Hello QAVvers

It’s another Tuesday.

The AORD had a pretty good week, and it’s expected to rise again today. It didn’t help PRN yesterday though! They issued new guidance and their shares fell 8%. They recovered a little though and are sitting just below their 3PTL this morning, so I’m waiting to see what happens when the market opens.

Let’s have a look at the portfolio.

QAV PORTFOLIO REPORT

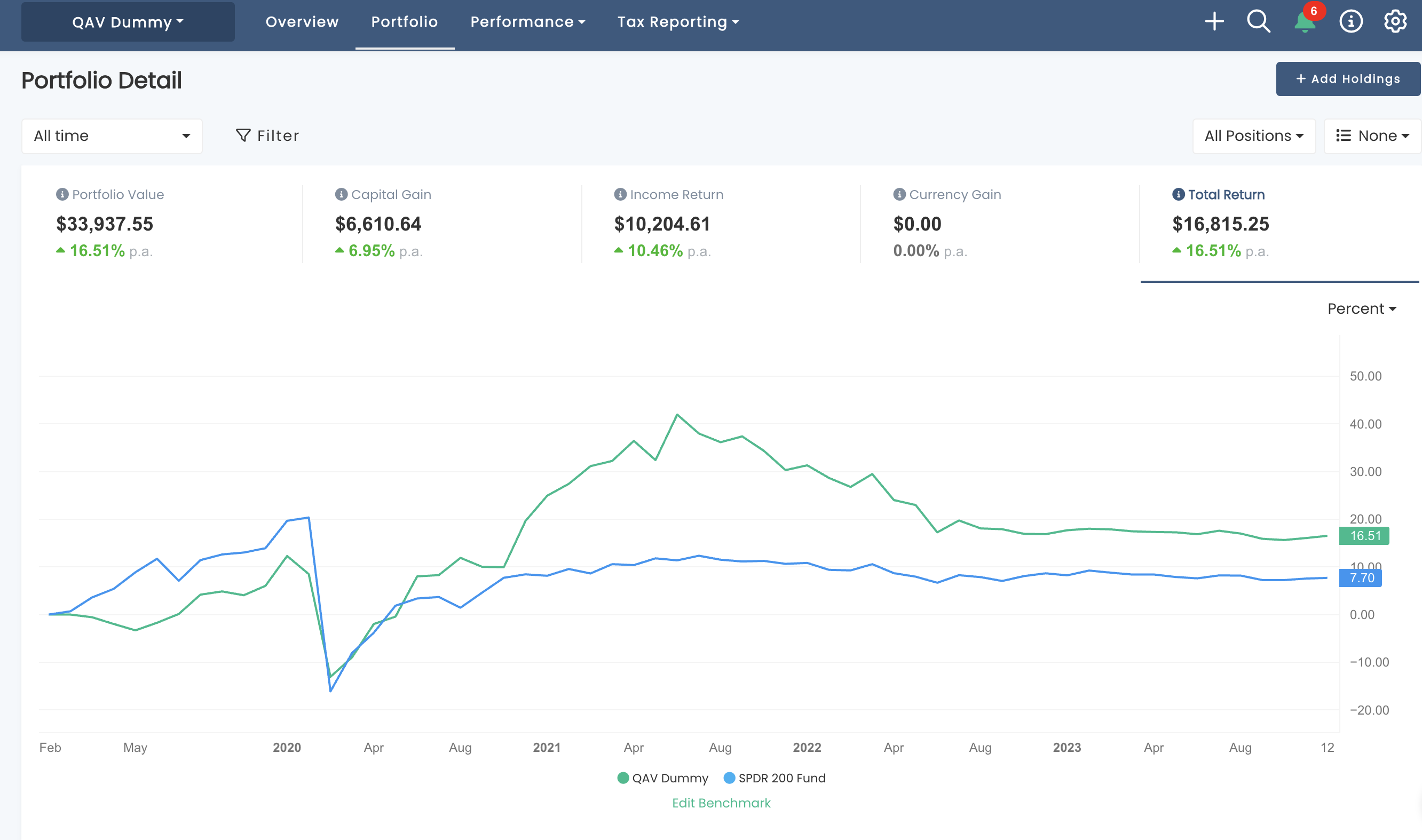

The Dummy Portfolio is performing well against the benchmark over multiple time frames.

SINCE INCEPTION (02/09/2019)

Our portfolio is still doing a bit better than double market since inception.

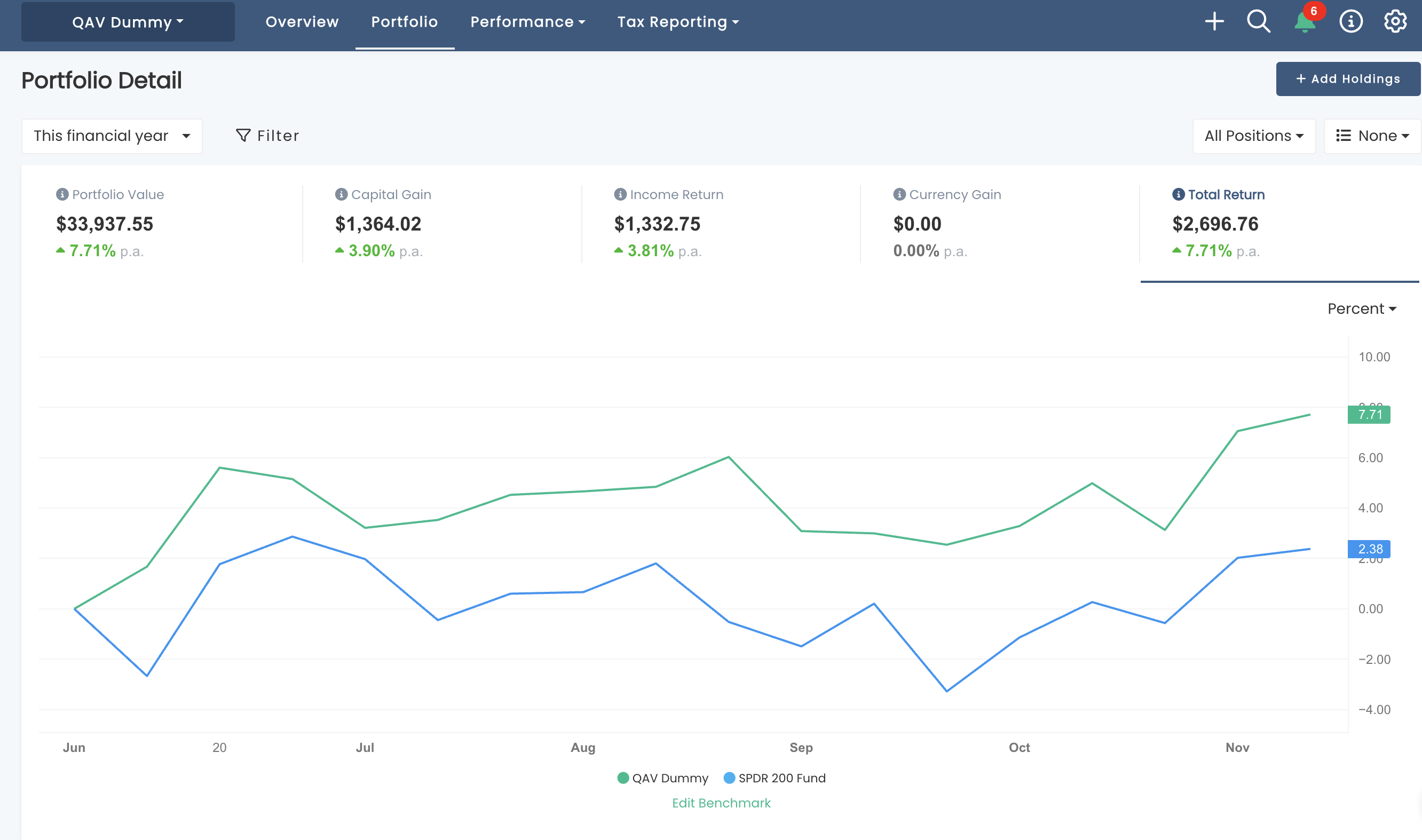

FY REPORT

For the FY we’re doing 3X better than the STW.

