Hello QAVvers

It’s another Tuesday.

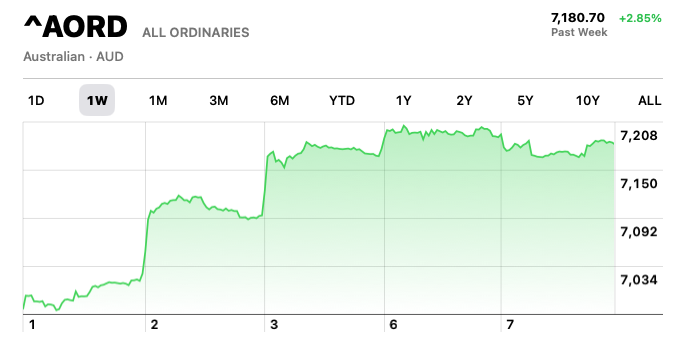

A better week for the AORD.…

… but as TK pointed out on this week’s episode, we feel a little punch drunk, because we’ve had so many false recoveries over the last 18 months… the RBA’s decision to raise interest rates today didn’t have the impact I thought it might, so maybe the market had already factored it in?

SURVEY

There’s a theory that QAV members might be contributing to the percentage rise and/or fall of shares if too many of us are trading in high volumes on the same day, and, as a result, affecting our overall returns.

To test this theory, we need to get a rough idea about how much dollar volume our combined trades might be.

Please complete this anonymous survey so we can put together some numbers.

Let’s have a look at the portfolio.

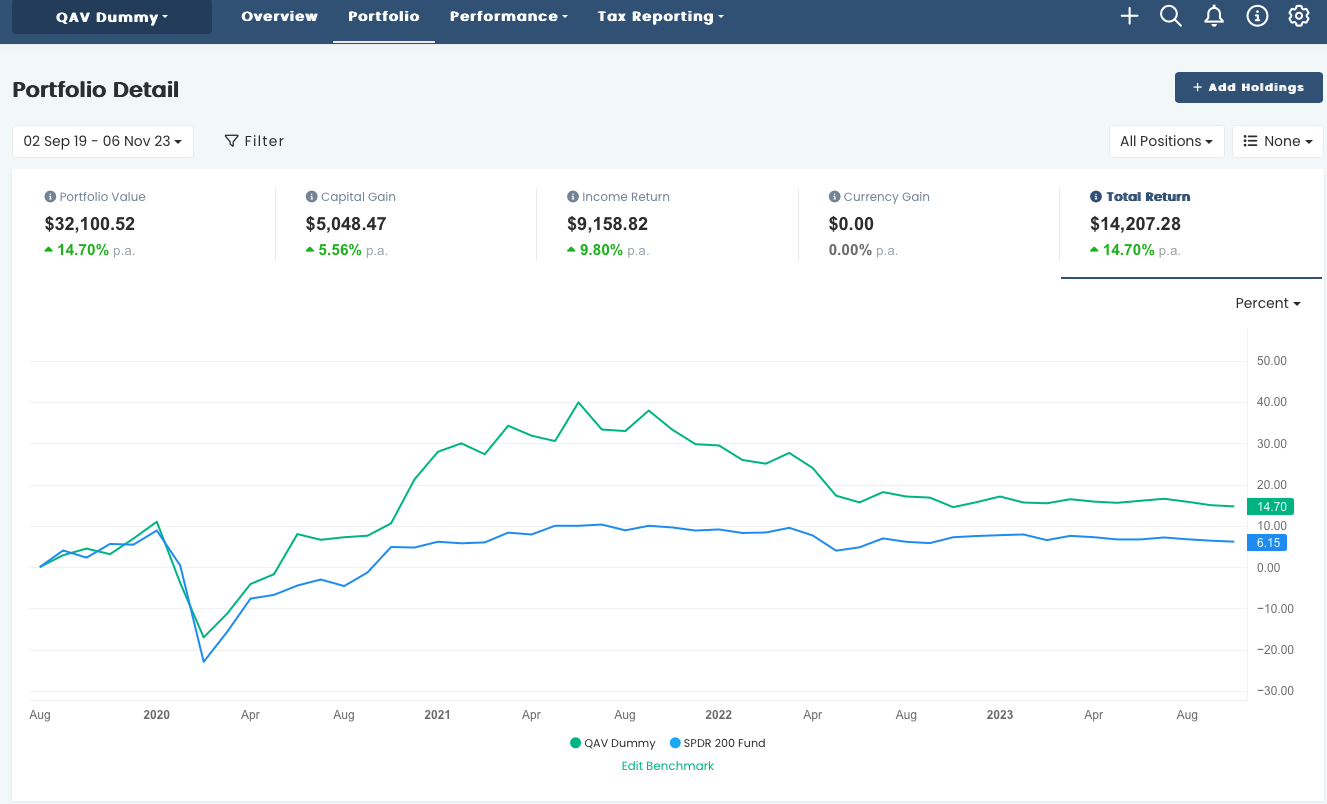

QAV PORTFOLIO REPORT

The Dummy Portfolio is performing well against the benchmark over multiple time frames.

SINCE INCEPTION (02/09/2019)

Our portfolio is still doing about 2.5x the STW since inception.

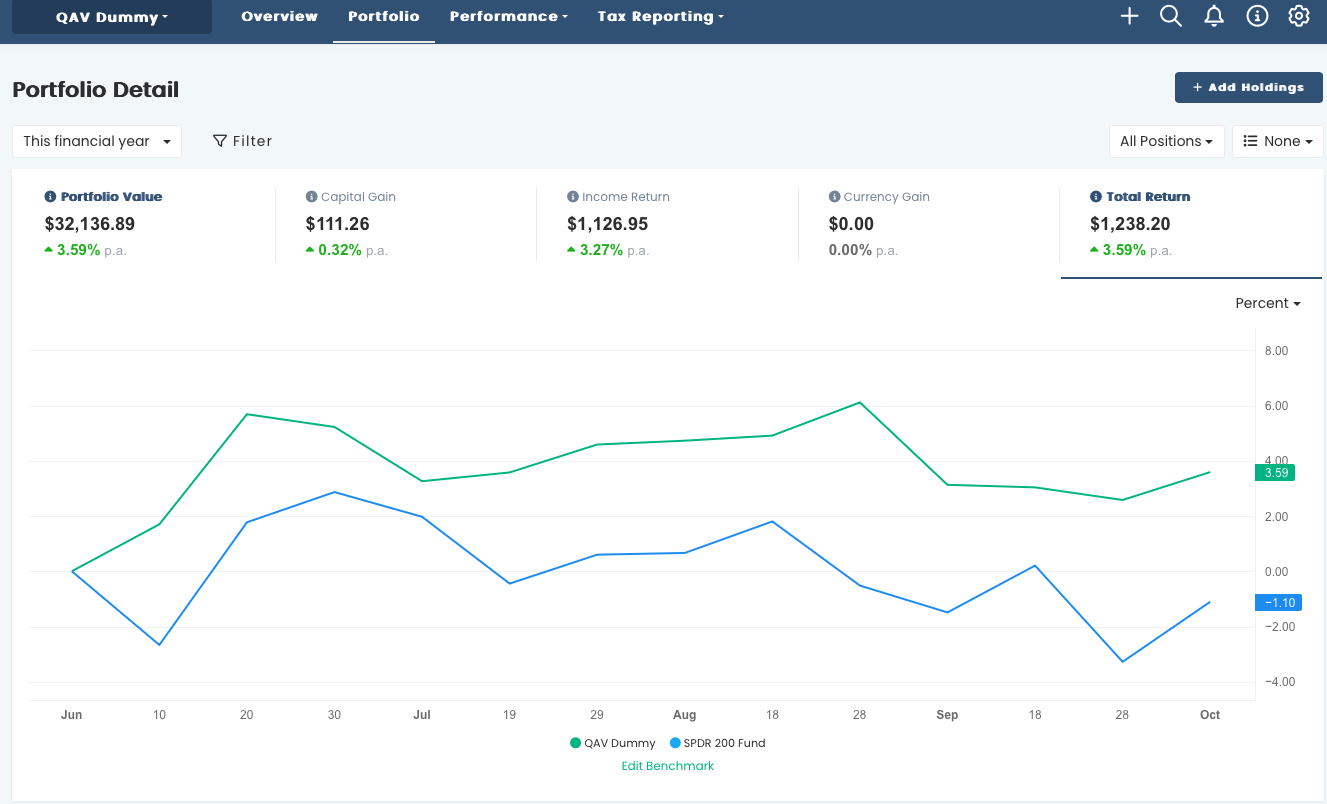

FY REPORT

Despite all of the gloom, for the FY we’re doing much better than the STW.

RECENT TRADES

In the last 7 days we have had no trades.

FREE WEBINAR

I’ll hold another one in a few weeks.

STOCKS OF THE WEEK

During the last week, we also traded some stocks in our Light portfolios. Details here.

** As always, please check our work, DYOR, and consult a financial advisor before making any investing decisions.

BUY LIST

Each week we produce a buy list that we share with our members. The intended primary purpose of this buy list is for club members to use as a reference for comparing their own buy list. In theory, all of our buy lists should look pretty similar each week.

As always, please check our work, DYOR, consult a financial advisor before making any investing decisions.

THIS SECTION CONTAINS CONTENT WHICH IS VISIBLE TO QAV CLUB SUBSCRIBERS ONLY.

THIS WEEK’S EPISODE

FREE EDITION:

Club edition only: JHG delisting; Light Sells analysis; new survey on ADT; SSR down; FPR up; Buffett’s cash pile; RBA meets; cup tips!

Episode Transcription

645 Club

[00:00:00] Cameron: Welcome to QAV, this is episode 645. We’re recording this on a Monday instead of a Tuesday because I don’t know, something’s going on tomorrow.

[00:00:19] Cameron: What’s going on tomorrow, TK?

[00:00:21] Tony: The biggest sporting

[00:00:22] Tony: event In the horse racing calendar is going on

[00:00:24] Cameron: In the world.

[00:00:26] Tony: Yes.

[00:00:29] Tony: Yes. The Melbourne Cup. happy, ASX

[00:00:31] Tony: camp.

