Hello QAVvers

It’s another … Wednesday. I hope you all had a Happy Festivus and didn’t get storm damaged.

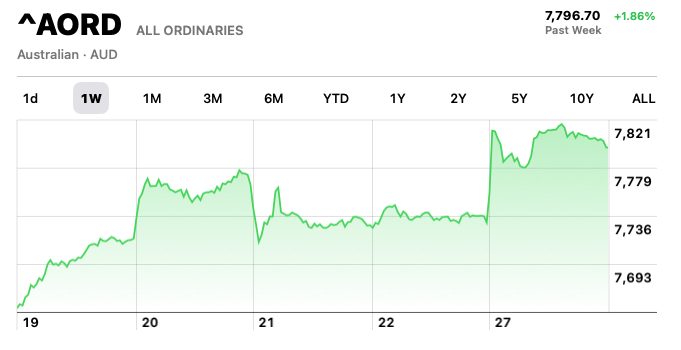

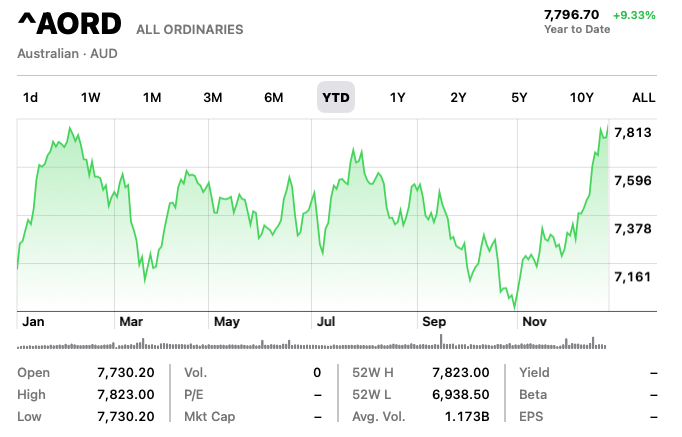

The AORD started the short week well. Hopefully it will finished the rest of the year just as strongly.

The YTD chart says it hit an all-time high, although the AFR is saying it was slightly short.

Let’s have a look at the portfolio.

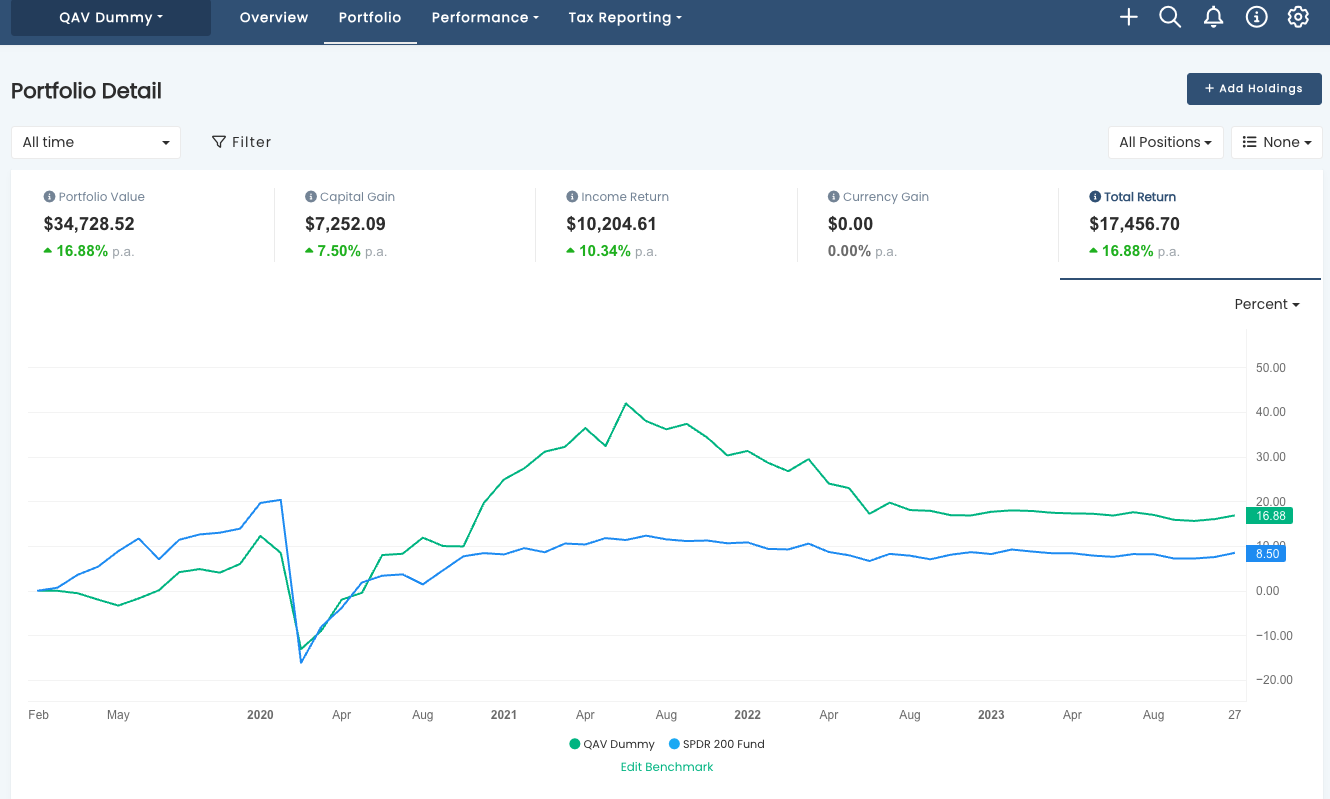

QAV PORTFOLIO REPORT

The Dummy Portfolio is performing well against the benchmark over multiple time frames.

SINCE INCEPTION (02/09/2019)

Our portfolio is doing roughly double market since inception. Right on track.

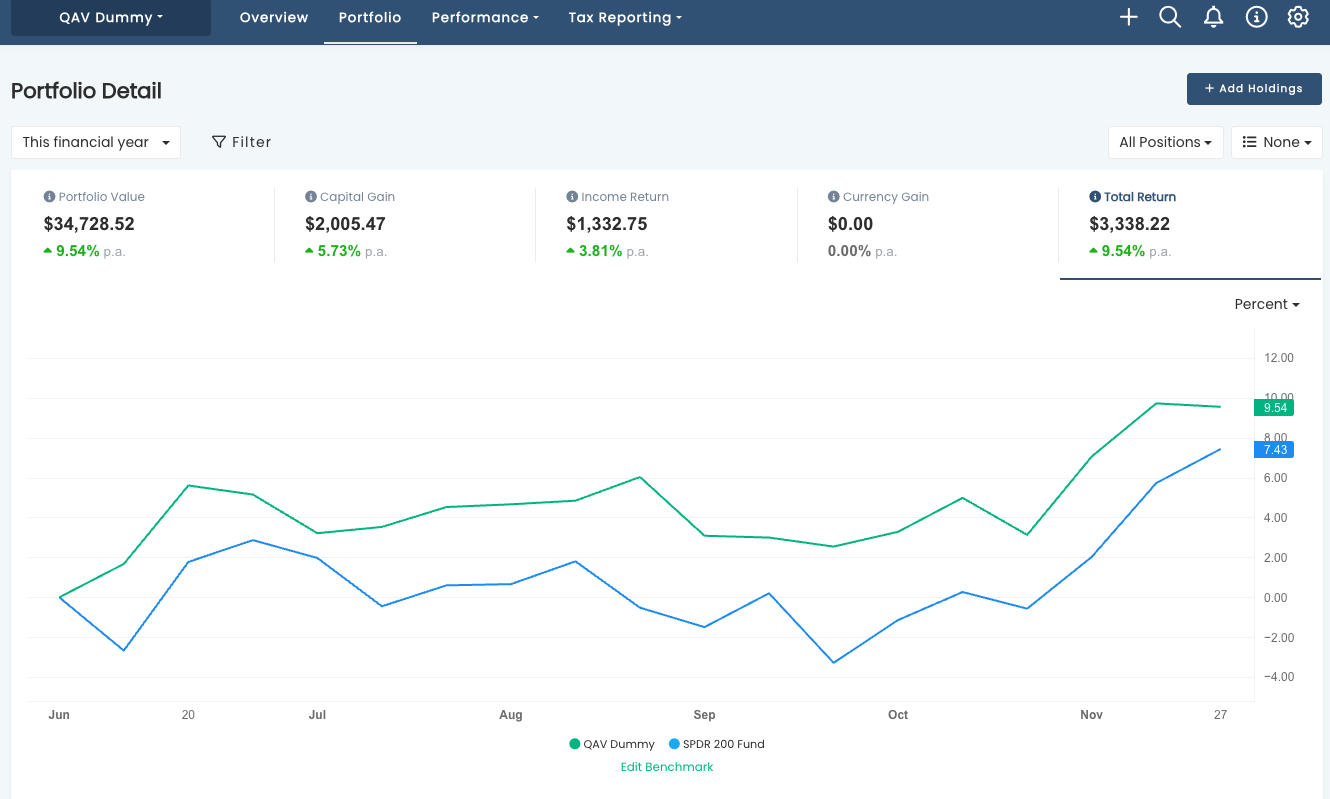

FY REPORT

For the FY we’re doing 1.3X better than the STW.

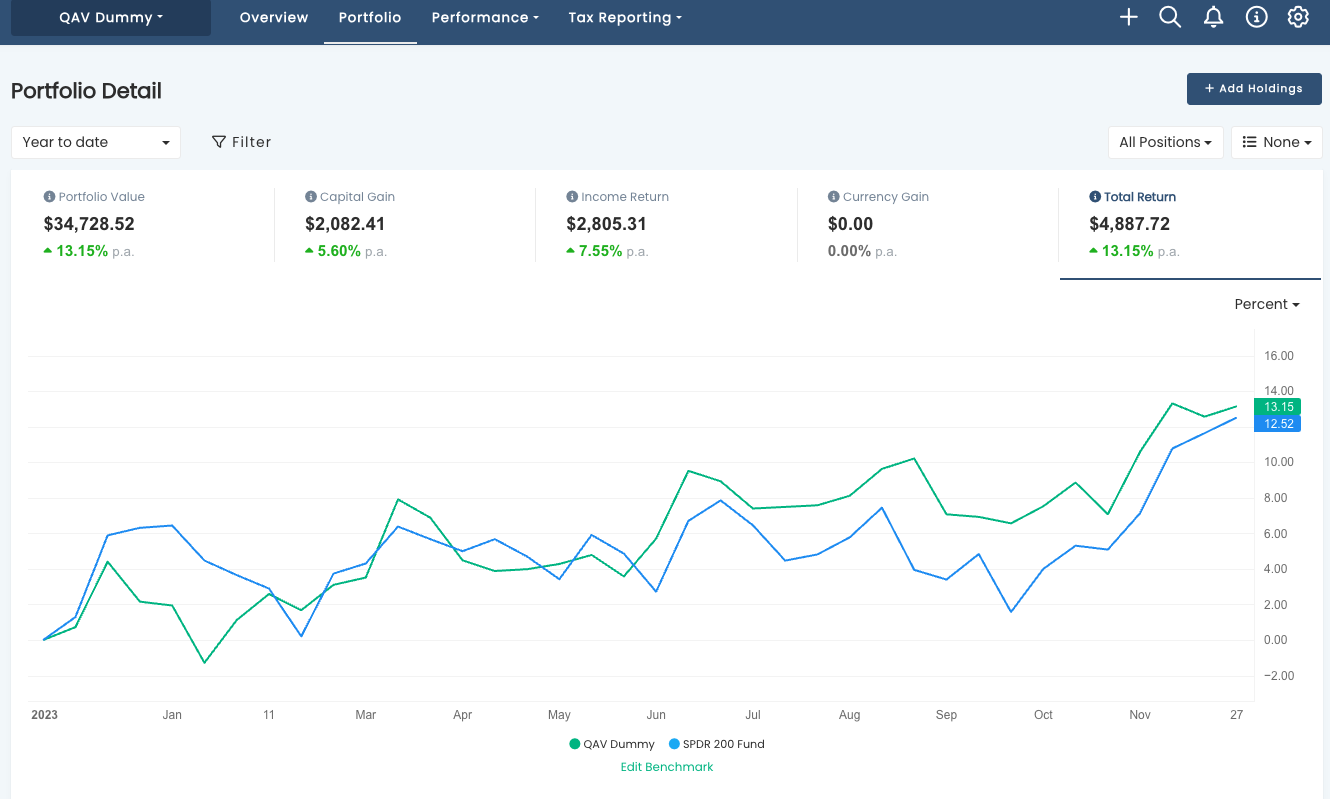

YEAR TO DATE

We did slightly better than the STW for 2023 YTD. Not bad for such a choppy year.