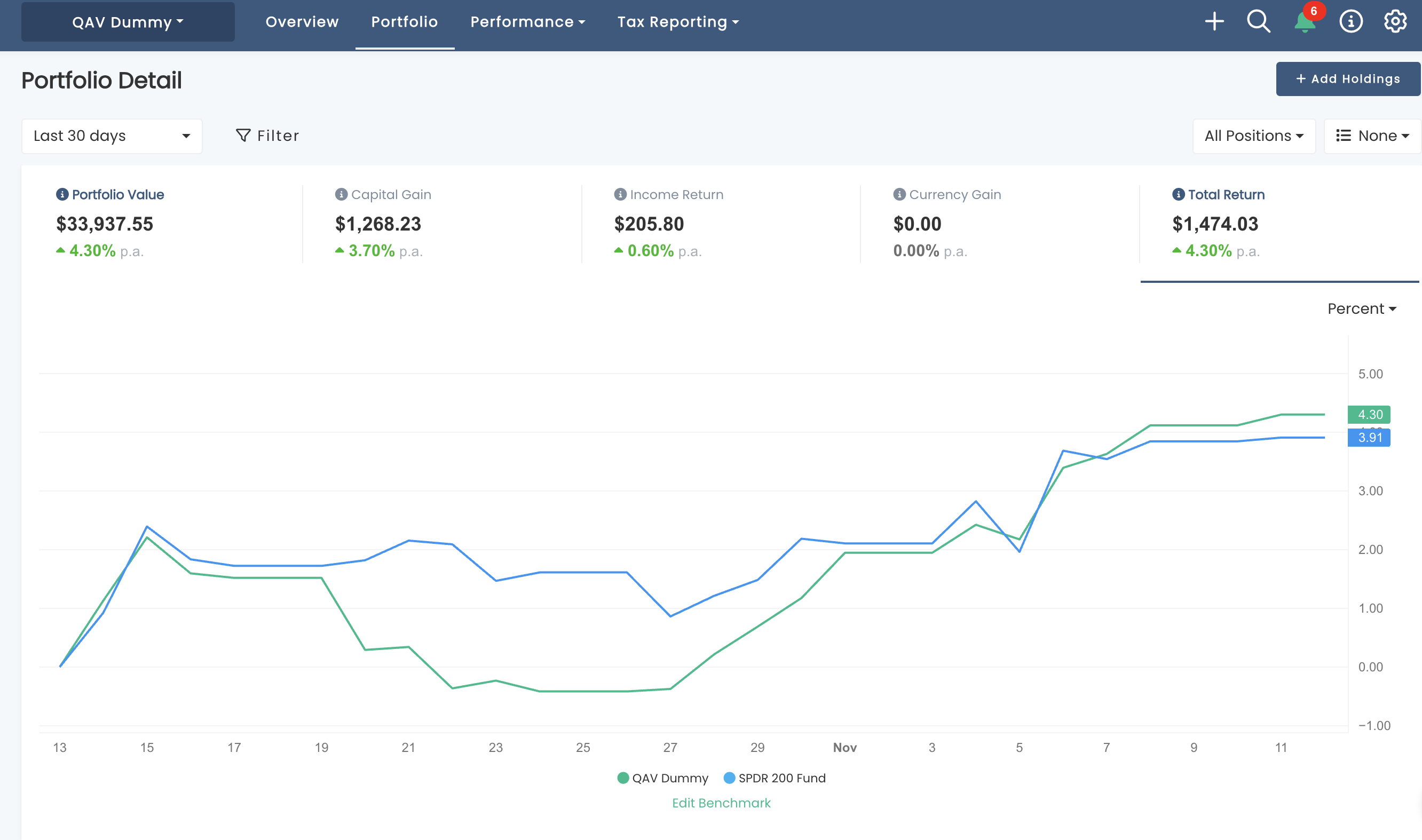

30 DAYS

in the last 30 days we’re a little better than the STW, but not by much.

RECENT TRADES

No trades in the last 7 days.

FREE WEBINAR

I’ll be doing another webinar in a few weeks.

STOCKS OF THE WEEK

During the last week, we also traded some stocks in our Light portfolios. Details here.

** As always, please check our work, DYOR, and consult a financial advisor before making any investing decisions.

BUY LIST

Each week we produce a buy list that we share with our members. The intended primary purpose of this buy list is for club members to use as a reference for comparing their own buy list. In theory, all of our buy lists should look pretty similar each week.

As always, please check our work, DYOR, consult a financial advisor before making any investing decisions.

THIS SECTION CONTAINS CONTENT WHICH IS VISIBLE TO QAV CLUB SUBSCRIBERS ONLY.

LAST WEEK’S EPISODE

FREE EDITION:

Last week I did a farewell to the late, great Charlie Munger, and in the Club episode, TK took us through the analysis he and Ryan did about Rule 1 and buying from the top or bottom of our list.

Episode Transcription

QAV 649 Club

[00:00:00] Cameron: Welcome to QAV episode 649. I’m recording this on Tuesday the 5th of December 2023. Happy share market everyone. So as you may have picked up from last week’s episode, TK is down in Victoria playing a charity golf tournament this week. So we pre recorded a bit last week, which I’m going to play in a few minutes.

[00:00:38] Cameron: That’s going to be Tony and I, mostly Tony, talking about Ryan’s analysis. So as you are probably aware, if you’ve been listening for a while, over the last year or so, Tony had a number of interns. Helping him out doing some regression analysis, experimenting with a few of [00:01:00] the variables that we use in the system, and he finally has a bit of a report on that, that he’s going to run through with you.

[00:01:08] Cameron: So I’ll start with that, because that’s probably the most important part of the episode, and then afterwards, I’m going to do a little bit of a memorial for Charlie Munger. Charles T. Munger, who passed away, as you know, last week, aged 99 and 11 months, about a month before his 100th birthday, finally kicked the bucket.

[00:01:32] Cameron: You know, Charlie famously always said that, uh, He just wanted to know where he was going to die so he would never go there. Apparently no one told him it was the hospital. But, uh, that is a life very well lived. We’re all very grateful, of course, for Charlie’s wisdom and wit and teaching over the years. I pulled out poor Charlie’s almanac, The Wit and Wisdom of Charles T.

[00:01:57] Cameron: Munger. Been rereading it over the last week. A [00:02:00] book, by the way, Tony recommended to me probably 10 years ago, 15 years ago, well before I was a value investor anyway. And I did get a copy of it at the time and skimmed it. But it wasn’t until we started doing the show that I really read it cover to cover and it’s a fantastic book.

[00:02:19] Cameron: A lot of anecdotes about Charlie by friends and family. Friends including Buffett and Bill Gates and people he’s worked with for decades. But then 11 speeches that he had given over the years. copied in there. So it’s, um, it’s a terrific read and I’ll cover what I think are some of the highlights of that and a little bit about his life, his biography.