[00:00:32] Cameron: and happy, happy, uh, Melbourne Cup for you

[00:00:35] Cameron: tomorrow.

[00:00:36] Tony: Thank you. Alrighty.

[00:00:37] Cameron: When people will probably be listening to this as it’s

[00:00:39] Cameron: running. And when we get to the end of the show, you can give us your tips. How did your tips work out last year? Were they good?

[00:00:45] Tony: No,

[00:00:46] Cameron: Okay.

[00:00:47] Tony: Ruddy’s tip was, I’m going to give you Ruddy’s tip

[00:00:49] Tony: as well later on in the

[00:00:50] Cameron: Oh, okay. Yeah, Ruddy.

[00:00:51] Cameron: Yeah, I’d take tips from Ruddy. ASX has had a better week this week. Tony, uh, but we’ve seen [00:01:00] this before.

[00:01:00] Tony: Why do I

[00:01:01] Tony: feel punched

[00:01:02] Tony: drunk? It

[00:01:04] Cameron: And the RBA is meeting tomorrow. And, uh, it doesn’t sound good. So, like, this is what I can’t figure. Like everyone, like everything I read in the financial review, et

[00:01:15] Cameron: cetera, says The RBA is meeting tomorrow to discuss interest rates. Michelle Bullock has been sounding very pessimistic about what’s going on in the economy.

[00:01:25] Cameron: It sounds like if I had to place a bet on it, uh, I don’t know what Ruddy’s tip is on this one, but I would say that she’s probably going to raise interest rates and yet the market’s been bullish for the last week. What, what am I missing here? Are they just doing it so it can fall again after that comes out tomorrow?

[00:01:45] Tony: does feel like a dead cat bounce, but um, it’s the latest increase has been driven by the US Central Bank. And even then, it’s been driven by Wall Street taking bets on what the US central bank’s going to do. Uh, [00:02:00] there’s a… There’s a theory, I guess, forming on Wall Street that the U. S. central bank is through with rate hikes.

[00:02:08] Tony: So that’s why the market went up in the U. S. It has come back a little bit because Apple’s numbers came out and they weren’t that great. I saw, we’ll talk about it in a minute, but I saw Berkshire Hathaway’s quarterly report came out and Warren’s warning that he expects his operating companies to do worse going forward.

[00:02:25] Tony: But that’s Warren. He never says they’re going to do better, but he is warning that he doesn’t normally warn that they could be facing problems. Um, yeah, so it’s strange. The latest uptick in the market has been driven by US central bankers being a little bit more circumspect on when the, when they’re You know, certain numbers

[00:02:48] Tony: like unemployment coming out in the US, which supports the argument that we’ve seen the last rate hike

[00:02:54] Tony: in the States.

[00:02:55] Tony: And as we know,

[00:02:56] Tony: um, America’s the dog that wags the [00:03:00] ASX as well, so

[00:03:00] Tony: it’s gone up a little bit too.

[00:03:02] Cameron: But then if the RBI writes, it’ll crash again.

[00:03:07] Tony: Probably. If I had a crystal, if I had a crystal ball, I wouldn’t, wouldn’t have been, um, gnashing my teeth over the last couple of years of the performance

[00:03:16] Tony: of the

[00:03:16] Tony: market.

[00:03:18] Cameron: I don’t know. I just, uh, I can’t make any sense of it. It goes up when it shouldn’t go up, goes down when

[00:03:23] Cameron: it shouldn’t go down. I’ve given up. I mean, not that I’ve ever tried that hard to understand it, but, uh, it’s just, makes no sense to me.

[00:03:31] Tony: Yeah. I think it’s largely noise. As we said, yes, um, I think the thing that changed for me in the last week or so was I was sitting on cash because I had nothing to buy and now I’ve got a couple of stocks to buy. So I haven’t gone completely all in for the same reason you just announced that I think if we survive tomorrow’s RBA meeting, that might be a better time to buy, but I bought some stocks Friday, Monday.

[00:03:56] Cameron: Okay, keeping your powder [00:04:00] dry. well, I,

[00:04:01] Tony: I agree with you. I mean, it’s, that’s the thing about since the GFC, the central banks have called the shots in

[00:04:06] Tony: markets

[00:04:06] Tony: really,

[00:04:07] Tony: haven’t they?

[00:04:08] Cameron: I went all in today, but knowing, as I did it, that I’m probably going to have to sell everything when the

[00:04:13] Cameron: RBA rises, raises interest rates tomorrow and everything plummets again, but I’m like, well, I, can’t predict. Don’t predict. I have to just do what the system tells me to do today. But, um, you know, I’m feeling pessimistic about what’s going to happen tomorrow.

[00:04:32] Tony: Yeah, well I haven’t gone all in also too, ’cause I only found a

[00:04:35] Tony: couple of things to buy. So it’s not like the floodgates have opened, so, to speak. Um, but yeah, I hope, I hope I’m wrong. I hope the, the, the floodgates will open soon at, um, it’s about time if they

[00:04:46] Tony: do

[00:04:47] Cameron: Well, there’s nothing going on dramatic in the world, Tony, so, you know, it’s smooth sailing from here on in, I’m sure. of,

[00:04:56] Tony: Speaking of that, I mean, do. What do you think Xi Jinping’s [00:05:00] sitting back and thinking right now? I remember years ago reading an analysis of the, or it might even have been public policy by the US Defense Department, saying they always had a budget that was big enough to fight four wars around the world at any one time.

[00:05:13] Tony: We’ve got two.

[00:05:15] Tony: Xi Jinping’s probably out there spreading a bit of dissent somewhere else in the Middle East to bring it up to three, or somewhere else in

[00:05:20] Tony: the world. And, uh, It’s not very far away from invading Taiwan when the U. S. fleets in the Straits of Hormuza, wherever they

[00:05:29] Tony: are.

[00:05:29] Cameron: you gotta stop believing the capitalist propaganda about Xi Jinping, my friend. He’s, like, all he’s doing is, uh,

[00:05:37] Cameron: building a better, more peaceful world. He’s the peace broker.

[00:05:40] Tony: Mm hmm.

[00:05:40] Cameron: He’s, he was the guy trying to do peace deals between Saudi Arabia and Iran. He’s the, he’s the builder of the Belt and Road Initiative.

[00:05:49] Cameron: A trillion dollars loaned out to developing countries. He’s, he

[00:05:54] Cameron: just wants peace and love, you know, deep down. He’s John Lennon, Xi Jinping, man. He just [00:06:00] wants peace, love, and harmony. Wants a, wants a happier world for everybody. Happy communist future for everybody. I don’t know. Don’t know what you’ve been listening to

[00:06:09] Tony: wonder what John Lennon would think of the Chinese army

[00:06:12] Tony: if he was ever in charge. Oh, what’s that missile

[00:06:18] Tony: for?

[00:06:19] Cameron: I don’t know, but I’m surprised Paul McCartney hasn’t taken half a comment John left on an answering machine 40 years ago and turned it into a new single yet.

[00:06:28] Tony: Yeah, using

[00:06:30] Cameron: We can talk about the Beatles new single in After Hours. I was going to say, speaking about smooth sailing, Tony, Qantas shareholder remuneration revolt. Well, I can’t decide if this is smooth sailing or not, because about 90% of the shareholders voted against the remuneration package or however you want it, whatever you want to call it. I read on the ABC that the outgoing chairman, [00:07:00] what’s his name, Goida?

[00:07:01] Tony: Goyder.

[00:07:01] Tony: Yep.

[00:07:02] Cameron: It’s like an attack of Goida. Um, at the start, it says in the ABC, at the start of the AGM, Mr.

[00:07:08] Cameron: Goida said that the vote against the report would likely be around 90%. He was right.

[00:07:14] Tony: Hmm.

[00:07:15] Cameron: But here’s what I can’t figure out. If you already know that, why put it to a vote? If you already know shareholders, 90 percent of shareholders are against it, what the fuck are you doing putting it to a vote in the first place?

[00:07:28] Cameron: Shouldn’t you be,

[00:07:31] Cameron: why?

[00:07:32] Tony: Well, you got to

[00:07:33] Cameron: I mean,

[00:07:33] Tony: oh, you mean you should change the package?

[00:07:35] Cameron: change the package to something the shareholders approve of. Why are you

[00:07:38] Cameron: trying to ram it through?

[00:07:40] Tony: that’s what happens. So He’s got to do that between now and next year, because if it, if a majority of shareholders voted down next year, then they’ve got to spill, then they then vote

[00:07:48] Tony: to

[00:07:48] Tony: spill

[00:07:48] Tony: the board.

[00:07:50] Cameron: Yeah, right, but he’s not going to be around. It’s not his problem. he’s gone. My question

[00:07:56] Cameron: is, if you know that everyone hates it, why are [00:08:00] you trying

[00:08:00] Cameron: to get it? Why are you going ahead with it? You’re a former senior executive, your wife’s a former senior executive. Explain to me the senior executive corporate thinking here that’s going on, because I don’t get

[00:08:14] Tony: the executive group think he would be, um, doesn’t matter what we put up, it’s not going to get approved, because it’s the only way. It’s a, it’s kind of a quirk of the, um, corporate law is the only way that shareholders can actually hurt the board is via this mechanism of voting down the REM report. Um, and if they do it two years in a row, then there can be a board spill, so they, they could lose, or lose their jobs.

[00:08:38] Tony: Um, so, it, it, yeah. They could have put up,

[00:08:44] Tony: well I mean apart from putting up Alan Joyce gives his money back to the

[00:08:49] Tony: Qantas, the Rem report was never going to get support under any guise this

[00:08:53] Tony: time around.

[00:08:54] Cameron: Okay, so it’s all backlash against Alan Joyce’s, uh, [00:09:00] running the company into the

[00:09:01] Cameron: ground and then taking a big

[00:09:02] Tony: correct. Yeah,

[00:09:03] Cameron: riding off

[00:09:04] Cameron: into the sunset.

[00:09:05] Tony: Yeah,

[00:09:06] Cameron: Alright, Macquarie

[00:09:08] Tony: it’s capitalism.

[00:09:09] Cameron: Bank. Macquarie Bank started the day in the red.

[00:09:13] Cameron: Last week, uh, they reported a 39 percent drop in half year profit to 1. 4 billion. Uh, what’s going on with Macquarie Bank?