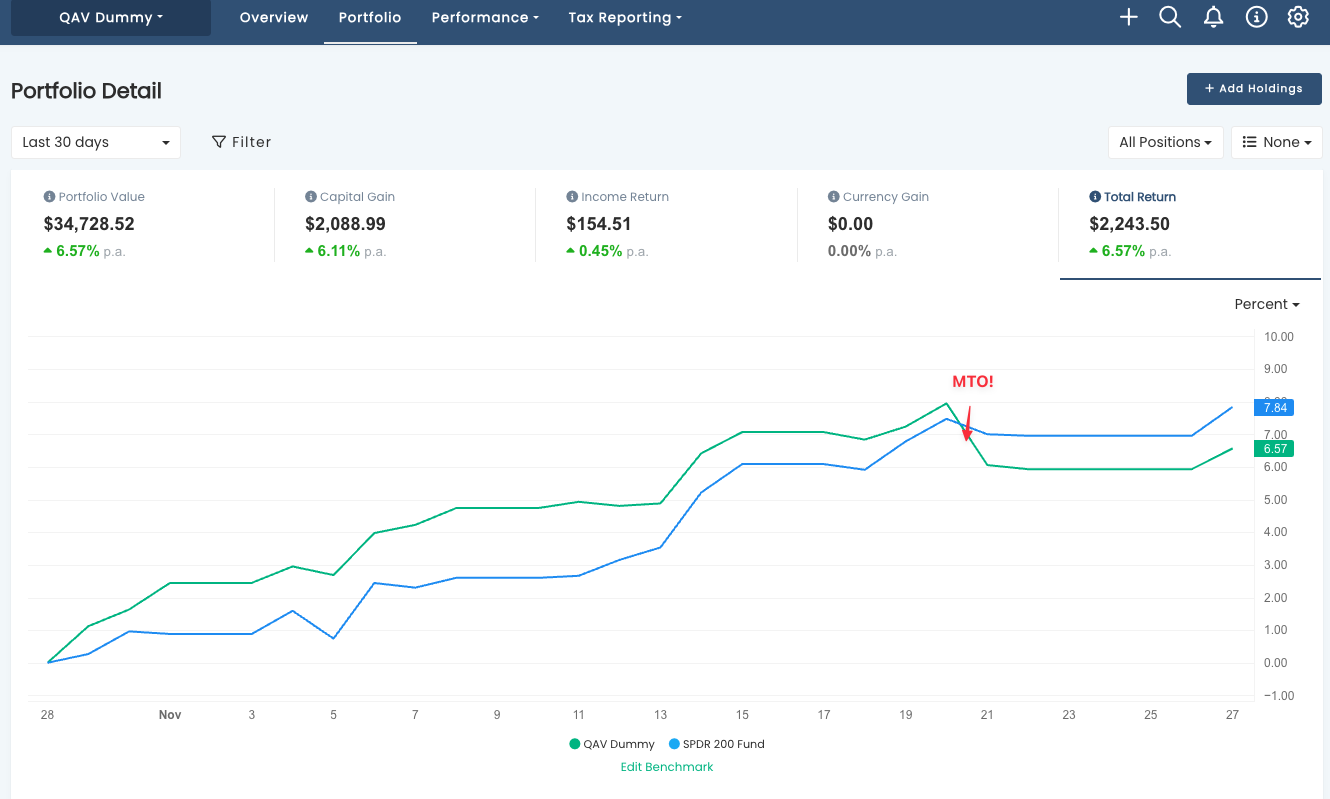

30 DAYS

In the last 30 days we’re slightly underperforming the STW, largely thanks to MTO’s spectacular collapse last week!

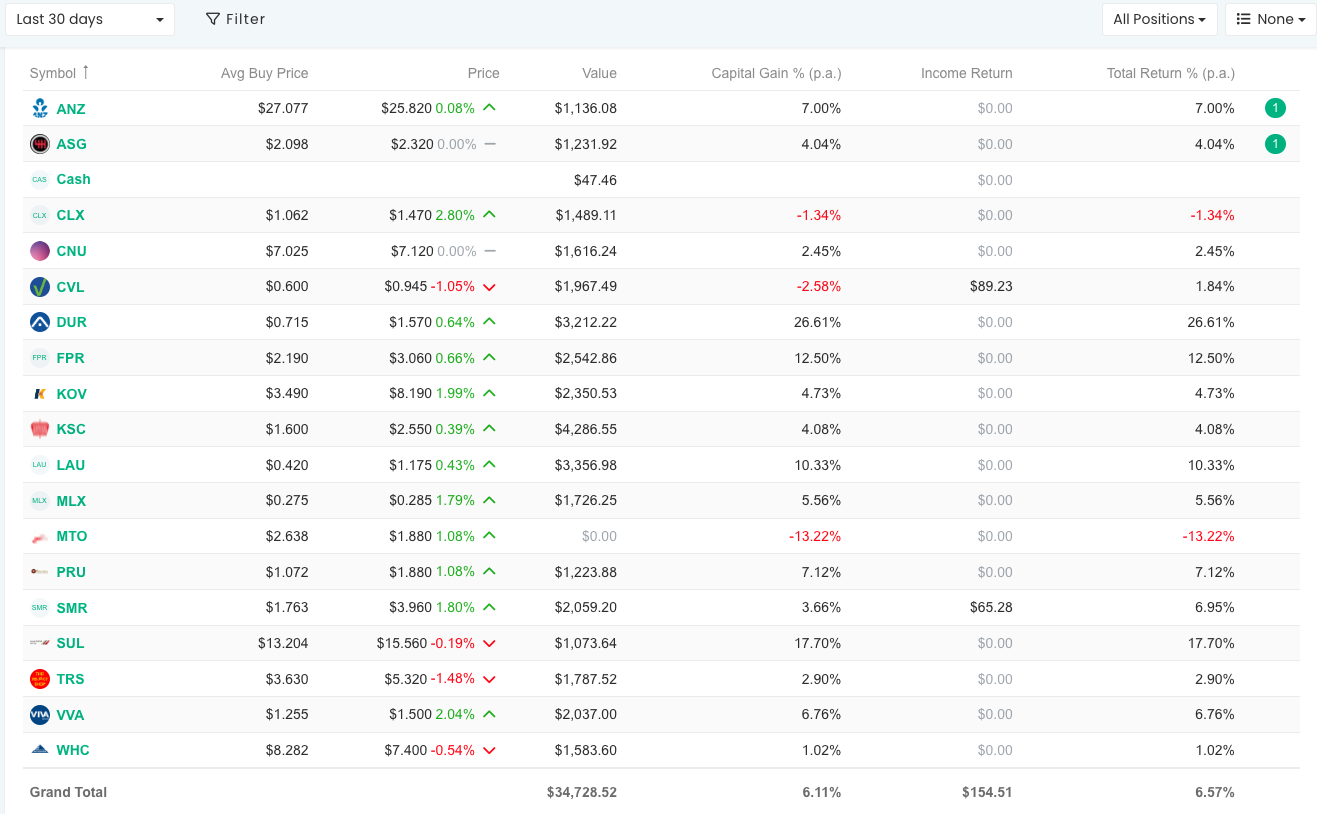

Here are how our stocks have performed in the last 30 days.

RECENT TRADES

In the last 7 days we sold MTO and replaced it with WHC.

QAV STOCKOPEDIA DUMMY PORTFOLIO REPORTS

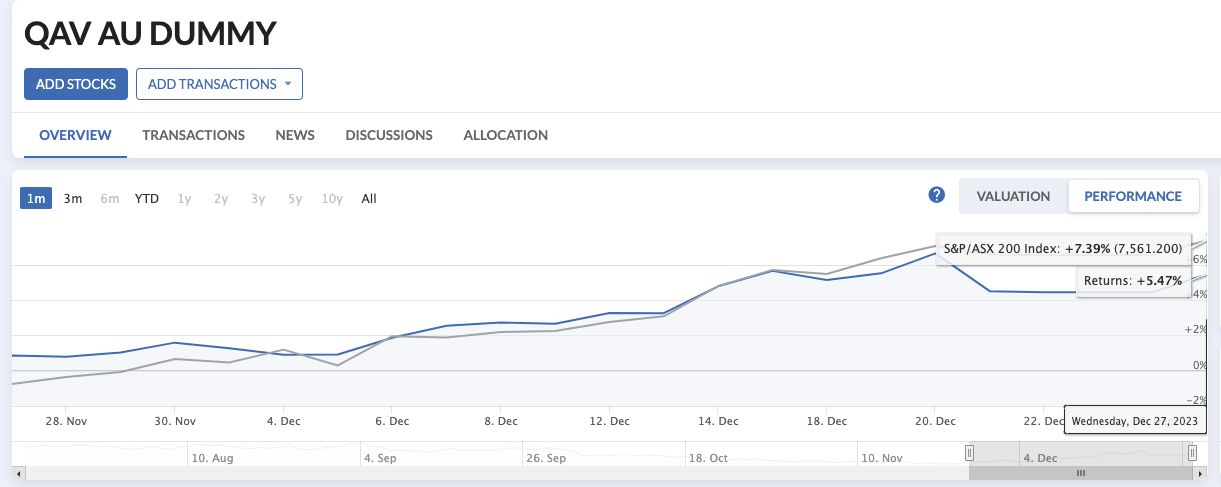

QAV AU DUMMY

Slightly lower performance than the Stock Doctor portfolio.

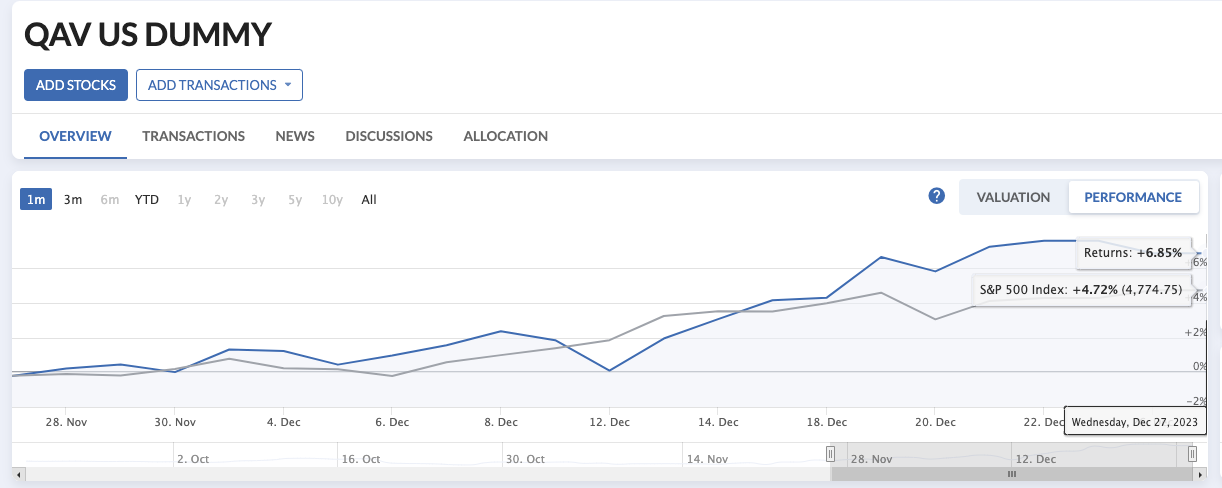

QAV US DUMMY

This one is doing better (but not as insanely well as I first thought last week, as I explained on the podcast… so stupid).

