Hello QAVvers

It was a strong week on the local market, with the AORD nudging close again to the 52 week high, before falling back a bit today.

Let’s have a look at the portfolios.

QAV PORTFOLIO REPORT

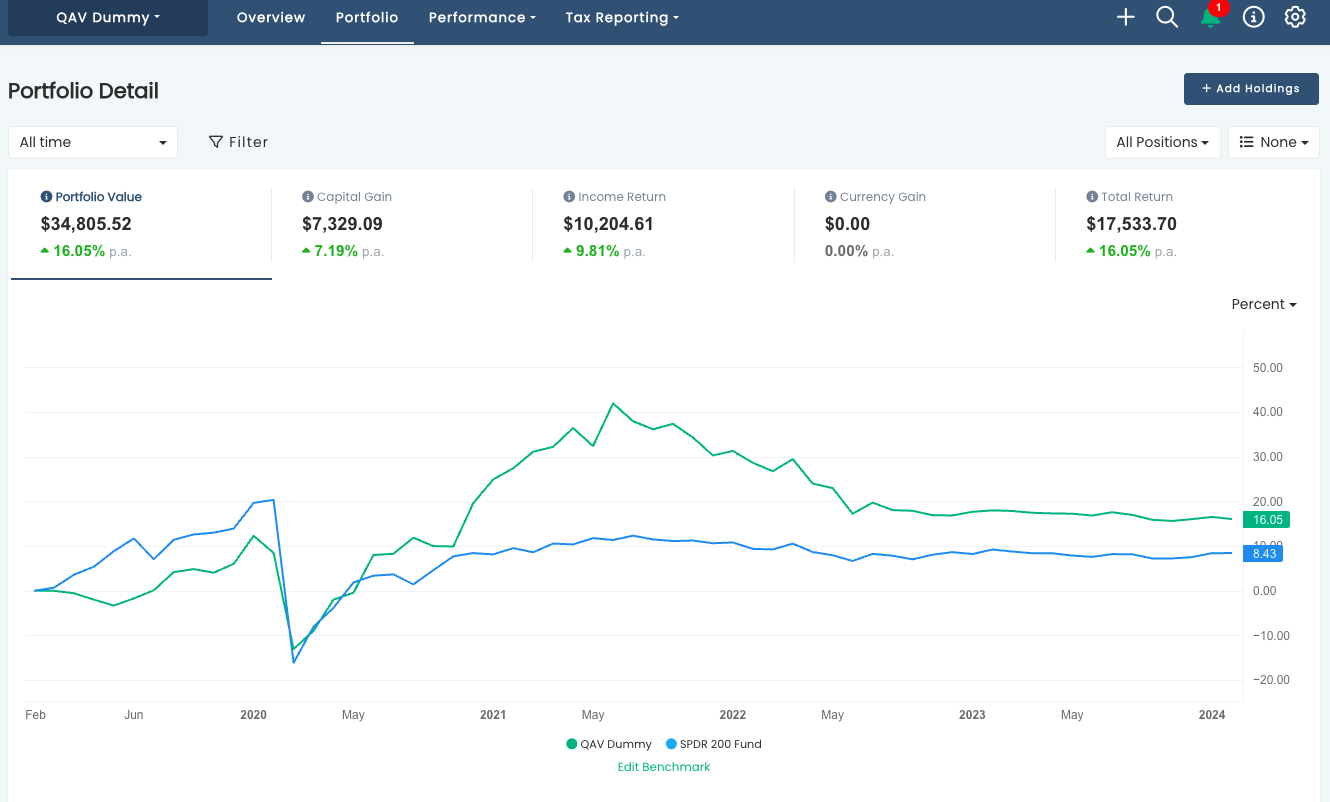

The Dummy Portfolio is performing well against the benchmark over multiple time frames.

SINCE INCEPTION (02/09/2019)

Our portfolio is still doing slightly less than double market since inception.

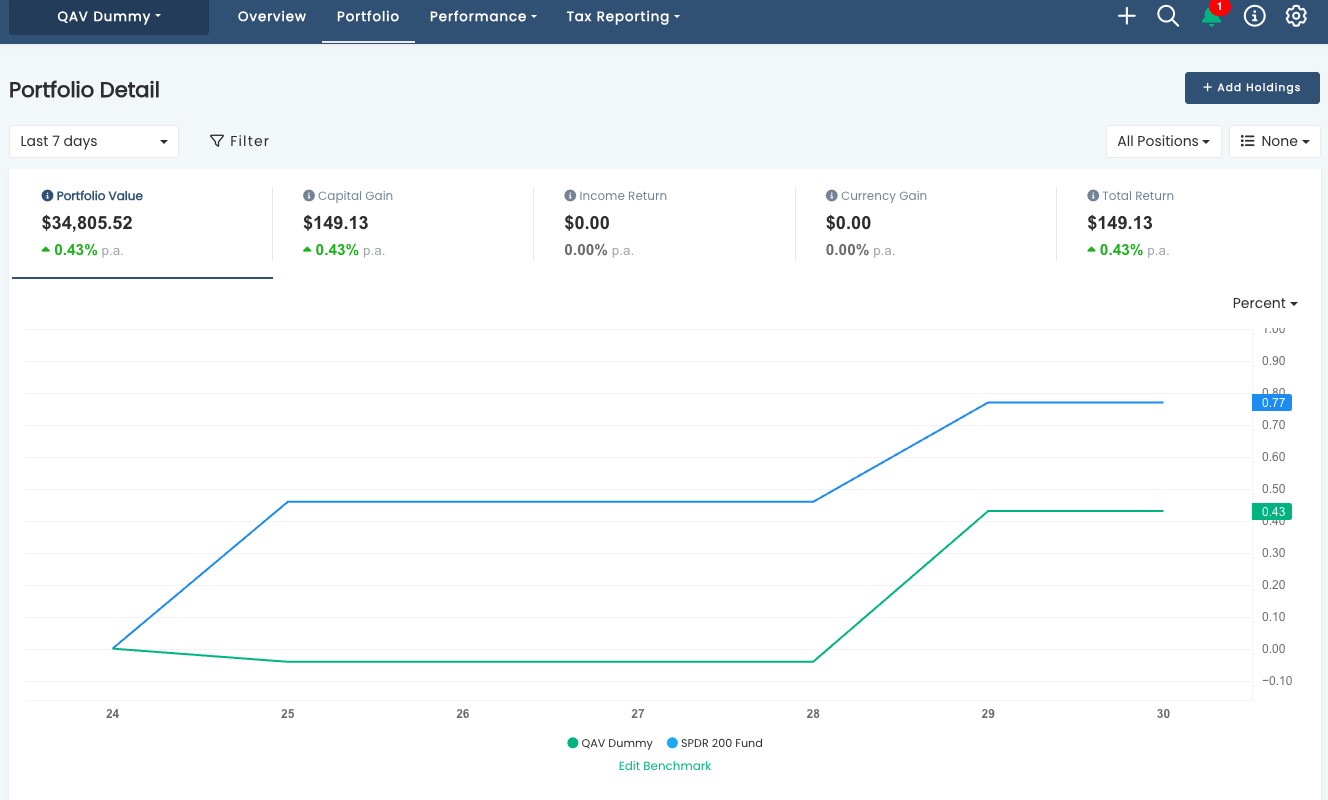

LAST 7 DAYS

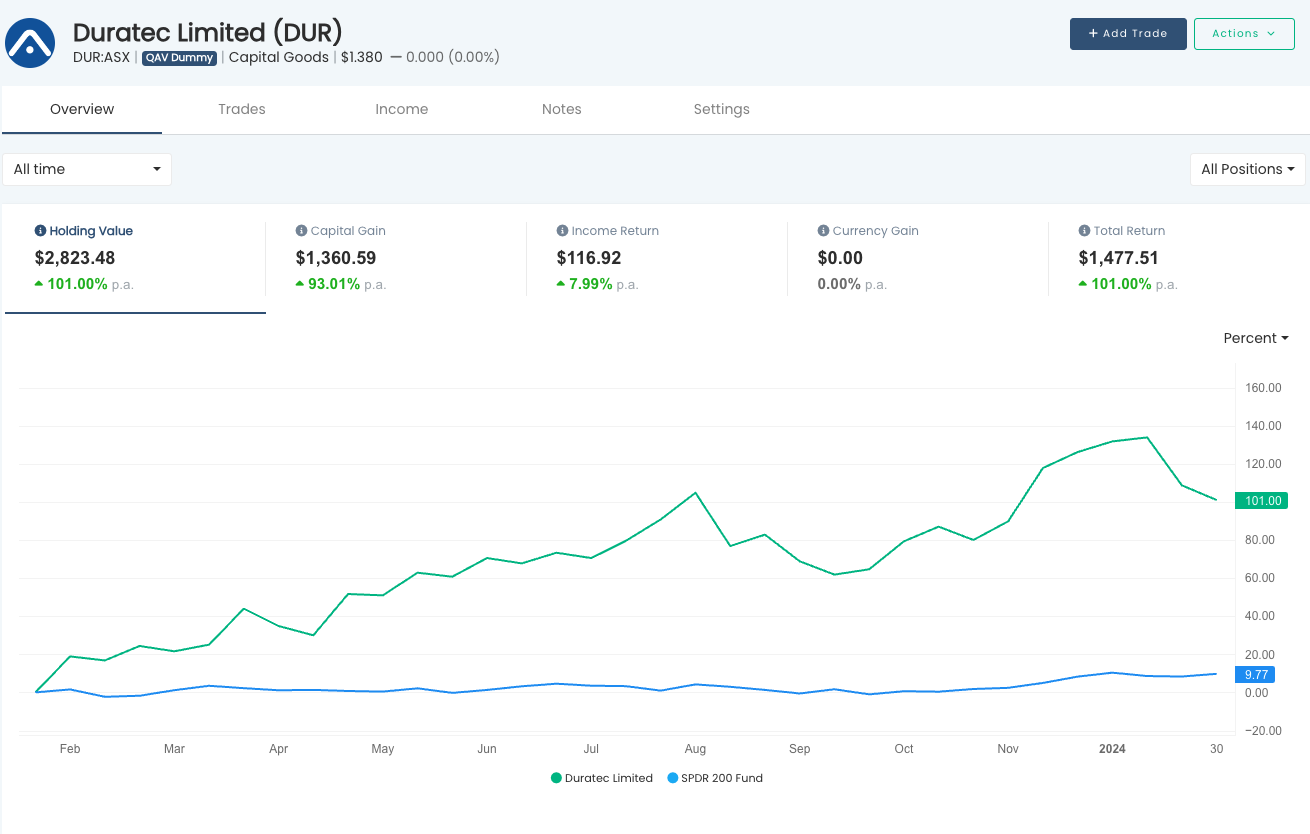

It’s underperformed in the last week with our current Michael Jordan DUR taking a hit, having fallen a long way from its high of 1.72.