[00:09:23] Cameron: They’re one of your favourites. Tony, what’s going on

[00:09:25] Tony: They are, and they are, they’re a volatile company, for sure, but it appears, I mean I haven’t done a deep dive into them, but it appears the issue is coming from the asset division, Macquarie Asset Management. Well first of all, it’s also coming from the commodities trading part of the business, so last year their results were bolstered by the fact that they had this guy trading oil.

[00:09:49] Tony: in, in Austin, Texas, or Dallas, Texas, somewhere, who made outsized profits. But a large part of, that’s not happened again this year, um, a large part of Macquarie [00:10:00] now is what they call Macquarie Asset Management, which is toll roads, so freeways, um, but any sort of asset really, bridges, um, Other forms of infrastructure, pipelines, et cetera, et cetera.

[00:10:13] Tony: And the sales, so normally they work on a sort of pipeline, Macquarie Asset Management, so they buy it, develop it, then turn it over. Sometimes they run them over a long period of time, but a lot of times it’s a buy and flip type approach. And with interest rates rising, no one’s buying, so they’re sitting on assets now, which normally they would be selling part of and booking as profit, which didn’t happen this year.

[00:10:38] Tony: So,

[00:10:39] Tony: you know, it’s one of those things it’s, um, again, I haven’t looked at it in detail, but they still got the assets and they’ll still sell them at some

[00:10:45] Tony: stage. So that profit will come to roost, but it is a very lumpy sort of business when

[00:10:50] Tony: you’re doing

[00:10:50] Tony: that.

[00:10:51] Cameron: It’s always been a very lumpy stock for me too. I’ve bought and had to sell it many times over the last few years. Uh, I noticed, like, it was, it wasn’t on our [00:11:00] buy list. Today. And, but I look at the share price. So when this report came out last week, it was trading at a dollar six. Well, the beginning of the 2nd of November was trading a dollar 61 dropped down to a dollar 56.

[00:11:14] Cameron: Today it’s at a dollar 62. It’s back up. Like it dropped for like 10 minutes and then bounced back.

[00:11:22] Tony: Which I think is that old thing we talked about before the stockbrokers running around town when the

[00:11:27] Tony: quality reports are coming out and picking up the phone and going, sell, sell, sell

[00:11:31] Tony: on the headline. And then over the next two or three days, having a look at the underlying results and saying, buy, buy, buy, we got it

[00:11:37] Tony: wrong.

[00:11:40] Cameron: Well, it wasn’t QAV. That’s for sure because, uh, I

[00:11:44] Cameron: haven’t owned it for a long time.

[00:11:47] Tony: Same. The other thing, I did hear some commentary, I think it might have been in the Fin Review, I’ll read some commentary in the Fin Review saying that Macquarie has gone very heavy into green assets in this Macquarie Asset [00:12:00] Management division and they’re finding it hard to sell them at the moment.

[00:12:05] Tony: Yeah, so that could also be the case, but again, unless the assets have to be written down, they’ll just sit on them until they can sell

[00:12:11] Tony: them.

[00:12:13] Cameron: Looking back through my trading, um, archives, uh, I sold it last out of my super and the dummy portfolio and the light portfolio a while back. I can’t remember exactly. It was a three point trend line sale at 1.

[00:12:31] Tony: Mm hmm.

[00:12:32] Cameron: Um,

[00:12:33] Tony: I did the same.

[00:12:34] Cameron: and it’s at 1. 62 now. So, you know, it’s been coming down since the 1st of September, really.

[00:12:42] Tony: Yeah, so we saved ourselves a bit of money by selling out when we did.

[00:12:45] Cameron: yeah.

[00:12:46] Tony: But it is a volatile stock, I agree. I thought the comment on the green assets was interesting because a lot of people have been getting into that sector. Now, whether that means it’s an overcrowded market because there aren’t that many green assets.

[00:12:58] Tony: Um, but I think, [00:13:00] uh, one of the issues that one of the analysts raised was and I may have, again, haven’t looked at this in detail, but there was a a wind farm or a solar farm in the U. S. which had to get written down heavily because the price it was getting for electricity from that. Um, asset wasn’t as high as forecast.

[00:13:18] Tony: So that could be also hurting the assets that Macquarie hold. And plus there’s this whole backlash in the US, which has been interesting as well, largely driven by Trump and his kin saying that, um, they’re suing fund managers for, for, uh, um,

[00:13:33] Tony: not buying

[00:13:34] Tony: into fossil fuel industries and buying

[00:13:36] Tony: green assets instead.

[00:13:37] Tony: So there’s a, um, a whole lot of fund managers who are now pulling out of that, that market as well.

[00:13:43] Cameron: You’ve been following the, uh, Trump court case in New York. He’s been banned from doing business in New York. They’re

[00:13:50] Cameron: pulling his name off of all of the buildings.

[00:13:54] Cameron: Uh, it’s, uh, it’s a kind of a riot. Yeah, look, I,

[00:13:59] Tony: Sad thing is he’ll probably [00:14:00] get re

[00:14:00] Tony: elected

[00:14:00] Tony: next year.

[00:14:01] Cameron: well, if he’s not in prison by then,

[00:14:03] Tony: Well, then he pardons himself.

[00:14:06] Cameron: he can’t.

[00:14:06] Tony: Why?

[00:14:08] Cameron: Because he’s being sued and he’s being found guilty and these

[00:14:12] Cameron: court cases are in New York and Georgia, they’re states. As a president, you can only pardon yourself for federal crimes, not for state crimes.

[00:14:20] Tony: Oh, that’s interesting, then.

[00:14:21] Cameron: Wow.

[00:14:22] Tony: Yeah.

[00:14:24] Cameron: is why they’re going after him in Southern District of New York and now in Georgia and places like that. So back to MQG before we get over that. We sold it early

[00:14:32] Cameron: July, 176 or whatever it was, went up to 185 a week later.

[00:14:41] Cameron: Um, so, I wouldn’t have noticed that because I don’t look back, but, um, it’s been falling steadily ever since then, so,

[00:14:49] Tony: So Do you think QAV was, uh, forcing the price down there for a while and it rebounded and then it dropped again?

[00:14:54] Tony: Oh, you don’t know? Yeah.

[00:14:57] Tony: You don’t know? All right.

[00:14:58] Cameron: Did it, did it, did

[00:14:59] Cameron: it [00:15:00] cause the price

[00:15:00] Cameron: to drop a couple of days ago and then it rebounded

[00:15:03] Tony: Yeah, nah,

[00:15:04] Cameron: us then I don’t know, man.

[00:15:06] Tony: Yeah,

[00:15:07] Cameron: Um, okay, moving right along. Janus Henderson, J H

[00:15:11] Cameron: G. Um, the

[00:15:14] Cameron: God of, uh, looking both ways, the God of Janus,

[00:15:17] Tony: There’s a guy with a

[00:15:18] Tony: crossing the road,

[00:15:20] Cameron: Yeah,

[00:15:22] Cameron: look to the left, look to the right,

[00:15:24] Tony: also called

[00:15:25] Tony: Hector the Cat,

[00:15:26] Cameron: yeah, is that what it, that’s where I was, yeah, uh, delisting Tony.

[00:15:30] Cameron: Now, shouldn’t be a

[00:15:31] Cameron: problem for any of our

[00:15:33] Cameron: members, yes, shouldn’t be a problem for any of our members because it was a three point trendline sell on the 24th of October, about weeks ago. Thank Um, but I know that not all of our members, uh, abide by the rules when it comes to selling. So

[00:15:52] Tony: We set up a, set up

[00:15:53] Tony: a

[00:15:53] Tony: court

[00:15:53] Tony: in Stonedom,

[00:15:55] Cameron: uh, yes.

[00:15:56] Cameron: Yeah. Yeah. Yeah. We should, at Heresy.

[00:15:59] Tony: Do I get to wear a [00:16:00] really big cap?

[00:16:02] Cameron: Yeah.

[00:16:03] Cameron: Yeah.

[00:16:04] Tony: I like that scene in the Life of

[00:16:06] Tony: Brian that I love when John Cleese has the big cap. All I said was. By Jehovah, that meal was good What? Taking the Lord’s name in vain?

[00:16:17] Tony: Stone

[00:16:18] Tony: him!

[00:16:20] Cameron: although we shouldn’t gloat too much because, um, When we sold it the 24th of

[00:16:24] Cameron: October, it was uh, about 35 bucks, and now it’s 38

[00:16:28] Cameron: bucks.

[00:16:29] Tony: Right,

[00:16:30] Cameron: That’s actually gone up

[00:16:31] Tony: but at least we sold something. We had a share

[00:16:34] Tony: to sell.

[00:16:37] Cameron: Yeah, so what happens now? So, well, I do know what happens because I read about it in their release. It’s a voluntary sale facility. It’s expected to

[00:16:45] Cameron: operate from Wednesday the 13th of December to Monday the 12th of February, 2024, to be followed by a compulsory sale process. If you don’t sell during the

[00:16:56] Tony: Mmm.

[00:16:58] Cameron: if you hold on and go, no, [00:17:00] not selling.

[00:17:00] Cameron: I don’t care what the rules say. That’s what we need is a compulsory sale process. I don’t know. So, so, uh, yeah. Is there anything to talk about with this? I know there’s some questions about it on Facebook, but basically if you are still holding it, you’re going to be forced to sell it at

[00:17:17] Tony: Right, yeah, I, I, look, who knows how it will go, but I don’t like the for sale process because there’ll be someone on the other side treating it like a fire sale. And, um, I’m not sure of the process, but it could even be delisted by then, so they’ll probably have to give you the last price or something like that, which may not be, which then, you know, um, If I put my Machiavelli cap on, and I was an underwriter doing that, I’d be manipulating the stock price at the end of trading to make it cheaper for me to buy out the four sellers.

[00:17:50] Tony: Not saying that will happen in this case, Janus Henderson’s a reputable company, but that’s, that’s a risk. Uh, yeah, so, I mean, the… I did the, [00:18:00] we talked about this company a little while ago, I may have even done a pulled pork on it, but it’s an international fund manager, I think it’s domiciled in the UK from memory, may even be in New York, but it’s listed on a number of exchanges, and so they’re saying, look, we don’t need to list in Australia anymore.

