Hello QAVvers

It’s another Tuesday.

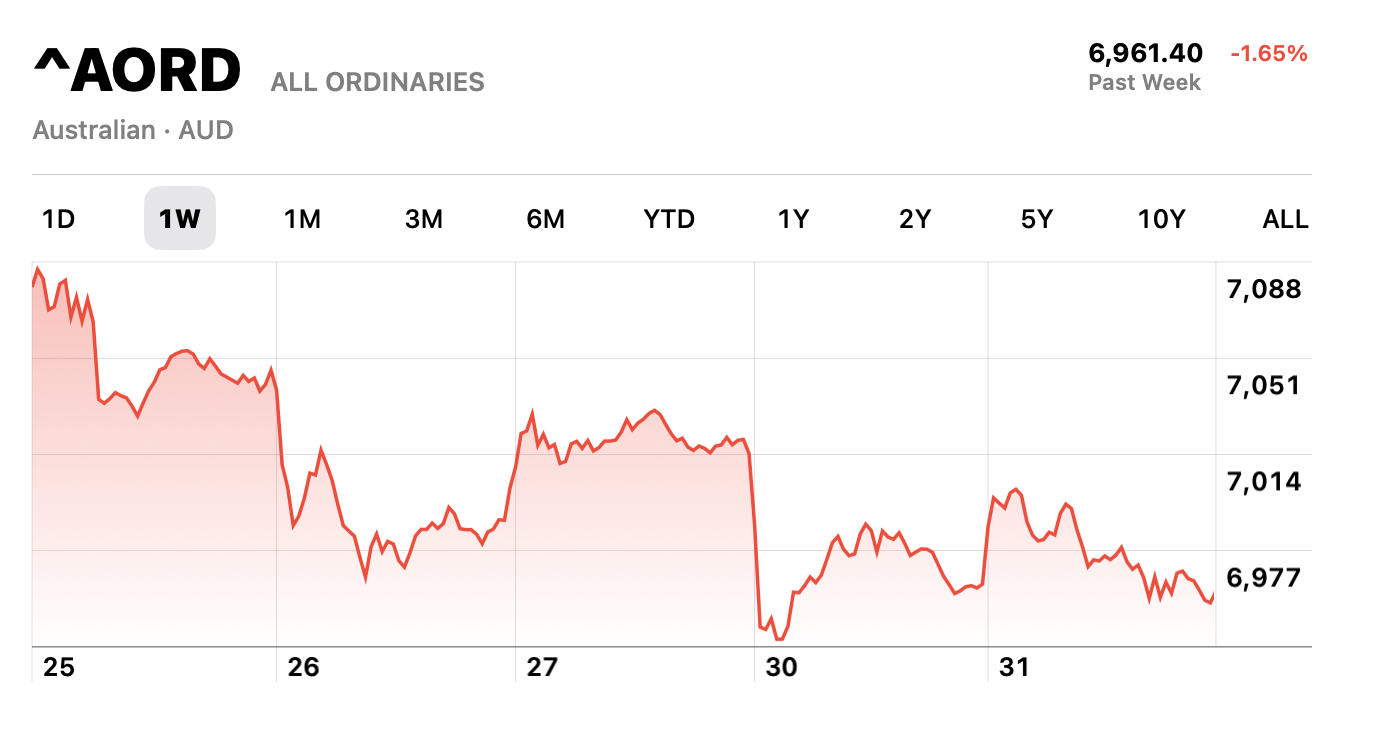

Another dismal week for the AORD.…

As TK pointed out when we recorded today, it’s almost back to where it was in 2007 before the GFC.

Let’s have a look at the portfolio.