I note that DUR has had a few large drops in the two years we’ve held it in the DP and, so far, it’s always recovered strongly. But there’s always a last time. No tree grows to the sky. Our 3PTL is 0.54.

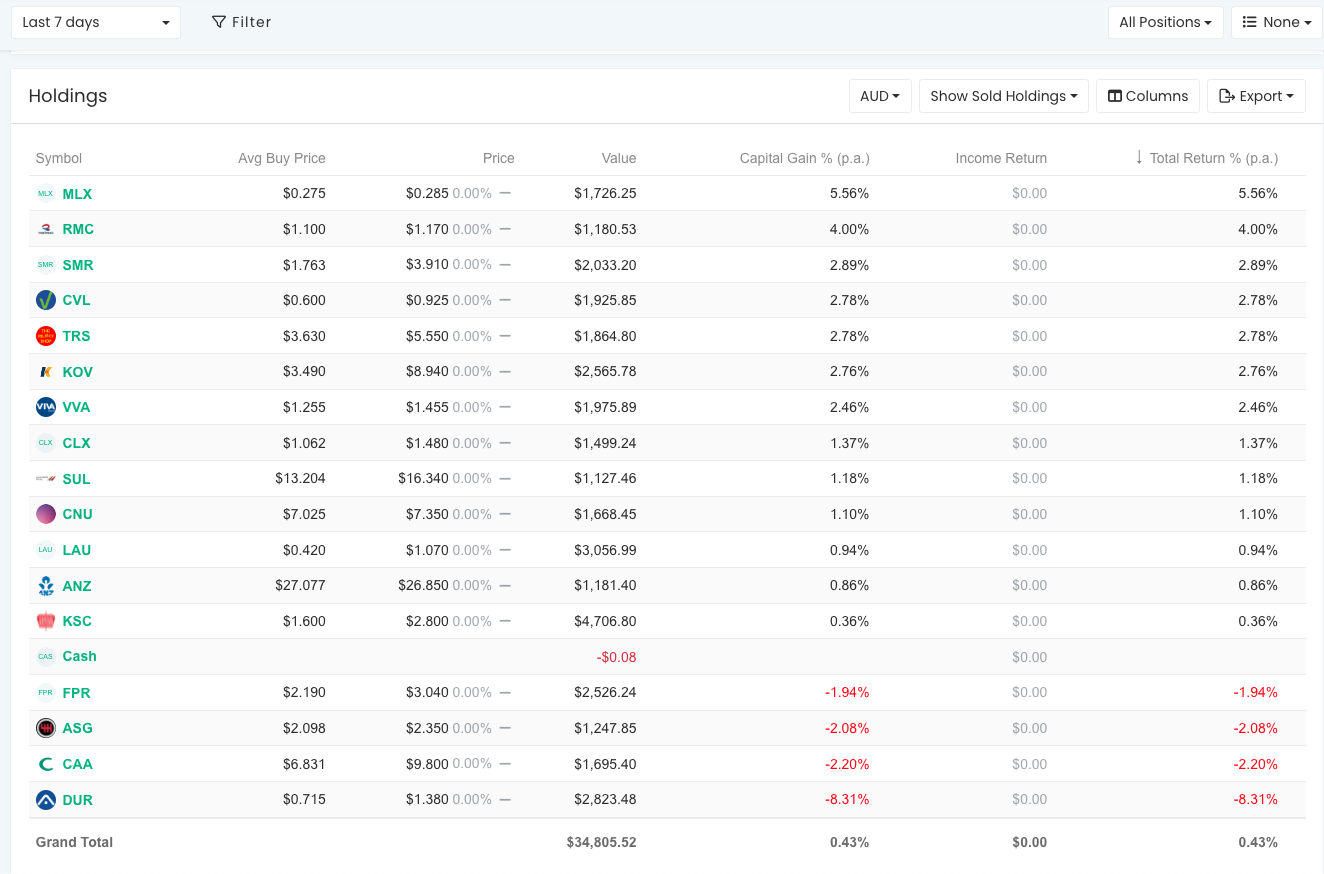

RECENT TRADES

No trades in the last week.

QAV STOCKOPEDIA DUMMY PORTFOLIO REPORTS

QAV AU DUMMY

It slid down in the last week and is slightly behind the benchmark, which is neutral for the last 30 days.

QAV US DUMMY

The US portfolio is up for the 30 day period but underperforming the benchmark. It’s sitting on a bit of cash which I’ll invest today.

FREE WEBINAR

I’ll be doing a free webinar on Tuesday, Feb 6, 8pm Brisbane time. It’s a chance for anyone to ask any questions you have about QAV (or anything else).

Zoom link: https://us02web.zoom.us/j/5799199150

STOCKS OF THE WEEK

During the last week, we also traded some stocks in our Light portfolios. Details here.

** As always, please check our work, DYOR, and consult a financial advisor before making any investing decisions.

BUY LIST

Each week we produce a buy list that we share with our members. The intended primary purpose of this buy list is for club members to use as a reference for comparing their own buy list. In theory, all of our buy lists should look pretty similar each week.

As always, please check our work, DYOR, consult a financial advisor before making any investing decisions.

THIS SECTION CONTAINS CONTENT WHICH IS VISIBLE TO QAV CLUB SUBSCRIBERS ONLY.

LAST WEEK’S EPISODE

Retail traders are suffering from fatigue; Lithium and tech stocks crashing; AI means the cost of intelligence will plummet.

Club edition also includes: Why TK keeps his mortgage facility open; Pulled pork on FND.

Episode Transcription

QAV 704 Club

[00:00:00] Cameron: Oh, welcome to QAV, TK! We’re recording this on Tuesday, the 23rd of January.

[00:00:19] Cameron: It’s episode 704. how was the barn boogling, Tony?

[00:00:24] Tony: Yeah, really good. Great fun. Uh, first couple of days were very windy, which made golf difficult, but You know, that’s part of golf. And then, um, third day was lovely. But yeah, the whole thing was just great. Good food, good golf, good place. We, um, we flew into Launceston and it’s about an hour and a quarter, hour and a half.

[00:00:45] Tony: North east of there, it’s on the coast, beautiful, beautiful scenery. Little town called Bridport, a fishing village nearby, and we went in there one night for, for dinner to a place called The Bunker, which I think is the um, the RSL club in town, and it was just really good food. I don’t drink, um, sometimes I feel like I wouldn’t be, wouldn’t mind

[00:01:07] Tony: having one, and they’re the kind of nights that, um, I wasn’t tempted, but you know, like it was good wine and good food and good setting.

[00:01:18] Tony: So it was lovely. But then, you know, the next day you get up and play golf and there’s a lot of sore heads and I’m just glad I didn’t drink. So that was

[00:01:24] Cameron: How long have you been off the booze now?

[00:01:27] Tony: Uh, 15 months at the end of this

[00:01:30] Cameron: Wow, well over a year. That’s impressive.

[00:01:33] Tony: Oh Yeah.

[00:01:34] Cameron: Ruddy with you and Tazzy?

[00:01:36] Tony: he wasn’t, no, it’s, this is a different group of

[00:01:38] Tony: friends, basically racing people from the Hunter

[00:01:42] Cameron: Taylor sent me a photo of Ruddy’s face this morning.

[00:01:47] Tony: know Taylor was in Wagga Wagga or Ruddy was in L. A.

[00:01:51] Cameron: He had a FaceTime where he got a photo from. Apparently, Ruddy had an accident over the weekend.

[00:01:58] Tony: really? I hadn’t heard.

[00:01:59] Cameron: He was mucking around with his nephews. I think he was on a BMX

[00:02:05] Cameron: and he tried to go over a jump and he stacked it and face planted. And he’s said, Taylor photo, his face is all covered in blood, you know, grazes on his upper lip and

[00:02:15] Cameron: everything. Taylor said, my dad did the exact same thing off my, on a scooter of mine, like 10, 11, 12 years ago.

[00:02:25] Tony: Oh, no. I’ll have to give him a call. Well, that’s Taylor’s fault because his nephews, um, I don’t know if they met Taylor or they heard of Taylor, but they’ve been bugging Ruddy for a long time to,

[00:02:39] Tony: like, make TikTok videos. And, um, and I don’t know how old his nephews are, I’m going to say they’re like 12, but, um, Ruddy’s been saying no, no, you’ve got to be 18

[00:02:50] Tony: to go on TikTok, so he’s been putting them off and putting them off.

[00:02:52] Tony: And they keep seeing Hunter’s stuff on TikTok and they’re going, he doesn’t look 18, what’s going

[00:02:57] Tony: on?

[00:02:57] Cameron: doesn’t look 18 really.

[00:02:59] Tony: Well, maybe a couple of years ago when he started.

[00:03:02] Cameron: He’s 23 now. So he was definitely 18 when he started. Um, right. Well, we don’t have a lot to talk about today, Tony, no questions today. And that sort of. Brings me to the first article for the day, which is from the ASX, Retail Traders are Retreating from the ASX. This is the AFR, not the ASX, the AFR, talking about the ASX.

[00:03:26] Cameron: This is Jonathan Shapiro, uh, came out yesterday. The army of day traders that stormed the Australian share market during the pandemic. Is showing signs of fatigue, but could mount a comeback in 2024 if the Reserve Bank starts cutting interest rates. Morgan Stanley’s equity strategists, who have closely tracked the activity of retail trading, said December’s data revealed a further decline in the share of market trading volumes accounted for retail traders.

[00:03:56] Cameron: Also known as day traders. By their numbers, retail traders accounted for less than 5 percent of total trading volumes down from the 8. 3 percent peak reached in February, 2021. That share is also down from 6. 2 percent last January. So that’s a pretty big drop from 8. 3 percent down to 5 percent over the course of the last, uh, what’s that, three years, I guess.

[00:04:20] Cameron: Um. And I was talking to Steven Mabb, Chairman of the Australian Shareholders Association and QAV club member yesterday, and uh, I mentioned that we’d seen a big drop off in QAV membership over the last year or two, year in particular as well. And he said they’ve seen a big drop off in ASA membership as well over the course of the last year.