[00:18:17] Tony: It’s the, you know, the stock isn’t very liquid here, or it’s not a big, big enough, a big enough, you know, pool of investors to, to, um, make it worthwhile given there’s costs of listing here. So they’re, they’re consolidating their, their, um, Shareboards, I think they’re only going to be listed in London and New York going forward, maybe some other places too, but not Australia.

[00:18:41] Tony: So it’s a delisting company, a delisting process, the company isn’t going away, but they don’t want us to be shareholders in Australia anymore. So you’ve got choices to sell your shares online now. To go into the voluntary process where I’ll give you, um, I haven’t looked at how they calculate the price, but again, it’s, [00:19:00] um, it’s, uh, I think they’re going to use the NY, the New York Stock Exchange price as the basis to sell your shares, um, voluntarily, and then they’ll do it compulsorily at the end.

[00:19:12] Tony: And they may use the NYSE then too to work out the price, um, probably will. So, um, it just depends how long winded you want to be during this process. Get your, I’d, I’d, if it’s me, I’d, and if the price is above the three point trendline, sell price, you’ve made three bucks over what I did when I sold out, um, but I’d be

[00:19:32] Tony: selling out while

[00:19:33] Tony: it’s

[00:19:33] Tony: still available.

[00:19:35] Cameron: Yeah.

[00:19:35] Tony: look, there’ll be, there’ll be someone who’s at large instos, um, who’s watching the NYSE like a hawk and comparing it to the price here, and they’ll make a couple of pennies on the trade by buying it or on

[00:19:46] Tony: stock beforehand, um, at a price less than what it is in the New York listing, and then try and arbitrage it.

[00:19:53] Tony: So there’ll be someone buying your

[00:19:54] Tony: shares

[00:19:55] Tony: now.

[00:19:57] Cameron: Yeah, like it, the share price [00:20:00] hadn’t really changed a great deal from when we sold it until Thursday. It jumped 10 percent on Thursday last week with the announcement of this, you know, so

[00:20:10] Tony: yeah, that’s interesting, isn’t it? So that suggests to me someone has already spotted an arbitrage up to 10 percent difference and they’ve bought in. Because you think, you think most people would say, Oh, it’s going to be delisted, I’ll sell. Because if you sell, you get your money in two days.

[00:20:25] Tony: And I don’t know if they’ve come out and said how long it will take to get the money to you if you’re selling into their voluntary sale or whether you’re being compulsorily

[00:20:33] Tony: acquired. But it’s probably going to be 30 days would be my guess.

[00:20:38] Cameron: right.

[00:20:39] Tony: So you get your bucks quicker if you do it this way. On

[00:20:42] Tony: market.

[00:20:44] Cameron: I’m just, um, pulling up, uh, Stock Doctor to see if I can see the trading volume the last couple of days. It’s 30 day, oh, oof, yeah, oof. Yeah, [00:21:00] big spike on the second. Um,

[00:21:04] Tony: yeah,

[00:21:04] Tony: which would have been, you think, people getting the news and then selling, so why

[00:21:07] Tony: did the price go

[00:21:08] Tony: up?

[00:21:10] Cameron: there was a lot of people were buying.

[00:21:12] Tony: Right,

[00:21:12] Cameron: why are they, yeah, why are they

[00:21:13] Cameron: buying?

[00:21:14] Tony: well, they must see an arbitrage between the NYSE price and the

[00:21:18] Cameron: yeah, right. Yeah, right. So a lot of people are getting out, but somebody’s snapping them up.

[00:21:24] Tony: Australian

[00:21:24] Tony: price.

[00:21:26] Cameron: Well, is it the

[00:21:26] Cameron: company? No, this isn’t the voluntary sale facility, right? It’s not the company buying its own shares.

[00:21:33] Tony: No, the voluntary sale facility starts in December.

[00:21:36] Cameron: Yeah. Right.

[00:21:38] Tony: I’m not saying the company didn’t buy them, it could be the company buying on market

[00:21:42] Tony: on the day of the announcement, I don’t know.

[00:21:43] Cameron: Right. Well, speaking of not selling things when you’re supposed to sell them, um, you know, we always, we always have this, uh, conversation about the rules and when we sell something and [00:22:00] sometimes things go up and sometimes they don’t go up and I was speaking to somebody last week who said, yeah, I don’t sell things when they breach, I just hold onto it.

[00:22:10] Cameron: If they’re a good company, I don’t sell it, I just hold on. Which prompted me to do a little bit of analysis. So I took the last 18 months of the light portfolio and looked at all of the cells that I’d done over the course of the last 18 months. And there has been a depressing lot of them because it’s been a very volatile period.

[00:22:34] Cameron: So I looked at all of the rule one cells. The three PTL cells and the commodity cells. The only ones I didn’t look at is where the company is delisted or they’ve changed their code from ECX to FPR or something like that, because that just added a little level of complexity too. Tracking it. What I did is I, I wrote a script or several scripts actually to download [00:23:00] all of the closing prices of all of the shares that I’ve sold in the last 18 months since about April 2022, maybe a little bit earlier than that.

[00:23:11] Cameron: And all of the dividends that those stocks have issued since then, and then calculated. Uh, in which cases would have been better off just holding that stock, taking into account any price increases since we sold it and dividends that have been accrued since we sold it versus where we did end up when we sold it, not taking into account how we redeployed those funds.

[00:23:40] Cameron: So after we sold it, you know, what happened with those stocks, just looking at a very base level, would we, would I have been better off? NetNet holding that stock or doing what we did, which is sell them. And when I added it all up, it said that if we just held all of the stocks rather than [00:24:00] selling them as a, as a group, the portfolio would have been 5 percent better off.

[00:24:05] Cameron: However, nearly all of that came from a single stock, which was. TGA, Thorn Group, which had a 391 percent increase since I sold it in May of 22, and it’s currently being acquired. But if I take that out as an outlier, the benefit of not selling was negligible. It was basically a zero sum game. Um, some stocks have gone on to recover quite well, mostly DUR, which I bought back into anyway.

[00:24:42] Cameron: We’ve held DUR in the portfolio and it’s up like 140 percent I think since we bought back into it. So that, you know, there is that argument that we sell and then we buy back into things, as we always say. But the overall benefit of holding everything versus never selling was basically zero. [00:25:00] Now, that doesn’t take into account what would have been brokerage.

[00:25:04] Cameron: guess of trading in and out. So if I added in broke, we don’t have brokerage with the dummy portfolio cause it’s a paper portfolio, but if I added brokerage in there would be, uh, that would, you know, be a difference because there’s a lot of trades accounted for in there, so that’d probably take a couple of points off it, but, um.

[00:25:26] Cameron: Yeah, a couple of disclaimers there. Obviously, so that’s only 18 months of history, and it’s been a very volatile period, as we know. If I ran that over a five year period, um, uh, it could be… Have a different outcome. If I did factor in how we redeployed the funds and how those things have performed, that might change the outcome as well.

[00:25:48] Cameron: But I just wanted to see, you know, I think, uh, Cosman and a few other of our listeners have done their own analysis like this over the last year. So I thought I’d do my, mine now that I’m a [00:26:00] scripting God, uh. And, uh, yeah, so that was my takeaway is really nothing, nothing, no, would have really gained nothing apart from brokerage if we just held onto those stocks over that 18 month turbulent period.

[00:26:20] Tony: Yeah, right. I mean, for me, buy and hold, well, buy and hold was killed for me during the GFC when, when I did buy and hold and everything just halved in value over 18 months. and so I thought there has to be a better way. And given that it’s, the way I view what you’ve said is given that the buy and hold is roughly similar to the trade, uh, at least with the trade side of things, we’ve been taking out insurance

[00:26:48] Tony: that we don’t have another big drop during that 12 month period. And it sounds like if it’s a net net, then the insurance was free over that period, except that we’ve had to do a lot of work compared to the buy and

[00:26:59] Tony: hold [00:27:00]

[00:27:00] Tony: approach.

[00:27:01] Cameron: Yeah. And again, if I took brokerage into account, there’d be a bit of a difference, but yeah, I don’t know how much I could, I could do some quick numbers on that, but I don’t think it’d make a huge impact. Um. Yeah, so, and the market, you know, has been not great for the last 18 months, but it hasn’t had a GFC like fall and no recovery.

[00:27:25] Cameron: It’s sort of gone up and then gone down and gone up and gone down and, you know, not like the GFC where it went down and then stayed down

[00:27:33] Tony: Yeah, right.

[00:27:33] Cameron: took 10 years to

[00:27:35] Cameron: get back,

[00:27:35] Cameron: right.

[00:27:35] Tony: Yeah. Well, hopefully that doesn’t happen. Um, we’ll we’ll see.

[00:27:40] Cameron: Hmm.

[00:27:41] Tony: It’s not going to take much for that to occur, though, I can, I mean, you know, with, um, interest rates having risen, with, uh, unstable geopolitics, with, uh, You know, there’s still a fair bit of, um, still a fair bit of forecasting of a recession in the US and certainly if [00:28:00] you look at what Credit Corp said about the customers who are working, walking away from their repayment plans in their business, that’s got to be a bad sign.

[00:28:07] Tony: So, you know, I played golf with a mate of mine from the States who was visiting Sydney a couple of weeks ago and he said, yeah, it’s terrible over there, so. Again, these are all anecdotal types of pieces of information, but if, if, if the economy does take a downturn, particularly in the States, then yeah, the share market may come off in a GFC type way. The, the reason for saying all that, and I hope it doesn’t happen, is because we have some kind of process for handling that, which is just our rule one and three point trend line sales. Whereas the buy and hold person just has to… Put the shares in the bottom drawer for a couple of years. And as we saw with the GFC, the share market’s only back to about that pre GFC

[00:28:47] Tony: level now, some 15 years later.

[00:28:51] Cameron: Hmm. Yes. If I look at, yeah. Yeah. You pointed that out, I think, last week, right?

[00:28:59] Tony: Yeah, well, if you [00:29:00] had a, if you bought an index fund and it got up to the heights, you bought it before 2007 and it

[00:29:04] Tony: got up to the heights it,

[00:29:05] Tony: did, which I think the ASX was about 7, 200 around the time it started to slide

[00:29:11] Tony: into the GFC. It’s, it’s around that

[00:29:13] Tony: level now. That’s 15

[00:29:15] Tony: years

[00:29:15] Tony: ago.