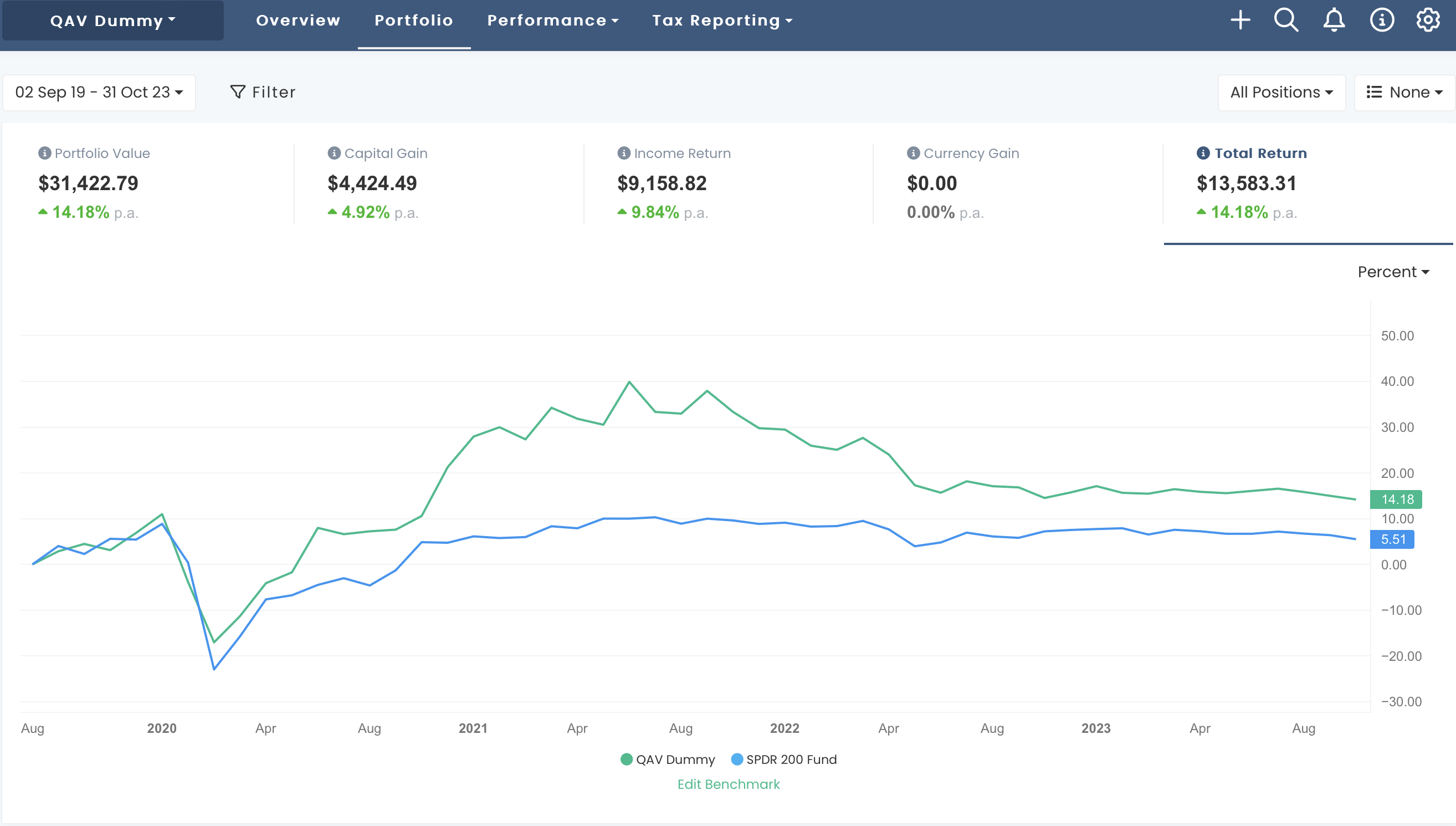

QAV PORTFOLIO REPORT

The Dummy Portfolio is performing well against the benchmark over multiple time frames.

SINCE INCEPTION (02/09/2019)

Our portfolio is still doing about 2.5x the STW since inception.

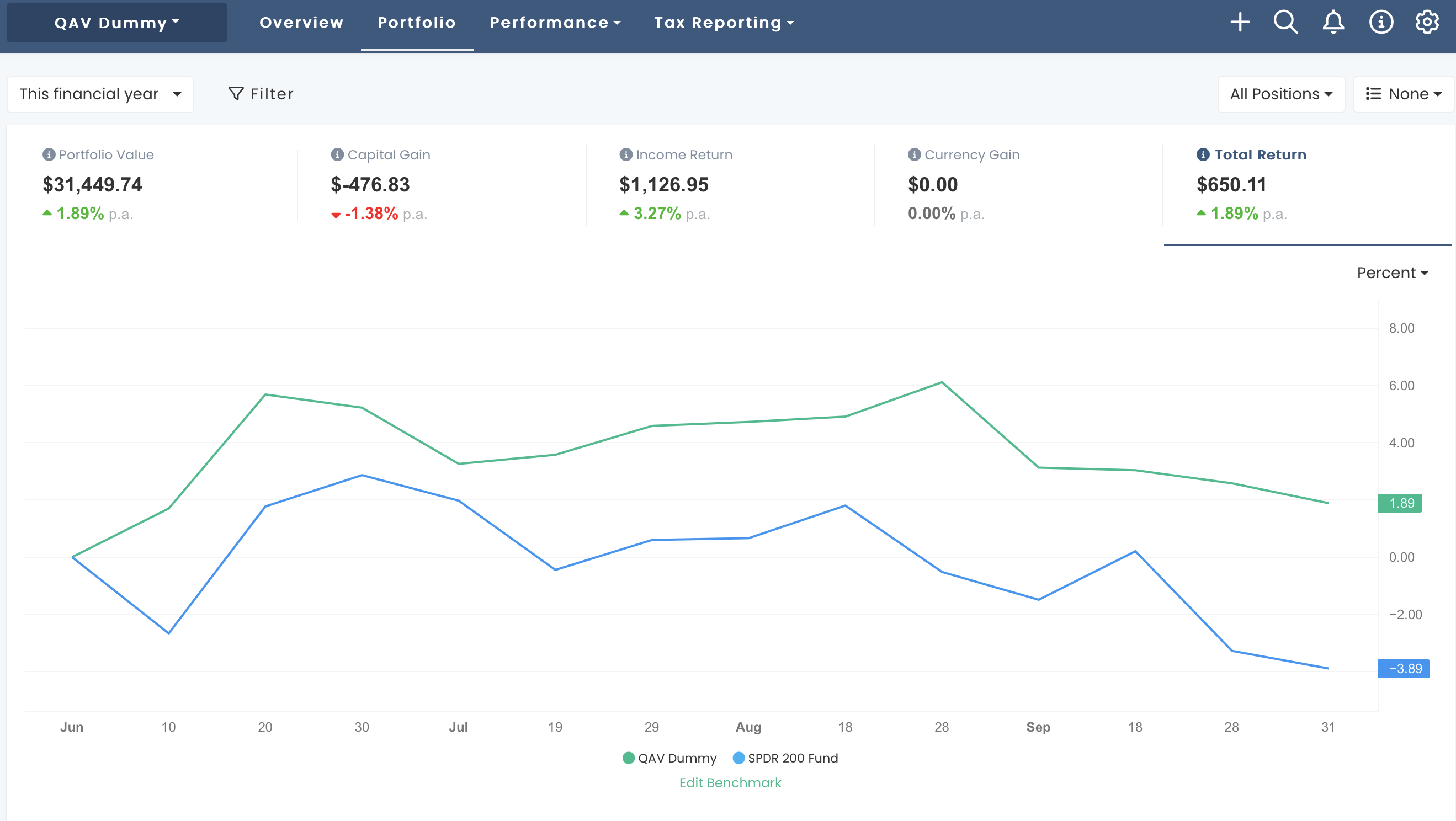

FY REPORT

Despite all of the gloom, for the FY we’re doing much better than the STW.

RECENT TRADES

In the last 7 days we sold NHC and OML and added SUL and PRU.

FREE WEBINAR

I’ll hold another one in a few weeks.

STOCKS OF THE WEEK

During the last week, we also traded some stocks in our Light portfolios. Details here.

