Hello QAVvers

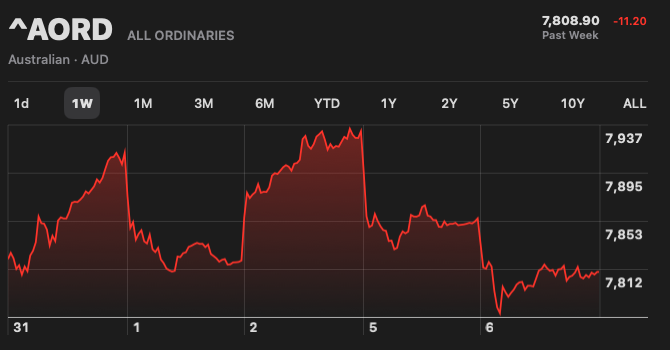

Mr Market hit an all-time high last week, before changing his mind and turning down again. He needs to take a Zoloft.

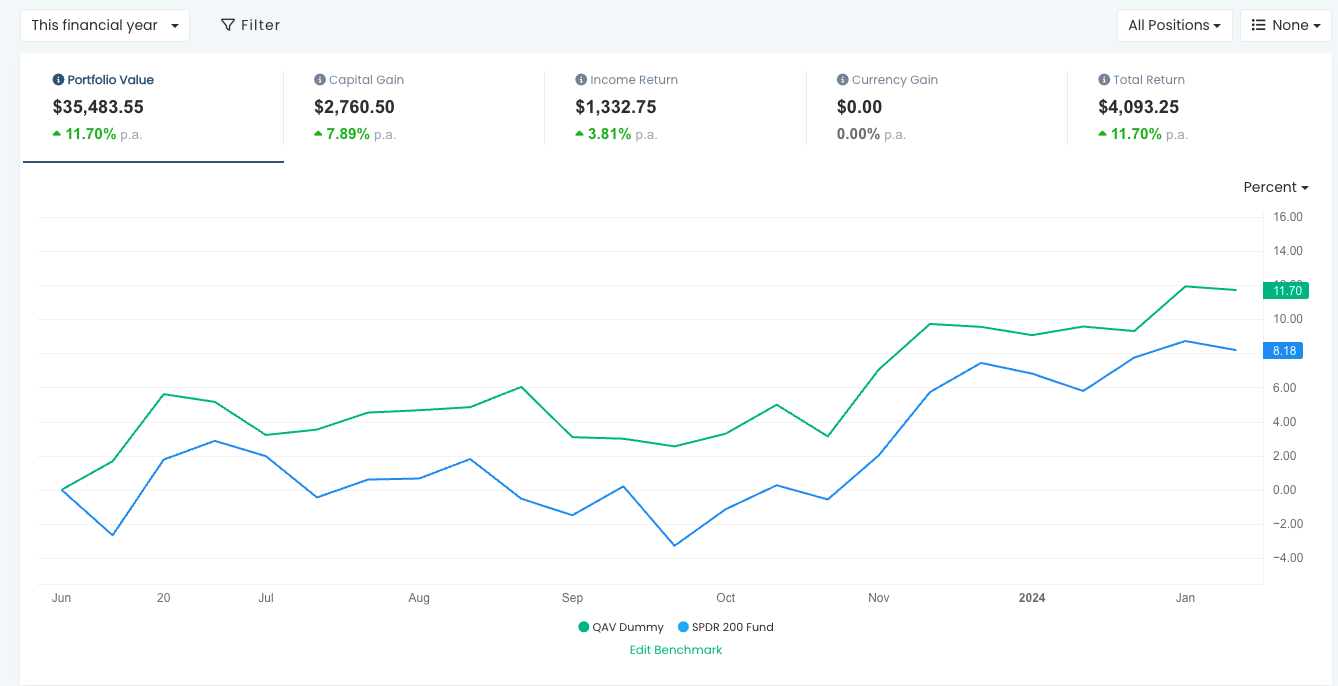

Let’s have a look at the portfolios.

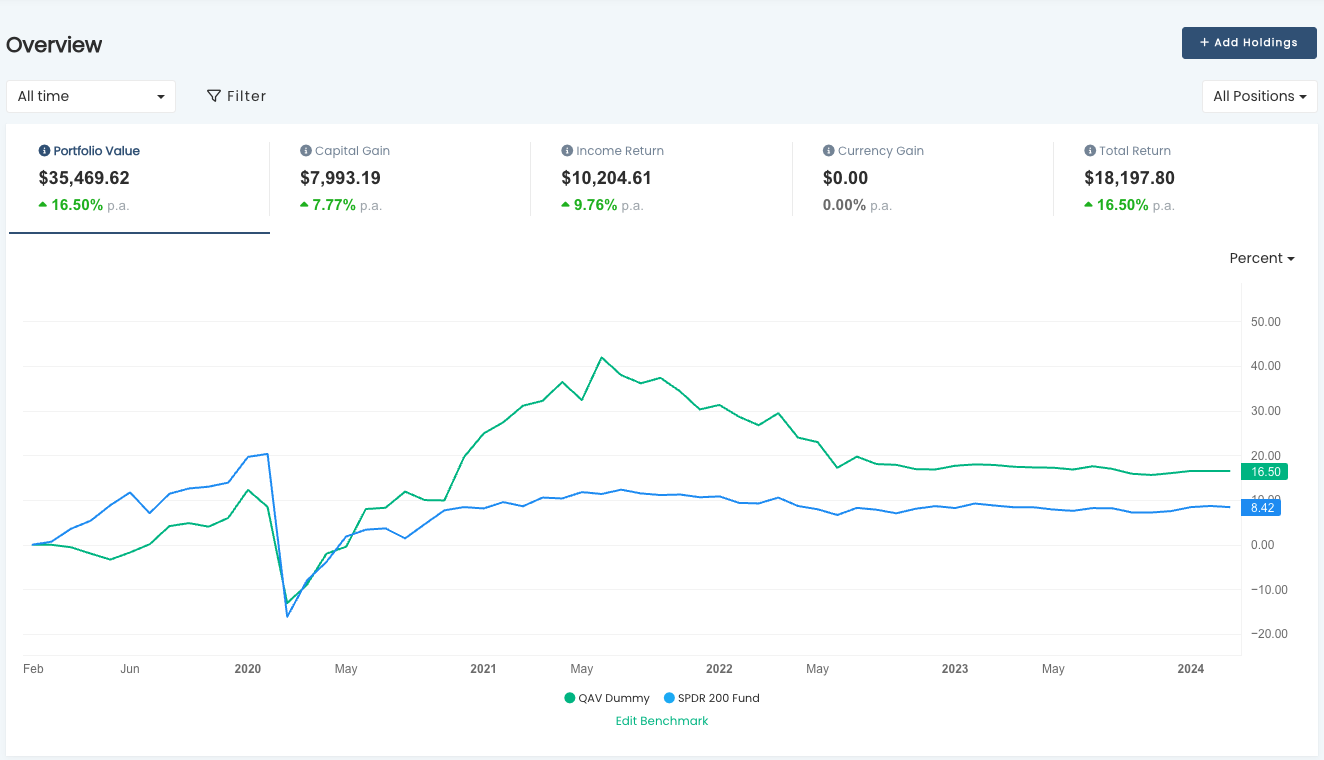

QAV PORTFOLIO REPORT

The Dummy Portfolio is performing well against the benchmark over multiple time frames.

SINCE INCEPTION (15/04/2019)

Our portfolio is still doing slightly less than double market since inception, which is coming up to five years.

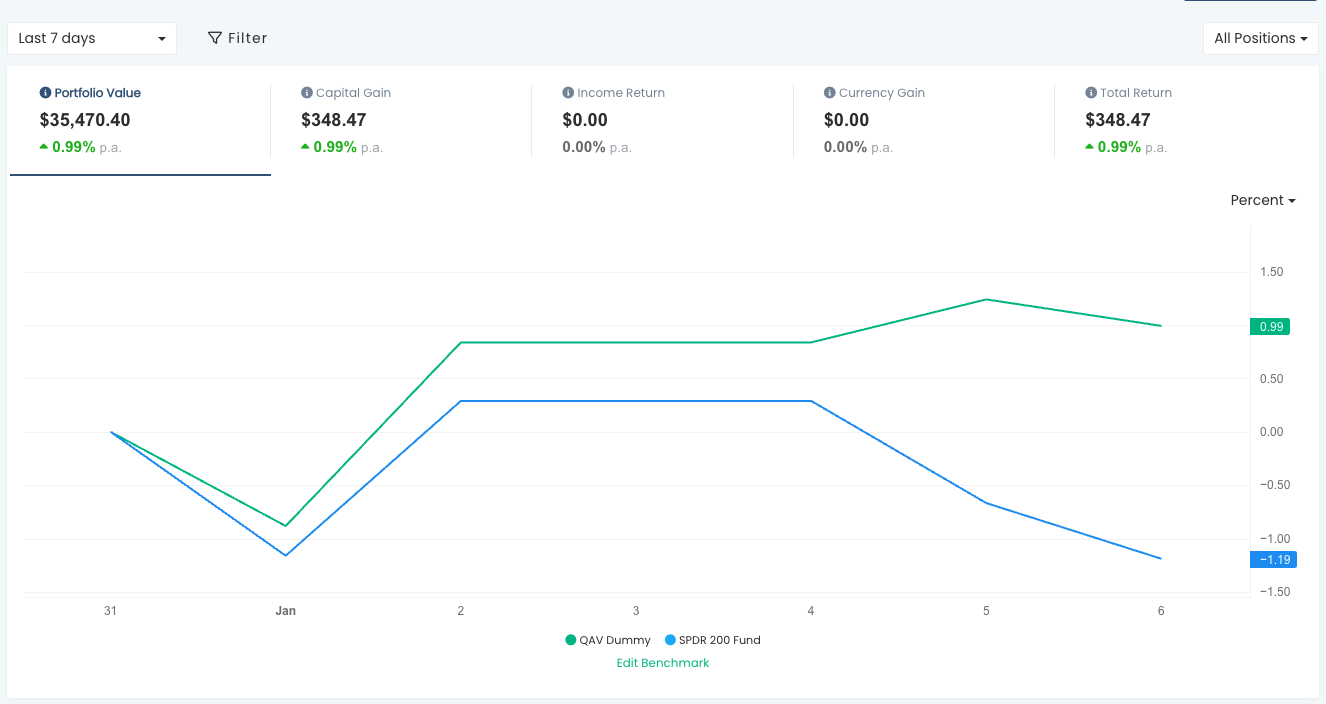

LAST 7 DAYS

It’s performed well in the last week with our current Michael Jordan DUR recovering nearly 10% since last week!