[00:29:18] Cameron: Yeah, the All Ords hasn’t really, I mean, it, its peak in August, 2007 was 6 7, 7 9. Today it’s 7 1 9 8. It did go up to 7, 6 86, November 22. But um, yeah, it hasn’t gone very much above where it was back in 2007. Bit of 15 years

[00:29:42] Tony: Or more. Yeah, Whereas if you had sold, gone to cash during that GFC period, you were buying it at a much cheaper price.

[00:29:52] Cameron: buying back in.

[00:29:53] Tony: Buying back in at a much cheaper price. Yeah.

[00:29:55] Cameron: Yeah.

[00:29:57] Cameron: Well, speaking of buying things at a cheaper [00:30:00] price or not.

[00:30:01] Cameron: Let’s talk about let’s talk about our survey. So by the time people listen to this, I will have published

[00:30:07] Cameron: this. This is based on the idea you’ve been kicking around for the last couple of weeks about whether or not QAV is actually affecting our returns.

[00:30:18] Cameron: Particularly In the high ADT side of things. So what we’ve done is we’ve published a survey and asked people to anonymously give us an indication about the sort of size of parcels that they are buying or selling when they’re trading, what your average trade parcel is, because we’re trying to get an indication about how much of an impact.

[00:30:42] Cameron: QAV members might be having on certain stocks, and it’s the first step in what I think will be a multi step process of trying to drill into this, but, uh, in a nutshell, the theory is that it [00:31:00] It’s possible that because there’s been so little to buy, particularly in the high ADT space over the last couple of years, that when something does become a buy, uh, enough QAV members pile into it in the, on the same, in the same period, same couple of days, push the price up in the process and push the price up on each other in doing that.

[00:31:29] Cameron: Um… And maybe pushes it up by 5 percent over the course of a couple of days. Um, and then when we stopped pushing the price up, the price retreats back to where it was earlier, and then maybe even a little bit more so, which forces us to sell because it becomes a rule one. And then we repeat the

[00:31:54] Tony: Hmm.

[00:31:55] Cameron: a week later when something hits the buy list.

[00:31:58] Cameron: Is that [00:32:00] kind

[00:32:00] Tony: a good summary. It’s and it’s only a hype. It’s only hypothetical at this stage. I’m just trying to, um, make sense of the last couple of years. I know it’s a volatile market, but in my trading history. It’s been extra volatile, and I haven’t experienced a situation like this before. Um, yeah, so it could be that that’s just the way it is.

[00:32:19] Tony: That’s the process. Or it could be that somehow QAV is…

[00:32:26] Tony: And I must admit, whenever I’ve tried to, you know, dial into some of my trades, I’m not seeing evidence of it. So this is only a theory, um, but, you know, but the theory goes, if there’s a certain stock and it sits at five times, you What, you know, my, if the ADT is five times what I want to buy, and there’s five of me out there, then suddenly I’m not buying, well, QAV’s not buying 20 percent of that daily transaction, we’re buying the whole lot, and if there’s a, if there’s enough, [00:33:00] um, stock waiting at a higher price, we’re buying up The latter, so to speak, and pushing the price up, as you said before.

[00:33:06] Tony: Um, so it’d be good, good, it’d be good to know,

[00:33:10] Tony: uh, what the profile, I

[00:33:12] Tony: guess, of the base is. It’s all anonymous, um,

[00:33:15] Tony: but it may help us try to understand if, uh, QAV has been causing us to trade more than what I normally

[00:33:22] Tony: would.

[00:33:24] Cameron: Yeah, we’ve been doing. A range of analysis over the last couple of weeks, trying to figure this out and haven’t really made any progress yet, but this is the next step in trying to get some numbers. So if you don’t mind filling out the survey, it is anonymous. There are no names associated with it, but, uh, if we get.

[00:33:44] Cameron: Enough feedback that there are enough high ADT, uh, members that might be skewing the performance of some of these stocks. We’re probably all we want to get together and have a chat about it. So, the next step will be say, okay, if you, if you, if you said that you were one of those high [00:34:00] ADP, ADT people, how about we jump on a Zoom call and have a chat,

[00:34:06] Tony: well, and it could also be, I mean, you know, we’ve seen some strange things happening, um, like, Credit Corp, for example. I know it put out some bad news and that could explain away the reason why it dropped by, what was it, 30 percent in a day?

[00:34:19] Cameron: 38.

[00:34:20] Tony: Yeah, but it was also the day after it crossed the three point trend sell line for QAV.

[00:34:26] Tony: So, we may have been in the mix. Maybe it would have dropped 10 percent without QAV. I mean, it’s, I

[00:34:31] Tony: can look up Stock Doctor in the volumes,

[00:34:33] Tony: but I can’t tell who’s in those volumes. So,

[00:34:35] Cameron: Yeah,

[00:34:36] Tony: yeah, like I said, it’s just a theory, so it’d be good to have some more information. So, um, thanks in advance if you fill out the anonymous survey.

[00:34:43] Cameron: yeah. Um, all right, moving right along. What else is in the news that you want to talk about TK?

[00:34:52] Tony: A few things, um, there has been some stocks in the moves, speaking of, in the news, sorry, speaking of moves. Uh, [00:35:00] SSR went down, it’s on our buy list, but it went down quite a bit on the back of a quarterly update. And that seems to be happening a lot in this market, that, uh, stocks are dropping or raising 10 percent in a day, which is really kind of unusual in my experience.

[00:35:17] Tony: Oftentimes, a quarterly update won’t make much difference because, you know, it’s only three months since the last update, so either it’s a sign that there’s a very big deterioration in the economy around the corner that’s coming through on some of these stock updates, or it’s a sign that, I don’t know, people are getting their hair triggers out and just shooting.

[00:35:39] Tony: The reverse happened with Fleet Partners, um, the old ECX, which you talked about before. Uh, it went up on the, on an update, which said that they were, um, uh, buying back their stock again, and they’ve been doing that for a while. So again, the stock was up, I think, um, might even have been up 5 to 10 percent on the day that was announced.

[00:35:57] Tony: So there’s a lot of moves going on, which [00:36:00] is a bit strange. Uh, a couple of things while we’re at it on the buy list. Um, I was going to do a I was going through the buy list today working out what to do a pulled pork on and there’s a stock called PACT, P A C T. It’s one of the, um, uh, container manufacturers that, um, kind of, um,

[00:36:20] Tony: is part of the loose Pratt family.

[00:36:23] Tony: So a guy called Rafi Jeminder. Um, who I think is related somehow to the people who, uh, uh, to Anthony Pratt, who now owns Vizzi. But anyway, that’s not, that’s not irrelevant. No, I may have got that wrong.

[00:36:33] Cameron: Best, best friends with Donald Trump?

[00:36:36] Tony: Well, Anthony Pratt is. Um, so PGH anyway, look like, well, he’s on the buy list, but be careful. It’s, it’s, um, uh, Rafi Jaminder, the CEO and major owner is gonna, has issued a, um, a takeover to take it off the, ASX to buy it out basically, so just be aware of that.

[00:36:56] Tony: I think we spoke about Harvey Norman once before, it’s still [00:37:00] on the buy list, but I think it’s a mistake in the data from memory

[00:37:03] Tony: in terms of the number of shares it’s coming through from Stock Doctor’s data providers, so just be careful with that

[00:37:09] Tony: one too.

[00:37:11] Cameron: Yeah, I keep asking Victor about that and I, Victor at Stock Doctor, and I don’t think he’s resolved that one yet.

[00:37:21] Tony: Yeah. Okay. But just be careful. I mean, do your own research when you’re going to buy a stock, but that’s, there’s a couple there which are on the buy list, but maybe shouldn’t be bought at the moment. Unless you’re an experienced trader during takeovers, then just be aware that PACT is under, under a deal.

[00:37:37] Tony: I noticed today that, um, Buffett’s quarterly report came out and Berkshire Hathaway is sitting on its largest pile of cash ever. The headline in the AFR was Buffett’s cash pile hits 241 billion, record high on scarce deals. So, I know he’s, uh, his ADT is a lot larger than our ADT, so he’s, [00:38:00] uh, he’s finding it hard to buy things at the moment just as we are.

[00:38:03] Tony: Uh, but the other thing which, um, Which struck me, and I’ll just try and find it in the article. Uh, there’s a section in the article talking about the fact that his operating companies were expected to report lower numbers next quarter. Um, they’re buying back more stock, which is not unusual if they can’t find something to do with their cash. anyway, I can’t find it, I’m just skimming through the article. But, but, uh, another sign that the U. S. economy may not be as strong as it, um, is going forward than it is now. well that’s all I got. RBA meets tomorrow as we spoke about. The other interesting thing is that the government went through this big rigmarole of reviewing the RBA.

[00:38:47] Tony: Now, you know, maybe that was done to, um, justify not, uh, renewing the seven year term of the past, uh, person who retires soon. Uh, But they, the, the [00:39:00] review set up said, let’s set up two boards. One to look after monetary policy and one to be the governance for the operating parts of the RBA. Uh, so the government just announced they put Michelle Bullock in charge of both.

[00:39:12] Tony: So , I, I, you know, was the reviewer waste of time. What’s, what’s the point guys? Um, it’s, it’s Meet the new Boss, same as the old boss, meet the new corporate structure, same as the old corporate structure. The RVA seems to have, uh, gotten a. Come through a review with a clean bull of health in, in effect. And the only thing that’s changed is the governor.

[00:39:34] Tony: And, and the only difference between them, well, is there’s not

[00:39:37] Tony: much difference between them. So one’s male and one’s female.

[00:39:40] Tony: Um, so it’s a, I think it’s a bit of a shame, this whole review of the RBA. But

[00:39:46] Tony: anyway,

[00:39:48] Tony: uh,

[00:39:49] Cameron: Is it just a temporary thing, like they’re putting her in charge of both until they can find someone to run one. of them?