FREE WEBINAR

I’ll be doing another webinar in a few weeks.

STOCKS OF THE WEEK

During the last week, we also traded some stocks in our Light portfolios. Details here.

** As always, please check our work, DYOR, and consult a financial advisor before making any investing decisions.

BUY LIST

Each week we produce a buy list that we share with our members. The intended primary purpose of this buy list is for club members to use as a reference for comparing their own buy list. In theory, all of our buy lists should look pretty similar each week.

As always, please check our work, DYOR, consult a financial advisor before making any investing decisions.

THIS SECTION CONTAINS CONTENT WHICH IS VISIBLE TO QAV CLUB SUBSCRIBERS ONLY.

LAST WEEK’S EPISODE

FREE EDITION:

On this episode: The AORD is having a good Xmas (so far), STW and AFI above their buy lines, our portfolios are doing well, pulled pork on CXO (Core Lithium)

Club: new Commodity Status history feature, PRN poll, FPR net operating cf, CCP on a tear, talking about REITs, and why BFG is having a run.

Episode Transcription

QAV 651 Club

[00:00:00] Cameron: All right, welcome back to the QAV.

[00:00:06] Cameron: Happy share market. Tony.

[00:00:08] Tony: Happy ASX Cam,

[00:00:10] Tony: and Merry

[00:00:10] Tony: Christmas

[00:00:10] Tony: too. It’s coming up.

[00:00:12] Cameron: Merry Christmas to you too. It’s, uh, it’s, it’s a merry Christmas for the all ordinaries. Tony,

[00:00:18] Cameron: a look just before we went to air. It’s almost back at, its all time high. I think we’re about one and a half percent off the all time high, which having a quick look through my little chart on Yahoo Finance is about, I reckon the end of August 2021, it hits 7826.

[00:00:40] Cameron: It’s currently at 7701 today, which is about one and a half percent below 7826.

[00:00:48] Cameron: So, that’s been a fun two and a half years.

[00:00:52] Tony: Well, we had a couple of good years,

[00:00:54] Tony: and

[00:00:54] Tony: then we’ve had a couple of sideways

[00:00:55] Tony: years. So it’s it’s been the usual ride on the ASX, but it’d be a good [00:01:00] Christmas present if we got back to the, uh, the all

[00:01:02] Tony: time high.

[00:01:04] Cameron: Yeah,

[00:01:05] Tony: Yeah.

[00:01:06] Cameron: opened my notes. I was like, can we move on now? Are we done with that whole period? Is that phase

[00:01:11] Tony: Well, I think the market thinks you can because I noticed that, uh, both STW and, um, AFI, the two sort of big market indexes, ETFs and LLCs, have both crossed over into buy line

[00:01:26] Tony: territory. So, uh, the trend is telling us that the, uh,

[00:01:31] Tony: yeah, it could be a happy Christmas and a good 2024, but we’ll see.

[00:01:34] Cameron: We’ll see. Uh, let me talk about our portfolios while I’m on

[00:01:41] Cameron: the subject of things in the market, et cetera. I did a weekly report today for the Stock Doctor dummy report.

[00:01:50] Cameron: It’s doing a little bit better than double market since inception. I

[00:01:54] Cameron: think we’re up. just a little bit under 17 percent per annum over the

[00:01:59] Cameron: last,

[00:01:59] Cameron: [00:02:00] whatever it is, four and a bit years. Um, versus, uh, what did that say, 8, uh, for the STW, 8. 25.

[00:02:09] Tony: That’s pretty bloody good. 17. Percent per annum for the last

[00:02:13] Tony: four years. Let’s

[00:02:15] Cameron: that is pretty

[00:02:15] Cameron: bloody

[00:02:16] Tony: a moment and reflect on that. That’s pretty

[00:02:17] Tony: good. No,

[00:02:20] Cameron: I mean, and, you know, I’ve run it, I’ve run

[00:02:22] Cameron: it for, what, I guess, the last three years. I don’t think you’ve had much involvement in the decisions for the last three years. And I know

[00:02:28] Cameron: fucking nothing about investing. So, if I can, well, I didn’t five years ago. So,

[00:02:36] Cameron: if, if little dummy me can learn how to run this thing and get double market consistently over the last, uh, four and a half, five years.

[00:02:45] Cameron: I mean, that’s,

[00:02:47] Cameron: I mean, I, I, I take it for granted

[00:02:49] Cameron: now. That it’s doing that well. Like, it’s not, like, it’s not even a thing. Like, yeah, it’s doing a bad double market. Boring, you know, you know, but it is, like, it’s really insane. It’s [00:03:00] the, the, it’s, it’s, it’s all the system. Uh, for the financial year, we’re doing 1.

[00:03:06] Cameron: 6 times better than the STW. We were up

[00:03:08] Cameron: as much as three times last

[00:03:10] Cameron: week, but we’ve slipped a little bit this week. Um And for the 30 days, we’re slightly below. We’re up about 4. 5 percent though, per annum for the last 30 days, STW is up about 5. 5%. But, one thing I wanted to point out, we’ve talked about this a bit over the last couple of years, uh, the, the breakdown in our portfolio performance between capital gain and income return.

[00:03:33] Tony: yep,

[00:03:34] Cameron: for a long time there, income was driving most of it. In fact, if I look at the all time Stats, capital gain is worth about seven and a half percent of that 17. Uh, income returns about 10, 10 and a half percent

[00:03:51] Tony: right,

[00:03:53] Cameron: per annum. But if I look at the financial year, capital gains five and

[00:03:57] Cameron: a half, income returns 3.

[00:03:59] Cameron: 8.[00:04:00]

[00:04:00] Cameron: so capital gain has been the major

[00:04:02] Cameron: driver in our return so far in the last six months.

[00:04:06] Tony: yeah, dividends tend to mean, are more meaningful

[00:04:10] Tony: over time. So, you know, you buy a

[00:04:12] Tony: stock and it’s 5%, that’s fine in the first year, but if you keep it for a couple of

[00:04:17] Tony: years and that, you know, if it’s doubled in value in four years time,

[00:04:20] Tony: the dividend yields doubled in value as well, so you’re kind of getting a guaranteed 10 percent

[00:04:24] Tony: straight away.

[00:04:25] Cameron: Yeah, right. Okay.

[00:04:26] Tony: Yeah.

[00:04:27] Cameron: In the last 30 days, our big performers have been DUR up 25 percent in the last 30 days per annum. Uh, MTO up just, you know, just slightly under 15 percent per annum, SUL up 12. 7, FPR up 12. 32. Oh! Got something to say about FPR. So Alex F., Alex Franklin pinged me. And said he noticed that FPR was on this list as, as being one of the strong performers, but wasn’t on the buy [00:05:00] list and he didn’t know why.

[00:05:02] Cameron: And I tried to figure out why. I went back, I looked at my download, wasn’t in my download this week, wasn’t in Alex Kynaston’s download. And I was trying to figure out why. I went back through a couple of downloads and it wasn’t showing up. I went to Stock Doctor and started going through the numbers and they reported on the 13th of November and they reported negative net operating cash flow.

[00:05:29] Tony: Yeah, right. I can see

[00:05:30] Tony: that from the September numbers. Yeah. Okay.

[00:05:32] Cameron: Yeah. So I’ve got, I actually went to their website. Report their annual report in case it was a Stock Doctor mistake, which wouldn’t be the first time, but no, this is legit. Operating cash flow, customer receipts 815 million for FY23, payment to suppliers and employees 413 million, income tax paid 10. 8 million, net interest paid 51.

[00:05:57] Cameron: 8 million. [00:06:00] Uh, but then they’ve got a purchase of operating

[00:06:04] Cameron: finance lease vehicle 611. 3 million. Proceeds from sale of operating leased vehicles, 215. 1, leaves them with net operating cash flow of 56. 8. so good. business, doing well, but it’s

[00:06:21] Cameron: the nature of their business, right? They’re out there buying a lot of vehicles

[00:06:25] Cameron: and it puts them in a negative.

[00:06:27] Cameron: So it doesn’t even show up in our download because what our filter is You have to have Operating Cash Flow greater than zero. So

[00:06:34] Cameron: it’s one of the few filters that we have that actually does filter out companies. Because most of them, most of our filters say any, any, any, any,

[00:06:42] Cameron: any, but Net Operating Cash Flow

[00:06:44] Cameron: is one that we actually want them to have positive.

[00:06:48] Tony: Yeah. And it’s, it’s been something which I’ve noticed in the past that when something goes from a string of positive cash flow halves to a negative one, it can be a leading indicator for a downturn. Um, I haven’t [00:07:00] done the research on that, but it’s, it’s kind of on the list. But, um, it may not be the case for Fleet Partner, because as you say, if they’ve decided to bulk up and buy all the cars that are going to be leased out, then It might be a short term occurrence.

[00:07:17] Cameron: uh, just if people

[00:07:18] Cameron: are

[00:07:18] Tony: just just on that too, Cam.

[00:07:20] Cameron: wasn’t on the list, that’s why.

[00:07:21] Tony: Yeah, thanks. Just on that too, I, I spoke last week about, um, whether you were better off buying all three listed fleet, uh, management companies, um, fleet partners and, uh, SIQ, Smart Group, and MMS Macmillan Shakespeare. And that was on the basis of Macmillan using, losing a contract and, It’s like you picking it up.

[00:07:43] Tony: Um, yeah, so for this year it would have worked out well. It would have beaten the index, um, but over five years it was underperforming the index and,

[00:07:54] Tony: um, I did a couple of other periods in between and it still looks like you’re better off buying the best one [00:08:00] out of the three at the time. So Fleet Partners has been that for us.

[00:08:04] Tony: It’s been on the buy list all year and it’s outperformed this year compared to its two cohort.

[00:08:09] Cameron: There you go. There you go. Well, that’s Good bit of analysis. Thank you. Just staying on the reports, a couple of things I want to mention. I, I have mentioned on here over the last couple of months that I’ve been working on Stockopedia version of the checklist and testing that out

[00:08:27] Cameron: both with an Australian dummy portfolio built

[00:08:30] Cameron: purely from Stockopedia and a US dummy portfolio.

[00:08:34] Cameron: And I thought starting this week I’ll report on how those are going and over Christmas one of my plans is to sort of clean up the stockopedia version of the checklist so I can share it with people because I’ve had some people reach out and express interest in having a look at that. There’s a lot of metrics that we use in our regular checklist that we can’t get out of stockopedia [00:09:00] because they don’t track things like Own a Founder or PE History, things like that, at least not in a way that’s easy to get access to.

[00:09:10] Cameron: But, um, just by the by, the AU dummy portfolio that I’ve built, Using Stockopedia. It’s performing about the same over the last 30 days as the Stock Doctor one.

[00:09:24] Cameron: It’s up about a little bit more than 4 percent versus 5 point something for the,

[00:09:29] Cameron: uh, STW. So it’s doing about the same. Um

[00:09:33] Cameron: And the US one, I have mia culpa, I did send out my report this morning and said it was killing it, it was like four times as good, and I can’t, how many times do I have to do this mia culpa?