CURRENT FY

RECENT TRADES

No trades in the last week.

QAV STOCKOPEDIA DUMMY PORTFOLIO REPORTS

QAV AU DUMMY

If I look at the Australian Stockopedia portfolio since inception, it’s underperforming by quite a bit. It’s also sitting on 5% cash, which I need to invest. It seems to have started lagging the benchmark around November last year, so I’ll have to dig into why.

QAV US DUMMY

The US portfolio has dropped a lot in the last couple of weeks vis-a-vis the benchmark. Looks like I missed a Rule 1 on MMLP a couple of weeks ago due to an Excel error and it’s now down 17%. I’ll have to deal with that tomorrow.

STOCKS OF THE WEEK

During the last week, we also traded some stocks in our Light portfolios. Details here.

** As always, please check our work, DYOR, and consult a financial advisor before making any investing decisions.

BUY LIST

Each week we produce a buy list that we share with our members. The intended primary purpose of this buy list is for club members to use as a reference for comparing their own buy list. In theory, all of our buy lists should look pretty similar each week.

As always, please check our work, DYOR, consult a financial advisor before making any investing decisions.

THIS SECTION CONTAINS CONTENT WHICH IS VISIBLE TO QAV CLUB SUBSCRIBERS ONLY.

LAST WEEK’S EPISODE

This week we’re talking about:

Munger’s final portfolio, Base-Rate Neglect, Pulled Pork — TLS

Plus, only on the Club edition: Evergrande liquidation, Aluminium and CAA, Fund managers reveal their big investment mistakes, Crypto still isn’t legit, Reporting season about to start, and using Renko chart to track Duratec’s decline.

Episode Transcription

QAV 705 Club

[00:00:00] Cameron: Welcome back to QAV, Tony Kynaston. It’s episode 705. We’re recording this Tuesday the 30th of January, 2024.

[00:00:22] Cameron: How are you, TK?

[00:00:23] Tony: Good. Cameroon, really? Really good.

[00:00:30] Tony: Have you done that thing? Like, I’ve been, uh, writing memos and signing things with last year’s date still. 24th of the 1st, 23. Took me a few

[00:00:41] Tony: days for the brain to click

[00:00:42] Tony: over that it actually was 2024.

[00:00:45] Cameron: You know why I don’t do that? It’s because I never actually write the date. I have code. If I’m writing something, I just write date, and then an asterisk, and it just inserts the date.

[00:00:59] Tony: Yeah, but some things you have to sign and put them

[00:01:01] Tony: date, right? Legal documents.

[00:01:04] Cameron: legal documents, like what legal documents do you think I’m signing?

[00:01:09] Tony: I had to sign a consent for surgery to gel the horse recently, and I put 2023 in it. And I had to sign a proxy, because I don’t live at Cape Schanck, I had to sign a proxy for the AGM down there. I didn’t have to, but I wanted to, to give the, give the chair a vote, and got it sent back to me and said, uh, this is for last year,

[00:01:27] Tony: because I dated at 23.

[00:01:30] Cameron: know. I don’t do anything apart from sit here and record podcasts and go to Kung Fu. That’s my entire life.

[00:01:35] Tony: Ah, living the dream, living

[00:01:38] Tony: the dream.

[00:01:41] Cameron: Uh, well, speaking of living the dream, Tony, the market, you know, it’s, well, at the end of last year, the end of December, it was like, going all guns. The beginning of this year, beginning of January, it fell in a heap.

[00:01:57] Cameron: For the first couple of weeks now, it’s back! With it all, all up since the, well, almost, since when, like, the 18th of January. Just can’t get enough of it. Markets just going gangbusters. One minute down, the next minute up.

[00:02:13] Tony: Pretty hard to predict, isn’t it?

[00:02:16] Cameron: Pretty hard to care about too, really. It’s like,

[00:02:19] Tony: Exactly, it’s noise.

[00:02:21] Cameron: you know the only reason I care is I, I read the Fin, I look at the Fin in the morning. If it says the market’s going to be up, I’m like, all right, well, I don’t need to think about anything today. If it says it’s going to be a rough day, I think, uh, I may need to check the alerts more rigorously than I would otherwise.

[00:02:36] Cameron: But generally speaking, which I haven’t actually even checked my alerts today, I probably should do that. Um, but, uh, generally speaking, it’s all been fairly smooth running. For the last week, a couple of the stocks in our portfolios are close to their sell lines. I think McMahon, McMahon is struggling a little bit.

[00:02:57] Cameron: It’s around a three PTL and our rule one. And, um, what’s the other one? There’s another one that’s been sort of hovering around there for the last couple of days, but I’ve kind of just been letting them hover. You trying not to think too hard about it, seeing where they go, because they’ve been doing it for like a, a week, you know, they’ll sort of hover around that line and they’ll dip below it, but then they’ll go back above it.

[00:03:21] Cameron: There seems to be like a, it’s a support line in there for somebody. Um, what’s, oh, gem is the other one that’s sort of hovering around a real oneself for us. But anyway.

[00:03:34] Tony: well the other thing that’s happening too now is we’re getting, oh well, quarterly updates from the mining sector, but um, you know, Woolworths came out today for example and had to confess that they’re going to take a write down in their annual results, which they’ll present probably next month. So there’s going to be some movements in stocks over the next six weeks or so.

[00:03:54] Tony: With annual results coming out. So reporting season starts in a couple of days. Uh, so be aware of that. Um, and if I, I know I don’t like to predict things, but I’m going to go out on a limb and say, Credit Corp will report early, and

[00:04:06] Tony: they’ll under promise, and the shares will go down.

[00:04:09] Cameron: Well, we talked about this six months ago, I seem to recall, or a little bit after their last results, and I asked the question, should we sell before they report next

[00:04:20] Tony: Yeah.

[00:04:22] Cameron: And you say, yeah, maybe we should, because yeah, I look

[00:04:24] Tony: a trade.

[00:04:26] Cameron: chart for the last year, wow, September was really bad, September they really plunged.

[00:04:32] Cameron: A lot. They dropped down to 12 bucks. They were trading, like, at the beginning, middle of September, they were trading at 21 bucks. By the middle of October, they were down to 12. From 21 down to 12. They’re back up to nearly 18 bucks, 17, 73, you know. Is it part of the QAV system to, uh, just go, well,

[00:04:57] Cameron: CCP’s gonna,

[00:04:58] Tony: That’s a side job. That’s a side deal. It’s a hustle. Yeah.

[00:05:02] Cameron: it’s,

[00:05:02] Cameron: a hustle.

[00:05:03] Cameron: It’s gonna take a hit. We might as well sell it now and buy it again in a month when everyone goes, Oh, they’re fine.

[00:05:09] Tony: Actually, it wasn’t that bad. Yeah.

[00:05:12] Cameron: I’m serious. Like, should we,

[00:05:14] Tony: Are you serious?

[00:05:16] Cameron: I’m serious. Hey, you’re

[00:05:18] Cameron: laughing it off. You don’t think so?

[00:05:21] Tony: Wow. I mean, like I said, it’s a prediction. So it might not

[00:05:23] Tony: happen this year. Seems to happen all the time.

[00:05:27] Cameron: We’ve been doing this show for five years and you tell me

[00:05:30] Cameron: every, you’ve been telling me for five years that’s what CCP does.

[00:05:33] Tony: Yeah. Oh, it

[00:05:35] Cameron: won’t, I won’t do it then. Um, Evergrande, Tony, Evergrande is being liquidated. I remember we talked about Evergrande, wow, like a year ago, two years ago. remember when that bad news about Evergrande first started popping up.

[00:05:52] Cameron: For people that don’t know what we’re talking about, this is this Chinese property development company, one of China’s biggest property developers, it’s been forced to liquidate by a judge after it was unable to reach a restructuring deal with creditors over hundreds of billions of dollars it owes.

[00:06:12] Cameron: According to the ABC, the liquidation could have severe consequences for the world’s second largest economy as the Chinese property sector continues to struggle to recover from the pandemic and Beijing grapples with an underperforming economy. So, you know, there’s always predictions about China’s economy, we’ve talked about this before, this is a big deal though, there’s no denying that, it’s a big deal,

[00:06:38] Tony: Evergrande’s huge. I mean, when I think about Chinese property developers, I think about people building, you know, 10 or 12 high rises in the street, and that’s what this Evergrande was doing. Huge property developer. it got the wobbles a year or two ago and everybody said that’s the end of the Chinese economy and what’s the kind of what’s its impact going to be on Australia because I mean, somewhere else in that article, it talks about iron ore taking a hit.

[00:07:05] Tony: Because, uh, these property developers use a fair bit of steel when they build these buildings. Um, however, again, I don’t want to predict, but, um, further, in a different article in the AFR, the headline is, Citi, which is short for Citi Group, Citi tips Sinoor to reach 150 US on China hopes.

[00:07:29] Cameron: mm,

[00:07:30] Tony: And it goes on, Citi has doubled down on its call for iron ore prices to rally to US$ 150 a ton and has upgraded its copper forecast after China pledged further support for its struggling economy and share market last week.

[00:07:45] Tony: China’s central bank announced that next month it will cut the amount of reserves that banks must maintain. injecting about U. S. 140 billion of liquidity into the financial system. That coincided with reports that Beijing is considering a package of measures to stabilize the nation’s slumping share market.

[00:08:05] Tony: So, and then it goes on. The move sparked a rally across base metal markets, lifting copper prices to a three week high above 8, 500 US a ton. Meanwhile, iron ore futures traded in Singapore hit 136 US a ton.

[00:08:19] Cameron: mm.