[00:02:46] Cameron: But first let’s cut to Tony’s chat about Ryan’s analysis and then I’ll come back and talk about the great Charles Munger.

[00:02:55] Tony: I’m going down to Melbourne and to Cape [00:03:00] Schanck and it’s my annual golf trip down to play some of the good courses in Melbourne with a group of guys. It’s not really a fill in show, it’s still going to be excellent content, up to par. Yes.

[00:03:17] Tony: Yes. And I sent you through a PowerPoint presentation that Ryan and I put together. So I don’t know if you might want to put that on the website or something. I guess, um, I think this has been an issue for me over the last couple of years that, um, there’s been lots of, uh, questions asked about the QAV process and how might it change and how might it improve, but I’ve been, I guess it pains to do it, um, the right analytics for it, which has just been both costly and time consuming and And, and there are some limitations, right?

[00:03:55] Tony: So if, uh, what Ryan has, has been given is the, [00:04:00] all the buy lists that we’ve been using, uh, since we sort of formalized QAV three or four years ago, and using that as a start, as the start to put together some trial portfolios and then look at the results under certain circumstances, which is, Good, good work and useful work, but you know, there’s limitations for it.

[00:04:20] Tony: It’s really only three or four years of data. And, and if this is a different period to all, all the other periods that have gone by, then we could just be solving for one problem. So I kind of want to put that out there first

of

[00:04:34] Tony: all, and, and also put it out there that, uh, Whatever we come up with as findings out of this analysis, I think we need to run them through a paper portfolio first in some trials to really, you know, feel comfortable that they’re going to work going forward, which is what I’ve been doing.

[00:04:52] Tony: I’ve taken some of these and have been trying them myself. So let me go, let me go through it. So, uh, Ryan [00:05:00] looked at whether the question I asked Ryan was should QAV have a cutoff score of 0. 1, or should it be a QAV cutoff score of 0. 2? And that question was raised by Ryan’s predecessor, Dylan, who did some analysis, um, and came up with the idea that the QAV score should be raised to 0.

[00:05:24] Tony: 2. But there are a whole lot of other questions raised by Dylan’s analysis, because as good as it was, and it was good, and he had 10 years of data, because I subscribed to Refinitiv and paid for that. data access, but we didn’t have all the metrics in Refinitiv that we use for QAV. And he had no way of, I think at that stage, we didn’t have the bread lighter.

[00:05:47] Tony: So we had no way of sort of automating three point trend line checks. And so we decided we would rebalance the portfolio every month. I think it was. Um, for the analysis work that he was doing. [00:06:00] So rebalancing every month and using a QAV score of 0. 2 was better than rebalancing every month at QAV score of 0.

[00:06:06] Tony: 1. So I wasn’t convinced that that was necessarily the right answer. And I’ve been testing it with a trial portfolio ever since, and it’s not going too badly, but I’m not seeing sort of, um, knock it out of the park results. So I thought, let’s get Ryan to have a look at it. And again, it was difficult because sometimes our buy list only has a small number of stocks above 0.

[00:06:30] Tony: 2, um, to score with. And sometimes those stocks are very small and we wanted to have an ADT threshold. Uh, so we didn’t want to buy really small stocks, which is, would make the analysis skewed towards that. Uh, so we, you know, we, we looked at, um, uh, kind of a proxy for it. So we said, why don’t Why don’t we buy from the top of the buy list going down versus buying from the bottom of the buy list going up and see which one performs better.

[00:06:59] Tony: So don’t worry about whether [00:07:00] the cutoff is 0. 2. If you’re buying from the top down, you’re going to have higher scores. Some of them are going to be in the 0. 2s or higher. And if you’re buying from the bottom, you’re going to have scores in the 0. 1s and the teens rather than the really high end. And let’s look at the results there.

[00:07:18] Tony: And we also did it Did a comparison with large ADT stocks. So a 500k ADT portfolio in case there was something distorting about smaller stocks. So three years worth of buy list from August 2020. This is the methodology that was used. Ryan put together 10 stock portfolios constructed by buying from top down and bottom up.

[00:07:40] Tony: So 20 portfolios and he used six different starting dates. So We didn’t just all start these portfolios on the same day, we used different starting dates. 6th of August 2020 was the first one, and the last one started on the 19th of July 2021. So almost a [00:08:00] year’s difference there, which means the later ones have less time than the earlier ones, but we didn’t want to have all the portfolios starting in August 2020.

[00:08:10] Tony: We wanted to spread them out a bit to make sure that there was nothing seasonal in the results. Um, and then we also did a A 500k ADT top down portfolio for the same six start dates. I guess it’s a bit of a benchmark, but to see if there was a big difference. Each, um, each purchase started at 100k. So we were looking for a reasonable sort of size of portfolio.

[00:08:33] Tony: The methodology was that Ryan would check the buy list and see, um, if the stock was a buy, and not a Josephine, for example. So he used the bread loader, and the bread loader has the ability to put a, um, a date in together. Um, a snapshot in history of five years worth of data. And if it was a commodity stock, he would then go and look at the underlying commodity graph and see if it was a buy.

[00:08:55] Tony: Um, for the, for the trial, we [00:09:00] used a minimum ADT of 10, 000 as a filter. And then, um, going forward, uh, he would run the portfolio month by month and check to see if there were brettolator times for three point trendline sells. And whether there was, in the mining sector, commodity sales during that time period.

[00:09:20] Tony: And also he checked the graph for any Rule 1 sales. So a fairly painstaking manual process to go through. Um, He, if the, if the stock was a sell, then he, he’d find the nearest buyer list after that sell date and buy a replacement stock with it. So kind of a, a manual, uh, pro manual process. Replicating the QAV pro QAV checklist process, uh, for d.

[00:09:48] Tony: Um, top types of portfolios, one from top down, one from bottom up. Uh, basically what he found was there was little difference in those portfolios in terms of RRI. [00:10:00] So the top, the buy list, uh, from the bottom up was slightly better from the top down, which was a bit surprising. So the numbers were, from the bottom up, the average RRI was 19.

[00:10:11] Tony: 5. That’s a CAGA number. RRI is that simple CAGA formula in Excel. From the top down, the RRI was 18. 5, so about a 1 percent difference. And I know 1 percent matters, but it’s statistically, you know, in the three years of data and the number of portfolios used, it’s not really a big difference to be able to And interestingly enough, my experience over time has been, even though I like to buy from the top down, I’m not getting, I have never really felt uncomfortable buying stocks from the bottom of the buy list.

[00:10:50] Tony: I’ve never been able to say that buying from the top has produced much better returns than buying from the bottom. So, I consider that the [00:11:00] results too close to suggest a bias, and I also think that having a QAV cutoff score at 0. 2, which forces us more up the buy list, is maybe not the way to go, although I’ve done a, so I set up a dummy portfolio Um, which I’ve been tracking of QAV stocks above 0.

[00:11:20] Tony: 2 and it is outperforming for the last three months. It’s kind of come back more towards the STW and I’m happy to share those results. Um, when I get a chance to tidy up the portfolio, uh, so yeah, STW. STW, so I’ve got a, yeah, sorry, I need to, I need some time to pull that portfolio, to tidy up that portfolio, so let me just call it up and see what I’ve got there at the moment.

[00:11:55] Tony: No, it’s, it’s being, it’s being benchmarked against the dummy [00:12:00] portfolio and against the STW. Let me, I haven’t updated it for a while. Let me have a look. So, Yeah, it’s actually, okay. So where’s the portfolio performance? The last time I did the analysis, the, the, the portfolio started in. Uh, it’s been like, it took a long time to become invested. The first purchase was made back in April, 2023, and it didn’t become fully invested until about August. So it took a while to create the portfolio.

