05:19] Cameron: What I ended up doing was comparing the, um, stock doctor data for NWS from this week’s download to the previous week’s download, and noticed that stock doctors had the shares outstanding drop from 578 million down to 28 million, uh, shares outstanding, which thought, wow, really? Maybe Rupert’s doing a big

[01:05:47] Cameron: buyback.

[01:05:48] Tony: I gotta say StockDoctor did this last half as well. ’cause I got sucked into buying news Corp until I realized that the, that the data was wrong. And they actually changed it about a week later. So they, they’ve fallen for the same trap again, but listeners shouldn’t. Um, the, the, if you go into StockDoctor and have a look, the, I think the prior number of shares and the prior half

[01:06:10] Tony: is the correct one.

[01:06:10] Tony: That’s about 570,000, not 29,000 or whatever the

[01:06:15] Tony: number is now.

[01:06:18] Cameron: Well, I looked at Stockopedia and I looked at Yahoo Finance. They were all up around the

[01:06:23] Cameron: 578 million. And then I went to,

[01:06:26] Tony: thousand. Yeah.

[01:06:27] Cameron: yeah, well, yes, it’s in Mill, it’s in thousands in StockDoctor, isn’t it? 578,000 thousand. I went and pulled up News Corp’s most recent report and looked at that

[01:06:37] Tony: did too.

[01:06:38] Cameron: got the same number.

[01:06:40] Tony: Yeah. Pulled out

[01:06:40] Cameron: So where,

[01:06:41] Tony: there. Is it 4

[01:06:42] Cameron: yeah, so where, where’s

[01:06:43] Cameron: StockDoctor getting the 28

[01:06:44] Tony: And they’ve done it

[01:06:45] Tony: twice now.

[01:06:46] Tony: Yeah, the form

[01:06:47] Cameron: I emailed. Yes, I emailed Victor Pasquale, the, uh, data research guy at, uh, Lincoln Indicators and asked him to look into it. He hasn’t replied to me yet. I sent him an email last night on that. So just, uh, be careful of that members when you’re looking at your bios.

[01:07:07] Cameron: Good, good Spotting Toby. Um, another issue I’ve had with Stock Doctor recently too, I’ve had a few new members. You know, when people sign up to QAV stock doctor gives them the QAV filters, Um, well, something’s happened at Stock Doctor, and the filters are in the wrong order. This has happened on and off over the last 18 months, and always the same thing happens.

[01:07:35] Cameron: The new member. Signs up, they get the filters, they, they’re going through the Bible, they download the report, they put it into the checklist, and it doesn’t work. They have all these errors. They then spend hours trying to figure out why it’s wrong. They can’t figure it out. They email me. I spend an hour trying to figure out what’s going wrong and can’t figure it out, and then eventually I go, hold on a second, and I go and check the filters and notice that the filters are in the wrong.

[01:08:04] Cameron: Order. Uh, so I’ve emailed Stock Doctor again about that. Again, they haven’t got back to me. Uh, well, Robert Manfre, who’s the head of the user interface, people said he’d get his team to look into it yesterday, but I haven’t anything back. But this has been an ongoing thing with Stock Doctor over the last couple of years.

[01:08:21] Cameron: I dunno what happens on their end to bugger it up, but, um, it seems to bugger it up. So if you are a new QAV member and you’ve, you’re, you know, you’ve downloaded your, your filters from stock doctor and it’s not working, uh, email me. But look at that. Look at the order that the filters are supposed to be in, in the Bible.

[01:08:44] Cameron: Compare them to the order that your filters are in because the spreadsheet is built for a certain order of data, right?

[01:08:51] Tony: Yeah.

[01:08:51] Cameron: You, you cut and paste it into the. Checklist and it expects certain data to be certain columns. You can easily move them around and stock doctor and fix it yourself, but you know, it’s only gonna take you a couple of minutes to fix it.

[01:09:04] Cameron: But it’s the figuring out what’s broken, which is the biggest pain in the ass. So I apologize to the people that’s happened to recently. Um, the other one from Toby was talking about WAF, west

[01:09:20] Tony: Ah,

[01:09:22] Cameron: Resources. Is that what WAF is?

[01:09:24] Tony: is West African. Yep. Resources, a mining company, gold

[01:09:27] Tony: miner

[01:09:28] Cameron: he says, WAF’s forecast earnings after expenses for the coming year

[01:09:32] Cameron: of 200,000

[01:09:35] Cameron: ounces

[01:09:37] Tony: dollars.

[01:09:38] Cameron: USD equals 140 million. Versus mind-caption works. Expenses of 270 million is a bit of an eye-opener and potential debt-negative. Interested in yours and Tony’s feeling on the company at the moment? Toby?

[01:09:57] Tony: Yeah, so my, my feelings on West African resources is summed up by the sentiment, um, which is going down. Uh, so even though it’s on the buy list, it’s got a QAV score of 0.15. The sentiment’s not great. It’s a Josephine. And, uh, I think gold just recently became a Josephine as well. So the, the gold, the gold market’s turned down a little bit.

[01:10:20] Tony: Um, but again, this might be a stock doctor issue as well in terms of why it’s on the buy list. Because if you look at the front page of stock doctor, it says the, uh, forecast earnings per share growth is negative 38%. Then if you go into the download, it’s saying it’s up 7%. So there’s a disconnect there between those two pieces of data.

[01:10:44] Tony: And it could be just again, that um, uh, yeah, our download is still showing results from 30th of June. I. 2023. We don’t have the latest half-year results in. I’m not sure if they’re out yet, but perhaps the, um, the front page of Stock Doctor has been updated, um, with more recent data and the download hasn’t, but it be, it as it may.

[01:11:07] Tony: Um, in terms of our scoring, it would only take us one, one point off the score, a negative. It would turn the, um, forecast earnings per share to a negative one. Uh, so it’s definitely sentiment, which is, which is, um, downgraded. But negative thirty-eight percent makes sense to me given, um, what Toby said that, uh, you know, they’re forecasting earnings after expenses of 140 million, but they’re doing works of 270 million.

[01:11:31] Tony: So that does seem to be a negative. Um, I haven’t done a deep dive into WAF’s balance sheet, but if it’s been doing things, um. Properly, it should have had depreciation and amortized or depreciation capital set aside to do this. Uh, this works, um, if it’s, if it’s for, for mines that, that already exist, but I’m not sure, um, what’s on the balance sheet or whether they’ll have to, uh, get some more debt or even, uh, do a capital raise to fund the shortfall.

[01:12:04] Tony: Um, hopefully it’s in the balance sheet. They can fund it, um, through normal depreciation, uh, or cash reserves. Um,

[01:12:12] Tony: but that’s worth checking. But yeah, I, I, I didn’t go any further because the negative sentiment just stopped me in its

[01:12:17] Tony: tracks.

[01:12:20] Cameron: Yeah. And, and as Tony pointed out, gold did become a Josephine this week, the underlying commodity. And I think Alex, uh, Franklin posted in Facebook that he’d bought WGX and the share price had just

[01:12:35] Tony: Oh.