[00:08:21] Tony: So you’ve always got to consider the secondary effects, um,

[00:08:24] Tony: not just the headline. But, uh,

[00:08:28] Cameron: So it’s either going to be really bad for the

[00:08:29] Tony: All, yeah, all really good.

[00:08:32] Cameron: good,

[00:08:32] Tony: Yeah.

[00:08:34] Cameron: take your pick.

[00:08:35] Tony: Yeah. And then there’s other articles about how the budget in Australia has been, is in surplus because of iron ore prices and now they’re going to drop and it’s going to affect the whole economy. And it’s like, I wish, I wish someone would raise the price of ink so we could have less of this crap being written about what’s going to happen because, uh, yeah, it’s on the one hand and then on the other hand,

[00:08:57] Tony: um, who knows.

[00:08:59] Cameron: What’s that old, that old story about all I need is a good one handed economist? I think it

[00:09:08] Cameron: was a Truman, Truman quote. So, uh, when you read stories like Evergrande and you read the one side it’s gonna be bad, the other side it’s gonna be good, I’m guessing you just do

[00:09:19] Tony: Tune it out.

[00:09:20] Tony: Yeah.

[00:09:20] Cameron: Tune it out.

[00:09:21] Tony: Yeah. It is a good lesson in the fact that it’s never the primary effects that cause the problem. It’s always the secondary and tertiary effects that you’ve got to look at. And I think Charlie Munger used to say that a lot. Look at the secondary effects

[00:09:33] Tony: for anything that happens. Um, economically.

[00:09:37] Cameron: Well, that leads me into a story I was gonna say for later, but I’ll do it now. This is in The Fin, uh, today. Uh, Fund Managers Reveal Their Big Investment Mistakes. Did you see that one?

[00:09:48] Tony: No, I didn’t.

[00:09:50] Cameron: Uh, it starts off, Benjamin

[00:09:52] Cameron: Graham, renowned US finance professor and author who mentored Warren Buffett, had said, The biggest mistake many investors made was to pay too much attention to what the stock market is doing currently.

[00:10:03] Cameron: That is, they get thrown off course by day to day noise. Graham, who died in 1976, also warned that obvious prospects for growth in a business did not always translate into profits for investors. To take a contemporary example, investors should not assume that soaring demand for batteries in electric vehicles means lithium miners are a good investment.

[00:10:27] Cameron: But then I go on to get, take some quotes for some fundies in Australia and, um, I thought a couple of them really resonated with me. Andrew Mitchell, co founder of Ofa Asset Management, uh, recently confessed on social media that his biggest mistake was to spend too much time and energy analyzing one particular stock.

[00:10:49] Cameron: Sure, as an investor I’ve made mistakes and lost money on investments I’ve made, he wrote, but what made this investment so bad? was the time I put in for the return and the stress it caused. The stock was a tech company selling to multinationals. The knowledge required to analyze the company took a lot of reading and talking to experts.

[00:11:07] Cameron: In the end, Mitchell said he sold the stock because the significant research required to follow a complex business. Wasn’t worth his limited time as a busy fund manager. I fell victim to a common mistake I think many managers and decision makers and companies make. He wrote, make a good call on risk versus return, however, fail to recognize the opportunity cost of the decision in terms of the time it requires and the stress it causes.

[00:11:37] Cameron: What do you

[00:11:37] Tony: I think also too, if you, I think, just adding to that, if you do too much research into a company, I don’t know if you can do that, but if, I’ve seen cases where people switch from being, Hey, I’ve uncovered a great stock to buy, to being an apologist for the company. To, to, Hey, I know all this stuff about, about this industry and this company, it should be doing better.

[00:11:57] Tony: And

[00:11:58] Tony: it’s not. So it’s like, yeah, you gotta be careful on that one.

[00:12:01] Cameron: You get a little bit too invested.

[00:12:03] Tony: Yeah, you become emotionally invested. But getting back to Ben Graham’s comment there, I think that was, that’s a really, really insightful comment. And the, and the, the bit that struck me was he said something about, uh, companies don’t always have their growth prospects reflected in the share price.

[00:12:20] Tony: Um, and you and I were sent a link to watch a documentary about the history of index funds and how the market is. So, all that is told in one sentence, and it’s not completely efficient and all information is reflected in the price. Well, I mean, doesn’t Ben Graham just turn that in its head straight away?

[00:12:39] Tony: I’ve never been a fan of the efficient market theory or efficient market hypothesis, even though Eugene Fama and his mates won. Nobel prizes for it. And it’s still, it’s still taught him business skills today as far as I know. But Buffett pulled it apart in his famous, um, his famous, uh, oh, I was gonna call the story, his famous article, the Super Investors of Graham and Doddsville, which I hardly recommend.

[00:13:05] Tony: Um, and now Ben Graham’s tearing it apart. The growth prospects of a company aren’t always reflected in the share price. And that’s, I mean, that was his classic saying that the share market in the short term is a voting machine, in the long term, it’s a weighing machine. So how do those two things, how does the fact that Graham’s saying there’s some kind of There’s something under the hood which eventually will reveal itself and the market will weigh it correctly in time with Eugene Fama who says, no, no, no, no, everything’s always reflected in the price because the markets are completely efficient.

[00:13:37] Tony: One of

[00:13:37] Cameron: I think the

[00:13:38] Tony: famous investors is wrong.

[00:13:40] Cameron: I think the Graham quote though was saying something different in this article.

[00:13:44] Cameron: the quote is Obvious prospects for growth in a business did not always translate into profits for investors. To take a contemporary example, investors should not assume that soaring demand for batteries in electrical vehicles means lithium miners are a good investment.

[00:14:00] Cameron: So isn’t he saying here that, you know, opportunities for growth don’t necessarily mean the share price is going to do well.

[00:14:08] Tony: Yeah, but like the flip side of that is, to take that battery example again, is if the market is completely efficient then, you know, at some stage it was inefficient because it assumed that lithium was going to be a boom metal with a boom price forever because all the cars were going to be replaced by electric vehicles and have batteries that required to use it.

[00:14:27] Tony: But. You know, secondary effects again, everyone who could, who could open the lithium mine when the price crashed. So it’s like, um, I can’t see that markets are efficient. I think they’re anything but efficient. I think they’re wacky. And again, as Ben Graham said, they’re, they’re, what do you say, they were a moody, a moody neighbor who came to you every day.

[00:14:49] Tony: Some days he was happy and offered you too much for your, your house and some day he was unhappy and offered you

[00:14:54] Tony: not enough for it and you just had to ignore him.

[00:14:57] Cameron: manic depressive. Yeah, it’s well, the way I’ve. Thought about it is that the market is affected by human emotion. Humans are greedy and fearful and, you know, generally speaking, not efficient. You know, they, they get caught up in things and they’re motivated by short term, short

[00:15:21] Cameron: termism, short term bonuses and profits and press releases.

[00:15:25] Cameron: And

[00:15:26] Tony: And easily manipulated by

[00:15:27] Tony: fear and greed.

[00:15:29] Cameron: yeah.

[00:15:30] Tony: Yeah, amongst

[00:15:31] Cameron: the AIs are running the markets, maybe it will be efficient,

[00:15:33] Cameron: but

[00:15:34] Tony: We’ll have to pack up and go home. Ha, ha,

[00:15:35] Cameron: yeah. Well, and that’s what Buffett said at the last Berkshire Hathaway AGM, when somebody asked him about AI, he said, yeah, it’s, you know, as long as humans are involved, greed and emotion is going to stop people from, there’ll still be opportunity in the marketplace because people will still be greedy.

[00:15:55] Cameron: and emotional and fearful and all that kind of stuff, you

[00:15:57] Tony: Mm.

[00:15:58] Cameron: even if they have better tools,

[00:16:00] Tony: Yeah. That’s a good point.

[00:16:03] Cameron: unless you have a tool like QAV. Which teaches you to remove the emotion, but even then, people go, Oh, you know, we’ve seen, we talked about this

[00:16:12] Tony: Nah, yeah, they capitulate.

[00:16:13] Cameron: the, the capitulation, yeah. Even if you, when you have a

[00:16:16] Cameron: tool and a system that says, Ignore the noise, don’t be emotional, just stick to your guns and keep going, keep doing what you’re doing.

[00:16:24] Cameron: Give, just stick to your discipline. People go, nah, too hard. You know, for a whole bunch of reasons, you know.

[00:16:31] Cameron: Well, moving on. Aluminium and CAA, Tony. We’ve talked about this several times over the years. Capral, Capral,

[00:16:41] Tony: Mm hmm.

[00:16:41] Cameron: want to pronounce it. Uh, one of our listeners a few years ago did some good research and contacted Capral.

[00:16:48] Cameron: So my understanding, my recollection of the story is Capral, Produce finished goods for aluminium and they sell those, so they’re not an aluminium miner or refiner, or a bauxite miner, that they, uh, the last time one of our listeners reached out to them about it, they were How they’re affected by the aluminium price, they seem to say that they, you know, they had certain hedging in place to mean that they were passing those aluminium price fluctuations on to their customers and they weren’t really affected by it, because, you know, the reason I ask this is, you know, aluminium became a commodity sell for us.

[00:17:29] Cameron: Uh, last week. And I was looking at Capral again, because it was in one of our portfolios, what we should do. When I compared the aluminium price to the Capral price, I thought they kind of mapped fairly closely. And there’s a little bit of a lag. Between the commodity price and the Capral price. But generally speaking, they seem to follow each other over the last five years.

[00:17:56] Cameron: So I made it, I made a decision to sell Capral out of our portfolio last week, but a couple of people in the forums. questioned my, uh, genius brain. Um,

[00:18:10] Tony: How dare they? I hope you barred

[00:18:12] Cameron: show for too

[00:18:13] Tony: hope you barred them.

[00:18:17] Cameron: So I wanted you to have a look at this, uh, and tell me what you think.

[00:18:21] Tony: Well, I was the one who originally said that we should be using aluminum as the, um,

[00:18:26] Tony: as the graph for for capital. And then

[00:18:30] Cameron: re you sort of reversed that position

[00:18:33] Cameron: last year.