[00:12:33] Tony: over that period, SDW is down 4%. Um, the latest numbers I’ve got in here for the dummy portfolio are down 3%, but that’s not, I haven’t updated that today. And I’m just trying to find the portfolio performance for this. Oh, here we go. The QO, the 0. 2 portfolio has, is down 2%. So, Um, but 1 percent again is not a huge difference, so, um, I’m not [00:13:00] seeing, Anything at this stage to say that the QAV cutoff should be 0.

[00:13:04] Tony: 2. what else though? So, some of the issues, so then we looked at, um, Okay, so when, when Ryan did the analysis, he, he and I went through it, and we both said, Gee, there’s a lot of these death spirals going on, so he would sell a stock because of a rule 1, buy a stock, sell it again because of a rule 1, buy a stock, sell it.

[00:13:25] Tony: So, over the three years, sometimes there were, in some cases, 6 or 7. Buys and sells. And that, that portion of the portfolio was dropping, you know, instead of

dropping

[00:13:37] Tony: 10 percent and then going on to buy something that went up, it was dropping, you know, um, 60 percent after all the buys and sells were taken into account.

[00:13:45] Tony: So then I asked him to go back. And in fact, in the case of the analysis, there were 116 rule one consecutive sells at 10%, a 10 percent stop loss, stop loss. So I asked him to go back and run the whole analysis again, [00:14:00] using a 20%. Rule One Stop Loss. And there was only 10 consecutive rule one sales using a 20 percent stop loss.

[00:14:09] Tony: Um, and the numbers overall, so there were still lots of rule one sales, um, because there was a large number of stocks. We had what? 120 stocks in 12 portfolios, tracking over Say three years, um, with 10, a 10% rule. One in invoked there was 545 cells, uh, with a 20% rule. One invoked there was 366 cells, so much less.

[00:14:35] Tony: And you know, only 10 consecutive rule rule one cells at 20%. Um. So, that sort of caught my attention, and the other interesting thing though was that, um, using a 10 percent Rule 1, the RRI was slightly better, so even though there was a lot more

trading

[00:14:55] Tony: going on, 10 percent RRI was 19. 95 percent [00:15:00] versus 18 percent with a 20 percent stop loss, so, you know, I guess the reason for that is if you’re waiting for it to drop 20%, um, and you’re still having Rule 1 sales, you’re losing more.

[00:15:11] Tony: But you’re not going into that death spiral of continuously buying something and then selling it, um, for a 10%, because the 10 percent number was too small. Um The other thing which was, um, so, you know, again, given the small sample size, given the small time period, um, even though there’s a two, nearly two percentage point difference there for 10%, it’s not statistically a big number, a big difference.

[00:15:37] Tony: And also too, the other thing which was, um, driving performance was there was, in both cases, a small number of stocks that had outsized returns. And you’ve mentioned that with the dummy portfolio. There’s generally one stock which has done really well. And it’s kind of a luck of the draw as to which portfolios had that or not.

[00:15:54] Tony: Um, and whereas the numbers I’m talking about are averages across the different portfolios. [00:16:00] So, uh, I guess the, the The thinking was that even though you’re getting into these death spirals by rapidly selling and buying 10 percent Rule 1 stop losses, you were, you did actually have a bigger chance of picking up that high performing stock.

[00:16:16] Tony: So, it’s kind of swings and roundabouts. So, then I asked Ryan to have a look at transaction fees. So, it was a portfolio that was cycling a lot more, 545. Sales versus 366. Was it going to cost us much more in transaction fees? But it was kind of negligible, given that transaction fees are fairly small. It was basically 2, 000 to 3, 000 difference per portfolio, which wasn’t a big deal in the numbers.

[00:16:45] Tony: So kind of, um,

[00:16:47] Tony: Kind of not drawing big conclusions from it, so what I’ve been doing is trialling the 0. 2 QAV score, which is not showing a huge difference compared to dummy portfolio and STW, [00:17:00] but it is better, and then in my own portfolio, Picking some stocks and using a 20 percent stop loss on those, and that has worked better for my own portfolio over the last few months.

[00:17:12] Tony: Um, so there’s, I think there’s only been about 4, 3 or 4, um, stocks which I would have sold at a 10 percent rule 1 stop loss, and I, I, you know, didn’t, and, and, Kept them and put a 20 percent rule one stop loss in and all, all of those turned around. So, um, three of them I can think of quickly. There was, um, Remilius Resources and Perseus Mining that both went through my 10 percent rule one sell and I held onto them and put a 20 percent alert in and they both have turned around and been at least break even if not positive for me since then.

[00:17:51] Tony: And there was another one which isn’t a QAV stock but Frontier, um, Frontier Hydro, Frontier Energy, FHE, which I, you know, have as a non QAV [00:18:00] stock in the portfolio, a very small holding of it, did the same thing. It went, it actually went down through its 10 percent and 20 percent and kept going and I said I’ll bugger, I’ll just see if it comes back and it did.

[00:18:10] Tony: So it’s now back to being, um, Break even for me as well. So the next, the sort of question that poses to me is, uh, do we need a rule one stop loss or should we just be relying on commodity sales and three point trend line sales? So that’s the further bit of work that, that, um, I should, I think should come next.

[00:18:32] Tony: And, uh, I’m also thinking too. The way I might approach all these different questions and I guess theories that I have going forward is not to try and regression test them because even though it’s useful, I can always statistically say, well, we didn’t have enough data or, um, it was, it was a certain period in time and it’s not, it’s not like we have a large data set to work from.

[00:18:58] Tony: Um, and coding that can give us [00:19:00] all of the QAV process without spending a lot of time and effort doing things manually. So what I’ve changed to be doing is to just set up a portfolio of 10, 10 or 20 stocks in spread, in a spreadsheet. Use the automatic stock price feature. Benchmark it against dummy portfolio and STW and see if these things work.

[00:19:20] Tony: And so going forward over maybe 12 month period and see if they work and whether that is worthwhile looking at starting up as a trial. But, you know, I’m kind of thinking that’s the better way to do this rather than to try and spend money and time. manually regression testing them?

[00:19:36] Tony: [00:20:00] Yeah, I think, I think if I was to design the ideal world for regression testing, you would have to have a large history of data, and ideally going back to GFC time. So you’re comparing recessionary times versus good times in the market. Um, and then the ability to, to have all the metrics that we use, which is going to be hard to automate, right?

[00:20:39] Tony: Because we don’t automate qualified audits, for example, that You know, that’s a small number of stocks, but there are other things that, um, we were finding it difficult to automate. Even the process like commodity checks were difficult to, you know, to go through manually looking for them. Yeah.[00:21:00]

[00:21:01] Tony: Yeah. Correct. Financial health. Yeah. Yeah. Mm

[00:21:12] Tony: hmm. Mm

[00:21:27] Tony: hmm.

[00:21:37] Tony: I think I’m trialling the 20%. I was convinced enough that that was, even though it had the same or similar RRI number, it just churning the stocks less, I think has got to have a benefit for us somewhere, either in transaction fees or just making the whole process easier to manage. Yeah, so I’m trying that, and at this stage it’s [00:22:00] working for me, so I’m going to let it go for, you know, maybe through until next reporting season and see how it works, uh, and then report back.

[00:22:06] Tony: But we might want to go to 20%, and I’m going to set up another portfolio to test having no rule 1 in there. Yeah.

[00:22:17] Tony: Mm hmm.