[00:09:46] Cameron: When something looks better than it should be, You would think there would be part of my bra like, in every other aspect of life,

[00:09:55] Tony: You’re a

[00:09:56] Cameron: it’s a political thing, I’m a skeptic. I’m like, oh, hold on a cotton [00:10:00] picking minute, that can’t possibly be right, but this, nah, my red alarm didn’t go off. I went, oh, yeah, that’s legendary, because I did know that some of the stocks have been doing really well.

[00:10:10] Tony: right.

[00:10:11] Cameron: Um, but then getting ready to do the show, I was drilling down on those stocks so I could talk about one of them, uh, I would talk about them and why they were doing so well. One of them, WLFC, Willis Lease Finance, I believe their catchphrase is what you’re talking about, Willis.

[00:10:27] Cameron: Um, I had screwed up the buy price when I was, uh, putting the transaction into, uh, Stockopedia

[00:10:36] Cameron: put it in at a quarter of what it really

[00:10:38] Cameron: was, so that, uh, blew those gains away when I adjusted it.

[00:10:43] Cameron: But some are up really well. Like A AMC networks is up 24% since I bought it. Le Lands end is up 26% gas. Stealth gas, GASS, is up 34%. [00:11:00] Um, pretty sure I didn’t screw that one up, but maybe I should look at that too.

[00:11:09] Tony: Land’s End, is that the direct marketing clothing company?

[00:11:13] Tony: Do you know?

[00:11:15] Cameron: Uh, uh, yes, yes it is.

[00:11:18] Tony: Oh, that’s fine. I used to sell Land’s End clothing in Australia through MyerDirect. Yeah.

[00:11:25] Tony: Whenever that was, 20 years

[00:11:26] Tony: ago. Yeah.

[00:11:27] Cameron: Uh, I thought you meant like you were like going door to door.

[00:11:30] Tony: no, no, no, no, no,

[00:11:31] Cameron: you like to buy some

[00:11:32] Cameron: Land’s End clothing?

[00:11:33] Tony: no, it was one of the brands that my direct, uh, Retailed in Australia. We had a deal with Land’s End in the U.

[00:11:38] Tony: S. In fact, I think it was the U. K. from, from memory, but

[00:11:41] Tony: anyway. Um,

[00:11:43] Cameron: gas, the gas buy price is right. I just double checked it by the way. So that’s all good.

[00:11:48] Tony: AMC, isn’t that, wasn’t that one of

[00:11:50] Tony: the game stock to the moon?

[00:11:52] Cameron: It was! It

[00:11:53] Tony: So it’s come good, has it?

[00:11:55] Tony: Anyway.

[00:11:56] Cameron: Wow. I mean, it’s not up, you know, a thousand [00:12:00] percent, uh, like they thought it was going to be or whatever, but it’s, it’s, you know, it’s doing okay from when I bought it. Um, yeah, I bought that at, uh, 15

[00:12:16] Cameron: and what is it now? 19. 37.

[00:12:21] Cameron: So yeah, it’s had a little bit of a

[00:12:22] Cameron: spike. Anyway, so I’ll keep reporting those each week and you know, where, just to let people know where my head’s at with all of this stuff is because we’re missing a lot of data points and we don’t have the tools yet to sort of. Do large scale regression testing with historical data to see whether or not these data points are going to be long term important or not, or how important.

[00:12:50] Cameron: I’m sure they are important, but how important? Uh, so I’m just sucking this and seeing it for a while, testing it out, running it, seeing how things seem to perform. Um, [00:13:00] So far so good, but, you know, it’s only been a month or two, so, um, we need, obviously, more time than that. One other thing I did want to mention about the report today is I have a my little coding project this morning was to collate all of the commodity status history, um, over the year or 18 months or so that we’ve been ad putting it in our buy list each week.

[00:13:30] Cameron: Into a single sheet. Which I’ll have in the buy list each week. It’ll be a single tab. I think it’ll probably replace the existing tab. So rather than the existing tab in the buy sheet each week, which just has the commodity status for this week, it’ll be a, um, uh, uh, historical view with the latest. This week will be the latest, uh, column in the sheet.

[00:13:53] Cameron: Because I figure it might be interesting, uh, in some of our analysis to go back and have a look at the commodity status. I know you [00:14:00] and I were talking off air before about regression testing and How do we get that data? We’re going to try and figure that out, but I thought it might be interesting just to have a look at it and go, okay, well, when, at any point in time, so when did iron ore last become a buy?

[00:14:14] Cameron: When did it become a

[00:14:14] Tony: yeah, right. Yeah, good.

[00:14:16] Cameron: a look. So,

[00:14:17] Tony: That’s really useful because what we found was using the four years worth of buy list was our own regression database. Um, you don’t have to try and go from scratch to find source data. We’ve got it if we keep, you know, building it in a, in a uniform way over time. So that’s a good

[00:14:34] Tony: idea.

[00:14:35] Cameron: and as Gary knows, cause he said this on Facebook, it gets really addictive when you realize you can sort of, I was sitting there like yesterday, last night, I was thinking, wow, I wonder if I can just write some script that will go through. 18 months worth of spreadsheets and just pull out all of the data I want and

[00:14:55] Tony: Wow.

[00:14:55] Cameron: it.

[00:14:56] Cameron: I went into GPT this morning and said, Hey, can I, can you help me do that? Yeah, [00:15:00] absolutely. No problem, mate. And, um, half an hour later, it was done. A little bit of testing, little bit of back and forth debugging, all done. So yeah, it’s fantastic. I love it. Yeah. Um,

[00:15:14] Tony: the Stockopedia portfolio, the Australian one and our dummy portfolio, how similar are they? How many stocks are in both?

[00:15:24] Cameron: Um, but I can, I can work it out.

[00:15:27] Tony: That’s all right.

[00:15:28] Cameron: just have a look. No, it’s let’s do that. You’re not going to be here for the next couple of weeks. Tony’s taking his Christmas vacay as a usual. I’m gonna, I’m going to do some really, really just, you won’t believe how good the things are

[00:15:44] Tony: can I put my hand up and say, don’t play all my bad pulled porks this time in the Christmas compendia.

[00:15:51] Cameron: What?

[00:15:52] Tony: Pick out the good ones.

[00:15:56] Cameron: Hey, that was for science. I was seeing [00:16:00] how they went. Cause, cause they recover, like half the time they recover and it’s all good. Okay. So I’m looking, uh, I’ve got the two buy lists side by, uh, two, sorry, portfolio side by side, looking for commonalities. Um, ASG is on both. FPR is on both. LAU is on both, MTO is on both, now obviously these were started at different times, you know, so, the, the, the, Stockopedia one’s far more recent, TRS, the reject shop is on both, and VVA, Viva Leisure, but, I’ll just, I’ll run through the, uh, sorry, the, the Stockopedia one, so you, you can see the, the stocks that are on here, ABG, Abacus Group, ALD, Ampol,

[00:16:50] Tony: That’s just off our buy list from memory, or it was anyway, at

[00:16:53] Tony: the bottom.

[00:16:54] Cameron: Yeah, it just came on. I think I did one late. I think I put it in the light portfolio [00:17:00] too late last week. I saw it turn up when I did one Thursday. Afternoon, this is Stockopedia, oh sorry, Stock Doctor, uh, buy list for light, ASG, ERD, Eroad, uh, Fleet Partners, JYC, Joyce, Lindsey, McMahon, MAH, MTO, NAB, NZM, OML, AK, see, I feel like I’m reading the alphabet here, TRS, SSM, Service Stream, SKT, Sky Network, SXE, Southern Cross Electrical, Viva Leisure, and Vysan, V Y S.

[00:17:34] Cameron: So they’re all,

[00:17:35] Tony: NAB’s the only one that’s either not on our buy list or close to our buy

[00:17:39] Tony: list.

[00:17:40] Cameron: and I think I added that to light last week too, I think that

[00:17:43] Tony: Ah, okay,

[00:17:45] Cameron: week on, uh, my, let me just check that. I think, I think I did find that turn up when I did a buy list on Thursday.

[00:17:53] Tony: so they’re fairly similar.

[00:17:55] Cameron: Oh no, it wasn’t NAB, I didn’t add NAB. What was the big, there was a really big one that I

[00:17:59] Tony: Yeah, [00:18:00] I added ANZ a couple of weeks ago, so it could have been ANZ on the Stock Doctor

[00:18:04] Tony: buy list.

[00:18:06] Cameron: I do have A and Z and a couple, um, oh, Blue Scope Steel, it might have been. When did I add that?

[00:18:14] Tony: No, Bluescope’s been on our buy list, but I think it’s been a commodity sell for a while, with steel.

[00:18:19] Cameron: uh, really? Steel a commodity sell?

[00:18:23] Tony: Oh, I thought so. Well, it was when it was on the buy list, because I couldn’t buy

[00:18:25] Cameron: no, this is the one that I added, um, last week. It was BSL. That was, God, how could I have missed that? Steel’s a buy on our, uh, commodity sheet TK. Let

[00:18:39] Tony: well, I’m going back a month or so, so maybe it’s, uh, it’s just become a buy.

[00:18:44] Cameron: me just, uh,

[00:18:46] Tony: Well, maybe BlueScope was a three point.

[00:18:49] Tony: Anyway, last time I looked at trying to add BlueScope Steel, I couldn’t do it

[00:18:52] Tony: for some reason.

[00:18:54] Cameron: well, you know what I can do, Tony? Um, I can look at the commodity history tab [00:19:00] that I just built and I can tell you now exactly when steel became a buy. It became a buy, Oh, quite a while ago. Um, 30th of October, it became a buy.

[00:19:14] Tony: Yeah, okay. Well, that’s a couple of months ago, which is probably when I was looking at BlueScope Steel

[00:19:17] Tony: then. Okay.

[00:19:20] Cameron: for three, no, four reporting periods before that, then it was a buy in September, Josephine, buy. Last time it was a sell was, uh, late August, it has been a Josephine for a few reporting periods, a few weeks, sorry, I mean, there. Oh my god, this is so cool! status, history, I knew I was gonna need that at some point.

[00:19:42] Cameron: God, I, I impress myself sometimes, I tell you,

[00:19:44] Tony: Oh, that’s always a great way to be to impress yourself. Um, well, you keep impressing yourself. I’m just going to take a step away from the microphone for a minute and turn some fridges off, which I can hear whirring in the background, which may impede the

[00:19:58] Tony: quality. Hang on.

[00:19:59] Cameron: I’ll quietly go [00:20:00] and impress myself while you do that, yeah. Just kidding, folks. I don’t impress myself. I’m being facetious. I’m never impressed with myself. I’m struggling just to keep up and be half as smart as most people. I was at Kung Fu the other day and my Sifu walked past and said, you got it? And I said, I’ve never got it. You know I’ve never got it. I don’t know what I’m doing.

[00:20:20] Tony: I don’t know. I saw you on the Facebook group listed as Kung Fu

[00:20:22] Tony: expert.

[00:20:24] Cameron: yeah, which I thought Facebook had worked out, uh, but then it turns out I must have done that myself at some point.

[00:20:31] Tony: Really?

[00:20:32] Cameron: I think it, well, it, it, it gives you suggestions about what you can be an expert in. And I think I was like, sure, that’d be fine.

[00:20:38] Tony: How would Facebook even know you did

[00:20:40] Tony: Kung Fu?

[00:20:41] Cameron: I don’t know. I think you, you put in your interests, what are your hobbies? You know, that kind of stuff. I think I put that in. Hey, speaking of people that aren’t experts, we did that poll after last week’s show about PRN. And I asked people, you gave them four options in the poll. They sold it Monday when [00:21:00] it first became a three point trendline sale, Tuesday, which was the next day, uh, the third option was I own it, but I haven’t sold it because I don’t follow the rules.

[00:21:09] Cameron: And the fourth option was I don’t own it. Uh, last time I looked at this was last night, 73 percent of people who responded said they don’t own it, which is not really a useful piece of information, but okay, uh, the majority of people who own it didn’t sell it, and uh,

[00:21:27] Tony: Yeah, but if you take out the 73 percent who didn’t own it, about a third of the people who did own it sold it Monday, Tuesday.