[00:39:56] Tony: No, possibly, but at the moment, she’s going to be doing what [00:40:00] the old guy did, but just do it with two boards rather than

[00:40:02] Tony: one,

[00:40:04] Cameron: Well, that’s what they always say, Tony. Two boards are better than one, I’m

[00:40:07] Tony: especially when they’re doing the same job overall as the old board was. So it’s twice the cost, by the way, to the taxpayer.

[00:40:14] Cameron: Hmm.

[00:40:15] Tony: Anyway, I’m going to do a pulled pork, uh, that reminds me, I was going through working out what to do a pulled pork on, and it’s hard to find something on the buy list that’s a buy and that we haven’t done before.

[00:40:28] Tony: So do you keep a list of the prior pulled porks? I may have to start repeating myself, but I’ll do it with the oldest ones

[00:40:35] Tony: first.

[00:40:36] Cameron: Hmm. I don’t, but I can

[00:40:39] Tony: No, that’s fine. I’ve…

[00:40:40] Cameron: together.

[00:40:41] Tony: My memory’s fading over the last four years as to what I’ve done and what I haven’t done.

[00:40:45] Tony: Uh, I was gonna do one on BlueScope Steel, but I started to look into it and I thought, yeah, I think I’ve done this.

[00:40:51] Cameron: Hmm.

[00:40:52] Tony: Um, do you recall me doing BlueScope Steel?

[00:40:56] Cameron: Um, no,

[00:40:58] Tony: Okay. Well, I can do it [00:41:00] next week. It was back on the buy list again today. So, um, I can do it next week, but I thought I’d done it when I started to do it. Anyway, I have found one, um, it’s called ServiceStream and the code is SSM. uh, it’s a, it’s a company that, um, designs, builds, and maintains infrastructure basically for telcos, utilities, and a bit of transportation infrastructure these days.

[00:41:28] Tony: So it deals in large complex cabling. Structures and companies, uh, was big in the NBN when it was first rolling out and probably still is big in the NBN, uh, big, big customer. The telcos are a big customer. Uh, it’s currently a Josephine. Um, it’s above its sell line and it’s buy line, but it’s, I think it’s a couple of cents below last month’s close.

[00:41:51] Tony: So it’s not necessarily a buy right now, but. People may wanna have a look at it. Um, interesting company and I, and it’s on the buy list and it’s, [00:42:00] it’s definitely there for value. I’m not sure it’s gonna be there for quality, so I’ll just run through that and, and talk about it. Talk about why I think that, um, ADT is 623,000, so it’s a reasonable size.

[00:42:12] Tony: for people to have a look at, uh, with their own portfolios. As I said, engineering firm. Um, history largely came out of the telco sector. And I remember them, they’ve been around for 20 odd years or more. And interestingly enough, I couldn’t find a history, a corporate history on their website. So I pieced together a little bit through newspaper clippings, etc.

[00:42:31] Tony: Um, I remember them, but my memory of them as being a telco infrastructure provider. And one of the problems that they had over the years was they basically only had two key customers, Telstra and the NBN. But it looks like, um, now they’ve, they’ve realized that and they’ve de risked that dependence. And even though Telco is still probably half their business, they’re now about 40%, um, with, uh, the, uh, other types of infrastructures, mainly electricity companies, and 10 percent [00:43:00] is this growing part of their business with, uh, transport networks.

[00:43:04] Tony: Uh, they, they did. Uh, purchase, lend, leases, uh, services, business a couple of years ago. So I guess they’ve been acknowledging the fact that they don’t want to be too dependent on big telcos and they’re trying to diversify away from them. So that’s all good. Uh, I think, um, I think it’d be fair to say without, you know, being too negative on the company, they’ve had a bit of a rocky road of acquisitions and contracts gone wrong.

[00:43:31] Tony: Uh, contract blowouts, um, fixed price contracts not being, um, You know, profitable for them, or construction delays, etc. And I went back over their history, they do put all their annual reports online, and um, this was the… Lead sort of sentence in the 2023 director’s report, and it goes, while the board was disappointed with the reported onerous contract and associated financial impacts on the [00:44:00] business, we are pleased by the way in which the executive team has steered the business through this issue.

[00:44:05] Tony: And if I go back to the The oldest report on their website, 2010, it says, I am pleased to report that the management team have dealt decisively with the problems the company encountered with the service stream infrastructure services. The management of that issue has not prevented the company from retaining its major contracts and relationships with Telstra, Etsa, Optus, and Vodafone, and winning the business with important new customers such as Origin Energy and the Queensland State Government.

[00:44:31] Tony: So, large contracts on thin margins can make for a You know, a very volatile business. And I guess that’s my, um, headline for, for people who are interested in looking at this, it has a rocky history. It has been a bit of a falling knife over the last sort of four or five years, but it has just sort of come around a little bit, uh, and started to appear on the buy list, um, it’s turned, the stock price has turned around, um, [00:45:00] it’s looking like a kind of Nike swoosh at the moment, long decline down the, um, down the main part of the logo, and then just.

[00:45:06] Tony: Turning up at the bottom. So that’s the business. Um, if I look at the numbers, the share price I did the analysis at is, was 83 cents, which was less than consensus target, very low yield of only 1. 81%. So we can’t score it on that. Stock Doctor, Stock Doctor financial health wasn’t strong. It’s currently in their early warning category.

[00:45:28] Tony: And it’s been there for a long time. So it’s not going to score on the financial health, um, Dimension, which is a bit worrying in itself, but anyway, um, but it does score because it’s a recovering financial health. So I’ve spoken about that before. I tend to like recovering financial health. Um, it does, it does mean the management are dealing with their problems and they’re concentrated on the financials and trying to write them.

[00:45:52] Tony: If I go through the numbers, the ROE for this company is only 2. 5%. Not that we use that in our scoring, but it’s, um, it’s a very [00:46:00] low Uh, Margin, Business, and that’s one of the things which works, um, against it, I think, in some ways. Um, however, PropCaf is 5. 39 times, so this is going to score well from the valuation metric, but thin on the ground from the, um, the sort of business performance side of things.

[00:46:19] Tony: Uh, The share price of 83 cents isn’t below IV one or IV two, so we can’t score it from that point of view. Uh, but it is below the net equity per share plus 30, which is 98%, 98 cents, sorry, net equity per share, plus 30%, which is 98 cents. So it’s, IT scores from that point of view. So on the valuation side, not too bad.

[00:46:41] Tony: Uh. The other thing it scores well for is earnings per share is forecast to grow and almost triple over the next year or so. So whether we believe that or next year’s annual report starts with, uh, despite the problems we’ve had in our big contract with so and so, we, our management have got us through it.

[00:46:59] Tony: We look forward [00:47:00] to the future. But anyway, they’re forecasting a large Forecast, uh, uh, increase the forecast. Increase in earnings per share is 270%, which is good, which means we score it for growth over pe, which in this case is 6.16. Um, when the threshold is 1.5, before we scare it, uh, score it. So that’s good.

[00:47:19] Tony: Uh, don’t have an owner, founder directors only hold 1%, so we can’t score it for that. Interestingly enough, the PE on this company is 45 times. Um, which we, which we can’t score it for. It’s not the highest or the lowest though, funnily enough. But that’s a huge lot of cash coming in that doesn’t make it to the bottom line.

[00:47:37] Tony: Um, which is an interesting sort of telling sort of thing in itself, and I’ll come, I think the reason in this might be that it might be like the one I did last week, the pulled pork last week, where I spoke about Data 3, where they tend to have Large contracts where, uh, you know, basically they get large revenues from supplies and then pay that, sorry, large revenue [00:48:00] from customers and then pay most of it back to suppliers on, on their thin margins.

[00:48:03] Tony: I think that might be going on here as well, uh, because you can look at the operating cash flow and it, um, if you break it down, there are large, uh, sales to customers, but then there are large payments to suppliers and the cash flow that’s left is, uh, you know, quite tiny compared to the billions going in and out of the account.

[00:48:21] Tony: On top of that, it looks like there was a tax refund this year of some, uh, 44 million, which is boosting operating cash, uh, which was about, operating cash flow, I think was about 90 odd million. So, um, it’s, it’s possible it’s in one of the companies, those companies that have a good, a good half or a good year from a PropCaf point of view, and then it disappears again into the future.

[00:48:44] Tony: Uh, But yeah, definitely a thin, a thin margin. Net profit for this company was 0. 58 of a percent this year. So look, the risks, um, well, sorry, I should give you the score. All in all, uh, well, sorry, it did score for a new [00:49:00] upturn and didn’t score for consistently increasing equity. All up, it was 11 out of 16 or 69 percent, uh, for the quality score and the QAV score was 0.

[00:49:10] Tony: 13. So towards the bottom of our buy list, um, I think the risks on this are. probably self explanatory from what I said that this company operates on razor thin margins and therefore if there’s a mistake it doesn’t have a big buffer to trade its way through it without damaging the profitability. But they have also called out in their in their recent statements that inflation is impacting on their business and I guess that may be because a lot of the contracts are fixed price and were put in place.

[00:49:41] Tony: Before inflation was as big an issue as it is now, but even if that’s not the case, they are also calling out that it’s difficult to find labor at the moment. There’s a labor shortage going on in their engineering businesses. So a couple of risks there. On the positive side though, they are forecasting a big increase in earnings.

[00:49:58] Tony: So if we [00:50:00] take that at face value, then the shares should go up based on the earnings increasing next year. So on the buy list, may not be there next half. Um, raise the thin margins.

[00:50:11] Tony: Um, does have a history of being volatile, uh, but does have a forecast to, um, improve profit next, uh, next year and is trading at a very low PropCaf.

[00:50:21] Tony: Ha

[00:50:21] Tony: ha

[00:50:22] Cameron: And I own it in my Super Portfolio. nearly a rule one sell for me. I think on Friday, but it’s rebounded a bit today, so I’ve still got it.

[00:50:34] Tony: Okay.

[00:50:36] Cameron: Hopefully, now that you’ve done that, it’s going to go to the moon,

[00:50:39] Tony: Yeah,

[00:50:41] Tony: right, Well, I’ll do Blue Scope

[00:50:43] Tony: Steel next

[00:50:43] Tony: week, which, unless something

[00:50:45] Cameron: I looked it

[00:50:46] Cameron: up. You did it in

[00:50:47] Cameron: December.