[00:04:45] Cameron: But he said, you know, it tends to grow in bullish years. And then declines in volatile or down years.

[00:04:54] Cameron: The people who stay disciplined,

[00:04:57] Cameron: uh, succeed when those people come in, and they did, they, like, when they came in, they brought a ton of money into the market,

[00:05:05] Cameron: and, as we know, a lot of it wasn’t invested wisely, it went into shares like Appen, which we’ll talk about in a minute,

[00:05:14] Tony: ha.

[00:05:16] Cameron: And, uh, you know, they don’t have a discipline of trading through the upswings and the downswings, so they come in with fresh money, fresh blood, and we profit from that because we’re in the market already when they come in with all that money because we’re fully invested and we go through the upswing.

[00:05:35] Cameron: And then they all get scared when the market has a downturn, particularly, we’ve had a particularly bad downturn. And I was saying to him, like, you know, and the thing that gets me is we bang on on this show all the time about staying fully invested, staying disciplined, up market, down market, and our listeners know that.

[00:05:56] Cameron: It’s not like they don’t know because we go, we, we reiterate that point over and over. And I know that, you know, I get emails from some members of saying, you know, I got one from somebody this morning saying that he’s sort of basically cashed out a lot of his investment portfolio cause he’s buying a property and people lose jobs or they lose marriages or they move or, you know, there are lots of legitimate reasons why.

[00:06:21] Cameron: People have to, uh, you know, sell off their share portfolio and they’re no longer active investors because life takes them in different directions. But I’m sure there’s a percentage of people too that just suffer from fatigue. Capitulation, as you call it.

[00:06:39] Tony: Yeah, well, I think the other, the other dimension. Yeah, everything you said there I agree with and I think it’s true. There’s another dimension to all this and that is that during COVID times, the federal government allowed people to draw down from their super, um, as a way of, you know, staying afloat if they lost their job or whatever other hardships they had.

[00:07:02] Tony: And we know, anecdotally, that a lot of those people just took that money and because there wasn’t as much sport going on and they couldn’t bet on what they normally bet on, they took, they draw down from super and put it into Bitcoin, put it into the share market, sat on their couch and traded shares or coins or whatever they did.

[00:07:23] Tony: And you know, the other potential reason why they’ve left the market is because they lost all their money. Well, they lost a significant part of it. So I think that’s part of it too. The interesting stat though, out of all of that was I think you said that the share of now, the AFR calls them day traders or their source calls them day traders.

[00:07:43] Tony: I think we just got to clarify that terminology. They’re basically saying they’re retail investors. Day trading as a term means something else, which is basically people whose business it is to sit at a screen all day and open their account in the morning, put it in the market and close it down at night, um, and just trade per day rather than, um, over a longer timeframe like we do.

[00:08:06] Tony: Um, but retail investors, the small end of the market, um, it’s interesting, I think you said it was down by Uh, about 3%, so down from 8 to 5, but elsewhere in the article, it also says the share market, I think, or the money invested, or new money coming in, I forget now what the term was, is also down, so if retail investors are down as a percentage plus the overall number that their percentage of job is going down and it’s actually even worse than what those numbers look. But yeah, I mean, if fatigue, capitulation, you know, I had this conversation with a guy in Barnbergle. He was asking me how the podcast is going. I said, it’s all good. Our dummy portfolio is tracking along nicely at double market. It’s been going for four years. And I said, however, we have had lower subscriber numbers in the last 12 months.

[00:08:59] Tony: Um, And, you know, asking around in the industry, that’s pretty standard as the market comes off. Uh, that people, you know, stop, stop, either, either cancel their subscriptions or stop investing. And, you know, I said it’s just a classic. Retail investor who buys high and sells low and just chases the next, the next idea and it’s, or the next story.

[00:09:22] Tony: And as we’ve said, we, you don’t want to listen to stories and we’ll, and like, you know, Lionstown, the company that’s a lithium miner and Core Lithium, which has now shut its mine, um, You know, they’re doing terrible. But last year, all we could hear about was lithium stores and how good that was going to be and how Elon Musk had knocked on all these doors and wanted to sign up deals to take lifetimes amounts of, of lithium and nickel.

[00:09:47] Tony: And in the nickel markets almost shut as well now because, well, not shut, but the Australian mines are shutting down because Indonesia is flooding the market with. Um, with cheaper nickel and nickel prices way down. Something else which is you needed for the electrification thing that’s going on. So yeah, that’s, I mean, that’s a, that’s a point we make in on our coffee mugs.

[00:10:09] Tony: If you want to buy a story, go to a bookstore because there’s a lot more that goes on. than just the story. And yes, um, electric vehicles will be a thing. And yes, potentially there will be no more internal combustion engine vehicles one day. Um, but there are even now stories that I’m reading saying that lithium won’t be used in batteries for, uh, for electric vehicles going forward.

[00:10:33] Tony: That there’s a different way of storing energy, which is far more 20 minutes, um, using some other. Um, mineral besides lithium. So, you know, that’s just a factor of mining and of business in the mining business is that they go through booms and, and bus cycles and, you know, and it’s the old, uh, taxicab tipster or Uber driver tipster.

[00:10:55] Tony: When you get a tip from your, from your taxicab driver, you pretty much know it’s very, very late in

[00:11:01] Tony: the, in the cycle because just think of how many hands or how many years that

[00:11:05] Tony: tip has passed through before it gets to you sitting in the back of a, an Uber or a cab.

[00:11:12] Cameron: The Lionstown LionTown article in Chanticleer says, uh, Gina Rinehart’s lithium love affair faces Liontown test. Liontown is the poster child for lithium’s

[00:11:24] Cameron: price plunge and the news is getting worse.

[00:11:28] Cameron: So it says, Lyontown will need to drastically scale back its ambitions at Kathleen Valley. The 3 million tonne per year mine set to start production this year will go ahead, but the development work for the mine’s eventual 4 million tonne per year underground expansion will be put on ice.

[00:11:47] Cameron: And, uh, talks about Gina Reinhardt’s involvement in it, but it says, I like this, on October 15th. So that’s, what, three months ago? The company was sitting on a 6. 6 billion takeover offer from US lithium giant Albemarle. But Liontown sooner abandoned its bid the following day, and just 14 weeks down the track, Liontown is worth just 2.

[00:12:13] Cameron: 2 billion. The stock crashed another 21 percent on Monday to 94 cents. With hindsight, it would appear Albemarle’s decision to walk had much to do with the looming lithium price crash. But at the time, it was blamed largely on the intervention of Reinhardt, whose investment vehicle Hancock Prospecting spent 1.

[00:12:32] Cameron: 3 billion, or 3 a share, to build what was effectively a blocking stake in Liontown, one of several stakes in Lithium Critical Minerals Junior’s it took stakes in last year. So, uh, that’s a big drop.

[00:12:48] Tony: It’s a huge drop, and, um, it’s interesting, the whole Gina Reinhart dimension I think is interesting as well, because she stepped up because she thought the company was going to be taken over and taken overseas, and she wanted to block that. But she’s taking the sort of, but she’s also taking the sort of classic approach to this which a lot of retail investors don’t do.

[00:13:10] Tony: She’s not putting all her eggs in one basket, she is, um, she knows that the, you know, the mining industry can go boom and bust, so she’s, A, she’s diversifying away from iron ore, and B, she’s putting her eggs in a lot of different baskets, not just Linetown, so she can absorb. When one doesn’t go as well. I suspect that it might play out, um, depends on what her appetite is, that she’ll loan the money that the company needs to open, I think there’s a, um, a new development, a new mining tenement they’re trying to develop and that was one of the reasons for, um, getting Abimar Um, and the collapse in the share price yesterday, I believe, was because the banks refused to lend it the money to do the necessary development work because they didn’t see a future.

[00:13:58] Tony: at a lithium price, um, in the, in the medium term recovering. So, um, they’re left high and dry. Now whether Gina steps up and puts that money in, I don’t know, but that’s a possibility, so she could help in that way. But my point is that she didn’t just bet on one lithium company. She’s not just betting on lithium companies.

[00:14:16] Tony: She’s got a whole mining portfolio of investments. Um, and she knows to do that to ride out the storm, but a lot of retail investors will have one or two lithium companies in their, in their portfolio, and a whole heap of other companies outside of that sector in their portfolio, which is fine, but, um, it’s diversification as well, but if you’re going to play in a speculative space like that, it can work out really well.

[00:14:41] Tony: Uh, cause the, you know, in the early days you were buying lithium companies before they were having any sort of income and when they started to produce and sell and the lithium price went up, you did really, really well. And there’s plenty, been plenty of stories in the Fin Review this last 12 months about people who’ve made tens of millions of dollars, retail investors who put, you know, 80, 000 into a lithium mine as a stock investment.

[00:15:06] Tony: And it was speculative. And now they’re, they’re worth 50 or 60 million dollars. So that can happen. But you, you, unless you have some kind of detailed knowledge and you’re, and you’re a retail investor, you’re more,

[00:15:19] Tony: the more prudent thing to

[00:15:20] Tony: do is to just to make it a very small part of your portfolio. Um, but the even better thing to do is to focus on companies that make

[00:15:27] Tony: money and have existing proven business models and have quality business models, just as well.

[00:15:33] Tony: Mm

[00:15:35] Cameron: Yeah, I’m going back through our show notes over the last year or so about lithium. We’ve talked about lithium a lot. I think we flagged that it became a sell back in July,

[00:15:47] Cameron: which meant I think I got outta PLS

[00:15:50] Cameron: because of that.

[00:15:51] Tony: hmm.

[00:15:52] Cameron: But I was looking back earlier, about a year ago, 18th of January, we had a story.

[00:15:58] Cameron: Um, somebody had sent us a screenshot from Livewire. They were talking about the most tipped small caps for

[00:16:08] Cameron: 2023. One of them was Line Town Resources. Um, it was trading at, let me see, what was it trading at back then, LTR, it was trading at 1. 54 back then, then it went up to, I think it peaked at about 3. 15 in June, uh, it’s currently at 91 cents, so, it was, it did have a good year until September, and then the price caught up with it. Coal Lithium was another one. They were predicting, they were saying it was most tipped, CXO, CXO a year ago was trading at 1.

[00:16:54] Cameron: 11, it’s now trading at 0. 195, there

[00:17:01] Tony: Mm hmm.