[00:21:35] Cameron: Uh, well, yeah, maybe, because I’m not sure about that. Sold it Monday. Last time I looked at that, I think there was only one person. I think it was Daryl. I’m just bringing it up here. So yeah, only Daryl sold it on the Monday. three people, including me sold it on the Tuesday.

[00:21:56] Cameron: Eight people said they own it, but haven’t sold it. [00:22:00] So yeah, you’re right. There’s a third, even when I do it that way. A third of the people sold it Monday or Tuesday.

[00:22:06] Tony: Yeah, but I think you, you identified somewhere else that the volume was quite heavy on that day, so it wouldn’t have been an issue, I don’t think.

[00:22:14] Cameron: No. And I feel bad for the people that haven’t sold it because at least when I checked last night, it had kept falling. see where it is today. Oh, it’s down again

[00:22:27] Tony: just shows that people aren’t good robots, they don’t follow the rules.

[00:22:32] Cameron: So I sold it at 1. 04, it’s currently at 0. 97.

[00:22:37] Tony: A good AI would have followed the rules, it would have sold

[00:22:41] Tony: straight away.

[00:22:42] Cameron: yes. So, well, I hope for the people that haven’t sold it, that, um, it turns around. But so far, uh, it does not look good for

[00:22:52] Cameron: them.

[00:22:54] Tony: Hmm.

[00:22:54] Cameron:

[00:22:54] Cameron: pointed out in our Facebook chat that CCP’s been on an [00:23:00] absolute tear this week. We love CCP. I went and had a look and they have, they’ve been doing well since Looks like the middle of

[00:23:09] Cameron: October, but I RULE 1’d it back in October when it plummeted.

[00:23:15] Cameron: Remember they came out with their results and just the bottom fell out of it? I RULE 1’d it at 17. 31. And today it’s at 15. 93, so glad I sold it when I did, but um, yeah, it’s had a, it’s had a good couple of weeks, it’s gone from 12 bucks up to nearly 16 bucks, but um, yeah, Rule 1 did me well in that instance.

[00:23:53] Tony: It did really well and I remember at the time commenting that this is, I’ve seen this before and Credit Corp are [00:24:00] really cautious about their guidance and like to under promise and over deliver and I think the market’s working out now that it probably overshot when it sold off that quickly. Well,

[00:24:14] Cameron: in the market are working out something that you’ve been telling me about CCP for five years. ’cause you, you always tell me that about CCP, even I know

[00:24:24] Cameron: that about c ccp. What are these highly paid professionals doing?

[00:24:27] Tony: we see it every half that the stock price goes down after they release their results and it recovers ground steadily and gets to new highs after they market digest

[00:24:38] Tony: what

[00:24:38] Cameron: So why don’t we sell it a week before their results or the day before the results are due out in future?

[00:24:44] Tony: And that’s, yeah,

[00:24:46] Cameron: or

[00:24:46] Tony: that’s a good idea. I don’t, I don’t think this, this big downturn that happened recently was after their results. I think they came out with an announcement about, um, the U. S. [00:25:00] The US business not going as well as they

[00:25:02] Cameron: Uh, it was a confession.

[00:25:04] Cameron: Hello, Alex!

[00:25:06] Tony: Hi, Al. I just wanted to say that we found out recently that Alex graduated

[00:25:10] Tony: with her Master of Fine

[00:25:11] Tony: Arts and she’s on the

[00:25:12] Tony: Dean’s List,

[00:25:14] Tony: which means she did really, really well.

[00:25:16] Alex: Yeah. I still

[00:25:17] Alex: haven’t figured out what it means exactly, considering I did not attend my graduation.

[00:25:24] Tony: Why not?

[00:25:25] Alex: Uh, I don’t know. It’s a lot of effort. I, and I, um, it’s like six months out

[00:25:30] Alex: from me actually finishing my degree and a whole year after I did my grad show, so I didn’t

[00:25:35] Alex: feel the particular need to go to Marble Stadium

[00:25:38] Alex: and spend a

[00:25:38] Alex: couple hundred dollars renting a gown and a cap for

[00:25:41] Alex: a day,

[00:25:42] Tony: fair enough.

[00:25:43] Alex: minus, um,

[00:25:44] Cameron: I

[00:25:44] Alex: extra ticket costs, but, oh well.

[00:25:46] Cameron: I

[00:25:47] Cameron: I knew, I

[00:25:47] Cameron: liked you, Alex. That’s exactly how I feel about things. I didn’t, I didn’t go to my high

[00:25:54] Cameron: school

[00:25:55] Cameron: prom. I was like, really? Why would I want to do

[00:25:58] Cameron: that?

[00:25:58] Cameron: I’m going out to dinner with my [00:26:00] girlfriend.

[00:26:01] Alex: I was prom queen, so what can I say?

[00:26:03] Cameron: Wow. Prom Queen. Wow. I bowed down. We’re not worthy. Wow.

[00:26:12] Alex: thank you.

[00:26:13] Cameron: Do we have photos? Do we have photos, of that? Do I have a photo of that somewhere?

[00:26:19] Cameron: Have you ever sent me a photo?

[00:26:20] Tony: I will

[00:26:21] Alex: I’ve got

[00:26:21] Alex: photos, yeah. I should say I wasn’t like some extremely popular person in high school. I just was in a steady relationship. So everyone decided to vote for us.

[00:26:30] Alex: It was the easiest, least controversial pick for

[00:26:34] Alex: prom queen and king.

[00:26:38] Tony: Yes, you were the compromise candidate. It’s always a good place to be in

[00:26:41] Alex: Yes.

[00:26:41] Cameron: The safe bet. Yeah.

[00:26:45] Cameron: Well, do you have a

[00:26:46] Cameron: question

[00:26:46] Tony: Anyway, so I seem to remember from high school and university in Toronto,

[00:26:50] Tony: Dean’s List was

[00:26:51] Tony: the

[00:26:52] Tony: top 10%, I think, of graduates, wasn’t it?

[00:26:54] Alex: what it was

[00:26:55] Alex: when I was in

[00:26:55] Alex: high school. Um, some people have said it’s the top 1%, [00:27:00] I doubt that. Some people say it’s the top student from the graduating class, um, which could be true, I don’t

[00:27:06] Alex: know. Uh, but I’m happy about it, so that’s

[00:27:09] Tony: wonder how RMIT, I

[00:27:11] Tony: wonder how RMIT, feels when they call out who the top

[00:27:14] Tony: student was and she said, I

[00:27:15] Tony: can’t be

[00:27:16] Tony: buggered buying a gown for 200 bucks

[00:27:18] Alex: I hope that they have some serious reflection, is what I hope they

[00:27:22] Cameron: and and she doesn’t even know what it means or care very much by

[00:27:25] Cameron: the sounds

[00:27:26] Cameron: of it. She’s like, yeah, so?

[00:27:28] Tony: Well, that’s

[00:27:28] Tony: good you didn’t turn up,

[00:27:30] Tony: you probably would find out what it means

[00:27:31] Tony: if

[00:27:31] Cameron: Yeah. If they, If they, they, stood up and said, and everyone welcome Alex Kynaston to the stage. And they’re like,

[00:27:37] Cameron: Alex?

[00:27:39] Alex: You’re right. Next time I’ll send a proxy or something. So at least someone’s there

[00:27:43] Cameron: Like Marlon Brando

[00:27:45] Cameron: sending a little feather

[00:27:47] Cameron: to the Oscars.

[00:27:47] Alex: Yeah. absolutely. I rewatched that recently. It’s great.

[00:27:50] Cameron: make a,

[00:27:51] Cameron: speech saying, uh, you know, protesting

[00:27:53] Cameron: something, racism, yeah.

[00:27:58] Cameron: And she wasn’t even Native

[00:27:59] Cameron: [00:28:00] American, right? She was a fake Native American who got up and

[00:28:03] Cameron: protested, uh, racism

[00:28:05] Cameron: and the treatment of the Native Americans.

[00:28:08] Alex: Was she?

[00:28:09] Tony: And so next year they had a

[00:28:11] Tony: Indian Actress

[00:28:12] Tony: Award for best

[00:28:14] Tony: performance by a non Indigenous person.

[00:28:18] Cameron: I think that’s the story. Don’t call me to that. All right. You got a

[00:28:22] Cameron: question

[00:28:22] Cameron: for us this week, okay?

[00:28:25] Alex: Yes. I was reading through Dave’s question and I decided to leave

[00:28:28] Alex: that to you two. So I’m going to read Jim’s.

[00:28:31] Tony: Okay.

[00:28:32] Cameron: Right.

[00:28:32] Alex: Um, so Jim says, Hi Cameron, I hope

[00:28:35] Alex: You are well. Can I request to pull pork on two interesting companies currently on the buy list, which are ERD, E Road Limited, and CXO, Core Lithium Limited.

[00:28:46] Alex: Not sure if multiple requests are a good form. Um, would also love to hear Tony’s thoughts on. the potential Woodside and Santos merger. In closing, thank you both for creating a wonderful platform, and I know it is early, but Merry Christmas to and yours. Cheers, Jim.[00:29:00]

[00:29:00] Cameron: Thank you, Jim.

[00:29:01] Tony: Uh, well, I’ve got two pulled porks

[00:29:04] Tony: ready to go on those companies.

[00:29:05] Tony: would, would you believe I spent like three hours

[00:29:08] Tony: doing pulled porks and I haven’t looked at the Woodside

[00:29:10] Tony: Santos Mergers? I can’t answer that

[00:29:13] Cameron: Okay, so just

[00:29:14] Cameron: Pulled

[00:29:14] Tony: ha ha ha. You just pulled pork. Sorry about that, Jim. I can hold it over until the new year and

[00:29:19] Tony: do it

[00:29:20] Cameron: Will it be relevant then? Probably.

[00:29:23] Tony: Yeah, well, I don’t think the merger’s going ahead just yet,

[00:29:26] Tony: so it should still be relevant by then.

[00:29:27] Tony: So this, this was requested by Jim. It’s a pulled pork first. There’s two pulled porks, first of all, on Core Lithium and then on E Roads.

[00:29:35] Cameron: Actually folks, Cameron, in the editing booth here. Tony recorded three pulled pork’s today. It seems like a little bit overkill to put them all in the one episode, particularly when I’ve got to do a couple of episodes without him over the next couple of weeks we’ll do a Core lithium today and then I’ll save the others for the next couple of weeks.

[00:29:55] Cameron: So you have something to listen to. Over Christmas.

[00:29:58] Tony: Um, and I [00:30:00] have to

[00:30:00] Tony: say Uh, they may have been on the buy list recently, but they’re both just off the buy list at the moment. So bear that in mind if people are listening to this, they should do their own research.

[00:30:11] Tony: Starting with Core Lithium, which is a Northern Territory Lithium explorer and now miner. They’ve started to export mine into China. Uh, their, their biggest, well, their Their big project, which is just getting into operational status now, is the Finis Lithium

[00:30:31] Tony: project, which is just south of Darwin, about 88 kilometers south of Darwin.

[00:30:36] Tony: So that’s a, that’s a bonus for them because they’re not running an hour outside of the

[00:30:41] Tony: port of Darwin, which is where they need to export their stuff. So that’ll be a cost saving for them rather than being in the middle of the Western Australian

[00:30:49] Tony: desert or something and having to build a rail link to the port.

[00:30:52] Tony: So that’s good. Um, They have already signed off take agreements with two large Chinese lithium companies, [00:31:00] Sichuan Yahua and Ganfeng, Ganfeng Lithium, both of which I’ve never heard of.

[00:31:07] Tony: But, um, it’s always good for a miner to have an off take agreement, so it’s guaranteed sales. Uh, they’re also growing because they, uh, Progressing a second tenement area known as BP33, which may end up being bigger than Finis.