[00:50:48] Tony: I thought so, okay, I won’t do it then. I’ll try and find something else.

[00:50:51] Cameron: Good luck with that.

[00:50:52] Tony: Yeah,

[00:50:55] Cameron: Well, that’s it.

[00:50:55] Cameron: We have no, uh, questions this week. Again, [00:51:00] people are too depressed to ask questions, so, um, After Hours, Tony, Melbourne Cup Tips.

[00:51:06] Tony: well that’s the question on everyone’s lip is that’s the unstated question out there is

[00:51:09] Cameron: the only thing anyone’s

[00:51:10] Tony: what does Ruddy tip for the Melbourne Cup?

[00:51:15] Cameron: and,

[00:51:16] Tony: Oh well, Ruddy’s tip, he likes the Japanese horse called Breakup. That’s his tip for the Melbourne Cup. My tip is vow and declare. Which has had some terrific runs recently and, uh, it’s got a good weight. It won the Melbourne Cup a couple of years ago. Um, so I like Vow and Declare and my best ruffy is a horse called Virtuous Circle, which is about 200 to one.

[00:51:39] Tony: Um, it’s, uh, hasn’t.

[00:51:41] Cameron: a roughie?

[00:51:42] Tony: Uh, a horse at long odds that could still win. The value, the value proposition, not the quality, the value proposition. Um, so virtuous circle. So it’s not unusual for a horse at very triple digit odds to run a place in the Melbourne Cup. So virtuous circle might be that horse this time and [00:52:00]certainly gets into the very low weight given its form, not its recent form, but its form

[00:52:05] Tony: behind that.

[00:52:06] Tony: And it’s a New Zealand bred horse and they tend to breed, stay as better than we do. So vow and declare to win virtuous circle each way. That’s my tip.

[00:52:14] Cameron: Right. Well, good luck with that. Tomorrow, we’ll see how you go this year, and Breakup is Ruddy’s, uh,

[00:52:24] Tony: yeah. And he, the reason I’m giving you Roddy’s tip is he tipped GoldTrip last year. Which one? And it’s back in this year. He likes Gold Trip again this year, but he likes

[00:52:35] Tony: Breakup better.

[00:52:36] Cameron: Right. What’s his long term track record like,

[00:52:40] Tony: Well, he lives in Wagga Waggas, and

[00:52:43] Tony: they’re slowly traded down from Brisbane, Sydney, and Melbourne, so you get

[00:52:48] Tony: a

[00:52:48] Tony: fair idea. It’s not funny, his lavish

[00:52:51] Tony: lifestyle.

[00:52:53] Cameron: I don’t want to cast dispersions on Wagga Wagga. Sure. It’s a very lovely place to

[00:52:58] Tony: it is, he’s one from one at [00:53:00] the moment, which is better than

[00:53:00] Tony: me.

[00:53:01] Cameron: particularly if you’re sleeping with the, uh, Premier of New South Wales, Wagga Wagga a place to be.

[00:53:07] Tony: He went out on Friday night to, um,

[00:53:08] Tony: the conservatory of music or something to see a school concert. And he came away and I said, how was it? And he said, Oh, it was money well spent by Gladys and her boyfriend.

[00:53:18] Cameron: There you go.

[00:53:20] Tony: Yeah. What about you? What have you

[00:53:21] Tony: been seeing or watching or

[00:53:23] Cameron: We went to the Sparks concert, came to Brisbane for the very first time last Thursday night, Chrissy and I and Fox all went. Cause Fox is a bit of a Sparks fan too. Um, and it was fantastic. I want to thank Jeff, QAV club member down in Melbourne who, uh, gave me notice that the tickets were on sale and I grabbed them.

[00:53:51] Cameron: That was my birthday present to myself was to go see Sparks this year. And, um, it was fabulous. A great night. Very, very, [00:54:00] very great night. One, one to remember.

[00:54:03] Tony: really? Wow. What was special about them? Because my memory of them is, um,

[00:54:08] Tony: the time MTV launched, and they had some,

[00:54:11] Tony: uh, a clip called Beat the Clock, I think it was called. It was just on continuous rotation, and I got thoroughly sick of seeing and watching, waiting for something else to come on

[00:54:19] Tony: MTV.

[00:54:21] Cameron: right. Well, um, It’s like, I mean, I guess it’s, they, they were very entertaining for I mean, you know, you’ve

[00:54:29] Cameron: seen the documentary, they’re a bit of a, they’re sort of somewhere between a comedy act and real music, like their songs have always been heavily

[00:54:41] Cameron: dosed with. sarcasm, and their lyrics, uh, are very, very funny.

[00:54:49] Cameron: Like every song typically is kind of sarcastic and funny and is a, is a, some sort of a

[00:54:56] Cameron: commentary on modern life. And they have been going since [00:55:00] 1971. They’ve, put out 26 albums. Uh, so two, for the people who don’t know Sparks, two brothers, Russell and Ron Mayle, been going since 1971, as I said, um, Russell’s the singer. He’s 75. Ron, his older brother is 78, I think. He’s the songwriter and plays keyboards.

[00:55:22] Cameron: Russell bounced around the stage for the full 90 minutes, jumping, singing in this high falsetto, gave it 150 percent performance, like insane amount of energy for a 75 year old. I, I think I would be flat out bouncing around the stage for 90 minutes like that, but doing it and singing in a high falsetto through most of it, forget about it.

[00:55:46] Cameron: I couldn’t do it. Ron sits there. Ron’s whole shtick has always been to look like he’s totally bored. He used to have a Hitler mustache. Now he’s got a very thin, tiny mustache at the top of his lift. He’s wearing a suit [00:56:00] jacket, dress shirt, and a tie, and then comfy tracksuit pants red Nike sneakers on He looks completely bored for the whole night, except when he gets up and does a dance in the middle of one song. He does his patented dance, uh, with his big shit eating grin on his face. then he. Stop suddenly, gets the Dowel, look back on his face, turns around and back down and sits down at his keyboard.

[00:56:25] Cameron: So it was very, very entertaining. And the songs are great. If you’re a Sparks fan, you know, you love the songs. There’s a lot of really good sing along tracks. But I think the big thing is, you know, everyone knows that they have just struggled. They’ve never really had a big break in the 50 years they’ve going.

[00:56:44] Cameron: They just kept doing it.

[00:56:46] Cameron: had enough of a cult audience that they could just keep doing it year after year after year. And then Edgar Wright put out his documentary during COVID and now they’ve got this, now they’re playing at [00:57:00] Glastonbury, they did the Sydney Opera House. They’ve, it was their first time in Australia in like 20 years.

[00:57:06] Cameron: They’ve got this um, massive New global audience now. They’ve in their mid to late seventies, finally made it. And it’s just, I don’t think everyone there’s just a lot of love for them. Like, you know, congratulations.

[00:57:20] Tony: Right, it’s

[00:57:20] Cameron: you finally got there just by persisting for 50 years, you got there. And now they have this massive, um.

[00:57:29] Cameron: Global fan base and love for them. And yeah, it was kind of, I think everyone who went to see them goes to see them just to applaud their, um, persistence and, you know, their story, their journey, just doing what they’ve been doing, million different musical styles, but always the same sort of thing. Like they’ve always just, Ron just writes these highly sarcastic songs.

[00:57:55] Cameron: Um. And they were also pioneers with electronic [00:58:00] music and all this kind of stuff, as Edgar Wright’s documentary pointed out. They’re like, a lot of very famous musicians, uh, look to them, look to Sparks for inspiration, all that kind of stuff. Anyway, that was good.

[00:58:11] Tony: Yeah. good. And, uh, speaking of people who are 78, I watched the Sylvester Stallone

[00:58:17] Tony: documentary last night, Sly,

[00:58:19] Cameron: Yeah, that like?

[00:58:20] Tony: looks like it’s been put out to copy Arnold Schwarzenegger’s documentary, but it was good. It’s a good documentary, a good story, but he’s

[00:58:26] Tony: 78 too.

[00:58:28] Cameron: really,

[00:58:29] Tony: yeah, and, you know, talked about, they showed sort of x rays from his back where he’s got four or five bolts put in it, and he’s really taken a beating from

[00:58:38] Tony: being an

[00:58:38] Tony: action

[00:58:38] Tony: hero.

[00:58:39] Tony: Like,

[00:58:40] Cameron: Oh, yeah, like I’ve always admired his story, like I admire

[00:58:43] Cameron: Schwarzenegger’s story, like, the whole story about how he wrote Rocky and,

[00:58:48] Cameron: you know, demanded that, uh, he play, he star in it as well, he’s down on the bones of his ass, and, you know, it’s a great, it’s a great story. Yeah, he

[00:58:58] Tony: It’s worth watching. Quentin Tarantino’s [00:59:00] in it, which

[00:59:01] Tony: is always energetic and enjoyable to listen to. He about the Lords of Flatbush, which was

[00:59:06] Tony: Stallone’s probably, you know, first screen role that we

[00:59:08] Tony: would know. Uh, yeah. And, um, yeah, it’s, it’s, it’s, it’s worth watching.

[00:59:14] Cameron: Except Death Race 3000. Which I a year or so ago. It was one of the, um, Roger Corman’s low budget science fiction, dystopian things, and Stallone, very young Stallone, is sort of one of the over the top bad guys in this race car match. Him and, uh, David, um,

[00:59:40] Tony: Paradine.

[00:59:41] Cameron: Carradine, thank yeah. Who? Like that film came out in the mid 70s and he basically looks like Darth Vader.

[00:59:50] Cameron: Came out a couple of years before Darth Vader, before Star Wars. He’s basically wearing Darth Vader’s costume. And we know that Lucas worked for Corman, as all those guys did. Lucas [01:00:00] and Spielberg and Coppola, they all came up working for Roger Corman. Um, James Cameron, um, uh, the guy who made Scarface, what’s his name?

[01:00:12] Tony: No, Brian De Palma.

[01:00:13] Cameron: De Palma.

[01:00:14] Cameron: thank you, yeah. So, yeah, anyway.

[01:00:18] Tony: And you mentioned it was your birthday. I think I, I think I missed it. I’m sorry to say, so happy birthday for a couple of weeks ago,

[01:00:24] Cameron: That was a month ago,

[01:00:24] Tony: have, a month ago,

[01:00:25] Tony: sorry.