[00:22:21] Tony: No. Yeah. Yeah. So if, uh, it may be a change to QAV score of 0. 2, but at this stage, it’s, it’s better, but it’s not, it’s not, it’s not a whole lot better, and it’s very difficult to put together a portfolio of stocks that are above a QAV score of 0. 2. They’re big enough, because I’m using, for my trial, I’m using 50, 000 and above ADT.

[00:22:46] Tony: Um, so it’s hard to find. Biggest stocks above a QAV score of 0. 2 and under Josephine or a commodity sale or a three point trend line sale. It was took me months to put together a 10 stock portfolio to [00:23:00] test.

[00:23:06] Tony: Mm hmm. Yeah, because of this fact that we think because of the fact that if you saw if you’re cycling through stock purchases you’re more likely to come across the one that Is the rocket ship and that, you know, counteracts all the cycling you’ve been doing and selling, which is kind of that. Okay. That makes sense, but it’s, that’s a bit of a punt, isn’t it?

[00:23:28] Tony: Cause if you don’t get that rocket ship, then you’ve, you’re worse off.

[00:23:46] Tony: I’m thinking, I’m thinking that even though 10 percent is better return, it’s only better by percentage point or so. So, um, I don’t think that’s statistically significant. Um, [00:24:00] so for example, I didn’t read it out, but from memory, the, the portfolio that was, we also did where the ADT was 500, 000 or more, um, that performed much differently.

[00:24:12] Tony: That was like a 5 percent RRI, 5 or 6 percent from memory RRI. So the fact that we were having small stocks into those portfolios as well, even though I think they were above, I can’t remember what cut off we used. Um, they weren’t really very, very small stocks. There was, you know, some volume to trade in.

[00:24:33] Tony: Uh, that was a big difference. I mean, they were getting 18 and 19 percent in the, um, in the, The Rule 1 test versus 5 or 6 percent if we put an ADT of 500k in. So there’s so many variables in this and if you’re only getting a slight difference, I’m not, I’m not going to say that Rule 1 at 10 percent is better than Rule 2.[00:25:00]

[00:25:00] Tony: A real one at 20%, but what it does do is slow down the churn in the portfolio, which I, you know, I think makes it easier to manage the portfolio and probably also calms things down a bit as well that we’re not sort of getting into this death spiral of, and becoming disheartened that we’re selling stocks and then we sell them and then we see them go up again too, because there’s a number of sold something and in the future time re bought it again in the analysis as well.

[00:25:37] Tony: Yeah, right. Yeah. Yeah.

[00:25:47] Tony: No. Yeah.

[00:25:53] Tony: Correct. And we might change the QAV score from 0. 1 to 0. 2. And I’ll start a [00:26:00] new, a new Rule 1 portfolio of 0%, or sorry, no Rule 1 in the portfolio and see how that goes as well.

[00:26:11] Tony: Correct. Yep.

[00:26:22] Tony: Yeah, it was. It was very time consuming for him.

[00:26:28] Tony: Yeah.

[00:26:38] Tony: Yeah. Or if there’s a listener out there who can shed some light on an easier way to do it, that’s good. And I’m also going to throw it out there too for listeners to maybe do what I’m doing now. Just build a 10 stock portfolio and manage that under different. Scenarios, you know, for the QAV process and see if you can come up with ideas for change to the process.[00:27:00]

[00:27:00] Tony: Paper portfolios, definitely, yeah. Yeah,

[00:27:26] Tony: yeah, thank you. I think, I think if I’m, if I’m honest, I, I’ve been trying to do it, um, in the best way possible. And that’s probably not how I’ve done it in the past. I’ve been a bit more quick and dirty. in the past and, and, and probably also if I’m honest, the QAV process has been static for the last three or four years, largely static for the last three or four years and maybe, maybe there needs to be a bit more of evolution going on in it to keep evolving as things, as the investing scenarios change.

[00:27:56] Tony: So, um, you know, I’m going to set up a [00:28:00] number of these trial portfolios and we might see some more changes coming in the future.

[00:28:13] Tony: Hmm.

[00:28:16] Tony: Correct. Yeah. So I’ll be, I’ll be playing golf when you put this out, Cam. So, uh, have a, have a good week, everyone.

[00:28:55] Tony: Yeah. You can do that. It’s yeah. No, good. [00:29:00] Yeah. Good. Yeah. Okay. Yeah. As I was, it’s interesting. I was talking to Alex today about, about investment. investment groups. And, um, and I said how, you know, I tried a couple of them and it didn’t work out for me. I preferred to work alone and then, um, share results at the end.

[00:29:19] Tony: So everyone’s different. Um, I probably won’t join into the Google Sheets community, but, uh, others can.

[00:29:30] Tony: Yes. Yeah. Right. Well, it wasn’t that like, as I said to Alex, if you join. Um, if you join an investment community and you’re the only person who’s operating in a fact based way, it very quickly becomes what’s your opinion on the future of a particular stock. And I, I just, you know, it’s just a lot of hot air, you know, no one was sort of debating the fact that this company had good operating cashflow.

[00:29:57] Tony: It was more about, Oh, I think China’s [00:30:00] going to blow up and it’s going to, you know, the iron ore price will drop. Well, that’s good. That’s good. You know, but I’m looking at BHP has got lots of operating cash flow. I can probably absorb it. And it’s like, it’s a useless debate, right? And that’s what the stock market is.

[00:30:12] Tony: It’s a, it’s a scorecard for those debates. So they’re useless to actually have them. You’d be better off just going with what you think is going to happen and using your framework and then buying and seeing what happens.

[00:30:33] Tony: I hope so. Yeah, no, that’s a good idea. The other thing I think, the other thing I haven’t done yet, but I think is worth doing is to isolate parameters and like set up a portfolio of owner founders or set up a portfolio of, um, what else, uh, shares with consistently increasing equity, and that’s the only common metric and see how, you know, see, cause that was always going to be the work I wanted Dylan to do, which we never.

[00:30:59] Tony: Got round [00:31:00] to because we kept getting bogged down and trying to, you know, make the QAV process work with the data we had. Um, but yeah, because at the moment You know, most things score a one in the checklist and some things score a two. But I remember Dylan saying, Hey, I think PropCaf and consistently increasing equity are the things that are driving QAV.

[00:31:19] Tony: And if that’s the case, then A, we perhaps could take some things out of the checklist and simplify the process. And, but B, um, they should be scoring more than just a one or a two in the process as well. So that would be the other piece of work that I’m going to try and focus on going forward as well.

[00:31:48] Tony: Yeah, good. That’d be very helpful. And also too, the benchmarking. So it’s, you know, STW is pretty easy. You just have a STW price at the day you start the portfolio and then just use stock history to give you [00:32:00] a today’s price. The dummy portfolio, I had to jump into Navexa a lot to update, but there must be a way of Getting a feed from that somehow to benchmark.

[00:32:10] Tony: Cause the dummy portfolio was how QAV is now, right? So if we’re thinking about changing, it’s got to be better than the STW and the dummy portfolio. I think they’re valid benchmarks to use. Yeah.

[00:32:25] Tony: Thank you. We’re going down to, any golfers out there would have heard of uh, Peninsular Kingswood North. It’s a, it’s a, an old course which has a, um, a new upgrade and it’s getting rave reviews in the golfing world.

[00:32:44] Tony: Yeah, so after we finish I’ll go down to Cape Schanck until probably about the first week in January. So I’ll try and get a month down there, in June I’ll come down as well. Yeah. Yep. Okay. Cheers mate.