[00:18:34] Tony: you know, I was swayed by the person who contacted capital and said they had hedging in place to, to, to look after it. But, um, I wasn’t sure if it was hedging of the, of the underlying aluminum price or whether it was like a escalator in the contracts for the goods they sold so they could raise prices when the.

[00:18:50] Tony: Aluminium price went up. But it’s, um, yeah, I still lean towards using aluminium as a commodity for capital. Um, it’s a bit like Blue Scope Steel. It’s, these are, these are companies that don’t mind the underline, don’t mind the iron ore, don’t mind the aluminium, but they do, but their price has to change with the rising and falling of the underlying commodity price.

[00:19:16] Tony: Otherwise they go broke.

[00:19:18] Cameron: Right. Well, I did sell it. Um, and let’s see, what did I sell it at? I sold it at 9. 61. It’s 9. 85 now, so it has gone up a little bit since I sold it,

[00:19:33] Tony: Yeah. But as you say, I’m looking at the graph of aluminium physical in Stock Doctor against CAA and they’re, they’re reasonably similar, tracking up and down at the same time. There’s a bit of, bit of a demerger in the last six months. Capital’s done better than the aluminium price, but overall,

[00:19:51] Tony: they’re pretty close.

[00:19:53] Cameron: Yeah, we’ll see how that plays out. Munger’s final portfolio. I thought this was an interesting story in Business Insider. The late Charlie Munger’s final stock portfolio update is out, and it shows his iconic approach to investing. Uh, says Charlie Munger grew Daily Journal’s stock portfolio from nothing to 300 million within 15 years.

[00:20:20] Cameron: The newspaper publisher just filed its final portfolio update from the legendary investor’s time in charge, and it underlines Munger’s exceptional patience, discipline, and conviction. Uh, it goes on to say, skimming through it, la dee da dee da, The first portfolio filing for Daily Journal dates back to the fourth quarter of 2013.

[00:20:43] Cameron: Likely because that’s when the Valley of its Holdings breached the 100 million reporting threshold. The publisher and legal software provider disclosed 2. 3 million shares of Bank of America. Almost 1. 6 million shares of Wells Fargo, 140, 000 shares of U. S. Bank Corp., and 64, 600 shares of South Korean steel maker, POSCO.

[00:21:07] Cameron: Remarkably, Daily Journal held the exact same amount of Bank of America, Wells Fargo, and U. S. Bank Corp. shares a decade later. On December 30th last year, while it slashed its POSCO position to 9, 745 shares in the fourth quarter of 2014, it didn’t touch it again until the fourth quarter of 2022 when it exited the holding.

[00:21:33] Cameron: Munger made Only one other big change to Daily Journal’s portfolio. He bet on Alibaba at the start of 2021, quadrupled his wager by the end of the year, then halved it the next quarter after souring on the Chinese e commerce titan and deciding he’d made a mistake. Possibly when the Chinese government made the founder of Alibaba disappear, Jack Ma.

[00:22:00] Tony: those magicians, Abracadabra, Alibaba, whoop,

[00:22:09] Tony: disappeared, yeah,

[00:22:12] Cameron: Um, it’s worth noting that Munger’s hands off approach wasn’t a winner across the board. The value of Daily Journal’s Wells Fargo and U. S. Bancorp positions rose by less than 10 percent in a decade, while the S& P 500 surged over 150%. 50 percent in the same time frame. The company’s Bank of America stake did better, rising by almost 120 percent in that period.

[00:22:34] Cameron: Munger’s record appears to have been saved by an early bet on Chinese EV maker, BYD. The wager likely made up the lion’s share of Daily Journal’s 138 million in unrealized gains on September 30, and allowed it to realize a 1, 15 fold return on a 3. 3 million wager in late 2021. Even so, Daily Journal’s filings underscore Munger’s commitment to making concentrated bets, buying for the long term, and only at a compelling price, rarely selling, and resisting the urge to fiddle or panic.

[00:23:08] Cameron: What do you think about all that, TK?

[00:23:10] Tony: oh, I think, you know, I actually got a tear in my eye when I read it because it’s just such a shame that Charlie’s not longer with us to just learn from the master even more. But yeah, I mean, it’s a great story. I know that there were others other stories and people out there who said that they would prefer to go to the Daily Mail AGM and listen to Charlie speak than the Berkshire Hathaway AGM, because he just would sit there for eight hours and answer any questions people threw at him, which I guess he did at the Berkshire Hathaway AGM too, but there was less people at Daily Mail.

[00:23:43] Tony: Um, yeah, so somewhere else in the article he He said that the Daily Mail had a maximum number of shares of eight, I think, at any one time. You wouldn’t let the portfolio get above eight. Um, and

[00:23:55] Cameron: Daily Journal, I think, Tony,

[00:23:56] Tony: Daily Journal, sorry, not Daily Mail. I should get that right. Very different. Daily Journal. Um, and, and I think as you read out, there’s probably only really about four or five.

[00:24:07] Tony: Long term in the portfolio. Um, so it’s interesting that BYD was the one that really saved the bacon. I mean, you take BYD out and the rest underperform the index. So that’s interesting in itself. And, uh, and Charlie has spoken about why he bought BYD. He just saw so much upside potential in it, but it’s hardly what you’d normally expect as a value in.

[00:24:31] Tony: Investment, or the kind of stock, a value investor would buy. So that was an interesting one, I think.

[00:24:37] Tony: Um, Yeah,

[00:24:41] Cameron: Yeah, interesting that like it didn’t really, the rest of the portfolio didn’t perform well. So even Charlie with his great genius and taking long term bets and sticking in there, you know, one out of the five there really seemed to do well. All

[00:25:00] Tony: not unexpected. Is it? Really? It’s just, that’s what normally happens in the portfolio. but it’s interesting. It’s, it’s a small, I think the learnings for me are, it’s a small concentrated portfolio, he didn’t tinker with it much. And I wonder whether his non tinkering was the fact that he had so many other things to look at that, five shares in the.

[00:25:19] Tony: Daily Journal’s portfolio didn’t, you know, wasn’t top of mind for him very much. But, but he doesn’t probably tinker with things anyway. Um, his theory was fine on the other, other four, uh, Bank of America and, uh, Wells Fargo, et cetera. He bought those during the depth of the GFC. And they looked really good in the early days because they all went up a lot and he possibly even hung on to them for too long because they’ve gone back to being below index over the last, what, 15 years since then?

[00:25:51] Tony: So, yeah, perhaps he made a mistake, but it’s classic Charlie. He pretty much did everything right. And, um, even the Alibaba excursion, I mean, that’s interesting in itself as well, he got very bullish on China a couple of years ago, bought Alibaba and then doubled down and then sold it again. So, um, he’s, he was, it’s kind of like some, you know.

[00:26:16] Tony: Sometimes where I get to with QAV in the Australian market, that I can’t find things big enough to buy on our buy list. Um, and I think Charlie probably had that problem as well. So they were looking overseas. Um, and I think also too, as their, as their fame spread, they were getting lots of pitches from overseas fund managers and investors and brokers to look at these companies.

[00:26:37] Tony: So they were, they were exposed a lot more to them. Um, cause there’s a lot more overseas companies now in Berkshire Hathaway than there was. 20 years ago, for example.

[00:26:52] Cameron: Morgan Housel, 101 Little Ideas. Didn’t do one last week. This week, I’ve got two. They’re, uh, they’ll fit together though. The first one is Base Rates. The success rate of everyone who’s done what you’re about to try. Then, the next one is Base Rate Neglect. Assuming the success rate of everyone who’s done what you’re about to try doesn’t apply to you, caused by overestimating the extent to which you do things differently than everyone else.

[00:27:20] Cameron: A

[00:27:21] Tony: That’s like the Dunning Kruger effect, isn’t it?

[00:27:24] Cameron: little bit. A little bit. Yeah,

[00:27:26] Tony: I, I mean, I, I come across this all the time and it, um, it’s why I always emphasise if, you know, if you’re getting into the share market, um, work out what kind of investor you are, dip your toes in, um, have a paper portfolio, have your framework set, and then, once you’ve trialled it for a while, then start to invest, don’t Don’t just jump in and lose money.

[00:27:47] Tony: That’s the worst thing you can do. But yeah, I mean, like, uh, you see it a lot with share investors. Oh, I bought Bitcoin 000. It’s, I’m a genius. It’s like, no, you were just lucky. You were just around with money in your pocket at the right time. Um. You know, it’s, it’s, yeah, it’s a great, great, uh, concept, base rates and base rates neglect. And I also, I remember in the dot com boom, like, we would sit around over coffee and barbecues and things, me and my mates, and think, oh, we can’t miss out on this boom.

[00:28:18] Tony: How are we going to set up a dot com company? And we’d have all these great ideas. And then I’m like, do we really know about this? How do we, how do we actually add value to this process? And they’d be like, oh, stop it. You’re just

[00:28:29] Tony: a bloody killjoy. Let’s get into it.

[00:28:32] Cameron: Hmm. Whereas I actually did start a dot

[00:28:35] Cameron: com company twice,

[00:28:40] Cameron: thinking that I would be smarter than the average cookie. And you know, I know what, I know what business success rates are normally, even outside of dot coms, you know, classically 50 percent of businesses that get started don’t, small businesses don’t survive the first year. And 90, 90 percent of those that do survive the first year don’t survive the next four years.

[00:29:02] Cameron: So five years, the failure rate is extremely high. Dot com businesses is probably even higher than that. But it reminds me of when Hunter, my son, said he wanted to become an actor. And I was like, you know, you realize what the success rate of people who do that is? He goes, yeah, but you know, they’re all idiots, you know?

[00:29:23] Cameron: By the way though, he, you know, the boys are in LA at the moment. Hunter’s, Hunter’s going to New York. He got an invitation to fly to New York. He’s being flown to New York, put up at a hotel and he’s going to the Tommy Hilfiger event at Fashion Week in New York. He has to get there a day early because they have a stylist who’s going to fit him out with Tommy Hilfiger gear for the sort of the red carpet event because you have to be Style to be on the red carpet, apparently.

[00:29:52] Cameron: So I’m like, uh, dunno, as long as you’re prepared to sleep with someone there afterwards, it could be the big break for you, you know, who knows?

[00:30:00] Tony: Good. Good on him. Good luck.