[00:17:02] Cameron: was a few others on

[00:17:03] Tony: And, yeah, this reminds me of the GameStock saga when you, when you read out all the, uh, Wall Street investment funds who’d made a lot of money out of shorting GameStock even though they didn’t, um, they may have lost some on the way up. Um, this is classic. Wall Street behavior, right? It’s people getting into things late and then losing all their money on the way out.

[00:17:24] Tony: Um, and I imagine there were plenty of investment firms who were short, I don’t remember doing the pulled pork on call with you, man, that had a very high amount of, um, short, uh, short sellers in there on their registers. So, yeah, I mean, there are, yeah, I’m These things can hurt. If you’re buying a story, um, be very careful of buying at the peak.

[00:17:47] Tony: Um, just because someone made a lot of money on the way up and you didn’t.

[00:17:51] Tony: I know we’re banging on about this, Cam, but it’s so, it’s, it’s almost teaching the QAV story. by inverting it.

[00:17:59] Cameron: mm,

[00:18:00] Tony: we, I mean, I owned Pilbara Minerals at some stage last year, and as you said, the commodity was a three point sell, and I sold out of it.

[00:18:09] Tony: I can’t remember if I made money, or if I did, it wouldn’t have been that much, I don’t think. I think it paid a good dividend from memory at the time, because it was a lithium mine that was producing, and that’s why I liked it. Um, but I’m intact. The money I used to buy Pilbara is still there, invested in something else.

[00:18:29] Tony: I haven’t tried to write it all the way down. Um, so all the things that we talk about in QAV, about not following stories, about not following booms, about not listening to the fear of missing out, about finding companies that are at least making money, so you can look at the numbers and see how profitable they are, and you can decide whether they’re worth investing in or

[00:18:48] Tony: not, has all played out in this lithium boom.

[00:18:51] Tony: So it’s, it’s, it’s unfortunately, it’s the same

[00:18:53] Tony: story that keeps playing out time and time again. And it leads to the story you led off with,

[00:18:59] Tony: which was that retail investors get burnt and they leave the

[00:19:02] Tony: market.

[00:19:04] Cameron: yeah, I’m just looking at, uh, PLS for the light portfolios. Yeah, so, we owned it in, uh, a couple of light portfolios. I had it in my super portfolio as well, we had it in the dummy portfolio, bought them all around June or July, around about 4. 80 in June, up to 5, 5. 05 I think, the dummy portfolio, but then we got out when it became a sell.

[00:19:37] Cameron: When, uh, lithium became a sell, it’s now trading at 3. 30. So it’s fallen a long way from where we bought in. I’d hate to think, you know, where we would be if we kept holding it while lithium went down, but yeah, the commodity sell, it was a rule one sell for the dummy portfolio, my super, but for the lights, portfolios.

[00:19:59] Cameron: It was, um, we got out of the commodity sell, only lost 2 3 percent on it, because we got out so quickly when lithium became a sell.

[00:20:09] Tony: Yeah, right.

[00:20:10] Cameron: versus what we would have lost if we didn’t have the commodity sell giving us a tip off.

[00:20:16] Tony: I was going to say, of course, lithium hasn’t been the only boom in the last 12 months. And the Fin Review had another story today about it as well, um, about another company called Appen. Appen’s been around for a long time. I was just trying to look up, uh, what it did when it started.

[00:20:36] Tony: My memory of it is it was making circuit boards, um, for companies. So it was the, it was seen as being the picks and shovels, um, for any sort of tech, uh, you know, boom that was going on. And it’s had a real boom and bust. Lifecycle. And as these tech companies do they pivot and the thing that Appen pivoted into most recently was the provision of huge data sets to people like Google to hone their AI large language models and so another AI, I know the AI boom is dear to your heart, people piled into Appen because of the pivot into, uh, into providing large Data sets to Google, um, about 12 to 18 months ago.

[00:21:24] Tony: And of course, um, just recently, in the last day or so, Google’s walked away and said, No, we’ve got enough data now, thank you very much. And the app and share price has tanked as well. So, again, another story. I mean, I think, I think this is interesting, Cam. It’s, it’s, people need to fundamentally think about How they view the stock market and what its role is.

[00:21:45] Tony: It’ll always have a role to play in terms of speculation, uh, because, because, uh, a lot of companies who are on the, on the ASX or any stock market do so because they can’t take a business plan to the bank and get a loan for it, um, because it’s, um, it’s largely unproven or it’s, or it’s, um, It’s on a new sort of frontier, like AI or whatever, um, and so they rely on people to back them.

[00:22:10] Tony: And, and, and private equity does that, and venture capital does that, but again, they’re, they have a lot of experience at doing it, and they, they have very large portfolios of these investments, so their risk is reduced across any one company going broke, and it’s also reduced on the upside if they don’t, if they, if they only have one or two companies that do really well, then the portfolio gets the kind of average return.

[00:22:33] Tony: Like across the whole, the whole bandwidth. But, um, Unless you’ve got insider information or some kind of deep industry knowledge, it’s really hard as a retail investor to make money that way, to be speculative. Unless you’re a mining expert and understand the market and understand, you know, the life cycles of mines and all that kind of stuff, it’s hard to get in on at the right time.

[00:22:56] Tony: I mean, you know, I remember Geoff Wilson from Wilson Asset Management saying, 20 or 30 years ago, the best time to buy a mining stock is when it’s on its highest PE. You know, that’s when it’s cheapest. And that’s kind of ironic because, um, you know, it’s that way because it’s not making any money. So it’s the time when it’s least investable, but he often finds that’s the time to buy in because it’s the most speculative. The same goes for things like AI booms as well. I mean, yes, people have made money out of NVIDIA and investing in that, and the Mag 7 are doing well in the States. Um, but I don’t know how long that will go for as well, because it’s being, it’s being driven by the, by the FOMO, by fear of missing out now. Um, so it’ll probably all, all these things are priced to perfection.

[00:23:39] Tony: And, um, that’s not a great time to buy. So, I think in terms of what is this teaching us, it’s teaching us how we view the market and what we are. Are we speculative investors? Are we sort of trying to be quasi venture capitalists and actually do a better job than the pro venture capitalists? Or are we saying, no, no, there are a lot of, we’re investors and there are a lot of

[00:24:04] Tony: It’s quality, solid money making

[00:24:07] Tony: businesses out there, and all we have to do is find them and then decide if it’s the right price or

[00:24:11] Tony: not that we’re prepared to pay. And I think that’s the easiest thing to do

[00:24:16] Tony: in terms of, and the safest

[00:24:17] Tony: thing to do in terms of investing in the share

[00:24:19] Cameron: Hmm.

[00:24:20] Tony: Mm

[00:24:21] Cameron: Yeah, look, I do think AI is going to absolutely revolutionize life as we know it over the course of the next decade. But, who’s gonna win, if anyone is gonna win, that race? I don’t think anyone can know. I mean, I think the Mag 7 are a relatively safe bet. NVIDIA maybe not, because, you know, there are Plenty of opportunities for people to come along and build new chipsets to run this thing, run AI farms on, and everyone is getting into that now.

[00:25:01] Cameron: Microsoft are talking about it. Meta are talking about it. OpenAI are talking about building their own. China’s working on a bunch. And NVIDIA kind of Has a little bit of a monopoly on the GPU space for running AI farms at the moment, but that won’t be the case for much longer, I don’t think. The other guys, the other big tech companies are safe to an extent that it costs a lot of money right now to build.

[00:25:32] Cameron: a large language model that can perform at the level of ChatGPT 4. You’re talking hundreds of millions, up to billions of dollars to buy the GPUs and then to run them. Sam Altman, the CEO of OpenAI, has been banging on a lot about this recently. Like, we need way more power generation on the planet to run these things.

[00:25:58] Tony: Yeah,

[00:25:58] Cameron: But

[00:25:59] Tony: Ha ha.

[00:26:00] Cameron: The flip side to that argument is, what he and others are also saying, is, we’re very early on in the AI revolution right now, we still really don’t understand how it works. Even Ilya Sutskever, the guy who, until the failed coup, 6 weeks ago, was the Chief, um, research officer at OpenAI and, uh, was the, one of the masterminds behind ChatGPT.

[00:26:29] Cameron: You know, even I, I watched interviews with him late last year. It was like, the thing is we don’t know how it works. We, you know, we had a sense a couple of years ago that if you threw more. compute at this thing and scaled it up. It could probably do some amazing things. So they just started throwing thousands and thousands of GPUs at it.

[00:26:52] Cameron: And all of a sudden it developed some form of emergent intelligence. And like, we don’t know why. We don’t know why it is doing that, but it is. But here’s the thing is that everyone that I pay attention to this space, which is those guys and Kurzweil and Wolfram and, uh, you know, Musk and all of these guys, Gates, that are thinking deeply about it.

[00:27:16] Cameron: Is that we will figure it out at some point. And when we figure out how it’s doing, what it’s doing, we will probably realize that the models don’t need to be as big as they are. You know, we’ve, we’ve just like thrown a whole bunch of shit at a wall and eventually we’ll work out, Oh, it’s just this bit here where the magic happens.

[00:27:39] Cameron: We can get rid of all of that. And when that happens, you won’t need. 50, 000 GPUs to run a large language model. You’ll be able to do it on much less compute, which makes it more accessible to more businesses and more companies. And you don’t necessarily need to have the wherewithal to throw, you know, 10 billion at it to, uh, scale it up.

[00:28:01] Cameron: So, anyway, I guess my point is just that it’s very early days and we really don’t know how it’s going to play out over the next few years and, you know, everyone thinks Microsoft’s got this massive moat now because of its stake in OpenAI and it doesn’t actually control OpenAI as a lot of people seem to think, it just has, uh, a deal where it gets like 51 percent of the profits that it generates in the short term, but, um, You know, that doesn’t necessarily mean anything.

[00:28:31] Cameron: OpenAI could, I keep saying, could be the Netscape of the browser wars, you know? Netscape for a few years there back in the mid 90s looked like they were going to rule the world and very quickly they tumbled and fell and disappeared and became a division of Oracle, I think, at some point. You know, after Microsoft crushed them.

[00:28:53] Cameron: I was part of that.

[00:28:54] Tony: Yeah.