All right. [00:33:00] Well, let me talk about Charlie Munger. The man bill gates called the broadest thinker I have ever encountered that was in the wit and wisdom of Charles’ T Munger poor Charlie’s Almanack. So I’m going to start off with a bit of a bio on him. And then I might finish with just cherry picking some of the quotes from him from his speeches. He was born January 1st, 1924 in Omaha, Nebraska. As a kid, he worked for buffet and son, a grocery store in Omaha, about six blocks from the house he grew up in. And the boss was Warren’s grandfather.

Now, as Charlie was six years older than Warren, they didn’t actually meet as kids surprisingly enough, because I think of Omaha, Nebraska as a. To horse town. You want to put all the kids? Between certain ages knew each other, but no, they didn’t know each other. Charlie. Had gone or left buffin son by the time Warren also [00:34:00] worked there some years later, so they didn’t meet until later in life. Charlie was apparently a very big reader from early childhood and became fascinated with science. After reading. The medical library of his family, doctor Dr.

Davis, who was a neighbor and a family friend. And Charlie’s teachers described him as a smart kid who was also a bit of a smartass, always challenging teachers and fellow students. This is obviously something that started early in life with Charlie being a bit of a smartass. His grandfather was a respected federal judge and his father became a very prosperous lawyer.

And during the great depression, these things helped out a lot. His immediate family. Charlie’s immediate family did. Okay. During the depression. Charlie’s father actually belonged to a law firm. [00:35:00] There’s some story where they had to. Um, defend some S local, I think it was a soap or a shampoo company. But it, the, the sort of outcome of the case was going to have an impact.

I think it was on Procter and gamble. So Procter and gamble. Offered to like by. Charlie’s father’s legal firm out of the case, so they could replace him with a big city firm to handle the case. Uh, the big city firm ended up losing the case, but Charlie’s father got paid a ton of money to sit this one out and they coasted through the depression on that. But some of his extended family, weren’t so lucky.

His uncle Tom had a bank in Nebraska that nearly collapsed. So his Charlie’s grandfather, his uncle Thomas father. Came in and bought out the bad loans to save the bank. Ended up getting his money back apparently, but it took a long [00:36:00] time. So he came from. Some money, obviously not. Munga money as we think of it now, but he came from some money in a family of successful judges and lawyers and bankers.

When he went to university, Charlie initially chose mathematics as his major while he was there.

He became interested in physics. And later in life phases, we’ll see, uh, he said that everyone should study physics because it demonstrates how sound theories can explain. Uh, complicated concepts. When he turned 19, 19 43, he enlisted in the army air Corps and was sent to study science and engineering ended up studying thermodynamics and meteorology at Caltech. And then he went and studied Laura at Harvard. Where his father had gone.

Apparently he didn’t finish any of his undergraduate degrees. And so Harvard rejected him, but again, family [00:37:00] connections played a good role. He had. Family friend pulled some strings at Harvard and they let him in. Uh, ended up graduating cumbersome Loudy and was one of the top of his class. And also apparently upset a lot of people when he was at Harvard with his abrupt attitude. A bit of a smartass, even at Harvard. Instead of working in his father’s law firm, he joined a larger firm in Southern California.

This was his father’s idea. She’d go and work in a bigger city.

And in college and in army, he developed what he called an important skill, which was card playing. And he used to say later on that he used his knowledge of cards in his approach to business. Here’s a quote. What you have to learn is to fold early when the odds are against you. Or if you have a big edge back at heavily, because you don’t get a big edge, often opportunity comes, but it doesn’t come often.

So seize it when it does come. [00:38:00] And of course, I think of our cell triggers, particularly our rule one, which a lot of people. Struggle with, but that’s the folding early when the odds are against you. I think that’s exactly what that is. He was married, fairly young, had a few kids, uh, And including a young son who sadly became terminally ill with leukemia and. And back then, I think this is the late forties. They, uh, didn’t really have a cure for leukemia.

They didn’t know how to do bone marrow transplants and his son died. Broke his heart obviously, and also broke his marriage at the time. He ended up getting remarried to a woman who also had a couple of kids from a previous marriage. They then had more kids. For a total of eight and he stayed married to that wife until she passed away in 2010.

Now he was quite successful as a lawyer. Uh, started his own law firm ended up becoming, [00:39:00] uh, Munga tallers and Olson MTO. But he was never really happy with the amount of money that he owned as a lawyer. So he started investing in stocks and also in the businesses of his clients, which was apparently a fairly common practice back then. In the early sixties, he got involved in property development.

California made a lot of money out of that. And he also set up an investment partnership, like the ones Warren had. And this happened after he met Warren, finally. At a dinner party in 1959. So the story is. Charlie’s father had died. He went back to Omaha to deal with his father’s estate. And you remember, I mentioned the doctor, family friend earlier on the sons of, I think the doctor had passed away, but the sons of the doctor held a dinner party. Welcome Charlie back. And they also invited Warren as a guest.

Now that the father. The doctor had been an investor in one of [00:40:00] Warren’s investment partnerships. And apparently he said he invested in Warren because Warren reminded him of Charlie. Now. Warren had heard that story. Didn’t know Charlie, but figured he must be a good guy. Charlie had heard about this investment with this Warren buffet guy and figured he must be a good guy too.

Warren was 29 and Charlie was 35 when they met. Apparently that night. They discussed a business finance and history, and pretty much fell in love. Here’s a quote from Warren. He says, well, when I first met Charlie in 1959, when the Davis family got me together with him, Dr. Davis previously had often mistaken me for Charlie and I wanted to find out whether that was a compliment. Or an insult. So when Charlie came home to Omaha in 1959, the Davis’s arranged for us to go to dinner.

In fact, I think we had a small little private room with a few Davis’s in attendance. Sometime during the evening, when Charlie started rolling on the floor, laughing at his own jokes. I knew, I admit a kindred spirit.

[00:41:00] Warren gets asked in the book, what are the secrets of his success? Charlie’s success.

Warren says, well, one time, some attractive woman sat next to Charlie and asked him what he owed his success to. And unfortunately she insisted on a one-word answer. He had a speech prepared that would have gone on for several hours, but when forced to boil it down to one word, he said that he was rational. You know, he comes equipped for rationality and he applies it in business.

He doesn’t always apply it elsewhere, but he applies it in business. And that’s made him a huge business success. What other character traits do you think have contributed to his success? Warren says, I think actually it really does come out of Ben Franklin that he admired so much. I mean, there is honesty and integrity and always doing more than his share and not complaining about what the other person does. We’ve been associated for 40 years and he’s never second guessed anything I’ve done.

We’ve never had an argument. We’ve disagreed on things, but he’s a perfect partner. What would you say are his most [00:42:00] unusual characteristics? Warren? I would say everything about Charlie is unusual. I’ve been looking for the usual now for 40 years and I’ve yet to find it. Charlie marches to his own music and it’s music like virtually no one else is listening to.

So I would say that to try and typecast Charlie, in terms of any other human that I can think of, no one would fit. He’s got his own mold.

So, uh, a lot to like about that. In the book, there’s also a Q and a with Susie buffet. Uh, Warren’s wife at the time. They say, tell us about Warren and Charlie first meeting one another. She says the first night they met Neil Davis had gotten them together at this restaurant. And I’m watching these two people and I thought, did Neil bring them together?

Because he wanted to see what happened when these egos clashed. Because you have these two strong verbose, brilliant guys. It was amazing to me to see Warren get quieter and let Charlie take the lead. I’d never seen that before. Warren always took that role and I’d never seen anybody take that away [00:43:00] from him.