** As always, please check our work, DYOR, and consult a financial advisor before making any investing decisions.

BUY LIST

Each week we produce a buy list that we share with our members. The intended primary purpose of this buy list is for club members to use as a reference for comparing their own buy list. In theory, all of our buy lists should look pretty similar each week.

As always, please check our work, DYOR, consult a financial advisor before making any investing decisions.

THIS SECTION CONTAINS CONTENT WHICH IS VISIBLE TO QAV CLUB SUBSCRIBERS ONLY.

LAST WEEK’S EPISODE

FREE EDITION:

We’re in a technical correction; staying fully invested; CCP collapse; new 3PTL sells number jumped this week; Pulled pork RRL; the performance of AFI.

In the Club edition only: Is being rich a superpower?; staying enthusiastic during a long downturn; how TK differentiates between quality and value; the value/risks of a concentrated 10 stock portfolio; WWTD if he had cash but a full portfolio?

Episode Transcription

[00:00:00] Cameron: Welcome back to QAV. This is episode 643 TK. Do you have a superpower, Tony?

[00:00:11] Tony:

[00:00:11] Tony: Uh, I like, um, if I’ve got one it’s the same as Ricky Gervais, not giving a fuck.

[00:00:17] Cameron: it’s not like Anthony Pratt. You’re just rich. That’s his superpower, apparently.

[00:00:22] Tony: No, not in that league, that’s for sure.

[00:00:23] Cameron: You’ve been reading these, uh, Pratt stories that have been coming out this week.

[00:00:27] Tony: certainly gives credence to all the conspiracy theorists who believe the rich are controlling the world, that’s for sure.

[00:00:32] Cameron: Yeah, you know, he seems to be on record saying that he throws his money around in order to have influence with everyone from King Charles to Donald Trump to who knows who,

[00:00:46] Tony: Yeah, I’m not sure what buying influence with King Charles actually gets you as a business person, really.

[00:00:50] Cameron: King Charles on the speed dial. You know, you know, you want me to, I can make a, I can make a call to King Charles, he’ll, he’ll answer my call, get your credibility in a room. [00:01:00] It’s like that old, that old story about the, uh, I can’t remember who I first, I’ve heard lots of different versions of this, but this, the story of the, uh, guy in the restaurant in Sydney, Kerry Packer walks in, guy’s sitting there at the table, he sees Kerry Packer walk in.

[00:01:17] Cameron: And he, Kerry sits at a table by himself. The guy gets up and he goes over to Kerry. He says, Mr. Packer, sorry to interrupt you, but, uh, my name’s John. Huge fan of yours. Been following your career for decades. Listen, uh, you don’t know me. You don’t know me anything, but just wondering if you could do a fellow businessman a favor.

[00:01:35] Cameron: Like I’m, I’m trying to close this big deal. Got a client going to meet me for lunch. This could be make or break for me. I’m just wondering on your, we’ll probably be here for a while on your way out. If you wouldn’t mind just, you know, stopping at our table and saying, hey John, how’s it going? It’ll give me a huge amount of credibility and help me close the deal.

[00:01:55] Cameron: And Kerry’s like, yeah, all right. You know, he’s, he’s having a good day. Just, I don’t know, he just sold Channel 9 to [00:02:00] Alan Bond or something. He’s feeling pretty good. Yeah, all right, mate. So now later Kerry finishes his 25 courses and he gets up, he walks out, he stops at the table and he pats this guy and he goes, hey John, how’s it going?

[00:02:11] Cameron: John looks over, he goes, fucking hell, Kerry, I’ve told you, don’t interrupt me when I’m in the middle of a meeting.

[00:02:21] Tony: Oh, that’s gold.

[00:02:22] Cameron: does that with, Go does that with King Charles, maybe that’s Anthony Pratt’s model. Well, enough levity for this show, it’s been another dismal week on the ASX, Tony, uh, market has been down yet again, ticking up a little bit today, but, uh, not, you know, not

[00:02:41] Tony: Well, thank goodness

[00:02:41] Cameron: impact on the week.

[00:02:44] Tony: it has ticked up today because today is the anniversary of Black Tuesday in 2007 when the US stock market overnight dropped 20 percent in one session. Hmm.

[00:02:57] Cameron: that was, uh, thought the [00:03:00] GFC wasn’t until 2008, what, what

[00:03:02] Tony: No, it started in 2007. Yep. I’m not sure what the catalyst would have been, but it was probably going to be something like, uh, Lehman Brothers not being bailed out, or there was the bank in the UK which also wasn’t bailed out and went broke. Northern Rock, I think it was called, something like that. Yeah. So,

[00:03:21] Cameron: Mae and Freddie Mac and all of those came later.

[00:03:24] Tony: And Alan, I don’t know if you, I just happened to have the ABC News on last night when I got in at 7. 30 and Alan Cole does his shtick on at the end of the news on the business and he showed a graph of this year versus 2007 and it’s, you can overlay one graph on the other. And this was leading up to yesterday before Wall Street opened.

[00:03:45] Tony: So it was like, I woke up this morning and went, phew, history didn’t repeat.

[00:03:51] Cameron: Right. Well, I’m looking at the one year chart. The ASX is almost back to where it was a year ago.

[00:03:59] Tony: Mm hmm.

[00:03:59] Cameron: [00:04:00] If I look at a two year chart, it’s down about 10 percent from where it was two years ago. A 5 year chart, it’s up a little bit, maybe 10 percent from where it was 5 years ago, but it’s uh, you know, not, not a great looking chart, that’s for sure.

[00:04:18] Tony: Yeah. Well, I thought you were going to cheer me up today. After all the problems in the market.

[00:04:24] Cameron: No, no cheering up to be done, Tony, I saw in the… ABC yesterday, Australian share market moves into a technical correction as war and inflation realities hit home. Technical correction is a bit of a financial markets jargon for a market fall from a recent peak of 10 percent or more. ASX200 hit an all time high of 7, 628, August 13, 2021, and a peak of 7, 558 on February 3rd this year.

[00:04:58] Cameron: But as of [00:05:00] yesterday, it had fallen 10 percent since then. Not sure what today’s slight gains mean, but, uh, yeah, it’s been a, been a hell of a couple of years.