[00:28:54] Tony: and that’s, so let me ask you the question. You have a lot more

[00:28:57] Tony: knowledge on the AI space than I have. Um, where would, if you had, first of all, do you feel compelled to invest in it? And secondly, where would you if you did feel

[00:29:08] Cameron: Um, no and no. I wouldn’t. No, absolutely. Like, to me, it is like Bitcoin. Like, it’s probably going to be something, but how it’s going to

[00:29:18] Cameron: play out and who’s going to be on top when it

[00:29:20] Cameron: does, I don’t think anybody knows. And I think you’re fooling yourself if you think you do know. So, why would I invest in something where I have no idea how it’s going to play out?

[00:29:30] Cameron: Now, with that said If I’m right, an AI is going to be as revolutionary as I think it is going to be over the next 10 years. It probably has massive consequences for the global capitalist economy as a whole. So, our traditional ways of assessing the future of any business, uh, is up in the air as well. You know, Sam’s got this great Simon, I was reading a bunch of his recent quotes this morning, actually, and the thing that he says that I think people all need to think about is he says the people that most, the thing that most people don’t get about what’s happening right now is about the cost, he calls it the cost of cognition.

[00:30:13] Cameron: I tend to refer to it as the cost of intelligence. The cost of intelligence is about to drop through the floor. So we’re used to being in a world where if you want to Develop an intelligence. You need to take a human, you need to raise them, give them primary education, secondary education, tertiary education.

[00:30:37] Cameron: Then they need to go and devote themselves with a passion and a focus to a particular domain for decades to become really, really good at it. And then you’ve got an intelligence, somebody that’s really intelligent on medicine or biology or investing or whatever it is. And those people have limited time, limited energy that they can devote to any particular exercise.

[00:31:05] Cameron: If you want to hire them and they hire a bull. Not doing their own thing. It costs you a lot of money because there’s a lot of competition for them because they’re an expert in this particular domain and then they’re going to die one day and all of that’s gone. That expertise, they might’ve written some books or whatever, but somebody then needs to read those books and spend 40 years developing an intelligence.

[00:31:29] Cameron: What’s about to happen is the cost of intelligence is going to become near zero. Like the cost of communications did over the last 20 years. You remember the days when you used to ring somebody interstate and it would cost you 2 a minute, or internationally,

[00:31:44] Tony: Oh, yeah. And dad’d be, dad’d be like in the background saying, come on, that’s

[00:31:49] Cameron: Yeah, well,

[00:31:50] Tony: It’s costing me a

[00:31:51] Tony: fortune.

[00:31:51] Cameron: her mum who has Alzheimer’s in Arizona, and she still says, well, this must be costing you a fortune. Um, you know, if you had said to somebody, imagine going back to 1990,

[00:32:04] Cameron: And saying, you know what, by

[00:32:07] Cameron: 2010,

[00:32:09] Cameron: you’ll be able to speak to anybody, anywhere in the world, for as long as you like, full video, and

[00:32:15] Cameron: it won’t cost you anything.

[00:32:18] Cameron: It’s basically free, because you’re paying for basic internet access. What’s that? Don’t worry about it, you’ll find out. You’re paying for it, like, 50 bucks a month somewhere else, and it’s all just bundled in, and you can talk to anyone for any length of time. People would have been like, nah, that’s not That’s not going to happen, but the cost of telecommunications dropped to near zero, right?

[00:32:43] Cameron: That’s what’s about to happen with intelligence in the next 10 years. As Sam says, imagine that anybody can have 10, 000 experts on hundreds of different domains, working on a problem or a business for them for next to zero dollars. What are the implications of that? to society, when we all have thousands of highly intelligent minds available to us, and not just in the Western world, but in Africa and developing countries and Asia and everywhere in the world, where everyone can tap into this.

[00:33:19] Cameron: Like, we’ve never gone through a revolution like this before. That’s gonna happen at this speed, with this low barrier to entry. It’s gonna be, uh, fundamentally, if it plays out like I think it will, it could all come to a crashing halt for a variety of reasons. But if it plays out like it is gonna play out, it’s gonna be, it’s gonna have far reaching impacts on the economy in general.

[00:33:49] Cameron: And, um,

[00:33:50] Tony: yeah, look, look, I agree with you. However, I think there’s a couple of guidelines that I can draw on, and that kind of, that kind of speech, I think I heard a lot in the dot com boom, right, because we have gone through a generational cost of intelligence quantum shift, it happened in 2000, when you could type into Google, tell me about or Define, or Help Me Do, etc, etc, whatever it was, and get access to a lot of information very, very quickly.

[00:34:23] Tony: And that led to huge productivity gains, and that’s probably been the only thing that’s been driving productivity gains in the last 20 or 30 years in most Western economies. It’s been the digitization of knowledge and how it’s used. And I think, so, I agree with you, once you get access to ChatGPT on steroids or whatever it’s going to look like, that’ll go through it again.

[00:34:44] Tony: But I think there’s a couple of Caveats I’ll put on that. I actually think the big money will go to the person who produces the GUI interfaces for AI. And I think the, you know, you’d hope there’s somebody out there right now who’s

[00:34:59] Tony: thinking that if I, what if I have this kind of, you know, floating genie screen and if I have a, An emotional problem, right?

[00:35:09] Tony: If my boyfriend dumps me or my girlfriend dumps me, I can go and talk to the big blue genie and they can give me really, really good advice.

[00:35:16] Cameron: will it talk to you in Robin Williams voice and then do a song and a dance?

[00:35:20] Tony: yeah, it could be, but that, but that could be the winner out of AI, right? Because regardless of how. Well, you and I use AI. The vast population out there couldn’t give a shit about intelligence.

[00:35:34] Tony: That’s the problem with the human race camp. Like I was going for my walk today and I saw any number of young women with their bare midriffs and their six packs and I thought, I thought, that’s what you’ve optimized your life for. You know,

[00:35:51] Cameron: you complaining about

[00:35:52] Tony: evolutionary. I’m not complaining about it, but, but tell me, tell me what they’re going to ask AI

[00:35:59] Tony: about, or how superintelligence is going to help their life, except for perhaps in getting better supplements

[00:36:05] Tony: and, and better exercise routines. So it’s the, it’s the, the person who provides the GUI interface for people who don’t think they need AI, but do

[00:36:14] Tony: need answers, is going to probably kill

[00:36:16] Cameron: Well, it’ll

[00:36:17] Tony: But it’ll be something left field

[00:36:18] Cameron: it’ll be built into all of our devices within the next couple of years. It’ll be built into your phone. It’ll be built into your watch. It’ll be built into your glasses. It’ll be built into everything. Um, but I think the, the analogy that you made with

[00:36:34] Cameron: the internet is the closest thing that we have.

[00:36:36] Cameron: But the difference. As I think of it, is the internet gave us access to information. It democratized and reduced to near zero access to information. You didn’t need to go by the Encyclopedia Britannica if you wanted to learn something. You know, first of all, it was Encarta on a CD ROM. And then it went from Encarta to Wikipedia and the internet.

[00:36:58] Cameron: And I, I lived through, you know, that. I was at Microsoft for some of those years and You know, I’ve probably, I don’t know if we’ve talked about this story on this show before, but I’ve talked about it somewhere before.

[00:37:09] Cameron: You know, the story of Encarta is fascinating. Um, it’s in a Microsoft history book somewhere that I remember reading.

[00:37:16] Cameron: Like Microsoft went to Encyclopedia Britannica, first of all, in the early nineties and said, we’re coming out with this computer called, this operating systems can be called Windows 95. The computers are going to be shipped with CD ROMs. We want to work with you to put Encyclopædia Britannica on a CD ROM.

[00:37:33] Cameron: And they were like, why would we ever do that? We sell these things for 2, 000, we’ve been doing it for a hundred years, we own the world, screw you and the horse you rode in on, we’re not going to do it. So Gates went, okay. Fine, I get it. And then he went back and said, we’ll build our own and they built Encarta and Britannica basically went out of business within five years.

[00:37:58] Cameron: Um, scaled down their business, you know, but yeah, they just, no, no, no one was buying Encyclopedia Britannica anymore when you could get Encarta for 29. 95 on a CD ROM. And then Encarta disappeared when, uh, Wikipedia and the internet came along, but the internet gave us access to information. AI is going to give us access to intelligence which is a step factor above that.

[00:38:25] Cameron: I don’t need to read something and learn it now because the AI will know it. I’ll just say do this, figure out that problem for me, solve cancer. And you’ve gotten to lunchtime, because I’ve got something else for you to do after lunchtime. Anyway, people can listen to my Futuristic Show if they want to hear us talk more about that.

[00:38:48] Cameron: How’s the property sale of the Sky Palace going, Tony?

[00:38:53] Tony: Oh, early days. We got our first inspections tomorrow.

[00:38:56] Cameron: Right.

[00:38:57] Tony: Yeah. Yeah. And, uh, but, but just been busy. It’s on the market. It was listed last weekend. Um, all the photography was done on Friday while I was away. Um, been a heck of a lot of work of moving our furniture out into storage and. and staged furniture in so everything’s themed and low

[00:39:17] Tony: profile to highlight the views and all that kind of stuff.

[00:39:21] Tony: Um, and there were, I think there was something like 50 email inquiries to the estate agent on the weekend asking about the property and a couple of inspections scheduled for tomorrow. So yeah. We’ll see. Fingers crossed. It’s rolling along.

[00:39:34] Cameron: And I was talking to somebody yesterday, and the subject of your move

[00:39:39] Cameron: came up, and they said, why does Tony still have a

[00:39:41] Cameron: mortgage? He’s surely eager to afford to pay off his mortgage, why does he still have

[00:39:46] Cameron: a mortgage? And I gave them my answer, but I thought I’d throw it out to you and let you answer for yourself.

[00:39:54] Tony: Yeah, sure. A couple of reasons. It’s, um, just like a business, it’s good to have some gearing. So, um, I’ve been good at investing in the stock market over the years, so it’s, um, it’s useful to gear. And, um, so there’s that, uh, it’s, um, we’ve talked about this before about, you know, my, I think my secret sauce over the years, apart from the QAV system has been to buy a property, gear it up, um, pay it down, then re gear and put the money into the share market.

[00:40:29] Tony: So you’ve got, you know, more money. Um, earning for you and then let the dividends pay off the mortgage and then rinse and repeat as the properties increase in value, sell them, start again, take out a mortgage. So it’s a bit of a leftover from that. Um, I’ve always adopted the same. Rule of thumb that I use for companies and that’s a gearing level of no more than 50 percent.

[00:40:54] Tony: Uh, you know, ours is much less than that now. It’s probably 25 or 30 percent, um, of the, of the property value because, um, things can go wrong and you don’t want to be forced, a forced seller. So, but you want to have more exposure to things that work for you. So it’s kind of that fine, for me, the fine balance between that, the efficient.