[00:31:25] Tony: And that’s not too far away from having a go no go decision on developing a mine. So, they should, they should grow if that goes through, or they will grow if that goes through. And they’re going to grow anyway because they’re going to, this year, The latest figures don’t have much in the way of sales, so as they ramp up the mining at their current tenement, their sales will increase as well.

[00:31:48] Tony: A couple of things about Core Lithium. They’re a small company. They’ve adopted an interesting style of mining, so they They talk about having a [00:32:00] lot of little mines in close proximity to each other rather than one big mine. Um, that may or may not work out, but it’s a little bit different to how we normally expect a mine to look.

[00:32:11] Tony: Um, they famously turned down an off take agreement early on with Tesla. So Elon Musk came knocking, uh, before these Chinese off take agreements were secured. Uh, and they talked for a long time. The market went crazy on the fact that You know, Tesla were interested in a small Australian company, which didn’t even have a mine operation, I don’t think, at that stage, or was in the stages of doing that.

[00:32:35] Tony: Um, but they couldn’t come to an agreement, and I think Tesla’s had a bit of history of going into startup mines to do deals at low prices, and so it didn’t come to an agreement. When that didn’t happen, the share price went down. There is a bit of a premium if you can get a big customer like Tesla on the books.

[00:32:59] Tony: All of the [00:33:00] ESG investors tend to look at you even more so, although they look at all lithium companies. A couple of other things about this one. It’s one of the most heavily shorted stocks on the ASX and it currently has 12 percent of its shares shorted.

[00:33:14] Cameron: Hmm.

[00:33:15] Tony: The price for this company has dropped dramatically.

[00:33:17] Tony: Since August 2022, which was its high point, it’s down from 1. 40 to 0. 31. Having said that, it still remains above its buy line, so that’s in its favour, even though it’s a falling knife. Um, this is probably a chicken or egg situation, I’m not sure whether the share price is down because it’s being heavily shorted, or because it’s down because the shorters are paying attention to the lithium price, which is also down dramatically in a similar sort of period.

[00:33:48] Tony: Its high was 600, 000 a tonne in November 22, and the lithium price is now down to below 100, 000 today, around 97, 500. So um, It’s [00:34:00] down dramatically as well. I suspect the mining companies are following the commodity prices. They usually do. So that’s why the price is down. Um, but one of the positives for this company is that if the lithium price does look like improving and turning around and the short sellers will probably All have to do what’s called a short cover, sell their stock and give it back, otherwise they don’t lock in their profits, in case the core price takes off, but just that process of um, of getting out, because what they actually have to do is buy the core stock to return it to the people they borrowed it from, because if you’re shorting, you borrow the stock, sell it, and then buy it back at the bottom and give it back to the person you’ve been You’ve rented it from in the first place and that generally creates a bit of a price spike just just that process alone and and if 15 percent of the stock has to do that, we might

[00:34:53] Tony: see

[00:34:53] Tony: it turn around.

[00:34:55] Cameron: I think it’s known as a miniskirt, Tony.

[00:34:57] Cameron: Short cover. [00:35:00] Keep going.

[00:35:01] Cameron:

[00:35:01] Tony: yeah. Uh, so the numbers for this pulled pork, um, This is a large ADT company of nearly 6 million, so that’s a positive. The share price when I did the analysis was 0. 305 per share, less than consensus target, and almost IV2, 03, IV2 is 0.

[00:35:26] Tony: 29, so not quite. Below IV2, but fairly similar. Doesn’t have a yield because as you’d expect with these sort of startup mining companies, all of their cash flow goes back into setting up the operations and expanding. Stock Doctor give this company financial health of strong and a trend of recovering, which we like to see.

[00:35:49] Tony: So it gets a good score for that. Uh, if we were scoring on PE alone, we’d get a bad score because the PE is 51 times, um, and therefore it fails our test, [00:36:00] uh, for the last, uh, three years, but, um, that should turn around because it’s expected to grow. Uh, the earnings are expected to grow next year. Um, having said that though, price to operating cash flow is 7, just over 7 times, 7.

[00:36:14] Tony: 23. So it’s just off the bottom of our buy list. But again, that could turn around with a, um, fluctuation in the share price, if that happens. Net earnings per share is 16 cents, uh, so it doesn’t score. For us on that basis, book plus 30 share price is just over 0. 30, so we can’t score it based on its assets.

[00:36:38] Tony: Earnings per share forecast growth, however, is 400 percent and that’s due to the mine ramping up. So growth over P. E. is nearly eight times, which is way above our threshold of 1. 5, so it scores well for that. Uh, interestingly enough, no owner, founder, directors hold 1 percent that I could see anyway. So I can’t score it for that.

[00:36:58] Tony: Sometimes you do see that in [00:37:00] these small mining companies, but not the case here. Uh, equity is consistently increasing. So it gets a tick for that. So all in all, the quality score is 9 out of 14 or 64%. And the QAV score is 0. 09, which is just below our cutoff of 0. 1. Having said that, I mean, the 0. 1 is arbitrary.

[00:37:21] Tony: So if someone did like this company and wanted to buy it they could look at it at 0. 09 I would have thought but it is a falling knife at the moment so I wait until sentiment turned. I suspect when sentiment turns it’s going to turn strongly because the short sellers will be buying stock to give back to their lenders.

[00:37:38] Tony: And it’ll kick off quite nicely. So that’s a positive for it when it does eventually turn. Negatives and, well, risks, I guess. Um, the lithium price is probably the biggest risk. It’s still depressed and trending down. And I’ve seen this before with, with, um, mines and commodities. Uh, it’s a commodity that a couple of years ago was in high demand, largely [00:38:00] because of its role in electric vehicles and other electric.

[00:38:03] Tony: Um, uses, electrification uses, uh, so it meant the players who are already in the field did really well, but it also invited lots of new mines to, or lots of mining companies to explore for lithium. And so there is, um, uh, more lithium in the market now, so that’ll settle down to an equilibrium that works out in the long term and is economical for, um, most parties.

[00:38:27] Tony: But at the moment it’s, um, it’s now in oversupply. Other risks, um, probably the other biggest risk I can think of is that there has been noises made, um, in Australia, but also in the U. S. about, uh, exporting, um, certain minerals to China, and, uh, the two off tank agreements this company is relying on are both in China.

[00:38:53] Tony: Now, the government hasn’t come out and said that they have a policy against sending lithium to China. I think they have [00:39:00] called out some certain minerals to China. To, um, regulate exports overseas, but I don’t think the theme’s on that list yet, but it may happen if they decide to expand their, their, um, regulations of, uh, of, uh, Precious minerals too, or minerals that aren’t freely available to China.

[00:39:20] Tony: So, um, yeah, it’s, I think it’s a watch. I’ll be watching the lithium price before I bought into this one, but, um, longer term it probably should do okay. So that’s core. And I mean, again, before I leave core lithium, it was only a couple of, maybe even a year ago that, um, at least, at least one friend, couple of friends approached me and said, You know, I’ve been told I should get into lithium.

[00:39:45] Tony: It’s the next best, biggest thing. And it was a boom and it was, the price was up dramatically and companies were, um, mining lithium and their share price had gone up four or five times. Um, and of course that was right about the time that lithium peaked [00:40:00] and started to drop and it’s dropped, uh, five sixths of its, to five sixths of its price, so it’s dropped a long way down from that high.

[00:40:07] Tony: It’s the old classic proverb, when the, when the tip hits the retail market, you hear it from people who don’t usually. Buy stocks, it’s the time to get out.

[00:40:16] Tony: So, that held true in this boom, but lithium boom, it holds true in most booms.

[00:40:21] Cameron: yeah, I think my sister was one of those people. One of my sisters said to me, Hey, uh, what do you think about investing in lithium? I’ve heard lithium’s the place to be. Probably from somebody at a church. I said, yeah, yeah, be careful with that.

[00:40:43] Tony: yeah, so it’ll probably have its day again, but at the moment it’s, it’s depressed. So that’s Core Lithium.

[00:40:50] Cameron: Thank you TK.

[00:40:51] Tony:

[00:40:51] Cameron: Alright, that was really good. Um, don’t own CXOs, I’m not worried about the pulled pork curse on that,

[00:40:59] Cameron: [00:41:00] Uh, let’s Look at other questions. Dave from Newey. I got to apologize. Dave sent me this a couple of weeks ago and it got lost in my emails.

[00:41:10] Cameron: Hi Cameron, hope you’re well. Was hoping I could ask for a pulled pork with a twist. My dad has been talking about REITs for most of this year. It’s a quiet morning here in Newey, so I did a deep dive on the sector. Gee. There is some value starting to come through. A bunch of them have bounced off 5 year lows and are down 30 50 percent over 3 years.

[00:41:33] Cameron: The 11th of December scorecard is nearly all of the REITs with a score between 0. 01 and 0. 07. URW is the only buy and it’s been on a stellar run the last little bit on big volume. Disclosure, he owns it. Could Tony pull apart one of the REITs, e. g. CMW, ECF, COF, and use the numbers to help understand the following.

[00:41:58] Cameron: What will it take to get a basket of [00:42:00] REIT buys coming through on the QAV list? Price alone? Or is the quality forever going to hold them back? Are REITs like banks? Rather than putting money into an REIT, would an investor be better off buying the parent company, assuming listed, e. g. Charter Hall, CHC?

[00:42:19] Cameron: Stock Doctor has a good write up of risks on the CHC 9 Golden Rules page. In short, Occupancy versus work from home thematic, bond yields rising impacting competition for investing dollars, costs of money for REITs with flow on impacts to yields. Any other obvious risks the financial analysts have missed?

[00:42:40] Cameron: I’ve been sniffing around commercial property here in Newy in the Hunter recently. Prices have gone significantly higher, so yields at present are below the norm. I don’t get why prices are higher when interest rates are higher. Maybe the smart money has moved from the lower yields compared to interest rate expense in residential to commercial, therefore driving up [00:43:00] prices.

[00:43:00] Cameron: So how does this all play out in sentiment terms? 1. Interest rates peak and decline, so dividends can rise and REIT prices start getting bid up again. 2. Commercial property prices correct. which returns yields and dividends back to normal levels. There was a sharp jump in price in some of the REITs after the US Fed said last week that they were now forecasting rate cuts in 2024.

[00:43:24] Cameron: Seems a classic contrarian opportunity coming up, but I’m confused as always. And would appreciate Tony’s perspective, as always. Off for a battered QAV, Dave from Newey. A battered QAV. I like that.

[00:43:39] Tony: A battered QAV.

[00:43:41] Cameron: Uh, wow. All okay. All of

[00:43:43] Cameron: that’s

[00:43:43] Tony: Yeah. Gosh. I think, I think Dave, Dave may have exhausted his number of questions for a little while too. We could probably do a whole show on REITs, but I’ll I’ll go through and answer these. Um, [00:44:00] so answering his questions first, and then I’ll do the pulled pork. What does it, what will it take to get a basket of REIT buys coming through on the QAV list?

[00:44:09] Tony: Well, I think it will be, um, rice, because I guess the business structure of the REITs is there, so let me go back, let me explain what an REIT is, um, which is probably a good way to start, um, it’s a real estate investment trust, and they’re basically just a way of buying into large chunks of of commercial property that individual investors, retail investors, probably wouldn’t have the funds to do by themselves.

[00:44:45] Tony: So it’s a real estate investment fund, basically. It’s a managed fund that invests in real estate, just like there are managed funds that invest in the ASX and other commodities, etc. And it’s usually a trust [00:45:00] structure, which it doesn’t have to be, but it generally is. And the benefit of a trust structure is that If, uh, if a trust distributes, um, more than, I think, 90 percent of its income or profit, then it doesn’t pay tax.