[00:05:10] Tony: Yeah, and we were talking off air before about how this reminds me of the GFC, and we had an accelerated version of this going into COVID, um, and I guess the process helps us through all this, but it’s just hard losing money while you’re waiting for it to go to cash and find things to buy, and it could be a long way off, I just don’t know, but, um, yeah, I mean, good to have some more, some more levity, and, uh, I guess, you know, put things in perspective, at least we’re not, In Gaza at the moment or, um, Ukraine or, you know, out of job, out of work or whatever.

[00:05:47] Tony: So it’s, um, we’re complaining about losing a bit of paper money, which is, um, puts it in perspective, I think.

[00:05:54] Cameron: Well, how do you cheer yourself up in times like this, Tony, apart from giving yourself perspective?

[00:05:59] Tony: play more [00:06:00] golf.

[00:06:02] Cameron: Now that you’re off the booze, you can’t even drink to cheer yourself

[00:06:05] Tony: Well, probably a good thing during these times. I might trick myself to forget, but, um, anyway, look at Alex’s art. That’s the way they always cheers me up.

[00:06:14] Cameron: Hello, Alex. Welcome to the show.

[00:06:16] Alex: Oh, thank you. Thank you. Hello.

[00:06:18] Cameron: It’s a nice thing of your dad to say. Looking at your art cheers you up.

[00:06:21] Tony: yeah.

[00:06:22] Alex: Yeah, so it’s nice. Thank you.

[00:06:25] Cameron: Not, not looking at you, just looking at your art. No,

[00:06:28] Alex: Yep.

[00:06:31] Cameron: I thought he would have led with that myself, but you know.

[00:06:34] Tony: Alex knows as soon as she and I get into a room, we just. Giggle away, don’t we?

[00:06:39] Alex: We just giggle at each

[00:06:40] Tony: each other laugh.

[00:06:43] Cameron: Well you are very funny looking, I must say. The two of you have amused me no end. Ah yeah, there’s a lot of gnashing of teeth out there in QAV land, Tony, and I get it. I did a post yesterday about staying fully invested, and again, going back to those studies [00:07:00] about, you know, if you’re not invested in the 10 best days, what it does to your returns and the 20 best days.

[00:07:06] Cameron: Somebody sent me an email and said, yeah, but what if you’re not invested in the worst 20 days? It sort of accused me of cherry picking the data and I said, well, that’s a good point. It’s a fair point, but I think my reading of all of these studies is that what people tend to do is we have the worst days.

[00:07:26] Cameron: And then they capitulate after the worst days. It’s not like you can predict the worst days and you get out before the worst days happen. Although maybe there can be bad days and you get out and then the worst days come later on, but I don’t know. Do you think there’s any merit in the idea of just capitulation and missing out possibly on the worst days as well as the best days and it all balancing itself out over the long

[00:07:50] Tony: Well, it probably does balance out with both strategies staying in and staying out and trying to pick it. But yeah, it’s, I think it’s a fool’s game trying to pick the market. [00:08:00] But that probably does make sense that the market, if you look at the 20 worst days in the market, they’ve been pretty horrific.

[00:08:05] Tony: And if you’re in there, you’re suffering. And shareholders of CreditCorp last week would know how that feels, unfortunately. Uh, so yeah, there might be some merit in that. But yeah, luckily, well, at least for me, anyway, I got out of CreditCorp the day before it dropped because it crossed its three point trend line sell, which was probably as much of as luck as good management.

[00:08:27] Tony: But. But yeah, following the rules helps in this kind of time, I think, uh, because it takes the emotion out of it.

[00:08:34] Cameron: Yeah, um, so for I’m sure everyone did see this, but CCP collapsed last week, um, just after you said it was probably the one stock you would buy and hold onto for 10 years. I don’t know if that had anything to do with it. Um,

[00:08:49] Cameron: but yeah, across the three point sell line, I sold it from my own portfolio and the QAV portfolios, and then the next day it [00:09:00] dropped.

[00:09:00] Cameron: I think like 30%, maybe another 8 percent the day after. Um, I’ve got a quote here from somewhere. CCP was the worst large cap today, down 30 percent after revealing an anticipated 14 percent impairment of the carrying value of its US purchased debt ledged assets. The impairment is estimated to produce a one off reduction in CCP’s NPAD of 45 million.

[00:09:28] Cameron: Credit Corp said the impairment has arisen from a sustained deterioration in collection conditions. I mean, that seemed like a bit of an overreaction. I mean, I went back over CCP’s history because I knew, I know you’ve talked about this, um, when we’ve talked about CCP over the years. I think you’ve said before that, uh, the CEO tends to under…

[00:09:54] Cameron: Um, under promise and over deliver. Yeah. And if I look back, even over the last [00:10:00] five years, they’ve had a lot of big dips, lot, uh, beginning in April 22, they were trading at 30 bucks. Um, by June 22, they dropped down to 19. So that’s a 30 percent drop again. Then it recovered and then it declined again, recovered up to 24, then declined down to 17, uh, sort of from August to October.

[00:10:24] Cameron: So they’ve had lots of. Uh, you know, I mean, obviously leaving aside March 2020 when it dropped from 37 down to 9. 80, um, and then recovered back up to 33. They seem to have a lot of, uh, uh, quite a few big dips in recoveries over the last couple of years. But what do you, what do you think about a one off impairment?

[00:10:46] Cameron: Contributing to a nearly 40 percent decline in a matter of days. Is that an overreaction or is that a reasonable reaction?

[00:10:54] Tony: Well, it depends how you, you know, what point of view you come from. I think it’s an overreaction. However, um, [00:11:00] I called it a 10 year stock last week and it dropped. Um, my, I’ll give, I’ll give you my thinking for the 10 year stock and I’m, uh, this isn’t in no no, this is by no means me trying to Justify that position.

[00:11:13] Tony: I’m happy to admit that I was wrong with my timing on this one. However, I’ve seen Credit Corp and owned Credit Corp over the last 20 odd years. Um, Thomas Barighi, the guy who runs it, I think is one of the best CEOs I’ve seen. There’s probably only three or four people I’d put in that camp. People like Anthony Lascar, uh, Anthony Scali from.