And he relinquished it to Charlie that night. It was unique. I’ll never forget that evening. That was unusual. Well, Warren is usually so much quicker. He’s just so much faster and smarter than everybody. I mean, it can’t be helped. And he was Charlie taking off. You see, it was really fascinating to me.

And then what happened after that is history. I think Warren felt that Charlie was the smartest person he’d ever met. And Charlie felt Warren was the smartest person he’d ever met. And that was unique to each of them and it’s continued to be that way. And so their respect for each other’s intelligence was I think the beginning. You know, when they see the integrity they have in common and so forth, it’s a match made in heaven. It’s exciting.

It’s like chemistry and I could see always when they were together. I mean, it’s like combustion. It was really, really great. I think that Warren was an aberration in his family. Charlie perhaps was in his, and they just happened luckily to meet each other.

So I [00:44:00] love that those stories there, Charlie left his legal firm after only about three years, but his name stays on the masthead to this very day.

It’s first on the masthead, even today, when they have hundreds of attorneys. And this tells you a lot about the guy. When he left the firm, he didn’t sell his shares. He granted them. To the estate of his younger partner, Fred water, who had died of cancer or left behind a wife and children. So I think that tells you a lot about Charlie manga. Um, he always advised the firm.

You don’t need to take the last dollar and choose clients as you would choose friends. Over the years Charlie and Warren kept up their friendship. Frequent telephone calls and letters and so forth. Charlie. Uh, Charlie’s law firm was engaged by Warren to do legal work for him. Warren has said other clients there. And sometimes they would end up [00:45:00] investing in the same company. Charlie kept building his investment firm.

During these years, between 1962 and 1973, it grew it. 28.3% kegger compared to the Dow at 6.7%. But then in 1973 and 74, it fell 31.9% and 31.5%. In back-to-back years. Kind of know how he feels, what the last couple of years have felt like for us. In 1975, then rose 73.2%. So over 14 years, it grew 19.8% caregiver versus 5% for the Dao. But after this experience, Charlie like Warren decided he didn’t want to invest funds directly for other investors to stressful in the bad years, I guess. So we liquidated Wheeler Munger is investment firm. And his stakeholders ended up getting stock in Berkshire Hathaway.

[00:46:00]

So that’s how he ended up working as Warren’s partner.

They ended up, um, going into business together in the mid seventies. And obviously stayed together until Charlie passed away last week, 2023. So what’s that 50, almost 50 years. They worked together.

Now, Charlie, as I mentioned before, was a big fan of Benjamin Franklin. Think he read Benjamin Franklin’s autobiography. Early on in life and it had a big impact. On him. At the 75th anniversary of see’s candy, Charlie said. I’m a biography nut myself. And I think when you’re trying to teach the great concepts that work, it helps to tie them into the lives and personalities of the people who develop them. I think you learn economics better.

If you make Adam Smith, your friend. That sounds funny, making friends among the eminent dead. But if you go through life, making friends with the eminent dead who had the [00:47:00] right ideas, I think it’ll work better for you in life and work better in education. It’s way better than just giving the basic concepts.

And I can relate to that. Um, people are often, uh, surprised with the amount of history facts I can recall. Dates and events and those sorts of things. And I was explaining it’s not because I have a particularly good memory for that stuff. In fact, I don’t, I’ve got a terrible memory. But I know those dates because they’re part of a story.

They’re part of a timeline because of the way that I do history podcasts. I tell her usually a linear story. And I go into detail with that story. And I kind of remember the beats of the story. It’s like when you watch a film, right? You, you know, there’s what happens in the first act and the second act and the third act. And you, you can remember details when they’re part of a story, our brains. Have evolved over hundreds of thousands of years. To be very good at narratives, our brains [00:48:00] work. Uh, with narratives as a, as a fundamental concept. It’s how we understand ourselves.

We care at create a narrative about ourself. About the people around us about our lives. And about the lives of our tribes and our nations and our religions, et cetera, et cetera. So our brains are really designed to handle narratives and I’ve discovered with myself over the. Last couple of decades as I’ve been doing history podcasts, that if I want to learn anything. I need to figure out the narrative when we started QA V the reason I built my own spreadsheet in the beginning was because I had to have the narrative of why these things were important.

I knew I couldn’t just remember the facts. And that’s why when Tony came up with the. Cafe analogy early on in the show. It really helped me a lot too, because it was a, it was a narrative. It was a story that I could remember, and I could remember why the things. In the story we’re important to the story.

As part of his philosophy [00:49:00] of living. Simply Charlie, like Warren always lived in a modern house. He lived in the same house in California. I believe. For. I don’t know. 90 years. Maybe. No 70 years, probably up until he died. Instead of a really fancy house Charlie’s quoted as stating that in practically every case. They make the person less happier, not less happy, not happier.

A fancy house that is. I think this is a quote from Wikipedia monger appreciated the utility of a basic house with few advantages to living in an Austin Taisha. home. Monger appreciated modesty stating don’t have a lot of envy and don’t overspend your income. And monger’s last 2023 interview with CNBC. He created his success and longevity to a long-held sense of caution and an ability to avoid all of the standard ways of filing. I’ve got some quotes about that [00:50:00] a little bit later on. Uh, you’ve heard Tony talk on the show before about lattices lattice work and Charlie’s multiple mental models. Here.

These are some quotes from the, uh, poor Charlie’s Almanack book. From Charlie. Uh, I think this is from the speeches at the end of the book. What does elementary worldly wisdom? Well, the first rule is that you can’t really know anything. If you just remember isolated facts and try and bang them back. If the facts don’t hang together on a lattice work of theory. You don’t have them in a usable form.

You’ve got to have models in your head. You’ve got to array your experience, both vicarious and direct on this lattice work of models. You may have noticed students who just try to remember and pound back what does remembered? Well, they fail in school and fail in life. You’ve got to hang experience on a lattice work of models in your head. And then he goes on and he talks about some of the models that you [00:51:00] need. One of the first ones he talks about is probability theory. He says by and large, as it works out, people can’t naturally and automatically do this.

If you understand elementary psychology. The reason they card is really quite simple. The basic neural network of the brain is there through broad genetic and cultural evolution. And it’s not for Matt Pascal. He’s talking about the guys that came up with probability theory. It uses a very crude shortcut type of approximation.

It’s got elements of for mat Pascal in it. However, it’s not very good. So you have to learn in a very usable way. There’s very elementary math and use it routinely in life. Just the way. If you want to become a golfer, you can’t use the natural swing. The broad evolution gave you. You have to learn to have a certain grip and swing in a different way to realize your full potential as a golfer. If you don’t get this elementary probability into your repertoire. Then you go through a long life, like a one legged man in an ass [00:52:00] kicking contest. You’re giving a huge advantage to everybody else.

Other models.

He mentions are accounting. The five W’s. He talks about a rule at the Braun company when their communications, where you had to use the five W’s who, what, where, when, why, and how. And you had to tell who you had to tell him you communications, who was going to do what, where, when and why? And if you wrote a letter or directive, In the Braun company, telling somebody to do something and you didn’t tell him why. You could get fired.

In fact, you would get fired if you did it twice.

He also talks about having a backup system, understanding how to do a cost benefit analysis, the psychology of misjudgment. Microeconomics. Which he says involve concepts, like social proof phenomenon. The benefits of scale, the efficiency that comes from scale, et cetera. And he talks about what he calls to track analysis. First, what are the factors that [00:53:00] really govern the interests involved rationally considered? And second, what are the subconscious influences?

Where the brain at a subconscious level? Is automatically doing these things, which by and larger useful, but which often misfunction. So it was part of his process of analysis in life. To figure out what are the. Factors that really governed the interests evolved in this business or whatever the principal was. And what are the subconscious influences that would probably make himself or other people. Get it wrong.