[00:41:14] Tony: The efficient frontier, as economists call it, is, um, is around the 30 percent gearing rate. And then the third reason I do it is, um, as, uh, uh, someone pointed out to me many years ago, it’s actually a form of asset protection. It’s, um, less relevant now at this stage in our life, but if someone ever does take a legal action against, um, GENI for being on a, a director on a company or me through some of the smaller companies I’ve run.

[00:41:40] Tony: Over the years, um, and you’ve got a mortgage on your house, then it’s, it’s a little bit more difficult for them to take that asset away from you. They’ve got to take it away from the bank. So, um, there’s that too. So there’s a, um, and you know, that argument, take it to extreme,

[00:41:57] Tony: says you should have the mortgage at 100 percent of the

[00:42:00] Tony: asset value all the time Um, so I haven’t done

[00:42:05] Tony: that because I don’t want to take the risk, but that, that

[00:42:07] Tony: was the, that is the best asset

[00:42:09] Tony: protection. So for those three reasons, that’s

[00:42:11] Tony: why I have a mortgage.

[00:42:12] Cameron: And at this stage of your life Now that you don’t have an income, you haven’t had an income outside of dividends for a long time and Jenny has semi retired, apart from the boards, she doesn’t really have an income. If you did need to go and get a debt facility for some reason, how do you think you’d go?

[00:42:33] Cameron: Uh, yeah.

[00:42:37] Tony: Yeah, so Jenny and I have been talking about this. We have most, our mortgage is broken into two. So, and the smaller part of it is an interest only. Overdraft type facility, which is how, which is the kind of mortgage I recommend for people who are drawing down to invest in shares because, you know, the dividends get paid twice a year and you can, you can let the, the principal, um, and we can let the interest accumulate until those dividends come in and then pay it down in one hit.

[00:43:07] Tony: Um, so that’s the best, the best type of loan, but the bank wouldn’t give us a hundred percent. of that kind of loan because we came back to Australia posthang, um, so we couldn’t get 100%. Um, so we do have a P& I with an offset account, but, um, yeah, I’d, I’d struggle to get either of those. So we will probably keep the interest only portion of our mortgage going forward just to act as an overdraft for us, um, and give us a buffer.

[00:43:31] Tony: Uh, if I had to, I would probably have to go to a mortgage broker and take out a loan from a non traditional provider at a higher rate than what the banks are, the major banks are offering. And we spoke about a company that I think in the last book called Resimac who specializes in doing those kinds of loans for people.

[00:43:48] Tony: So that’s where I’d go. I’d go to a

[00:43:50] Tony: mortgage broker.

[00:43:51] Cameron: Yeah, because I guess on paper a bank would look at you and

[00:43:54] Cameron: say, well You, uh, don’t have

[00:43:58] Cameron: a normal job. You

[00:43:59] Cameron: don’t have an income. It’s your income is based on shares and no one knows what’s going on with shares. And, uh,

[00:44:08] Cameron: and you probably don’t carry a lot of credit card debt that they’re making money off of over from month to month.

[00:44:14] Cameron: So not really a good proposition for them. Right.

[00:44:18] Tony: no, correct. Yeah. So that’s, that is something to be aware of if you’re going into retirement phase like we are.

[00:44:23] Cameron: Speaking of Resimac, um. A week ago, uh, it was trading at 1. 10. It’s now trading at 1. 14. So, uh,

[00:44:34] Cameron: looking at how it, how it did.

[00:44:35] Cameron: It’s had a good run.

[00:44:38] Tony: Sense the pulled pork. Yeah, good.

[00:44:40] Cameron: Speaking of pulled porks, Tony, do you have one for us today?

[00:44:44] Tony: I do. And, um, I guess before I get into it, I’d just like to say if people didn’t like that last talk about AI and boom and bust companies, um, send us some questions next week. Hand some requests for pulled

[00:44:58] Cameron: Shut us up. Yeah.

[00:45:00] Tony: Yeah, because I was going down our buy list, and I think I’ve done a pulled pork on almost every company.

[00:45:06] Tony: Um, at some stage, so I might have to start going back and redoing them, but I did find one today I hadn’t touched before, nor did I know much about, and it’s called FINDI, F I N D I. And it’s a, it’s a FinTech payments and ATM provider. And I think the really interesting thing is it’s based in India. So we have a company on the ASX, but its operations are based in India.

[00:45:30] Tony: And I think that’s historical. I think the original founders may have been Australian. Um, and again, this is another kind of company that’s been through a few pivots over the years as well. Um, but that’s what they currently do. And they have a network of 6, 000 merchants and 21, 000 ATMs in India. And just to put that in perspective, they’re, they have 21, 000 ATMs in India, and they’re not. I guess by any stretch of the imagination, the biggest player, but, um, there are 26, 000 ATMs in Australia, so, you know, Indy is such a big place that a small company like Findy can have a, a meaningful market share or a meaningful presence as a business, um, almost the same sort of Presence is the whole banking system in Australia in terms of ATMs, um, but they’re still a small company.

[00:46:20] Tony: They employ, um, a bit over 650 employees, and they’re also applying to become a full digital payment bank in India. And I think that’s interesting as well. So, India has banks, retail banks like we have here. Um, but it’s, you’d have to say from what I’ve read anyway, the country’s reasonably underbanked and is still largely a cash economy.

[00:46:43] Tony: So, you know, going back to that discussion we just had, it’s pretty hard if your, if your job is riding a delivery cycle. Or something in the, in the out, out back of one of the smaller provinces in India to go to the bank and apply for a loan and, and get money to build your business, um, or to, um, even to, to build a house.

[00:47:06] Tony: So it’s, it’s an underbanked economy, a cash economy. But there’s also been a fair bit of leapfrogging of, of the way banks have evolved in Australia. A lot of banking in countries like India has done phone to phone. It’s a digital environment, and so, uh, you know, I kind of think that Findi’s tapping into this, and, um, the fact that they’re applying for a digital payments banking license, which is only a new thing in India, is, is, you know, quite possibly a good thing for them.

[00:47:37] Tony: Uh, The shares are up in the last 12 months, and they’re up 80%. And that’s largely on the basis of their, their rollout of, um, of ATMs and, and in particular, FPOS merchants. And I think the interesting business model, um, they, when they go out to a small merchant and do a deal to provide their FPOS terminal, they also go usually, well, they often go one step further and they rebrand the merchant as a Findi Payment Center.

[00:48:07] Tony: Um, again, because people are. used to being able to go to a particular location and top up their mobile phone or pay a bill or deposit cash or all those kinds of things. And if you go to the Findi website, you’ll see what I mean. So if you think about what might be, um, in Australian terms, a very small daggy corner store milk bar in the suburbs, that’s just sort of standard.

[00:48:32] Tony: Shop in a lot of these towns in India and, um, and if they sign up with Findi, they get a full sort of shop refit and rebrand and, you know, um, paint and, uh, internal fit out and better counters, better, yeah, display product better. And then they get a big sign above the door saying it’s a Findi payment center.

[00:48:51] Tony: So, um, that could be behind why they’re picking up so many merchants and they’ve actually increased their retail merchants by 90 percent in the last six months. So. They seem to be doing well in this space. Uh, what else can I say about them? They don’t just offer FPOS and ATMs, they offer bill payment services, credit card payments, these are all on the phone, domestic money transfers, some overseas transfers like India and Nepal, and they’re a cash drop merchant and prepaid recharges.

[00:49:25] Tony: So they’re sort of filling out what would look like a digital bank. And, uh, and the license will certainly help if they get that to do that. Uh, going, looking at the numbers now, um, you can see if people have access to the bread loader, they can see it’s a buy, but it’s a, it’s a pretty tough graph to see what’s happened in the last year or so, because it’s had a, um, over the last five years, the share prices dropped from a high of 80 down to a low of a dollar.

[00:49:56] Tony: And so it’s a huge, huge spike in the months, sort of four and five of the five year graph. Sorry, years four and five of the five year graph. And it’s down to almost a flat line if you look at it in those terms. But if you do have access to a, like a Stock Doctor graph or perhaps Yahoo Finance, you’ll see that if you do it over a three year time period, that it’s, it’s, um, it’s easier to see it as a buy.

[00:50:18] Tony: So it’s, um, it’s still gone down a little bit.

[00:50:29] Tony: ADT for this stock is 126, 000, so it’s reasonably small, but will suit a lot of listeners. I’m doing my numbers based on the price of 0. 98, which was the price on the weekend, but I did notice it jumped again yesterday to 1. 10, so my numbers are going to be a little bit out. Perhaps not by too much. And given it’s, this is the number three stock on the buy list, even if I’m out by a little bit, it’s not going to make a big difference to the QAV score.

[00:50:57] Tony: A couple of things to note. There’s no consensus target for this company, which I think is a good thing. I’ve actually set up a trial portfolio on companies which have no consensus target to see if they do outperform our normal, our normal buy list. But I think it’s a good thing because we’re not, we’re not attracting institutional money.

[00:51:16] Tony: Um, to this company, no one’s, uh, of note is researching it and therefore we have a chance to, um, to, to be first in. Um, Stock Doctor do have a, uh, uh, financial health, uh, a financial health measure for it. I’m just trying to find it now. It’s, it’s, uh, it’s solid and recovering. Um, but the interesting thing in the, in the Stock Doctor numbers is that they have free cash flow per share as a negative number.

[00:51:43] Tony: And we have. Um, a very good PropCaf for this, for this company, um, which is positive, obviously. So something’s, something, if I see this kind of disparity between free cash flow and operating cash flow, the money has to have gone somewhere and it usually goes in CapEx. So if anyone wants to look at the, the cash flow statements for this company, they’ll see that, uh, operating cash flow has been increasing recently.

[00:52:10] Tony: And this, this latest half is 25 million. But the. Investing cash flow is negative by 49 million and they’ve recently raised 20 million, they now have 20 million of debt on the books and they also did the share issue for 5 million, so this company is very much in growth mode. I didn’t go into research what the CapEx was used for but I’d be very surprised if it wasn’t used for either buying ATMs and FPOS devices or it was used for rebranding these stores to grow merchants.

[00:52:44] Tony: But clearly they’re funding the growth of the business, partly through cash flow and partly through debt. Which is not a bad thing but I just want to call out the difference between free cash flow and operating cash flow. Uh, no dividend yield as expected in the growth stock, um, yeah, Stock Doctor Financial Health is strong and recovering.