[00:30:02] Cameron: Yeah. He could, you know, just stumble his way to success. But so, I mean, I, I think in all of those things, there’s a certain amount of talent involved in that industry, but 99. 9 percent of it is luck and timing. I think,

[00:30:18] Tony: Luck and timing. And

[00:30:19] Cameron: has to happen to someone.

[00:30:21] Tony: Oh no, absolutely. Yeah. But like, yeah, as we spoke about before, there’s a, there’s often in most industries there’s a pyramid and we only hear about the people at the top. you look at the sporting salaries, same sort of thing. Someone just made three million bucks winning the Australian Open last week.

[00:30:35] Tony: But, you know, there’s someone, I remember meeting, I think it was the last person, the last Australian to win the Australian Open. Had a few beers with him and really enjoyed his company. And Mark Edmondson. And, uh, this was going back in the mid 90s when I, um, was, I was, uh, at an IBM event, it was actually the Australian Pro Am tennis and played tennis with him.

[00:30:59] Tony: And, um, and then I, like, afterwards we’re having a few beers and I said, um, so what are you up to these days? And he goes, oh, just finished laying the concrete on a, on a tennis court. So he was reduced, like, this is the Australian Sporting Champion, um, I think the last Australian to win the Australian Open.

[00:31:16] Tony: And he’s, 20 years ago, he’s, he’s laying concrete on tennis courts to make a living. It’s the life. Yeah.

[00:31:23] Tony: The pyramid has a very steep slippery slope, Wheatley,

[00:31:26] Cameron: It’s like the Johnny Farnham, John Farnham story, right? After his first splash of success in the late 60s, early 70s, by the time Glenn, what’s his face,

[00:31:39] Tony: Wheatley

[00:31:41] Cameron: Wheatley started working with him in the mid 80s, he was, yeah, building houses. I think he was like a plasterer or something like that. He was, you know, a tradie on the tools, back before that was the quick way to get rich in Australia was being a tradie.

[00:31:55] Cameron: You know, he was just doing trade y stuff.

[00:31:58] Tony: yeah. Well Tom Baker, when he heard

[00:32:01] Tony: he’d won the part for Doctor Who was on a building site,

[00:32:04] Cameron: yeah. Yeah, yeah. But he hadn’t been successful

[00:32:06] Cameron: and then failed. He was still working his way up. You know, Farnum had had success. He was like top of the pops, the king of top of the pops in

[00:32:15] Tony: Lady, the, cleaning lady,

[00:32:17] Cameron: or something? Yeah, that’s right.

[00:32:19] Cameron: Well, speaking about crypto, which you did, uh, another story I read this morning in The Fin, I like this, Crypto may have become boring, but it still isn’t legit.

[00:32:29] Cameron: So, I think we talked a week or two ago about the EFTs, uh, launches, but, uh, you scroll down in this article, it’s interesting, it says, the commission’s approval, Federal Trade Commission’s approval of the Bitcoin ETFs was not an endorsement of Bitcoin or crypto more widely, but rather was the result of a court ruling.

[00:32:50] Cameron: that found the SEC’s long standing opposition to Bitcoin ETFs, on the grounds they could be subject to fraud and manipulation, was arbitrary. In a statement, Gensler said that, though we’re merit neutral, I’d note that Bitcoin is primarily a speculative, volatile asset that’s also used for illicit activity including ransomware, money laundering, sanction evasion, and terrorist financing.

[00:33:16] Cameron: For context, some of the other ETFs that have been approved by the SEC include the God Bless America ETF, ticker YALL, Y A L L, an anti woke investment for God fearing, flag saving conservatives, The Inverse Kramer ETF, SJIK, that aims to invest in the opposite of whatever TV personality Jim Kramer recommends.

[00:33:44] Cameron: a VICE ETF, ticker code VICE, that invests in VICE related business activities.

[00:33:53] Tony: So that one’s been around for a long time, hasn’t actually, hasn’t outperformed the market. I thought it might. The sin one. I think it’s been called sin in the past. SIN

[00:34:01] Cameron: All right.

[00:34:03] Tony: only, only holds tobacco and guns and gambling,

[00:34:06] Tony: those kinds of things.

[00:34:07] Cameron: Sounds like our portfolios, really. Everything that’s unpopular, coal mining,

[00:34:12] Tony: Yeah, that’s right. Uh,

[00:34:15] Cameron: Well, that’s my stories for this week. I just, uh, I will be doing another free webinar on Tuesday, February the 6th at 8 PM Brisbane time on Zoom. Look for the link in the newsletters and whatever, but just an opportunity for people, whether they’re just free listeners, QAV Lite, QAV Club, come along, ask me anything about anything, QAV, Kung Fu, Free Will, AI, the history of Christianity,

[00:34:47] Tony: ask about ai, don’t ask

[00:34:48] Tony: about Uh,

[00:34:51] Cameron: Cold War,

[00:34:52] Cameron: Uh, you know, Russia, Ukraine, anything you want, but primarily QAV.

[00:34:59] Cameron: Cause you don’t want to get me started.

[00:35:01] Cameron: Right. Moving right along. What have you got to talk about before we get into Q& A, Tony?

[00:35:05] Tony: Oh, I didn’t have much at all. I say, be, uh, be aware that reporting season’s about to start. Things will get volatile. Shares will move quickly. Keep across your alerts. It’ll be a new month in a couple of days. So reset your alerts. Um, yeah, I think that’s probably it. That’s all I can say at the moment. Uh, I think it’s going to be an interesting one.

[00:35:25] Tony: Um, yeah, Woolworths came out with a write down, I think there’ll be some others. Uh, it’s, there’s been, it’s hard to understand how the share market’s at an all time high. I think Australia just reached that kind of level, um, in the last day or so. The US has been there for a while, um, when inflation is still, still out there, uh, least affecting the wallets that people are going to buy at these companies.

[00:35:55] Tony: So, uh, it’ll

[00:35:56] Tony: be an interesting sort of company reporting season, I think.

[00:36:00] Cameron: Interest rates have been going up, you know, I see Godfrey’s Vacuum Cleaners just went bust today

[00:36:06] Tony: Oh, really?

[00:36:07] Cameron: Yeah, they’ve been around since like 1931 or something, they’re gonna have to shutter 50 stores, but I think that’s mostly from competition from Kogan and JB Hi Fi and places like that. But, um, Yeah, like, you know, we’ve just heard all this doom and gloom about interest rates over the last year, and the impact that’s gonna have on the economy, and, uh, et cetera, et cetera, and yet the market’s at an all time high, so,

[00:36:31] Tony: Yeah, well, the share market’s looking forward to interest rate cuts, but it might get a bit of a rude awakening during this

[00:36:37] Tony: company reporting season. Might not, I’m not going to predict, but yeah, pay attention, people.

[00:36:41] Cameron: When’s the next RBA meeting?

[00:36:44] Tony: Uh, isn’t it the first Tuesday of every month? So it’ll be next week. I think they have January off, so they can all go overseas or something.

[00:36:50] Tony: But, um, yeah, go skiing in Japan or whatever they do.

[00:36:54] Cameron: Mm hmm, mm hmm.

[00:36:55] Tony: but uh, it should meet again in

[00:36:59] Tony: next Tuesday, I think.

[00:37:00] Cameron: Well, by the time we do this show next week, the market will

[00:37:03] Cameron: have come off by 10 percent again, and we’ll see.

[00:37:07] Tony: Yeah. I’ve got a pulled pork to do if you wanted to do that now.

[00:37:10] Cameron: Oh, lovely. Yes. Pulled pork. What are you doing? Is this the request?

[00:37:14] Tony: No, I’ll do that next week. Sorry, hang

[00:37:18] Tony: on. Can you hear that?

[00:37:20] Cameron: Yeah. No. What?

[00:37:22] Tony: Oh, I had a clicking noise here. I think I may have just rested something on the keyboard. Sorry

[00:37:26] Cameron: Oh no, I can’t hear

[00:37:27] Tony: you couldn’t hear it. Good. Um, yeah, so I’ll do the request next week. I didn’t, I actually got up this morning and did this, pulled pork while I was waiting for the notes to come through.

[00:37:36] Tony: So, um, and I don’t normally. Look at the buy list when Alex downloads it and say, Oh, I should look at that one in more detail because there’s very rarely something new that has a large ADT. But, but this week Telstra came

[00:37:50] Tony: onto the buy list. So I’ll do a pulled pork on Telstra.

[00:37:53] Cameron: Wow. We haven’t done one of those, I think since the beginning of QAV. It

[00:37:57] Cameron: was one we did in like 2000 and whatever it was.

[00:38:01] Tony: did we I didn’t think I’d done Telstra.

[00:38:05] Cameron: Well, not, we weren’t doing pulled porks back then but back then when we started, we were taking a stock each week and breaking it down and looking at its numbers. And TLS was one of the first stocks that we ever really analyzed when I was building my checklist based on trying to understand the gibberish that you were

[00:38:22] Tony: that’s,

[00:38:22] Cameron: about.

[00:38:23] Cameron: And so

[00:38:25] Tony: that’s

[00:38:25] Cameron: like episode, episode three or four, I think of the first season we did TLS, you

[00:38:30] Tony: I,

[00:38:30] Tony: think we were using Telstra as an example of how to find Stock Doctor data manually, wasn’t it?

[00:38:35] Cameron: I think that was part of a, yeah, looking at Yahoo finance and doing all that kind of stuff. Hmm, alright.

[00:38:40] Tony: Anyway, so Telstra’s back on the buy list. It’s at the very bottom of the buy list, so it may not be there for long, so do your own research, uh, and, and look, I’ve got to say, I’m, Telstra is one of those companies I’m very ambivalent towards, and I don’t mean indifferent, I mean the dictionary definition of ambivalence.

[00:38:57] Tony: I love it and I hate it, and, and doing this pulled pork just brought out all those emotions in me again, because Telstra’s really two businesses and a couple of years ago they actually separated them into separate companies under a holding company Telstra Group and the market got excited because they thought they’re going to spin off the infrastructure business.