Here’s another quote from him in the book.

And the most important thing to keep in mind is the idea that especially big forces. Often often come out of these 100 models. He said, there’s about a hundred models that you need to know, and that you need to figure out how they all work together. We’re several models. Combine you get the Lollapalooza effect.

This is when two, three or four forces are all [00:54:00] operating in the same direction. And frequently you don’t get simple addition. It’s often like a critical mass in physics where you get a nuclear explosion. If you get to a certain point of mass. And you don’t get anything worth seeing if you don’t reach the mass. Sometimes in the F the forces just add like ordinary quantities.

And sometimes they combine on a break point or critical mass basis, more commonly the forces coming out of these 100 models of conflicting to some extent. And you get huge miserable trade-offs. But if you can’t think in terms of trade-offs. And recognize trade-offs in what you’re dealing with. You’re a horse has. Tuit, you clearly are a danger to the rest of the people.

When serious thinking is being done, you have to recognize how these things combine and you have to realize the truth. Of biologists, Julian Huxley’s idea. That life has just one damn relatedness after another. So you must have mental models and you must see the relatedness and the effects from the relatedness. [00:55:00]

During a talk at Harvard in 1995 called the psychology of human misjudgment. He talks about Tupperware parties and open outcry auctions as examples of where people make bad decisions. He said three, four or five of these things, models work together and it turns human brains into mush. Meaning that normal people will be highly likely to succumb to multiple irrational tendencies. All acting in the same direction.

It’s like the negative version of the Lollapalooza effect. And the Tupperware party example, you have reciprocation consistency and commitment tendency and social proof. For example, the hostess. Gave the party and the tendency is to reciprocate. You say you like certain products during the party. So purchasing would be consistent with views.

You’ve committed to other people [00:56:00] buying, which is the social proof. So all of these things add up and you feel compelled to buy something. You. Probably don’t really need or want.

In the open outcry auction scenario, there’s social proof of others bidding. Reciprocation tendency commitment to buying the item and deprivation super reaction syndrome. IEA sense of loss. He says that’s an individual sense of loss for what he or she believes should be, or is his or hers. These biases often occur at either conscious or subconscious level and both in microeconomic and macroeconomic scale. So you, you. We’ll get yourself worked up and you think you deserve to own this house, and then you can’t stand to see somebody outbid you.

And so you go crazy with your bidding.

And one of the things that Charlie often did, um, was to invert. You’ve heard Turney talk about this a lot on the show. [00:57:00] And he often talked about what to avoid. So what to not do focus on that, start on that, and then you can work out what you should do. Um, this is where he, obviously, he said, as I said earlier on, all I want to know is what I’m going to die, where I’m going to die.

So I’ll never go there. He talked about the. Chess board and thinking about. The more productive regions of his, uh, strategy. Thinking about eliminating. Unnecessary parts of the board that he didn’t need to go to and fucking. Focusing on the parts of the chess board. That he did want to. Occupies, we would call it in chess. I don’t know how many of you are chess players, but you tend to think of the borders, the strategic positions that you really want to occupy.

You want to focus your energy on and you can ignore everything else. And. He [00:58:00] really tried to reduce everything down to the most basic unemotional fundamentals. Again. Which is like, yeah. Well QAV is right. We try and reduce. The value proposition of enough, of an investment in a stock down to something that’s a completely unemotional decision.

We’re looking at the fundamentals. Analyzing them as, uh, rationally and logically as we can. And letting the system spit out the decision, what we should do.

Um, but he said you also have to avoid what he called physics envy. The common human craving to reduce enormously complex systems such as those in economics to one size fits all Newtonian formulas. Instead he honored Albert Einstein’s admonition. A scientific theory should be as simple as possible, but no simpler. Uh, he also said what I’m against is being very confident and feeling that, you know, for sure that your particular action will do more [00:59:00] good than harm.

You’re dealing with highly complex systems where in everything is interacting with everything else.

And for me, that’s, you know, part of what we’re doing with QAV. We do try and reduce it down to an equation that is as simple as possible. But we also understand that we could be wrong when we make that decision. We don’t get wedded to that idea. Again, this is where our cell triggers and the commodity cells and those sorts of things come into play, but particularly rule one. We can do our own analysis, but we also realize there’s a lot of stuff going on that we’re not aware of.

Microeconomics. Uh, sector industry stuff that we’re not aware of. We can make bad decisions and that’s okay. We don’t have to make. Every decision be the right decision or we need is to get six out of 10 decisions to be right. That’s hard enough as it is. Quote from Charlie that I really like is take a simple idea and take it seriously. He says like [01:00:00] world-class bridge player, Richard, Zach Houser. Charlie scores himself, not so much on whether he won the hand, but rather on how well he played it. While poor outcomes are excusable in the Munga buffet world.

Given the fact that some outcomes are outside of their control, sloppy preparation in decision-making. I never excusable because they are controllable. Again, this is why we let the checklist determine our behavior. We make sure that all of our decisions are based on going through the checklist. And Charlie actually talks about checklists and airline pilots using checklists in one of his speeches. I think it’s speech number five.

If you want to go looking for it. He says, how can smart people so often be wrong? They don’t do that. I’m telling you to do use a checklist, to be sure you get all the main modes and use them together in a multi modular way.

So, I don’t know if [01:01:00] Tony came up with the idea of the checklist from Charlie, or he came up with it independently, but you know, great minds think alike, obviously.

He also talks in the book. I think it was his first, the first speech in the book, which was a Harvard graduation speech. When his son was graduating, one of his sons was graduating from Harvard. And he quoted. Uh, speech to the Johnny Carson had given it a Harvard graduation speech some years earlier when his own son graduated. Here’s what Charlie had to say. And he’s talking about, um, how to be miserable. What Carson said was that he couldn’t tell the graduating class how to be happy, but he could tell them from personal experience, how to guarantee misery. Carson’s prescription for sure.

Misery included. One ingesting chemicals in an effort to alter mood or perception. To envy and three resentment. I can still recall. Carson’s absolute conviction is he told how [01:02:00] he had tried these things on occasion after occasion and it become miserable every time. It’s easy to understand. Carson’s first prescription for misery ingesting chemicals.

I add my voice. The four closest friends of my youth were highly intelligent, ethical, humorous types, favored in person and background. To a long dead with alcoholic contributing factor. And a third is a living alcoholic. If you call that living. What Carson did was to approach the study of how to create X by turning the question backward.

That is by studying how to create Nanex. The great algebra brightest Jakoby had exactly the same approach as Carson and was known for his constant repetition of one phrase, invert, always invert. It is in the nature of things. As Jakoby knew that many hard problems are best solved only when they are addressed backwards. Well, I could go on. For [01:03:00] hours quoting Charlie and we, no doubt will. Sure. When Tony’s back next week, he’ll want to talk about Charlie as well. And I might add some more snippets from the book, but, um, There you go, ladies and gentlemen, raise a toast. Uh, to Charles Munger and a life well lived and. Also just for, I guess, teaching us and teaching Tony, not only how to be a great investor, but it had a live. A great generous life. Happy stock market quite a good week. And we’ll be back next week.

Ciao. [01:04:00] [01:05:00]

DISCLOSURE

In the interest of full disclosure, we would like to advise that as of the date of this post, the QAV team currently hold these stocks:

ALD ANZ PRN DTL EHE FHE FPR MMS PRU QBE RMS SSM SUL VUK WAM WGX

If you’re interested in learning more, please review our trading and disclosure policy.