[00:53:06] Tony: Directors hold approximately 12 percent of this company, so that’s good, but I, just looking at them, I don’t think they are the founders for this company. Like, again, I don’t think that’s a bad thing because this company has been through a number of iterations and pivots. And the directors who do own a large chunk of this company are basically investment bankers.

[00:53:30] Tony: And so this is a bit like the one we had last week, where we don’t have a founder, but we have a very experienced investment banker with a large stake in the company. And I think even though it doesn’t You wouldn’t think it scores there for as being an underfounder. I think it deserves a score for having someone with vast experience and skin in the game that we can invest beside.

[00:53:53] Tony: One of those directors I’ll call out is a guy called Nicholas Medley, who’s an investment banker from Australia, and it’s only of note to me because he’s the son of Peter Smedley, who’s an Ex Shell CEO that I used to work for. He was, um, he was very sharp. So if the Apple

[00:54:12] Tony: ROE for the company 17%, PE is 10. 3 percent which is The lowest in three years. But that’s only really because there’s only been two halves where the company has had a positive PE and, and been profitable. So, um, uh, even though, we’ll, we’ll score it for that, it, it’s, um, it’s a little bit meaningless. Uh, prop cap for this company is 1.44 times, which is very, very low.

[00:54:36] Tony: And as I said before, they, they do have to take on debt to get, um, to get the CapEx bill paid. So just be aware of that. But prop calf is, you know, price to operate in cash flow is very low. Um. IV1 for this company is 0. 48, and there’s no IV2, so we’re not buying it below that price, so we can’t score it. Uh, same with Net Equity Per Share, so, um, we can’t buy it for book, which is 0.

[00:55:00] Tony: 64, or book plus 0. 30, which is 0. 83. Uh, has been increasing, but not consistently over the last three years. So it’s been increasing in the last year or two, but not for the full six halves. So we can’t score it for that. But all in all, this company gets 100 percent quality score. So the things we can score it for gets 11 out of 11.

[00:55:22] Tony: And that’s because some of these, um, rated two. And it gets a QAV score of 0. 69, which is number three on our buy list. So that’s, that’s a really good score. Um, the interesting thing, I guess, is that we have a fintech growth company on the value investing buy list, so that’s, um, an unusual thing to see, but it’s happening now.

[00:55:43] Tony: And I did actually wonder if that was the case, one, because Findi, um, obviously burnt a lot of people in dropping from an 80 share price to a 1 share price, and so it’s being ignored. By a lot of, um, of institutional investors, but I also wondered whether, um, being a fintech payment company, whether, you know, that just wasn’t flavor of the month in terms of, um, the style of investment of internet companies that people are investing now, which tend to have an AI type flavor to them.

[00:56:12] Tony: Plenty of risks in a small company like this, not, you know, not the least of which is the fact that it’s on the ASX, but it’s operating in India. So it’s not like we can. Go for a walk and see how the Fendi stores are doing and whether they’re being populated with customers or not. We can’t do that easily.

[00:56:28] Tony: But I think there are real risks that there could be further capital raisings or increased in debt. I don’t know at what stage they are in terms of their growth into the ATM market or the merchant market or whether they’ll need. Um, increase capital investment if they get their digital banking license.

[00:56:45] Tony: But a lot of these companies, you’ve just got to go into them knowing you’ll probably have to put more in later. Um, there’s a risk, of course, that they don’t get the banking licenses that they want or require and that they, their growth could be therefore. Curtailed because of that. Uh, and the last risk I’ll highlight is that if the company is successful, it does invite bigger banks to muscle in.

[00:57:05] Tony: So that could be good if they, if they try to take over Findi and there’s a, um, a takeover premium, or it could be bad if they just sort of, um, muscle in and make it very, very difficult for a small company to compete. Um, they’re the, they’re the risks on the positive side of things. A lot of people are saying India is the new China.

[00:57:23] Tony: So, as China gets more and more of a middle class, India sort of, which is about, I’m going to say, a similar population size, and I know there are probably hundreds of millions of people different, but it’s still a very large population, and, um They’re still early days in terms of their expansion of the middle class, back where China was when it was starting out to do that.

[00:57:45] Tony: Um, the need for banking services is huge and there’s a strong demand for mobile banking. So they’re kind of bypassing

[00:57:53] Tony: the idea of having branches everywhere and people using laptops to do banking or across the Canada to do banking. So, yeah, interesting company. Have a look, do your own research. It’s a growth company, it will have growth company risks, but at the moment it’s good buying.

[00:58:10] Cameron: And what happened in 2020

[00:58:13] Cameron: and like March 2021, where it’s sort of the share price

[00:58:17] Cameron: plummeted, as you say, um, interestingly, like if

[00:58:21] Cameron: I look at it, the bread later,

[00:58:23] Cameron: you can see that big plummet from 80, 90 really in August, 2020. Down to where it is today. But if you look at, uh, Stock Doctor, even over five years, it’s adjusted the pricing.

[00:58:40] Cameron: Like if you go back to August, 2021, it has the share price at 4. 42, not 90. So some sort of a consolidation, it suggests, but I’m going back

[00:58:53] Tony: I’m not familiar.

[00:58:54] Cameron: I’m going back through their announcements in Stock Doctor around about that time. I can’t see anything about a consolidation. There was a return of capital, but, um, I can’t really, uh,

[00:59:08] Cameron: figure out why that. Uh, would cause the share price to be adjusted to that degree. They returned, um, that 20 million of capital to shareholders. Um, part of these a dividend and partly as just a capital, uh, return. So.

[00:59:29] Tony: Shame they did that because they borrowed 20 million dollars in the last year or so so they could have used it.

[00:59:34] Cameron: Well,

[00:59:34] Tony: Yeah, but I, I mean, this company’s pivoted and pivoted and pivoted. I think it’s now sort of, you could almost say it’s emerging from the ashes of Findi, the way it used to be. Even on Stock Doctor, it’s referred to as a, almost like a venture capital fund where they co invest with, um, with entrepreneurs.

[00:59:50] Tony: Um, then it plays down the banking side, but if you go to the Findi website, it’s all about the digital banking side of things, which is its current business. So, it’s obviously had a number of iterations and some of them probably weren’t

[01:00:01] Tony: successful. And, um, this guy Nicholas Medley, um, who, uh, you know, by all accounts is a sharp bloke, has spotted a niche and, um, is now using Findi to fund his expansion into

[01:00:15] Cameron: hmm. Um, interestingly, April 2021, Borders received further notices

[01:00:24] Cameron: seeking to remove recently appointed Independent Non Executive Chairman Nicholas Smedley.

[01:00:30] Cameron: urges shareholders to vote against all resolutions of the general meeting to be held on the 19th of April 2021. Company now forced a considerable cost of convening a further general meeting of shareholders due to wasteful ongoing actions by requisitioning shareholder.

[01:00:47] Cameron: So there was some sort of hostile action on them.

[01:00:50] Tony: I’m sure.

[01:00:53] Cameron: so

[01:00:53] Tony: Yeah, I’m sure there’s an interesting, interesting book in the history of a company like this. Would have chopped and changed them being lots of drama, I

[01:00:59] Tony: would have thought,

[01:01:00] Cameron: Hmm, hmm,

[01:01:02] Tony: Speaking of books, I read in the paper today that Joe Astin is writing a book on

[01:01:05] Tony: Qantas.

[01:01:06] Cameron: oh right,

[01:01:09] Tony: Yeah, it’s called The Chairman’s Lounge, which will be very

[01:01:11] Cameron: wonder if that was, uh, why he left the Fin.

[01:01:16] Tony: possibly.

[01:01:17] Cameron: That should be a good read. The Chairman’s Lounge, hahahaha, good for him, that’ll be great. Well thank you for that on Findy Tony,

[01:01:29] Cameron: uh, well. all I’ve got for the show today, Tony. After hours, what have you got for us?

[01:01:38] Tony: Well, we spoke about Barn Bugle, but, um, speaking of good books, I’m about halfway through Going Infinite, Michael Lewis’s book on Sam Bankman Freed, and,

[01:01:51] Cameron: I said, Oh God, Sam Bankman Freed. Wow.

[01:01:55] Tony: like, I haven’t been able to put it down. It’s, it’s one of the best things. I mean, I’m a huge Michael Lewis fan since I read, you know, Lies Poker back in the mid 80s, um, and Moneyball and all the other ones, these really good ones he’s written.

[01:02:10] Tony: I hardly recommend any of them to people. This one’s terrific. And I haven’t even, like I’ve written, I’ve read probably 120 to 150 pages and it hasn’t even gotten to Bitcoin. And the really interesting things are all about, uh. You know, how Bankman Free got to be recruited into a Wall Street fund.

[01:02:29] Tony: Effective altruism, if you’ve heard about that, and how that all works. But the thing that really What caught my attention and got me really interested was the operations of the company that Bankman Freed first worked for, which is called Jane Street Capital. And it’s a, um, an investment, an investment, a Wall Street investment firm.

[01:02:50] Tony: And it kind of, you know, the chapters on that, as it’s so interesting, their recruitment techniques, who they look for and what they do. If people want to have a good understanding of how Wall Street works now, or did a year or two ago, uh, it’s worth. worth reading. And just to pick on a couple of anecdotes of interest.

[01:03:11] Tony: So, I mean, first of all, Michael Lewis says that if you think Goldman Sachs or Morgan Stanley is Wall Street, forget it. You know, they’ve basically become much more like, um, a regular bank due to regulation changes since the GFC. The real action is in these small trading companies like Jane Street Capital.

[01:03:32] Tony: And they’re the ones that, you know, are making, are making outsize returns based on their CapEx size. And what they look for is people who can, in a very quick time, price a market and decide whether the investment or the bet is good or not. And so the way they recruit is, first of all, they look for people who’ve done things like run, won math contests.

[01:03:56] Tony: So Bankman Free was a, it’s probably on the spectrum, you know, just the Someone who completely had no interpersonal skills, parents were academics, but loved maths, did well on his maths competitions at some of the big Ivy League universities, got onto the radar of Wall Street recruiters and apparently it’s a thing that they all look for physics or maths.

[01:04:21] Tony: Brad’s who were precocious to go into Wall Street, paid him a lot of money. But the way that Jane Street recruited SBF was to just, um, take all the potential recruits for a day and just keep running games by them. And, you know, just without going into a lot of detail, the two that sort of stuck in my head were, um, Bankman Freed would be asked by, uh, by one of the Jane Street Capital people and generally it’s the other traders who are doing the recruiting, so, uh, a Jane Street Capital trader asks Bankman Freed, what are the chances that, uh, any of my relatives is a, is a professional baseball player?