[00:39:19] Tony: Telstra infrastructure. And that’s the part I love. I mean, we’re sitting here talking on Zoom and we’ll put out a podcast on people’s phones that they can listen to. And it’s all done over the backbone of all the telco infrastructure in Australia that, you know, has been around for a long time. And Telstra pretty much owns and manages most of that, if not almost all of it.

[00:39:40] Tony: I mean, Vodafone

[00:39:41] Tony: and Optus will have a bit, but nowhere near as much as Telstra has.

[00:39:45] Cameron: Isn’t it NBN? Isn’t it Kevin Rudd’s, uh, home network?

[00:39:50] Tony: Yeah, well, NBN’s in there now too. I think, didn’t it get sold back to Telstra a year or two ago, I think?

[00:39:56] Cameron: I don’t know, haven’t followed it.

[00:39:58] Tony: Yeah, so I’m not sure, but NBN aside, the rest, like the undersea cables, some satellites, all the data senders, the switches, all that kind of stuff, it’s all Telstra. And that’s the side I love. That just gets on with doing it.

[00:40:15] Tony: There’s very rarely an outage. Occasionally there’s an outage, but we rely on it all the time. To me, that’s a good business. Then you’ve got the other side, which is like the retail arm, which whenever I engage in them, they are just the worst retailers ever. I think I spoke years ago about when I came back to Australia and tried to set up my home phone and my home phone at Cape Schanck and just spent days.

[00:40:39] Tony: in call center waiting queues to try and sort out the most basic of situations. And don’t, don’t even, I don’t even know or try to guess what’s the best mobile service plan for me to be on. It’s just all too complicated. So it’s, that’s the side of Telstra I hate. And interestingly, interestingly enough, in going through some of their more recent, uh, announcements, they, they want to make, Custom, the customer experience part of their growth plans.

[00:41:07] Tony: And I, that wouldn’t be hard to do cause they’re coming off a very low base, but they’ve got to do a lot better than what they, I mean, go to a Telstra store. The last time I went to a Telstra store, there was no one in it. And I got told to take a number and come back in half an hour when

[00:41:22] Tony: it would be my turn.

[00:41:23] Tony: I’m like, there’s no one, there’s no one here.

[00:41:26] Cameron: Walk straight into the OptiShop. Yeah, that’s what I did.

[00:41:30] Tony: Yeah. Well, we actually have TPG here now cause I got so pissed off with using, trying to get onto Telstra. So anyway, that’s the side I hate. Um, I mean Telstra has a great storied history. It’s, it’s, it’s basically a government business that was floated under John Howard, um, in two trenches. But before that, you know, it goes right back to the early 1900s, 1901, I think, when the telegraph lines and telegrams were all put under the, the auspices of the Postmaster General.

[00:42:01] Tony: So for a long time, Telstra was called PMG. And then. Around about the time of World War II, Australia started to realise it needed to have reliable communications with the rest of the world and dropped a few undersea cables and that became, I think, OTC, Overseas Telecommunications Company, and then a bit after that they were combined, became Telecom, and then floated and became Telstra and then just recently had this kind of internal demerger and it’s now Telstra Group.

[00:42:35] Tony: So it’s been around for a long time, um, long, long history. Like I said, one side, the infrastructure side, um, is a good business and it’s growing too because the use of data just keeps, keeps on growing as things become more and more digitized. Um, I did have a laugh when they were talking about, um, increasing their satellite business.

[00:43:00] Tony: And I thought about the fact that I couldn’t get that at Cape Schanck, which was the only place I needed it. So I got Elon Musk’s satellite instead. So they’ve still got a long way to go with their customer service. Um, what else can I say about them? Australia’s largest telco, obviously. Uh, latest Investor Day update called out customer experience.

[00:43:23] Tony: 5G and satellite as their growth areas. And I just put a question mark against those three things, because I don’t think they do any of those things well. So, well, I shouldn’t say they don’t do 5G well. It’s a growing part of their business. But I remember all the hype on around 5G when it came out. And we, I think we had it in Canada, slightly ahead of Australia.

[00:43:44] Tony: And I had a SIM card that could convert from 3G or 4G to 5G. And I’m like, there’s no difference. And I still, I still can’t Name any benefit from 5G, you know, that we, that we get compared to what we used to have, really. It’s, it’s either all happened seamlessly or, um, or it’s all been a lot of hype. But,

[00:44:07] Tony: um, but yeah, so not sure about 5G.

[00:44:10] Tony: Infraco?

[00:44:12] Cameron: on 5G are massively higher than 4G if you’re, if you’ve got a good signal. Like, I get 200 megabits a second download on 5G, which I never would have got on 4G, but Don’t know if you ever try and download or upload anything that big from your phone to care about it. It’s not like you’re not streaming video on your phone.

[00:44:33] Cameron: I mean things like if you’re taking a FaceTime call or something like that when you’re on a walk and you’re away from your Wi Fi in the house, that’s where 5G comes into play really. But if you’re not doing that, if you’re just reading the ABC or the Fin Review on your phone, yeah, you don’t really need the 5G.

[00:44:50] Cameron: It’s

[00:44:50] Tony: Don’t read them on my phone. I read them on my

[00:44:52] Tony: laptop.

[00:44:53] Cameron: Yeah, so if you’re not using your phone for high bandwidth applications, but I think for, you know, people with jobs, uh, who are out and about, you know, doing stuff on their iPads and their iPhones and running corporate apps, CRM apps, ERP apps, Salesforce, all that kind of stuff, you know, a lot of data probably is a good thing.

[00:45:18] Tony: Okay.

[00:45:19] Cameron: I’m just here, like, I hate Telstra with a passion, and I’ll tell you why at the end of this, but I get it, 5G’s good, I’m not gonna, I’m not gonna let you shit talk 5G on my watch.

[00:45:29] Tony: Well, I’m not shit talking you. I just thought that was tremendous hype that I haven’t seen much benefit from, but I defer to your experience.

[00:45:38] Tony: Uh, okay. So,

[00:45:41] Cameron: that’ll be the only time that ever

[00:45:42] Cameron: happens.

[00:45:45] Tony: yeah. What else can I say? So, some of the things which I found interesting, which were also in their Investor Day briefing, um, they are calling out, uh, growth areas being data centers, which makes sense, um, growth in fiber, which might be NBN related, I’m not sure, and security. So, uh, I think they probably are legitimate growths.

[00:46:09] Tony: You know, grow centers for them. Um, probably going back to your 5G comments, the mobile business is seeing 30 percent growth in data usage. So, um, that’s year on year, which is, which is quite tremendous for them. Anyway, I think there’s no point going into Telstra in any more detail. Most people have. Use them or not use them or love them or being pissed off by them over the years.

[00:46:31] Tony: And it’s, yeah, the funny thing is it’s not just Telstra. When I was in Canada, Rogers was the big telco player and everyone just hated, loved to hate Rogers. I had a friend whose husband got a job working for Rogers and she just said, before you say anything, it’s just a job.

[00:46:47] Cameron: Yeah,

[00:46:48] Tony: Yeah, she just had to keep defending herself. Um, anyway, look at the numbers. And this is where it gets interesting because it’s a very large Company, I think it would be a difficult company to run. It’s quite possible that splitting it and floating off infrastructure, Telstra, Infraco, would be a good thing.

[00:47:05] Tony: I think those, but Telstra never came out and said they were doing that, and they’re certainly not saying it now, but it might happen in the future and things are being set up so it can happen. But just the span of all, everything they do must be You know, hell on earth for a CEO to try and manage all the, the fires and the risks and all those different areas.

[00:47:24] Tony: Um, and maybe a bit of focus would come if that it was split up. But anyway, um, we don’t have to worry about a DT ’cause it’s, uh, over, it’s nearly $71 million a day, so it’s a very highly traded stock. On the A SX I’m doing the analysis of the share price of $4, which is less than consensus. Target the yield.

[00:47:43] Tony: Telstra. Telstra for a long time has been, um, considered to be a. As I said once before, a bond proxy. So, uh, you know, something that has bond like characteristics. It’s a very stable share price. It’s probably traded in the 3 to 4 type range for the last five years. Um, and it pays a decent yield, but I think these days with interest rates high, um, the yield isn’t enough.

[00:48:06] Tony: So the yield at the moment is 4. 25%. Um, but it needs to have a yield of 6. 8 percent to score on our checklist. Uh, and I guess it begs the question, if this is the kind of bond, um, then if you can get those kinds of rates from putting your money in the bank, why do you take any sort of risk on and dealing with on, you know, Telstra stuffing things up and the share price going down.

[00:48:31] Tony: So I think that may lead to them raising their interest rate, or their dividends, sorry, yield at some stage. We’ll wait and see on that one. Stock Doctor actually rate them as a star income stock, which we give half a point for in our checklist. But I think You know, if I was a retiree and I can get the same sort of yield with less risk, I don’t think I’d be buying Telstra.

[00:48:53] Tony: I’d probably just buy an index fund, which has a similar sort of yield anyway. Um, Stock Doctor financial health is strong and steady, so that’s all good. Uh, PropCaf for this is just under our cutoff of 7, it’s 6. 79 times. Um, ROE is okay, even though we don’t use it to score with, I’ll just call it out for listeners, it’s 11.

[00:49:13] Tony: 3%, which is On the low side, I guess, but it is a big company with lots of assets. Uh, net equity per share is 1. 54. Um, so share price at 4. We can’t buy this for anything like the book value. Um, earnings per share growth is 10%, which again, isn’t bad for. Company the size of Telstra, but it doesn’t, it’s not enough to score for our earnings per share over P.

[00:49:38] Tony: E. score. Obviously no owner founder, it’s been around for too long, and the current board doesn’t have any large shareholders that we can score. P. E. is still pretty high, it’s 23. 95, but it is the lowest in the last six halves, so we do score it for that. So it is a It is still a reasonably highly priced company.

[00:50:00] Tony: The good thing about Telstra is it’s throwing off so much operating cash flow that we can score it on a ProcCaf basis. It’s a reasonably recent three point trend line upturn, so we score it for that. Just misses scoring for consistently increasing equity. There was one half when, um It dropped backwards slightly, so we can’t give it a score for that.