[00:11:35] Tony: Nick Scali, um, maybe the, the, I think it’s the Wilson brothers who run Rees, uh, or the Wilson family who run Rees, the, uh, person who runs ARB, who I’ve, the names escapes me for the moment, but anyway, there’s not many top tier CEOs that I would look at and say they’re a good CEO. And my criteria is that they’ve been there for a long time through thick and thin.

[00:11:56] Tony: So they’ve grown up and down with the industry, uh, rather [00:12:00] than just sort of parachuting in for their four or five year stint from a different. CEO position and then leaving with a golden handshake. Um, and they, they’ve been, I guess, like, I’ll call it transparent and honest with their shareholders. They, they tend to over promise and under deliver.

[00:12:15] Tony: They tend to quickly tell you if there’s a problem. They tend to take that kind of punishment on the share price on the chin, but they ride it out. Uh, and if I look at I guess my perspective on CCP and its share price is if you look going back to the GFC, before the GFC it was trading around 12 a share, it dropped down to as low as 42 cents in the bottom of the GFC.

[00:12:38] Tony: So if you had bought it, Then, um, it got up as high as 35 before COVID hit. So that’s a, you know, nearly a hundred times increase in the share price in that, uh, in that period. And it did decline though during COVID back to 13. Um, which it recovered from somewhat. And now it’s back [00:13:00] around those levels now.

[00:13:00] Tony: So it’s, it’s definitely a volatile stock. And I think what tends to happen with CCP is people say it’s not a good stock to own during a recession or a downturn in the economy. And that’s certainly what they’ve, um, flagged happened in the U. S. So, and this is actually an alarm bell. I think it’s possibly a red flag on the U.

[00:13:19] Tony: S. economy, but what they said was that people are walking away from their debt replacement plans in the U. S. So, um, The way this business works is they buy… Uh, debt ledgers from companies like banks or credit card providers, and typically what happens is the bank or the credit card provider or the telco or the utility has decided it’s too expensive for them to collect the last, say, 20 percent of people who owe them money.

[00:13:46] Tony: They put resources into call centers, etc. to get most of the bills repaid, but then they just give up and they sell off. The rump and then Credit Corp buys it and other companies like Credit Corp and they go out and try and collect as much as [00:14:00] they can from that money. So they’re only paying usually pennies in the dollar to buy the debt ledger because they won’t.

[00:14:05] Tony: Collect a whole heap because some people just can’t afford to pay. Some people they’ll have trouble even tracking down. But the way CreditCorp works, and which I’ve always had a lot of admiration for, is they, they talk to the customers and they work out a plan. And then they, um, you know, they try and support the customer in achieving that plan and giving them some slack when they can.

[00:14:26] Tony: And then even to the point where over time they have a good credit. History or picture of this customer. And then I can actually lend that customer money, which is a growing stream of their business. So, you know, that’s, that’s far removed from the sort of mental picture I had of a debt collector when I was, you know, starting out before I bought shares in CCP 20 odd years ago, where I, you know, I thought people were going around with baseball bats and forcing people to.

[00:14:50] Tony: to make their repayments or under threat of physical pain or sending the sheriff around to repossess assets or whatever. And that’s not what CCP does. So they’ve been [00:15:00] quite, um, quite good and quite fair in this space. But what happens when people say, look, I just can’t abide by my Debt repayment plan, as they have in the US, and they’re walking away.

[00:15:11] Tony: I guess the impact on the person is, in the US in particular, is their credit score goes down, but it was already down because they fell into arrears with their credit card statement or whoever they owe money to, a bank or a utility. But it gets worse if CreditCorp then lists them as being a write off.

[00:15:29] Tony: So it does have an impact for people over there, but it’s at the stage now where the impact on their credit score is, is not worth trying to repay. Credit Corp on the repayment plan. So I’m going to draw the analogy that that’s a bit like when people were just handing back their house keys to the bank during pre GFC when I’m just going, look, I’m underwater on my mortgage.

[00:15:52] Tony: It’s not worth me trying to even ride this route here, have the keys back. So I think it’s a real. Canary in the [00:16:00] coal mine for the US economy, which is like, which is one risk, I suppose. And Credit Corp, you know, will therefore have difficulty collecting money if things do go into a recession in the US.

[00:16:11] Tony: And I think that’s what’s probably driving the share price decline at the moment. However, they will. Come through it and they will, um, what tends to happen is it, either the banks will stop selling off their distress lists until the economy writes themselves and they can get some money for them, or Credit Corp can buy them for a really, really cheap price and then almost sit on them for a couple of years and then collect outsized margins when the economy turns up again eventually, and they can collect money from people.

[00:16:40] Tony: Um, but it’s just that intervening period when we’re going into decline until we come out of the decline that people don’t want to own. Credit Court. Um, so my, my sort of feeling is that it’s one to watch when it does turn up again. It’ll probably have outsized returns. And my evidence for that is the GFC in COVID when, when you were getting [00:17:00] 50 times sort of returns by holding it for five or 10 years after those events, particularly the GFC.

[00:17:06] Tony: In terms of the one off payment to your question, Cam, the one off impairment, sorry. It’s an, it’s a non cash item. And basically what it means is that they paid all this money for debt ledgers in the US and they’re now saying that they’re, they’re worth less because going into the market for new ones, they’re paying less.

[00:17:25] Tony: And also too, they’re saying, well, we just can’t recover the kinds of debt repayments we can to justify the price that we bought it at. And so they’re writing it down on their balance sheet as an asset. And the only way to do that is to take a paper hit to your P& L. Double bookkeeping. You’re paying money to write down an asset.

[00:17:45] Tony: It’s got to come from somewhere. It comes from the P& L. But there’s been no dollars changing hand in the real world. No cash changing hand. So operating cash flow isn’t effective, which is what we focus on. So probably the more important thing [00:18:00] is that they’ve highlighted that they think that their income from the US debt collections will be 10 million dollars less.