[00:45:13] Tony: The tax is paid by the recipient of the trust, just like a family trust. That’s how a family trust works. Um, you know, if you have shares that are, that are, um, invested in the family trust, then the dividends can be distributed to, um, a member of the, a recipient of the trust, so someone who’s in the trust, a member, but it can be diverted to the person with the lowest income.

[00:45:35] Tony: So like a, if, if you’re a, um, a couple and one person’s at work and one person’s at home, you can distribute the profits to the person who is at home and they pay tax based on their marginal tax rate, which is lower than the person who’s at work usually. So, um, that, that’s the benefit of a trust structure.

[00:45:54] Tony: It doesn’t pay tax until it gets to the, um, the trust unit holders, um, [00:46:00] hands and then they pay tax, uh, on that, which makes, makes it attractive to SMSF. Uh, holders, because superannuation taxation is light compared to personal taxation. So, if the trust doesn’t pay normal corporate tax rates and the unit holder is paying superannuation tax rates, which are usually 15 percent or zero after retirement, um, it could be a tax free income to someone.

[00:46:26] Tony: So, REITs have traditionally been, um, purchased by people as a retirement income. Um, for that reason, it can be either lowly taxed or tax free, but also because Uh, the yield on property, um, when it’s, you know, a well managed fund can be high. So sometimes, you know, some of the, some of the names that Dave has talked about are paying up to 10 percent yield and that’s tax free.

[00:46:55] Tony: Now, because it’s going through a trust structure, there’s no franking credit attached to it because there’s been no tax [00:47:00] paid on it. Um, uh, so it might be a 10 percent yield, but you’re not getting a franking credit. However, if you’re in a Retirement phase pension in your super fund, then you’re not paying any tax anyway, so it’s 10 percent you’re getting tax free and that’s attractive both for the income side of things when you’re retired, but it’s also, if you think about it, um, you know, throwing a bit of capital growth in the fund, which, you know, property prices Go up in the long term, you’re actually beating the market, being the, um, the ASX, which generally gets about 10 percent over time.

[00:47:34] Tony: So it’s a good way to invest depending on tax structures and depending on your need for yield or not. Even if you don’t need the yield, you’re paying little tax, you can always reinvest the yield back into the fund and, and buy more units or more shares and you’re still getting a Um, a pretty good return, uh, with exposure to commercial property, which goes, like I said, goes up in the long, in the long term.

[00:47:58] Tony: However, it [00:48:00] does, it can still be a little bit volatile and, and the area that’s volatile at the moment and has been depressed has been office, um, Office real estate and office real estate front funds. And that, that’s maybe what Dave wants me to focus on because he mentioned CMW, ECF and COF, and they’re all three office funds, um, which have been depressed lately because of the work from home trend following COVID.

[00:48:26] Tony: Um, that’s not the case across the REIT section, however, I hasten to add there are REITs, which, um, for example, own Data Centers, and they’ve done spectacularly well in the last couple of years because that’s a growing area. There have been REITs that house, uh, that own warehouses. Which I’ve also done well because of the trend, especially during and following COVID, to deliveries, home deliveries, so there’s more, um, electronic or e tailing activities going on, electronic retailing activities, and so those, those, [00:49:00] uh, REITs are doing well.

[00:49:04] Tony: So there are REITs for everything, and as Dave Um, called out, there is one on our buy list, which is URW, Unibail, Redamco, Westfield, which is the old international division of Westfield, if you can think about all the shopping malls around the world that badge Westfield. And I think Unibail and Redamco also had some other ones as well.

[00:49:22] Tony: So that’s a, um, a shopping centre trust. And, um, it’s now doing well as we’ve come out of COVID and people going back to shopping malls, but for a while there it was doing poorly, which is why it came onto our buy list. And to get back to Dave’s answer, if you think about the structure of these things, um, they’re, they’re, even if they’re yielding 10%, um, which, which means they’re, Uh, well, what am I trying to say?

[00:49:55] Tony: They don’t come on the buy list often because we have a price to operate in cash flow threshold of [00:50:00] 7. So, which means I’ve got a, that the property has to, on a net basis, be returning 14 percent because 1 over 7. Is is roughly 14 bit over 14. Um, and that’s on a net basis. So not only do they have to find property, which is has rental yields above 14%, it’s also gotta be after their costs, um, and borrowings.

[00:50:23] Tony: And, um, these funds can contain borrowing. So it, it does happen that you get either price, depression in the fund. Life happened with URW, um. or you get some fantastic real estate which has gone up and is yielding say 15 to 20 percent and therefore the PropCaf Compare to the share price can get above our seven times threshold, but generally the REITs don’t, don’t do that.

[00:50:48] Tony: So they don’t appear on our buy list usually. Um, so it’s generally an extreme situation. Now, a couple of these that Dave talked about are getting up close to the buy list. And, um, [00:51:00] you know, the, uh, CMW, Cromwell Property is currently a score of 0. 08. And ECF, um, Eleonora. Commercial Eleanor office is now up at 0.

[00:51:11] Tony: 07. Um, so they are getting close and, and I think, um, it’s possible that the manual, manually entered data hasn’t been updated for those for a while, so they could even be close to the buy list. Um, but generally some of the other ones I spoke about, so the big ones like Goodman, GMG, which um, is, is basically warehousing and has done well because of that.

[00:51:34] Tony: Uh, their QAV score is like 0. 01, but they are a buy on the, on the bread later for sentiment. So, um, that’s the thing. Um, other big ones, Dexus has a score of 0. 04. Um, it’s close to a buy on the bread loader, but the price is still below its sell, uh, price. Um, GOZ is 0. 03, Vicinity, which is a shopping center one, another [00:52:00] shopping center one, a local one, is 0.

[00:52:02] Tony: 03, Charter Hall, 0. 03. So that’s generally about where they, they fall because of the fact that they can’t get above our PropCaf of, of, um, seven times or less than seven times. So I guess that’s something to, to notice, um, to answer Dave’s question about why we don’t see many REITs. On the buy list, that’s the first thing.

[00:52:21] Tony: Um, he talked about, are REITs like the banks? Rather than putting money into a REIT, would an investor be better off buying the parent company? Assuming it’s listed, Charter Hall being one of those. So generally you’re better off buying the parent company, the manager of these things, rather than buying the fund.

[00:52:39] Tony: But it depends on your needs. So the funds suit people who want a retirement income or a high dividend income and have a situation where they’re not paying much tax. Um, but for growth, you’re better off usually buying the manager, because their fees go up over time as these, these companies or trusts grow.

[00:52:58] Tony: Um, I’m not [00:53:00] 100 percent sure Charterhall is just a straight manager, but it could be. I’m not familiar with it. But that’s generally what you need to do. So the yield on Charterhall, for example, is much lower than the yield on some of these other listed REITs. Uh, to paraphrase Dave, he’s asking about what are the risks of, um, of these REITs, including Occupancy versus work from home, bond yields, cost of money, etc.

[00:53:27] Tony: The biggest risk that he didn’t mention is is revaluation risk and this is one that I think is is hurting the office trust. It generally works in favor of office funds. It’s often called out as an abnormal, but we really should be taking into an account the fact that, uh, profit is impacted by these funds revaluing their, their portfolios every, usually every half, I guess, but sometimes annually, um, or periodically anyway.

[00:53:58] Tony: And so what they love [00:54:00] doing is to say that, look at us, the office buildings or the warehouses or the shopping centers we’ve invested in are now worth more than they were this time last year, and so we’re going to put that as a valuation increase on the assets, but to do that we have to put it through the profit and loss account, and so that’s what Historically supported the P& L of these companies, even though it’s often treated as abnormal.

[00:54:24] Tony: That depends whether you look at, you know, standard or, um, normalized or abnormal, um, profit for these companies. Uh, in the case of office funds at the moment, it’s, it’s, it’s hurting them. for the same reason. So, you know, it’s, it’s now being called out as an abnormal or highlighted as an abnormal. It’s not usually highlighted, um, when things are going up, uh, it’s just treated as part of the profit.

[00:54:47] Tony: Um, but it’s me being cynical, but yeah, so, uh, Office buildings are generally being written down because of the work from home trend, especially in the CBD. And [00:55:00] so that write down of asset valuations is knocking out the profit of some of these companies that, or some of these REITs that Dave spoke about.

[00:55:08] Tony: So that’s an issue that you should pay attention to, I think. Can’t really comment on Dave’s question about commercial property and Newcastle as to why it’s going up and I’m not sure whether when he refers to commercial property if he’s referring to offices or factories or something else but certainly everything other than office buildings have been going up and office buildings in regional areas haven’t been too bad because It’s really the CBD offices that are being hurt by the working from home trend.

[00:55:40] Tony: Um, perhaps they are in Newcastle, but it’s also probably the case that people going into work at Newcastle don’t have the kind of commute that people going into the CBD office in Sydney from the outskirts do, so it may not be as much of an issue. And certainly one of the ones that I’m going to go through and for a pulled pork has called that out as being a a benefit of their [00:56:00] fund is that it has more, um, or less CBD office spaces than some of the other funds.

[00:56:04] Tony: So that could be why. The commercial prices are going up in Newcastle. Uh, interest rates, you’re right Dave, interest rates will have an impact on these. Generally, the trusts aren’t overly geared. Um, it’s usually a reasonable amount of gearing, 20 to 30 percent perhaps, maybe 40 in some cases. So, they should be able to handle interest rate rises, but it’s going to be an issue.

[00:56:29] Tony: Um, you spoke about comparison to bond yields. That’s always an issue for these companies because, um, REITs are often called a bond proxy, which I’ve spoken about before. They’re companies which pay a yield, which, um, uh, people can get into easily because they’re listed, um, and sometimes easier than buying a bond, which, um, often aren’t listed, but they are in, in the same markets.

[00:56:52] Tony: Um, so they do try and, um, compare themselves to bond yields. And if bond yields are going up, which they have [00:57:00] been, then the, the yields on these, the dividend yields on these trusts have to as well. Um, He spoke about the REITs going up in value after the U. S. Fed last week because we’re people are now forecasting rate cuts in 2024 and that certainly, again, goes back to this theme of comparison to bond yields and interest rates being an issue.

[00:57:22] Tony: So, yeah, um. His last question, he talks about, uh, he asked a question about, um, looking at these things without using the buy list and, and so first of all, like, so how would you look at these REITs and decide which ones to buy and not to buy? Um, first of all, look at sentiment, so the bread loader will still apply to these, um, Trusts, even though they’re not on our buy list, it’s still, they still are subject to sentiment.

[00:57:54] Tony: Um, and they’ve generally been turning up as Dave has highlighted, um, probably because interest rates look like they may not [00:58:00] rise much further. Um, so the first thing I do in terms of buying REITs is to still use the buy list. So UIW is the clearly stand, the standout one for me. Um, but another one which is traditionally used in this area is to buy them when they’re priced below their NTA.

[00:58:19] Tony: And so, uh, That’s the case with the office funds at the moment, and it’s both good and bad, but it’s still a buying opportunity, so people are paying less for these unit trust prices, the REIT prices for the office funds, because they think that the, the offices haven’t been written down far enough, so again, that’s always been an issue with these things, they’re, they’re The office buildings are independently valued, and there’s certainly professional companies who do that, um, but the question is always whether they’ve been written down far enough, um, and, and, you know, what kind of metrics have been used to do that?

[00:58:59] Tony: [00:59:00] Because there weren’t many sales during COVID when the, when the, um, Office buildings were empty. And of course, because the office buildings are depressing in price, the only sellers at the moment are four sellers. People are tending to hold on to them for longer. So it’s hard to get comparables or enough comparables to make a meaningful decision.

[00:59:20] Tony: And therefore, the investors in these REITs are questioning whether the office buildings have been written down far enough. And, but that’s a buying opportunity because we can, um, Buy them below what the independent experts have priced those retail buildings at. So we’re buying them for less than NTA, which I think is another way to treat these.