[01:05:01] Tony: And, and then they judge, not just what the answer is, because it’d be pretty hard to, to work out what the odds were, but the process that, SPF got there and the questions they asked, so SPF asked, well, you know, define relative and the trader said, well, okay, immediate family plus cousins and uncles and aunts, okay.

[01:05:22] Tony: Now define professional baseball player and the guy said, okay, um, major league baseball player, current. Okay. or retired, or minor league baseball player. So Sam Bankman Fried sort of came up with a number of, there might be 30, 000 people in that cohort and got to the population size and came up with a number.

[01:05:41] Tony: But then he said to himself, Huh, why is this guy asking me this question? If he didn’t have a relative who was a baseball, professional baseball player, why would he have even have thought to mention that? Um, and not ask, what’s the chance of one of my relatives being a fireman or a carpenter? Um, so he said, okay, I’ve calculated what the, you know, percentage of the population are of the baseball athletes, but that’s wrong.

[01:06:10] Tony: That’s wrong. And he came up with a number of 1 in 50. And that was wrong too, but it was so much closer to the right number because the guy said, yes, my cousin is a Major League Baseball player. And, but they liked Sam understanding to ask the question or to think that the only reason he’s asking this is because it’s probably true.

[01:06:29] Tony: And so it’s going to be way less than the percentage of population. And there’s a few other ones like that. When they all start as interns, um, every day they get given a hundred bucks to, to lose and the traders keep coming up to them, offering them bets and testing them. And they had to cap it at a hundred dollars because early days people were just losing their paychecks on these bets because they’re so sort of hyped to, to make the deal and take the bet quickly.

[01:06:54] Tony: And one of them was, um, A trader walks up to a guy and says, uh, what’s the, what’s the chance of me having, um, a number of dice in my hand, in my pocket, a number of, you know, gambling dice, gaming dice in my pocket. And the guy came up with a number which basically hinged on there being five or less. And, um, And the, the trader offered him the deal that if he would pay him, um, I think it was like 10 for every dice less than five, but then the guy taking the bet had to pay 10 for every dice more than five.

[01:07:29] Tony: And the guy, the intern took the bet and then the trader pulled out a, um, pouch of miniature dice and there was 750 of them in his pocket. So like, again, it’s like the, the guy taking the bet didn’t ask enough questions, didn’t, didn’t frame the market properly and, and got an outsize.

[01:07:46] Cameron: Mm hmm. Mm hmm. Mm hmm. Mm hmm. Mm hmm.

[01:07:49] Tony: So, there’s just a couple of the stories.

[01:07:52] Tony: Really worth reading if you like that kind of stuff. And just really interesting at how the Wall Street trading firms work. Because SPF’s first job, this Jane Street Capital, was to trade ETFs. And so he had to very quickly, what would happen for example was, um, he’d get rung up and said when the market opens in India tomorrow I want to buy the Indian ETF.

[01:08:20] Tony: You know, the index ETF for the Indian market and, um, give me a price. And so Bankman Free would have to look at what the price it closed at, quickly scan the news. Has anything happened like a nuclear explosion or war with Pakistan? And then try and figure out what price to charge for the, this person who wanted to buy the Indian ETF before it opened.

[01:08:40] Tony: And then trade as well the ETF to try and, you know, if you got it wrong, recover the money. So it’s, um. Even that alone tells you a lot about how ETFs work, that there are players in the middle trying to make very small margins out of the stocks underlying the ETF compared to what the ETF is. And so, Bankman Free was putting big bets on large Indian companies who might drive the ETF, and then giving a price to the person

[01:09:07] Tony: for the ETF when it opens.

[01:09:09] Tony: That’s interesting,

[01:09:09] Tony: I thought. No, I saw the ad for it

[01:09:12] Cameron: good stuff. The thing about asking the questions reminds me of the new season of True Detective. Have you watched any of that?

[01:09:22] Tony: last night. Mmm

[01:09:23] Cameron: It’s only two episodes in. Really good. Jodie

[01:09:27] Cameron: Foster is the main cast in it. Christopher Eccleston turns up in episode two. But Jodie, it’s set in this small town in Alaska. Won’t tell you what’s going on but it’s creepy

[01:09:40] Cameron: as hell. But um, Jodie Foster’s sort of this grizzled old cop and she’s got a young guy who’s her uh, you know, up and comer, young fresh faced cop.

[01:09:54] Cameron: But one of her things with him is, What are the questions that we ask here? And he’ll come up with questions. She goes, no, you’re asking the wrong questions. You’ll have to stop and he’ll think it. She goes, yes. And what’s the next question that we ask? No, wrong question. Keep thinking. What’s the right questions.

[01:10:10] Cameron: And it’s good. You know, she’s like teaching him to think, you know, in the right way to solve the case and. You know, there’s the questions that you ask could determine, uh, you know, your, your answers that you come up with, I guess, you know,

[01:10:26] Tony: Yeah,

[01:10:26] Cameron: kind of reminds me of the, uh, Max Planck book I’ve been reading. Hmm. Asking the right

[01:10:34] Tony: and I’ve got to say, have you have you checked out Buki yet? It’s so good.

[01:10:39] Tony: Everyone I’ve recommended to has come back and said it’s just the best thing they’ve ever seen.

[01:10:43] Cameron: Oh no. I

[01:10:44] Tony: So funny,

[01:10:45] Cameron: add that to my list of TV things to watch. Bookie, I did watch.

[01:10:51] Tony: because what I, I went back and rewatched the last episode again last night, I just love it so much. And when I finished the streamer said if you like this check out Mr. in between.

[01:11:02] Cameron: right?

[01:11:03] Tony: It’s like that was a recommendation for it.

[01:11:05] Cameron: Yeah. Well, good. Uh, good, good call. Um, what was I gonna mention? Oh, Roger Rogerson. Died.

[01:11:17] Tony: Blue Murder. I watched that a

[01:11:18] Tony: couple of weeks ago

[01:11:19] Cameron: Did you? Where did you find it? I was just going to say, I’d love to find that to watch again.

[01:11:23] Tony: I think, I’m gonna say Netflix. Could be either Foxtel or Netflix. Netflix. Yeah, and they’ve, they’ve They’ve released it as two episodes, but each episode has two episodes in it, so that’s four episodes compressed, but Oh, man, it’s so good.

[01:11:39] Cameron: And I sort of remember that

[01:11:41] Cameron: as being, in my mind, that’s the beginning of good TV. Like before Sopranos, Blue Murder was the first thing I ever remember watching and going, Oh my God, why isn’t all TV this good?

[01:11:55] Tony: Yeah.

[01:11:56] Cameron: don’t think it gets credit for that, really. Like, everyone thinks good TV started with Oz or Sopranos and, you know, those HBO shows, but, uh, maybe Homicide, Life on the Streets, one of David Simon’s earlier shows, but Blue Murder was gritty.

[01:12:12] Tony: Blues, yeah. Yeah, oh, it’s Going, like, going back to watch it now, you just see all the actors when they were first Starting out, he became big. I think it’s Richard Roxburgh’s first big thing. He plays Roger the Dodger. But the thing that just really blew my mind was just how they did stunts back then.

[01:12:32] Tony: It says, first of all, there’s no CGI. And secondly, they just close off as little as they can of a busy street. So like, there’s a scene

[01:12:42] Tony: in a pub somewhere in Sydney. Botany or whatever. And the fight spills out in the street and you can see the cars in the background pulling up and people jumping out to see what’s going on as people, as people are being pounded on the footpath and then dragged back into the pub.

[01:12:56] Tony: It’s just incredible.

[01:12:58] Cameron: Oh, I gotta, I gotta watch that again. Um, the opposite of that is the Bollywood film that we watched this week, Pathan. So another Shahrukh Khan, massive action epic from last year. And I watched a bit of a behind the scenes VFX thing on YouTube afterwards. And there’s hardly a shot in the film that isn’t completely digital.

[01:13:27] Cameron: Like the amount of stuff that is just digital these days is insane. Like. It’s mind blowing how much of a film like that is digital, like, yeah, okay, you look at something like an Avengers film or whatever, and you go, yeah, okay, it’s all digital, you expect that, but this is, you know, just people, it’s like more of a Bond film, you know, like, it’s not, they do have superhero powers in these Bollywood films. One of my favorite scenes is there’s a big fight on a train and then they take down a helicopter which is attacking. The helicopter crashes into a bridge over this massive ravine and then the train goes over the bridge and as the train is going, the two heroes at this stage are on like the front carriage of the train, and as it’s hurtling over the ravine, they’re running up the carriage Then leaping to the next carriage and then leaping to the next carriage.

[01:14:26] Cameron: It’s absolutely ridiculous, but hilarious at the same time. Um, but like, okay. So you look at stuff like that and you go, yeah, of course that’s CG. But when you see the behind the scenes stuff, like. Nearly everything is CG. It’s 98 percent CG. These films. It’s crazy. It’s uh, but yeah, it was enjoyable. Over the top nonsense.

[01:14:53] Cameron: Um, alright, Blue Murder. Gotta make a note to track that down as well.

[01:14:59] Tony: Oh, it’s so good. Nettie Smith, Sallyanne Huxtep and her murder. Just all these things you used to read about as a kid.

[01:15:07] Tony: It’s incredible. And very chilling too, what

[01:15:10] Cameron: What were you reading as a kid?

[01:15:11] Tony: the cops doing. Well, you open up a paper and

[01:15:14] Tony: there’d be a whole feature about Sallyanne Huxtep and her murder and what the theories were behind it.

[01:15:20] Tony: All that kind of stuff.

[01:15:22] Cameron: You obviously were exposed to a lot of terrible stuff as a kid.

[01:15:27] Tony: Well, the Courier Mail mate, or the Sunday? The Sunday Mail.

[01:15:32] Cameron: I don’t know, did we, uh, speaking of kids, did I,

[01:15:35] Cameron: did, I told you about Fox’s

[01:15:39] Cameron: kindergarten teacher?

[01:15:43] Tony: You told me about one of the teachers, but I’m not sure if it was the kindergarten

[01:15:46] Tony: teacher.

[01:15:46] Cameron: that got done was, uh, Australia’s worst pedophile?

[01:15:51] Tony: No. Really?