[00:18:06] Tony: Then, um, they originally focused, or they originally, um, told the market, uh, last time they made, um, disclosures. So, it, but they’re still saying they expect to collect between 80 and 90 million, um, NPAT from the U. S., uh, down from 90 to 100. So, it… You know, it’s not, again, it’s not the end of the world as it currently stands, but people are extrapolating that forward.

[00:18:31] Tony: They’re saying if people are repayments, it’s going to get worse. If it gets worse, there could be more write downs, etc, etc. So it’s a kind of a, it’s um, people, I think the big end of town is saying, let’s get out of Credit Corp until things settle down in the economy, particularly in the U. S. And we, we can see it coming through the other side.

[00:18:51] Cameron: Well, let’s hope they’re wrong

[00:18:53] Tony: Well, I think I’m right. I think, I think the share price, you know, will, well, if the U. S. economy doesn’t [00:19:00] go bust and it’s looking like it may, um, then, uh, well, I mean, it’s always a two edged sword, right? I mean, that’s, that’s the second point I wanted to raise during this discussion is that, um, we’re really in an era of, of the economy being driven by central banks.

[00:19:18] Tony: And if, if the US economy does deteriorate quickly, uh, then the central banks will cut interest rates. And that may be a good thing for the stock market, won’t be necessarily a good thing for credit corp, but you know, it will be a good thing for the stock market. So it’s really hard to predict the secondary effects of what’s going on in the economy at the moment.

[00:19:38] Tony: But I think the, the fact that people are walking away from their repayments is a bad sign for the bottom end of the economy in the US. And I guess the third point I wanted to make when I was doing my. Analysis of all this was Credit Corp had been in decline for a couple of months prior to their announcement.

[00:19:54] Tony: So that to me says either someone was very savvy as an investment analyst and worked out that [00:20:00] customers in the U. S. were walking away from their repayment plans or there’s been a leak somewhere. Um, so I think there might be, you know, I, I tend to think ASIC is bloody awful at, at monitoring disclosure, and I think Credit Corp is very good at coming forward as quickly as they can, but clearly someone used something in the months preceding up to this, um, decline, and either the smart money did well, or, uh, there was a leak, and, you know, you’d have to think that at the management meeting a month before, um, the disclosure, they were seeing the trend starting to appear, not saying that, uh, You know, they should have disclosed then or that anyone did anything bad and I haven’t seen any selling by directors or anything like that.

[00:20:42] Tony: But you know, potentially someone, um, in, in the company told a mate who told a mate and started selling their shares. But, um, yeah, it’s that, that in itself was a bit of a flag as well that something bad was coming. And

[00:20:55] Cameron: Yeah, I mean, I know it’s been declining for the [00:21:00] last six months. I’m just overlaying its chart with the STW chart. Um, yeah, certainly has declined a lot more than the STW over that period of time, which has declined, like, CCP’s been declining since January 22, and it was trading at, uh, what’s that there, thirty, thirty three bucks, yeah,

[00:21:33] Tony: have a look at the last couple of months. I think it started to really turn down. Before the big drop last week.

[00:21:39] Cameron: yeah, yeah, it was, uh, trading at about twenty bucks back in July 23. And it’s dropped down to 12 bucks, as you said, it’s like half since then, but uh, yeah, I mean it started to decline, you know, February 22 when the Ukraine war broke out, so when [00:22:00] the markets started to tumble around, so it seems to have been tied with that and hasn’t recovered since.

[00:22:08] Cameron: Well, speaking of market indicators, you know, for the last, Five or six weeks each week when we put out the buy list, um, I’ve been doing this chart tracking the number of new buys, well the number of buys on our buy list versus the number of new three point trendline sales versus the number of Josephines that are on our buy list.

[00:22:30] Cameron: And it’s been tracking along fairly steady until this week when trendline sales really spiked. from the previous week. There was about, uh, 29 or 30 of them on the 16th of October jumped up to over 60 this week, three point trend line sells. So, uh, the buys declined a little bit, but that’s relatively steady.

[00:22:55] Cameron: It’s, they’ve been sitting between sort of 70 and 80 buys over the last [00:23:00] six weeks. Um, the josephines have been relatively steady between 30 and 40 josephines, but the three point trendline cells really spiked. I don’t know what I read into that, if anything.

[00:23:15] Tony: Well, I mean, I think we’re just painting a picture now that ASX is down, um, companies like Credit Corp of signaling hard times in the US, um, the share price graph this year looks like it did in 2007. I mean, I wouldn’t think the odds of a US recession in particular are increasing every day. And I guess that was, um, you know. I know there’s some questions about this later, but that’s the point I wanted to raise today too. If this is really bothering people, um, you know, if you’ve got debt, certainly think about putting money into an offset account or buying down debt. If you’re going into the market at this stage, I’d be, um, I wouldn’t be going in all on one day.

[00:23:56] Tony: I’d be like, if you’ve just retired or something, and you’re putting money into your super account [00:24:00] to, to invest, I’d be doing it, um, via dollar cost averaging over a 12 month period, something like that. Um, the trend at the moment isn’t our friend. So if people are, you know, if it’s making people unhappy or they’re not feeling confident, then, you know, by all means, take some money off the table.

[00:24:17] Tony: Um, you may miss out on the, on the upturns, or you may have some money still in the market and you get benefits from that, but there’s no point making yourself sick over this. It’s, it’s what the market

[00:24:27] Cameron: you’ve got to be able to sleep at night,

[00:24:29] Tony: Yeah, exactly.

[00:24:32] Cameron: if you don’t have the stomach for it. Don’t make yourself sick.

[00:24:35] Tony: And it, and it, it, it, it’s like, it’s no sign of weakness not to have the stomach for this. It’s, it’s not a great time to be in the market. Experienced people have seen it before, but if you’re new to it, I understand completely.

[00:24:46] Cameron: All right. Well, that’s all I have in my, uh, notes.

[00:24:49] Tony: Alright, shall I do a pulled pork?

[00:24:51] Cameron: Are you pulling today, Tony?