[00:50:22] Tony: But all in all, quality score of 10. 5 out of 16, or 66%, and a QAV score of 0. 1. So anybody who wants a large cap blue chip type of stock, this might be the time to buy

[00:50:38] Tony: it. So, but have a look and do your own research. Hmm. Hmm.

[00:50:42] Cameron: Thank you, Tony. You know, my, I’ve told you these stories before, but when I was in my Microsoft days, I had a lot to do with Telstra. And, uh, this is like Frank Blunt was the CEO and then Sol Trujillo and then Ziggy Swierkowski and like, there were, it was just like horrible, horrible, uh, just the, the corporate attitude of the company.

[00:51:09] Cameron: Then I go, like I took them, I remember taking all of the senior execs, like the general manager, I think they called them GMs of all the divisions. Out to dinner in New Orleans, flew them all over to the U. S. to meet with Bill Gates and all the execs, Frank Blunt and all the guys, took all the guys out for dinner one night, and this is like 2000 and, no, 1998, 1998, and they’d, they’d been rolling cable out around the country.

[00:51:41] Cameron: Bill Gates had made a big deal, you know, um, that they’d been rolling cable out, um, a couple of years earlier, did the joint venture, uh, with them, but they weren’t making it available. We had all of this cable in the ground, but they wouldn’t make it, I mean, you could get it, but it was like for a thousand bucks a month if you wanted high bandwidth internet access.

[00:52:02] Cameron: And I said to them, why, uh, why? Now, when are you going to make this stuff available, the high bandwidth access to people? And they said, when we’re forced to. I said, what do you mean? They go, well, when we’re forced to by the government, then we’ll do it. And I was like, well, why did you spend billions of dollars rolling out cable if you weren’t going to make it available?

[00:52:25] Cameron: And they said, it’s easy, just stop Optus. So if Optus laid cable in the ground, Telstra laid cable in the ground, it was just to stop Optus from getting, uh, foothold. I said, so you’re, you’re, you’re spending billions of dollars of taxpayers money, because they hadn’t been completely, I think they were like 30 percent or 60 percent floated at the time.

[00:52:48] Cameron: You’re spending taxpayers money to stop Australians from getting access to high bandwidth internet access. And they were like, yep. Because it’s, they were defending their, defending their moat, basically.

[00:53:03] Tony: Instead of working out ways they could

[00:53:05] Tony: sell it for and what margin And what services they could offer.

[00:53:09] Cameron: And if you were a privately owned company, fine, do whatever you want with your money. But when they were still. Partly taxpayer owned, to spend taxpayer money to stop taxpayers from getting access to internet just drove me nuts. And it’s their whole attitude, it was just like their level of arrogance out of all of the senior execs in these companies.

[00:53:33] Cameron: About how domineering they were and, and they were terrified. You know, the longer I spent in there, I realized they had no idea what would happen to telephony revenues and they were right to be terrified as well. Once people had access to VoIP, voice over IP, which is what we’re all talking about back then, now we just call it FaceTime or Skype, but it was voice over IP, what that would happen to their revenue stream, which was.

[00:54:00] Cameron: Telephone calls primarily. They, they knew it was going to white ant their own revenue and they were determined to stop that from happening as long as possible. Even though doing that meant stop, stop Australians from getting access to, you know, bandwidth. And which is one of the reasons why Microsoft dumped Telstra as a partner and went with Packer.

[00:54:21] Cameron: Um, for online, um, services was because Telstra were just dragging their feet. They, they were determined not to give Australians access to fast internet and fast internet enabled services until they absolutely had to. We could have been, Australia, one of the reasons Gates was excited in 95 and, and did the joint venture was Australia could have been the world leader.

[00:54:48] Cameron: in providing high internet access and services on top of that in the late 90s. But Telstra stopped us from being able to do that because they didn’t know what it meant to their voice revenues and also their Foxtel revenues, right? They had the Foxtel JV around at that time, didn’t know what it meant for that.

[00:55:09] Cameron: So them and Murdoch just, you know, prevented, made the NBN rollout really hard as well. All the politics involved in the early days of the NBN rollout and all of the FUD that was going on about, well, satellites versus cable. And, you know, remember Turnbull. You know, and I’ll never forgive Turnbull for this, saying, Oh, cable, putting glass under the ground, that’s going to be outdated in six months.

[00:55:34] Cameron: There’ll all be satellites, it’ll all be like, you know, wireless. Bullshit, bull. And everyone in the industry knew it was bullshit, but just stopped us again. The second time around, we could have had, you know, NBN 10 years faster than we had it, and all of the services that come from that, just. Anywho, that’s my rant over.

[00:55:57] Cameron: Moving right along.

[00:55:59] Tony: so you’re not going to be putting Telstra into the dummy portfolio, I

[00:56:02] Cameron: Oh, I will buy it if I have to buy it. Yeah, them and

[00:56:06] Cameron: Atlas, bloody, what is it, Apollo,

[00:56:11] Tony: Apollo.

[00:56:11] Cameron: Tourism, you know, if they’re in the portfolio, I’ll buy them. I hate them. I’ll do it with gritted teeth, but I’ll do it. Question time. John, can you please do a pulled pork on MTS?

[00:56:26] Tony: Yeah, no, I’d love to. John, I’ll do it next week.

[00:56:30] Cameron: Who are MTS?

[00:56:31] Tony: is Metcash, the third force, maybe fourth force

[00:56:36] Tony: now, depending on how big Aldi is in supermarkets in Australia.

[00:56:39] Cameron: I don’t think they’ve ever been on a buy list.

[00:56:42] Tony: No, I’d be surprised if they have been,

[00:56:44] Tony: but I can certainly do a pulled pork on them.

[00:56:50] Cameron: Cam, hope all is well. Potential question for the show, Duratech? Is my Michael Jordan at the moment. You’re not alone there, Danny. It’s all of our Michael Jordans at the moment. And most of my very modest portfolio gains are in that one share. It’s dropped around 15 percent over the last two weeks, down 5 6 percent again today.

[00:57:11] Cameron: And that was yesterday, and it’s down again today, I think. I’d like to hold my winners, but historically, when I held on to winners, they did crash, and most of the gains were wiped out. I know Renko charts have been discussed as a potential indicator, however, I don’t know where I can find that chart, nor do I know how to interpret them.

[00:57:29] Cameron: I don’t have Stock Doctor. Any insights from you or Tony, thanks in advance, Danny. I, um, did look at this in some detail today, Tony, because, um, I was looking at, um, the dummy portfolio this morning, and Duratech is a star portfolio, a star stock in our portfolio, sorry, and Duratech is a star stock in our portfolio, sorry, and Duratech Uh, you know, it has come back quite a bit, but again, as I always say, I can’t complain about it because it’s, uh, I think we’ve owned it for two years in the dummy portfolio and it’s gone up quite a lot in that time, up like 200 percent or something ridiculous like that since we bought it.

[00:58:19] Cameron: But, um, yeah, it’s, it’s, it’s come back quite a long way. But as I was, I was writing the weekly update this morning and I was looking at the, um, chart for, uh, Duratech over the last year or so, and it, it tends, it’s had a couple of big dips if you go back over the last year or even. Last year, it’s had a couple of big dips where it’s come back quite a long way.

[00:58:52] Cameron: If I go back, say April 23 was trading at a dollar, then it dropped down to about 93 cents. It was almost 10 percent down. Then it went back up and by September 23, it was a dollar 43. Then it crashed down to a dollar 15, uh, over the sort of two weeks. Then it went back up. 1. 30 crashed down to a buck nine and then it went all the way up to a 1.

[00:59:22] Cameron: 70. Now it’s down to a 1. 38. So it has had a number of peaks and troughs since we’ve held it and has recovered. But I mean, there’s always a last time when it’s not going to recover. No tree to the sky, as you’ve said before.

[00:59:37] Tony: Correct. No tree grows to the sky. Yeah. Well, a couple of, couple of points I make. It’s a good question, Danny, and we often get asked this one. Um, I think you make a good point, Cam. It’s nowhere near a sell using the bread later and it could easily keep going up because they, we have stocks that have pullbacks and then have second wins.

[00:59:59] Tony: That’s,

[01:00:00] Cameron: cents.

[01:00:01] Tony: yeah, so it’s got to come down sort of a little bit more than half. And where it is now for it to be a sell. Um, so a couple of things. It just depends how comfortable Danny is taking the risk. You could draw what we’ve called in the past a HUD line. So Danny, if you look at the bread later and look at what is currently, I mean, if you look at the share in general over the last five years, it’s only in the last, um, two years that it’s taken off.

[01:00:31] Tony: Which is why we have this problem, because the L1 and L2 happened before that take off period, so we needed to retrace back to that pre take off sort of share price.

[01:00:44] Tony: So you can decide to draw your sell line using more recent data, maybe perhaps the last two years worth of data. And if you look at the bread later, if you started with what is now L2 and make that L1 and draw a line, then it’s getting pretty close to crossing a particular sell line, a more recent sell line.

[01:01:05] Tony: You could do that. I’d hasten to add that, you know, it’s, it’s entirely possible given the shape of this graph that it’ll, it’ll come back, but then take off again. So, it just depends whether you feel more comfortable missing out than, than taking a profit. Um, that’s the first point I’ll make. Uh, the second point I’ll make is you talked about Renco graphs and I’ve I can look at the Renko graph in Stock Doctor, and it has just turned red, which means it’s a sell.

[01:01:33] Tony: And bearing in mind that Renko graphs are a graphic way of looking at, um, trailing stop losses. Um, and so, it’s, it’s gone up, come back, gone up, come back. So it’s a Renko red at the moment, only just a red, it turned red, it’s now 1. 38 in share price, it turned red at 1. 42. So, um. Using Renko you could sell, but it really comes down to what you’re trying to do here.

[01:02:00] Tony: It’s um, the other thing to look at is, is whether there’s been some announcements which is affecting it and causing the share price to go down because you could red flag it like this CFO’s left or something like that, but I can’t see any recent announcements which would affect the share price to bring it off.

[01:02:18] Tony: So it’s entirely possible it’s a people taking profits just like Danny’s considering doing. Um, because it’s gone up a lot, uh, and they don’t want to lose those profits, they want to bank them, and, or B, that, uh, sometimes coming into company reporting seasons, the fund managers will say it’s not worth the risk of, of something unusual coming out during the announcements and they’ll, they’ll bank it.