[01:00:26] Cameron: yeah, over and gone. Don’t worry about it. I try and ignore my birthdays as much as possible.

[01:00:32] Cameron: Uh, my only other tips this week, oh, the Beatles

[01:00:34] Cameron: track. What did you think of the new Beatles

[01:00:35] Cameron: track?

[01:00:36] Tony: Yeah,

[01:00:36] Tony: big yawn, I thought, and overhyped.

[01:00:39] Cameron: Yeah,

[01:00:40] Tony: putting out that

[01:00:40] Tony: documentary as well, which we’ve pretty much seen from get back

[01:00:43] Tony: anyway. Uh, yeah, it makes me think of Paul McCartney being a businessman first and a musician second when

[01:00:50] Tony: I see

[01:00:50] Tony: things like

[01:00:50] Tony: that.

[01:00:52] Cameron: Yeah, look, it was, it had some sentimental value, I guess, to hear. Them playing together, [01:01:00] but, uh, I was really, uh, I really thought maybe this time, this is the last ever Beatles single we’re ever going to hear. Maybe they’ll really knock it out the park.

[01:01:09] Cameron: Not really.

[01:01:11] Tony: it was definitely a B side, wasn’t it?

[01:01:13] Cameron: Oh, if that, like I, you know, John’s thing is nice. And I was waiting for Paul to come in with the Paul verse. Key change, little bit upbeat. Because it’s kind of dirgey, it’s slow and melancholy. Paul comes along. Woke up, got out of bed, dragged across my head.

[01:01:30] Cameron: No. No, like, really, like, it just needs George Martin.

[01:01:34] Cameron: I mean, Giles Martin is great, but it really needs George, I think, to go. Alright, this is boring. Let’s, uh, it up a little bit.

[01:01:42] Cameron: I think.

[01:01:43] Tony: Yeah,

[01:01:44] Cameron: He was more of the magic than

[01:01:45] Cameron: we often give him credit for.

[01:01:47] Tony: And that’s the thought I had when I saw Paul McCartney last week in concert. Like, there’s this. When you’re watching the songs, you sort of get the feeling there’s an orchestral quality to them. There’s

[01:01:58] Tony: a classical [01:02:00] music. It comes through like a subtext out of some of the songs.

[01:02:03] Tony: hard to explain, but, um, that’s the feeling I

[01:02:06] Tony: had. And, uh, that must’ve been the George Martin

[01:02:08] Tony: input coming through.

[01:02:12] Cameron: And I think Giles, his son, is a great producer, uh, and a good, um, curator, I guess, of their work and his father’s work. But, you know, George had a certain level of authority with the boys in the sixties and they respected him. And I think he had a lot of import into the final product, which, um. Or maybe, at least towards the very end, like in the get back sessions and that kind of stuff, I think his had dwindled to a certain extent.

[01:02:43] Cameron: Anywho, uh, look, my other, my music tip for this week is a French jazz trumpeter I’ve just discovered, Eric Trefaz. Been around for a long time. I think his first album came out in the early 90s. I’ve just discovered him. Very, uh, [01:03:00] similar to Miles’s really mellow, uh, Uber cool Myles, Spanish Steps, uh, that kind of stuff.

[01:03:10] Cameron: If you, if you like really mellow Myles Davis, check out Eric Trefaz. It’s nice sort of working background music or dinner music. He, he, he has a, he mixes it up a little bit with some modern beats, you know, every now and again, but it’s really just this atmospheric, slow, muted trumpet. A lot of it. Very good.

[01:03:34] Cameron: It’s like having a whole new Myles catalog to listen to.

[01:03:38] Tony: Wow.

[01:03:38] Cameron: And my TV recommendation for people who like really out there comedy, like people who like, I’d say Python and Mr. Show. If you don’t like those, don’t check this guy out, but have you seen I Think I Should Be Leaving with Tim Robinson on Netflix?

[01:03:55] Tony: No,

[01:03:56] Cameron: He’s done about three seasons. He’s an ex SNL guy. He [01:04:00] did like one season as a performer on SNL, then he was a writer. He’s got the show. It’s produced by the Lonely Island guys, Andy Samberg, etc. But it is, it is the zaniest, um, sketch comedy series I’ve seen, I think, probably since Mr. Show. Uh, it’s very out there.

[01:04:25] Cameron: Um, he plays these characters that are generally very angry and unhinged in, uh, social settings, but it’s,

[01:04:33] Tony: no. Perb your

[01:04:34] Tony: enthusiasm

[01:04:35] Tony: style or

[01:04:37] Cameron: Way more unhinged. Yeah, like a complete level. Larry’s just an asshole, um, and, doesn’t give a shit. This guy’s unhinged, uh, he plays these unhinged

[01:04:48] Cameron: characters in, you know, various social and work settings, but it’s, it, the thing I like, I like comedy where they take a strange idea. And then just [01:05:00] push it, and push it, and push it, uh, beyond where it should be pushed. Where it’s, it just becomes annoying for character to just keep pushing the same bad idea over and won’t let it go. You know, people who just can’t let something go? They just… Want want to do something because they want to do it, and they’ll just keep doing it.

[01:05:25] Cameron: Not give a shit about the consequences. They’ll just keep pushing. No, no social awareness.

[01:05:31] Tony: Like sparks.

[01:05:34] Cameron: Okay, I think they do it with full awareness of doing.

[01:05:41] Cameron: Well with that, uh, that’s all I’ve got to share, Tony. ASX to you.

[01:05:47] Tony: happy ASXCAM, and send some questions in next

[01:05:49] Tony: week, that’d be great, people.

[01:05:51] Cameron: Or don’t,

[01:05:52] Tony: Or don’t, yeah.

[01:05:54] Cameron: whatever. If you don’t, have any that’s fine. Happy ASX everyone. [01:06:00]QAV a good week.

[01:06:00] Tony: Yep. See ya. [01:07:00]

LAST WEEK’S EPISODE

FREE EDITION:

In the Club edition:

Pulled pork DTL; what TK looks for when he does a pulled pork.

Episode Transcription

QAV 644 Club

[00:00:00] Cameron: Welcome to QAV, Tony, episode 644, the 31st of October. It will be ended. That’s the name for this episode, Tony.

[00:00:22] Tony: Yes, it will be ended at some stage. Or it will just end, it will end at some stage.

[00:00:29] Cameron: I posted a quote from, uh, science writer Verna Vinge on Facebook the other day, Tony. Was offended by his grammar. ChatGPT told me it was fine though, so, I, uh, I don’t know. Don’t know who to believe, you or ChatGPT.

[00:00:44] Tony: I mean, I, I was reasonable familiar with that quote and I always cut up some slack cause I thought, well, you know, maybe Vinger is not speaking in his native tongue or something or, you know, but yeah, it always struck me as a really strange quote. The human era will be ended. It’s like, why don’t you say the human era [00:01:00] will end?

[00:01:01] Cameron: Because it will be ended by something else, by

[00:01:05] Tony: Well, then say that!

[00:01:07] Cameron: Well, it was inferred in the sentence. Superintelligent machines will arise and the human era will be ended. I think it

[00:01:16] Tony: era will end. That’s inferred too.

[00:01:21] Cameron: yeah, I guess you could say, yeah, that’s arguable.

[00:01:24] Tony: Anyway, I was just always told when you write something, don’t spend a dollar, spend 50 cents and say it with less words.

[00:01:31] Cameron: Hmm, Mark Twain who said I would have made this letter shorter, but I ran out of time. Well, Tony, it’s been another dismal week for investors and on the stock market. Uh, we’re speaking at about. 3 o’clock in the afternoon, Sydney time, and the market’s down to, uh, 6, 9, 6, 1, [00:02:00] uh, give or take. Um, a week ago it was up over 7, 000, 7, 080, so it’s lost about 100. points. You know, uh, over the last week, uh, I think over the last year now, uh, we’re sort of, sort of basically where it was a year ago.

[00:02:18] Cameron: No, it’s less lower than where it was a year ago. Lower than where it was, a lot lower than where it was two years ago.

[00:02:24] Tony: It’s less than where, it’s about where it was in 2007 before the GFC. In fact, it may even be lower.

[00:02:29] Cameron: Right. Well, I don’t know. What do we, what do we, what do we have to do? What do

[00:02:37] Tony: Yeah.

[00:02:37] Cameron: do to get it to turn around?

[00:02:41] Tony: I wish I knew. Maybe all the QAV subscribers can buy on the same day and push the share price up. Then we can, we’ll GameStop it.

[00:02:52] Cameron: Yes.

[00:02:54] Tony: we’ll get momentum that people can buy into and then we’ll sell out.

[00:02:57] Cameron: Yeah. To the, to the moon. Hold on a [00:03:00] second. Can I help you, sir? Oh, why are you in here then? You heard a robber in the house. Okay, well, go and tell him to take some of your Lego, because I’m sick of standing on it.

[00:03:16] Tony: How come he’s home?

[00:03:19] Cameron: Oh, it’s a long story, but, um, so, last week, he and his best friend and a bunch of kids were playing Tiggy at school. Fox tiggied his best friend a little bit too hard and his friend fell over and put his hand out and broke his wrist.

[00:03:36] Tony: Ooh. Oh.

[00:03:37] Cameron: He’s got a sling on it, and he had to have a follow up at the hospital today because they were a little bit concerned with how he was healing.

[00:03:46] Cameron: But both of his parents have COVID. So, Chrissy picked the kid up and took him to… Uh, the hospital and they were there for four or five hours and Fox went along too. It [00:04:00]was like, his appointment was at eight 30 this morning. So Chrissy and Fox and this kid Jack were there all day. And by the time they got out of it, they just thought, well, there’s no point going to school.

[00:04:10] Cameron: So they just, she took Jack home and, and his mother is one of Fox’s teachers, so she was home anyway. So anyway, yeah,

[00:04:20] Tony: Yeah, well,

[00:04:20] Cameron: bit of a. Bit of a drama day. Okay, um, yes, back to the market. So, yeah, it’s, uh, I don’t know, just, we don’t seem to be able to get a win at the moment. It’s just one thing after another.

[00:04:37] Tony: correct.

[00:04:40] Cameron: Well,