[00:24:54] Tony: pulling up, hopefully not pulling down, Regis Resources, so the [00:25:00] code is RRL, and the reason for doing it is it’s a large ADT stock, it has something like 6 million dollars traded per day, so a very large stock, it’s just come back on the buy list today, just snuck up above it’s 3 point trend line. As of this morning, I haven’t checked the market today for it, but, uh, it was on the way up yesterday and today. Uh, and it makes sense because, uh, I’ve seen this happen before to my investments in these kind of times. The gold price rises as people, again, try and get out of share markets and find an asset to park their money in.

[00:25:37] Tony: Um, historically it’s been gold. Some people argue it’s crypto at the moment, but I don’t buy that. It’s gold, um, or it could be bonds, or it could be real estate, or whatever, or cash. That’s the other point I think I should have made when I was talking before about, um, if you’re feeling unloved by the market and want to rest, um, you’re getting 5% Yield by putting your money into a 3 month term [00:26:00] deposit, um, or if you have an offset account against your mortgage you’re probably getting more like 6 or 7 percent given where mortgage rates are now.

[00:26:06] Tony: So that’s not a bad option. You’re getting, you’re getting not only are you sleeping at night. Um, you’re getting recompense for doing it. So, um, that’s a consideration for those people who are feeling, um, uh, nervous in this market. Anyway, back to Regis Resources. Um, it’s, it’s, uh, an Australian gold miner.

[00:26:26] Tony: It’s based in WA. Uh, it has three main projects. Uh, and each project, I call them projects rather than mines because they tend to be a cluster of mines. So they’ve started off with one mine and then they’ve done lots of exploration and drilling in the area and set up, um, smaller satellite mines, I guess we’ll call them in the area.

[00:26:47] Tony: But the three clusters of mines, one is called Duketon in WA, one is, they own 30 percent of another one called Tropicana, which is, uh, A couple of hundred, three hundred Ks northeast of Kalgoorlie in [00:27:00] WA and then they’re developing a mining area in New South Wales called Macphillian and, oh sorry, Macphillimie and that’s still in development and they’re waiting for approvals for that but if that comes online in the next year or two that’ll be a material increase in the amount of gold they can sell.

[00:27:17] Tony: They’re back on the buy list this week so that’s one reason for doing a pulled pork on them. I guess, Companies who are selling gold at the moment are doing really well and there’s a number of gold companies on the buy list and a number of gold companies in my portfolio as well at the moment. Again, not by design, just just how the buy list works.

[00:27:37] Tony: And I guess it makes sense because the Regis Resources called out that they Have been making about 600 an ounce margin on their gold sales. Um, so the Australian gold prices up around 24, 2, 400 an ounce. And they’re, um, they’re all in sustainable costs for this company’s around about [00:28:00] 1, 800 an ounce. So, you know, you’re making a good margin even for, um, uh.

[00:28:06] Tony: Mines that may still be a high cost operation, and this isn’t necessarily a low cost producer at 1, 800, all in sustainable costs, but with the gold price at a higher level, they’re doing well. They haven’t done well in the last year or two, and the reason for that is they got caught out by the rise in the gold price, and they hedged.

[00:28:26] Tony: Their delivery, and this happens from time to time with all kinds of resource producers. They, they feel a bit nervous about the gold price in this case, or any other commodity that they’re having to, having to sell into the future. And they, they, um, contract to make delivery at a certain price. And so in this case, it was just under 1, 600 an ounce.

[00:28:47] Tony: They were making delivery at, um, which is called hedging. And the hedging is almost finished. I think it’s about all their contracts that are about 70 percent delivered at the moment, and they’ve got a little bit to go next year and then they’ll be fully unhedged. So they’ll get [00:29:00] from next year onwards, they’ll get the full value of that margin spread between the gold price and what their costs are.

[00:29:06] Tony: But it did mean that this year in the latest results in June, they made a loss of some 24 million, uh, because of the hedging. Um, so I think that’s the upside with this, this company. I think that’s why the share price is ticking up at the moment. A, the gold price is going up with all the uncertainty in the world, and B, the hedge book is almost delivered for this, for this gold miner so they’ll start making full told odds on their margins going forward.

[00:29:32] Tony: And I guess C, um, if McPhilemys gets, um, gets a nod, I can’t see a reason why it wouldn’t. Uh, in the next couple of years, they’ll probably get another sort of 25 to 30 percent boost in their sales. So it’s all kind of, the tailwinds are starting to, to form behind this company. Uh, going through the numbers, uh, I’m doing this on a share price of 1.

[00:29:54] Tony: 64. It’s less than consensus target. Uh, the company suspended [00:30:00] dividends when it made a loss. Um, and they are saying then they’re not going to pay a dividend in this half. They, they, they will think about bringing them back next year, but they’re also balancing that up with the costs of bringing McPhilemys on to, uh, into production online, um, I guess as quick as possible.

[00:30:15] Tony: So they may not pay dividends next year. Um, the PropCaf for this company is currently sitting at 2. 7 times. So I’m really focusing on the cashflow for this one. It made a loss last year, so you can’t really look at the PE or, um, IV1 or IV2, which all use earnings per share, which is negative. Um, to get a valuation handle on things.

[00:30:35] Tony: So we’re not going to score any of those, uh, PE. Um, we’re going to focus on PropCaf. Uh, Net Equity Per Share we’ll also focus on. So Net Equity Per Share for this company is 2. 04, which is above the share price of 1. 64. So we can buy this at less than it’s, it’s equity position, which is a great thing to do.

[00:30:56] Tony: And obviously less than book plus 30. So, um, [00:31:00] don’t be surprised if the company before it. Pays dividends, weighs up a buyback as well. That, I think that would be on the agenda when they’re trading below its net assets. Uh, we don’t see any forecast earnings per share in Stock Doctor. And I found that quite strange because I looked it up in Stock Doctor and there are some 11 analysts covering this, um, this company, I didn’t have a chance to go.