[01:02:42] Tony: Bank it for a bit to take a profit or take some profit. So long story short, John, it comes, uh, sorry, um, Danny, it comes down to how comfortable you are. It’s if it was me, I don’t own Duratec, but if it was me, I’d still use the Breda later and I wouldn’t sell because it’s got a fairly, it’s got a reasonable.

[01:03:00] Tony: history of going up and coming back and going up further after that. So this could be one of those times. Um, but if you are feeling like it’s keeping you awake at night, then by all means, it’s, it’s just turned Orenco red. If you draw a more recent sell line, it’s getting close to a sell. So

[01:03:15] Tony: you could take some comfort from either of those.

[01:03:18] Cameron: They did just change managing director at the end of last year, actually, um, Phil Harcourt exited and Chris Oates was effective as of the 1st of December as the new MD, but the share price went up 6. 91 percent as a reaction to that news, so market handled it well. Uh, you know, I was reading that Financial Review article before about the biggest mistakes fund managers have said they made.

[01:03:46] Tony: Selling too early?

[01:03:47] Cameron: I, I, I, I saved a couple. Um, one is from Emmanuel Datt, fund manager and the founder of Datt Capital, says one of his biggest mistakes was selling mortgage insurance business Genworth. Too early, speaking of GEM, Genworth was trading at a fraction of net tangible assets despite positive long term macro trends and a plan to aggressively return capital to shareholders, he said.

[01:04:12] Cameron: It has since returned 30 percent compound over three years in capital growth and dividends. However, we cut our exposure too soon, so we didn’t have the benefit we should have. We learned much from this mistake, adjusting our investment and portfolio management techniques to mitigate this risk in the future.

[01:04:28] Cameron: And then it says, Sebastian Evans, the Chief Investment Officer and Small Cap Manager, NAOS Asset Management, agrees that a common mistake is selling too early, or put another way, failing to recognize that great companies with competitive advantages are worth holding because they increase sales and profit margins over the long term.

[01:04:48] Cameron: If you look at JB HiFi, Rees, Mondelfus, Monodelfus, I know you loved Monodelphus back in the day. These are businesses that many investors sold too early because they felt the market was saturated, or they were too expensive, but over time their moat has allowed them to grow one way or another, and the profit multiple has held or increased significantly over time, he says, selling a winner.

[01:05:13] Cameron: Sometimes referred to as taking profits, is often a more expensive mistake than buying an underperforming business and selling its stock at a loss. So, there you go. I thought I’d save those stories for Danny. Take it, take from it what you will. By the way, there’s another couple of stories here, uh, just finishing these off, which are good.

[01:05:35] Cameron: Richard Galvin, the co founder of Crypto Asset Management Group, Digital Asset Capital Management, says a common mistake made by investors is believing they’re too late to buy a business on the basis it has already risen strongly. And then Jesse Moores, a Co Portfolio Manager and Director of Quantitative Trading House, Spatium Capital, says spending too much on brokerage is a big mistake.

[01:05:59] Cameron: If you pay less on brokerage, you get to keep more, and hopefully generate outperformance for your account versus your broker’s account, he says. The big banks are popular for retail traders, but are the most expensive, so shop around for an online broker. As there are lots of discount ones and this is an easy way to improve returns.

[01:06:19] Cameron: And we talk about that quite a lot.

[01:06:21] Tony: Yeah. No, all good.

[01:06:23] Cameron: there you go.

[01:06:26] Tony: All good advice.

[01:06:28] Cameron: Is there any way outside of Stock Doctor that Danny can find Renko?

[01:06:31] Tony: Oh, it’s a good question. I don’t know off the top of my head. I don’t know if Google Finance or Yahoo Finance has it. But, um, yeah, I couldn’t say. Sorry.

[01:06:40] Cameron: Well, if anyone knows, let Danny know in the Facebook group or wherever. Well, that’s the Q& A, Tony. After hours. Let’s talk about True Detective.

[01:06:51] Tony: Oh, yeah. The twin peaks of our times. Fantastic show. Look, I watched probably half of the first season and it was good quality drama, didn’t quite get into it, but season 4, wow, with Jodie Foster, um, playing a pretty grizzled detective in the Arctic North, and every like episode starts with Day three of the longest night, day four of the long night.

[01:07:18] Tony: They’re just like, they’re going into their never ending nighttime period when the woo woo happens and you see things out of the corner of your eye scuttling across the snow and the ice. And it’s, it’s this great mix of Indian mysticism with a very gruesome murder in the, in the ice. But I’m loving it. I can’t wait every

[01:07:39] Tony: week for a new episode to drop.

[01:07:41] Cameron: Yeah, I haven’t seen the latest episode, but we’ve watched the first two and it was great. Like, yeah, really, really good. Great to see Jodie Foster at her age. I think she’s, I don’t know, 60, something like that. Uh, 65. Uh, you know, with a gritty role like this, it reminded me a bit of, um, What’s Her Face from Kate Winslet, in that show a couple of years ago, where she was a gritty cop, out in some small

[01:08:09] Tony: Mayor of East, Mayor of East town,

[01:08:11] Cameron: Mayor of Easttown, yeah.

[01:08:12] Cameron: Like, uh, these roles of these older actresses doing gritty cops, middle age, late middle age actresses, whatever, I like that.

[01:08:20] Tony: Mm.

[01:08:21] Cameron: And Christopher Eccleston got a bit of a role in this as well, the

[01:08:24] Tony: Yeah, it hasn’t come back after

[01:08:25] Tony: that little cameo. Not much anyway. Yeah. And has

[01:08:30] Cameron: loved every

[01:08:30] Tony: I didn’t like it.

[01:08:32] Tony: Christopher

[01:08:33] Cameron: You didn’t like?

[01:08:34] Tony: I didn’t like his accent. Like,

[01:08:35] Cameron: Yeah. Yeah.

[01:08:37] Tony: So, American cops can’t be born in the

[01:08:40] Tony: UK or be raised in the UK with a British accent? Seriously?

[01:08:44] Cameron: Yeah. The American, the British going in and doing American accents is hit and miss sometimes. I’ve loved every season of True

[01:08:53] Tony: Oh, okay.

[01:08:54] Cameron: Two, which copped a lot of crap. It had Vince Vaughn and um, Colin Farrell

[01:09:00] Tony: Mm hmm.

[01:09:01] Cameron: and I can’t remember the actress, Rachel something, the actress, but I, it got a lot of shit, but we really liked it.

[01:09:07] Cameron: I, I, Vince Vaughn doing a dramatic role I thought was great.

[01:09:11] Cameron: Colin Farrell’s always great. I’m a big fan of his when he does serious stuff and he’s done some Hollywood shit over the years, but he’s uh, you know, a very talented guy. I liked it. Copped a lot of crap, but I thought it was good.

[01:09:24] Tony: I don’t know why, but I started watching Alexander the Great with Colin

[01:09:28] Tony: Farrell playing Alexander. I couldn’t, I couldn’t last.

[01:09:32] Cameron: It was Oliver Stone, yeah, we’re not, not one of his great, yeah, no, um, Val Kilmer is Philip and, uh, Angelina Jolie is, uh, his mother,

[01:09:44] Tony: I didn’t get, didn’t get that far.

[01:09:45] Cameron: Olympia. Oh, yeah, no, terrible. I mean,

[01:09:49] Cameron: I pull out the battle scene. So the, the, the saving grace for that film is the Battle of Gorgomela, which I pulled, I pulled it out and showed Fox recently, but you know, if I ever need to show anybody anything about Alexander, like if anyone ever asked me about why Alexander the Great was the, deserves the epithet, the great, I talk about the Battle of Gorgomela.

[01:10:10] Cameron: Do you know anything about that? You ever listen to my Alexander series? No?

[01:10:14] Tony: Oh, I did a little bit.

[01:10:16] Cameron: Yeah, a little bit. This is like,

[01:10:18] Cameron: it’s absolutely, probably the most epic battle of all time. Alexander, he’s gone into Persia to take revenge to the Persians for their invasion of Greece generations earlier. The, the, the, um, you know, what was the, the The 500 or whatever it was, the Spartans.

[01:10:41] Tony: the 300, Yeah.

[01:10:42] Cameron: Yeah. And, um,

[01:10:45] Cameron: he, you know, he, he, he’s got a, it’s a reasonable size army, but when we don’t know numbers, but from memory, he’s got something like 20, 30, 000 guys. And he goes up against, uh, I think it’s King Darius of Persia, who, It’s facing him with, again, the ancient sources say something like a hundred thousand troops.

[01:11:08] Cameron: He’s, Alexander’s massively outnumbered and the Persians have battle elephants and they’ve just got everything. Like these, this is the dominant, this is like going up against the US military. It’s like, I don’t know, Iraq going up against the US military. And. All of Alexander’s generals are freaking out the night before, and he’s freaking out the night before, and then he just goes to sleep, and then he has this idea, and he wakes up late the next morning, they’re all freaking out, he’s not coming out of his tent, he comes in and he goes I’ve got a plan.

[01:11:45] Cameron: It’s all going to be good. So he goes out and they’ve got this massive Persian army lined up in the battlefield. His army’s lined up in front of it. And as soon as sort of daylight hits, Alexander is, um, on his right flank. He’s commanding his right flank. Somebody else is commanding the left flank. As soon as the battle starts, he and his right flank Just go 90 degrees to the battlefield and just look like they’re running away off the battlefield.

[01:12:18] Cameron: King Darius is in the middle of his army, uh, on his battle elephant, arrogant, and thinks Alexander’s panicking and running away. So he sends his left flank to chase down Alexander. Alexander Expects this, and they’re on this desert battlefield, a lot of dirt, right, so all this dirt and dust is thrown up, no one can really see what’s going on.

[01:12:43] Cameron: His right flank, he judges it until there’s a gap between Darius in the center and Darius’s left flank. When he judges there’s a big enough gap, he just pivots and goes straight for Darius and his right flank comes with him and blocks Darius’s left flank from getting back there. And Alexander himself just rides straight for Darius.