[00:59:40] Tony: A bit like buying LICs when they have a discount to their NTAs. So you’re paying 80 cents in a dollar for um, For office buildings, which is not a bad thing to do, because eventually I think they will, the situation will ride itself. I don’t think the CBD buildings are going to go to zero. Um, companies are forcing [01:00:00] more people to come back to work and, you know, probably through a leasing cycle.

[01:00:03] Tony: They’ll work out that they may or may not need less leasing space, but it will sort itself out as these trends often do. So that’s my comments on REITs.

[01:00:13] Tony: Dave, I hope that answers all your

[01:00:15] Tony: questions.

[01:00:16] Cameron: Cameron in the editing booth again, at this point, Tony did a pulled pork on COF Centuria office REI T. But again, I’m getting a, hold that back for some time over the next couple of weeks. We, I seem to recall, we had some issues with buying URW a while back. It’s, uh, a CDI out of France, and there was a French tax. Some brokers wouldn’t let you buy it, some would. I think Dave said he got it via SelfWealth with no issues. I think Steven Mabb bought it using one of the brokers, but some other people had troubles.

[01:00:53] Cameron: I ended up just putting a note in my buy list that it wasn’t something we could really look at because it was too, [01:01:00] um, I don’t know, difficult to get your hands on.

[01:01:05] Tony: Yeah, right. Which could also be depressing the price, which is why it’s on the

[01:01:09] Tony: buy list.

[01:01:10] Cameron: Um, uh, getting back to, well, talking about this broader issue of work from home, I read Chanticleer’s article in The Fin this week. They did their survey, their CEO survey, and it was one of the big issues, and it seemed, I mean, their conclusion was, uh, people, work from home is here to stay. It seems about half the week.

[01:01:30] Cameron: A lot of major companies have sort of accepted somewhere between two and a half to three days a week is where most companies are landing. It’s where they think employees are going to be. They seem to be trying to sell them on the fact that being in the office is good for career development. Um, don’t know.

[01:01:49] Cameron: I haven’t worked in an office for 20 years, so what do I know? But that sounds like bullshit to me. Uh, but I’m trying to figure out, like, when people are writing down the value of these offices, what do they [01:02:00] think’s going to happen? That these corporations are going to decide that they need less space because they’ve got less people in the office full time.

[01:02:08] Cameron: But the buildings aren’t going to go empty, right? There’s gonna Find other uses for those buildings you would expect. Is it just that the revenue might not be as high as selling it to corporates for offices and, uh, their revenues would take a hit?

[01:02:25] Tony: Yeah, I must admit, I would have thought this would have played out more extremely since COVID. That was my sort of hypothesis. Because if you think about it, I think you’re right. I think people are only going in maybe half time. Certainly it’s different across different SME space, which Centuria seems to be servicing, but I know the bank CEOs, for example, came out and said about half their staff are in the office, um, at one time, so you’d think that would mean they’d be getting rid of.

[01:02:56] Tony: Leasing space, um, or trying to sublease it. [01:03:00] So that to me says that when these leases come up for renewal, they won’t renew. And they’ll manipulate their portfolio over time to get out of spacing, get out of space. Whether that means the rents come down because there’s going to be less demand for, to, you know, when they go out to relist, when the REITs go out to relist, release these.

[01:03:22] Tony: Office spaces, or whether it means that people just aren’t building new office buildings, and that soaks up the lack of demand. I’m not sure, but yeah, it hasn’t worked. I mean, certainly, um, these REITs have been doing terribly. They’ve come down a lot, the office REITs, um, since COVID, so it’s played out in that respect.

[01:03:43] Tony: The valuations haven’t been, I mean, they’ve been written down, but not like you saw with this one. It’s an office building REIT, exclusive office building REIT, and they only wrote down the valuations 4 percent um, this year. So, you know, whether they have some kind of scope to smooth it over [01:04:00] time or, or whether the, um, expert valuers.

[01:04:04] Tony: Don’t think it’s going to be as bad as what, you know, inexpert bystanders like you and I think it might be. But I, I tend to agree with you and certainly the buyers of the shares in these REITs do because they’re buying shares at 30 percent less than NTA, which means I think the valuation is going to come down.

[01:04:23] Tony: Um, but yeah, it’s whenever you’re buying something below NTA, you’ve got to consider it because it’s, um, it’s nice to buy assets for less than what the, the experts think they’re

[01:04:34] Cameron: governments can buy up all of the, uh, free office space and use it to house the homeless people.

[01:04:39] Tony: Yeah, I remember the last time commercial property, particularly offices, had a big downturn. I’d just moved to Melbourne. It was like late 80s after the share market crash and companies were closing and going bankrupt, downsizing dramatically. And that kicked off a boom in converting offices into apartments, which was a, you know, alternative use and successful alternative use.

[01:04:59] Tony: And I think the [01:05:00] BP building became the Quayside Apartments or Key West Apartments in Melbourne. The IBM building in Melbourne was converted into apartments. So yeah, it doesn’t mean just because people aren’t going to use the space for office work that they won’t be able to rent it out for something

[01:05:14] Tony: in time.

[01:05:15] Cameron: Yeah, it’s interesting. I’ve been trying to get my head around it for a while, why people are so negative on that whole space and what’s going to happen with it, and also why companies are trying to force people back into the office. Instead of just, like, this whole thing about, well, they network better and it’s better for career development.

[01:05:33] Cameron: Yeah, really? I mean, can’t you just say, okay, we’ll schedule Zoom calls and Zoom meetings or cafe meetings or something like that? I would have thought Coming out of COVID that offices would be jumping at the chance. Businesses would be jumping at the chance to have less people in at the

[01:05:49] Cameron: office. So they could, you

[01:05:50] Cameron: know,

[01:05:51] Tony: correct. Let’s lower our

[01:05:52] Cameron: lower the overheads.

[01:05:53] Cameron: People want to cover their own costs by working at home for their office. Like fantastic, you beauty, lower fleet [01:06:00] costs, et cetera, et cetera.

[01:06:01] Cameron: Uh,

[01:06:09] Tony: you know, I’d say, sure, come in and I’d have security meet them at the door and fire them on the spot for being lick asses and being absolutely unproductive. And political for you to hang around with the CEO. Uh, you know, and that would also be a way of, um, saving costs as well.

[01:06:28] Cameron: nice. Alright, well thanks for going over all of that. Really, it is a really interesting space, which I understand nothing about,

[01:06:35] Cameron: but I find it

[01:06:36] Tony: It is. Yeah, and it, like, because of the, these things, um, tend to be dividend yield focused and not necessarily growth focused. They don’t pop up in our investment talks much, but there is certainly a market for people who are going into retirement to, to buy these REITs, um, and get a great yield.

[01:06:52] Tony: to live off.

[01:06:53] Cameron: Alright, well, last question for the year is from Kane. Hey [01:07:00] Cam, question for Tony today. Does he have any thoughts on why BFG is having a run? I’m up more than 30 percent over the last 5 weeks. Good for you, Kane. BFG, big

[01:07:13] Cameron: friendly

[01:07:14] Tony: Well, I

[01:07:14] Tony: Bell Financial Group. Well, I’ve been on the buy list in the past. I don’t think they are at the moment because, again, they have negative cash flow for this half as well. So they’ve fallen off our filtering. Um, so I haven’t paid attention to them for a long while. Um, so I can’t, I can’t answer Kane’s question with any sort of definitive answer.

[01:07:35] Tony: All I can do is Tell you what my research uncovered, which may or may not be the case. Um, I think it looks like the share price started increasing when, uh, the executive chair retired, a guy called Alistair Provan. And I don’t think that in itself was enough to cause the share price to grow, but there was an article on the AFR.

[01:07:56] Tony: Which reported some rumors that, um, one of [01:08:00] the founders who passed away during the year and had a large stake in the company and the retirement of Alistair Provan may have been enough to kick off, um, a takeover offer for BFG, whether it would be up for sale or not. And the fact that Alistair Provan was quoted as Swatting away that rumor, mentioning it during his retirement speech to staff and saying it definitely wasn’t the case.

[01:08:24] Tony: It was kind of unusual too, because you don’t sort of do that unless there is talk about, um, offers being made for the company. So all I can put it down to is perhaps there’s some takeover speculation for this company. Um, the alternative hypothesis I would have is that Bell Financial Group is a basically a stockbroke, stockbroking.

[01:08:45] Tony: Company does have wealth management and funds management and super, um, annuation platforms and super management. But given that the market’s going up, you would, you would think that that would also, um, with a bit of a rocket under the share price of [01:09:00] BFG and any other stockbroking companies as well. So that could be the case as well.

[01:09:05] Tony: But that’s all I’ve got. I can’t really explain why. And it did have negative cash flow, which could be for all sorts of reasons with a stock broker. Uh, yeah, so I can’t say it’s, it’s gone up because of buy list reasons or QAV reasons, but yeah, it’s potentially just a bit of hype on whether someone’s going to Pounce on it.

[01:09:29] Tony: Uh, and it hasn’t been on the buy list in the past. So those, that does happen to those kinds of stocks, or it could just be that the share market’s turning around and people are starting to factor that into their forecast for a stock breaking company.

[01:09:43] Cameron: Trying to figure out when I last owned it. It’s been a while.

[01:09:45] Cameron: Had a couple of bites of BFG over the years, but yeah, they’re not on, not in any of my portfolios right now.

[01:09:51] Cameron: Well, I, I, congratulations to Kane if he’s still holding it. Um, it looks like it’s doing well.

[01:09:59] Tony: Mmm. [01:10:00]

[01:10:00] Cameron: that is the Q& A for the year, Tony.

[01:10:03] Cameron: It has been a big year, been a, been a very, um, year full of trials and tribulations for investors in the market. It’s been a very tricky year for QAV. Uh, members too, I know a lot of people have Suffered and struggled, but you know, as I said at the beginning of the show, the market has been on a tear just recently.

[01:10:27] Cameron: It’s nearly back up to its all time high. So, you know, maybe it’s, you know, good. It’s going to be a good year. We’ll see. Who knows? We can’t predict.

[01:10:39] Tony: Correct. Yeah, it’d be nice to get a year off from all of the buying and selling we’ve done

[01:10:44] Tony: this year.

[01:10:45] Cameron: Well, let’s get into After Hours. Tony, what have you been into in your, uh, you know, holidays down south?

[01:10:53] Tony: Yeah, holidaying, playing golf. Um, Jen’s there with me now, which is lovely. So we’ll be taking a real holiday from [01:11:00] tomorrow onwards. Yeah, the only thing I can report watching, I can think of, is um, uh, a documentary on Shane McGowan, who was the lead singer from the Pogues, and I should say RIP Shane, he passed away a couple of weeks ago, I think his funeral may have been last week, and um, there was Clips on various platforms of people singing at the funeral.

[01:11:25] Tony: I think Nick Cave may have sung at the funeral. Um, but I remember going to the Pogues concert when they came to Melbourne in about 1987 or 88. It was a fantastic concert full of life. It was an amazing concert. Um, and, and so yeah, this documentary came out, uh, very recently made by Julianne Temple, who, um, anybody who has my background would know was the, the maker of the, um, Great rock and roll swindle back in the day.

[01:11:55] Tony: So he’s made one called Rock of Gold about Shane McGowan. And it’s, I thought [01:12:00] it was really great. It’s not going to be everyone’s cup of tea because Shane is, um, a notorious drinker and drug taker and, um, basically drunk and drugged himself to death at a very young age. Or he’s like, he’s about my age actually.

[01:12:14] Tony: Um, Reasonably young age. Uh, but yeah, it’s great to go back and see old footage of him. Again, this whole theme of, you know, he was, the Sex Pistols took the stage and, you know, there was a small audience there and all of them went off and formed bands soon afterwards. And he was one of them. Um, interesting guy.