[00:31:24] Tony: To all those individual stock brokers and look up reports on the company. And I may not even be able to, if I’m not a client of them all anyway. Um, but it seems surprising. There’s so many brokers covering this company and no one’s providing a earnings per share forecast. So, I mean, hopefully we’re getting in early to beat them, but obviously I think that might be a bit of an, uh, an error in Stock Doctor’s process.

[00:31:46] Tony: And I know they have some. Policy around that. I think they need three brokers to provide an earnings per share forecast before they start publishing one. So it could be that. I’m not sure. Um, but we’re not scoring it. It’s not scoring it for that, but that may hold back the [00:32:00] score, is I guess what I’m highlighting.

[00:32:02] Tony: Directors hold about 1. 5%, so we’re not scoring it, um, for an owner founder. Uh, we’re giving it a zero in PE because, um, it’s negative at the moment. It has just become a new 3. 0. Upturn, so we’re giving it a one for that. It hasn’t had consistently increasing equity, not surprising if it made a loss last year because of its hedging.

[00:32:22] Tony: So all in all, not a great quality score, 9 out of 15 or 60%, but because of that cheap, uh, PropCaf, the price to operating cash flow ratio, It’s giving a QAV score of 0. 22. So it’s um, it’s a large ADT stock of some six million dollars and it’s back on the buy list now with a QAV score of 0. 22, largely based on valuation.

[00:32:44] Tony: I think this is one to trade, as probably all gold stocks are in the long term, but um, the risk for this company are they’re a hundred, as of next year, they’ll be a hundred percent exposed to the gold price, which is happy days when the gold price is up like this, um, but if [00:33:00] they’re If their costs stay at around 1, 800 Australian, um, to produce the gold, uh, then the share price can re, can retrace back to that kind of level pretty quickly and squeeze their margins.

[00:33:13] Tony: Um, they did highlight that 1, 800 they thought was a high cost this year, so, uh, it’s always, it’s always difficult to predict the secondary effects of going forward with this, because if the gold price starts, Reducing, they’ll probably start reducing their costs in line. So they’ll do whatever they can to maintain margin.

[00:33:30] Tony: But that’s certainly a risk is the gold price retreasing. I’ve said in my notes here, there’s a risk that if peace breaks out, this company will, will, uh, turn down. Um, I’m not sure what the likelihood of that is though. Uh, the other positive is McFillamy’s approval is somewhere in the next 12 months and they can get that up, up and running quickly after that, hopefully.

[00:33:50] Tony: Um. Uh, I did also highlight during my analysis and I did this based on the U. S. gold price because it was in Stock Doctor rather than the Australian one. [00:34:00] And people can look this up if they’ve got Stock Doctor memberships. But, um, the U. S. gold price at least from sort of 2018 over the last five years has gone from 1, 200 U.

[00:34:10] Tony: S. an ounce up to 2, 000, just under 2, 000 U. S. an ounce. So, you know, that’s, that’s not quite doubled, but it’s been a big increase over the last five years. Um, so the trend is certainly suggesting the gold price will keep increasing, and perhaps that’s been driven by increasing interest rates, um, or just uncertainty in the world, but it’s, it’s certainly an upward trend for a long time now.

[00:34:33] Tony: So anyway, they’re the risks and the, and the positives, and I think it’s fun to trade based on the gold price trend.

[00:34:41] Cameron: I added a couple of parcels of it yesterday

[00:34:43] Cameron: to some light portfolios. Yeah. Well, it was also one of the only things you could buy this week, you

[00:34:53] Tony: Again, not surprising, we can buy gold stocks at this stage of the cycle. Yeah.

[00:34:57] Cameron: Yeah, I think I’ve bought three in the last week, you

[00:34:59] Tony: [00:35:00] Yeah.

[00:35:01] Cameron: some of the only things on there. That and GEM, G E M, um, G8 Education, I think.

[00:35:06] Tony: Okay.

[00:35:07] Cameron: Small cap stock though, I think. Um, alright, thank you for that, Regis. Well, will we do the questions?

[00:35:15] Tony: Yeah, sure. I’m good to go.

[00:35:17] Cameron: Then we can talk about Mr. Inbetween.

[00:35:19] Tony: Yeah, good.

[00:35:21] Cameron: All right. Alex, what have you got for us today from the listeners?

[00:35:25] Alex: I’ve got a question from Sam. Could TK comment on the performance of the AFI this calendar year? It has been a significant and material departure of their correlation to the XAOAI, which I had to look up, is the ASX All Ords Accumulation Index. Cheers, Sam.

[00:35:41] Tony: Thanks, Sam. Good question. Uh, And as people know, I’m a fan of AFI as being a low cost way of investing in the share market. It’s been around for a very, very long time. Has a very low management expense, expense ratio, um, around the sort of number that ETFs do, or even lower than ETFs, like it’s like about [00:36:00] 0.

[00:36:00] Tony: 15%, something like that might be 0. 2%, very low. Um, I can give you the. The sort of short answer as to what I think is happening, uh, so I think the difference at the moment is that, uh, rather than look at XAOAI, if people want to have a look at this along with us, um, have a look at STW, which is the, the ETF that tracks XAOAI, so it’s the, it’s the ASX 200 index with the dividends reinvested.

[00:36:28] Tony: Um, which kind of is a good proxy to, to benchmark yourself against. Uh, that hasn’t, um, well that’s been performing a little bit better than, than AFI. Um, but they are both going down, I, I hasten to add. And, um, if you look at the graph of the two of those two shares overlaid, they, they tend to directionally go the same, but occasionally one will rise slightly above the other one.

[00:36:51] Tony: At the moment the gap’s widened a bit, and STW is, is above. Uh, AFI, and I think the reason is because one’s a [00:37:00] listed investment company, which is AFI, and one’s an

[00:37:03] Tony: ETF. And the, okay, so the immediate difference is that, um, the ETF every day tells you what the underlying assets are worth, so it does a mark to market valuation and then publishes it, and it has what’s called a market maker sitting as part of its structure, buying and selling, um, shares or options or futures, or I’m not sure how STW actually trades, but it basically, uh, mimics the, very closely, the movements of the ASX200, um, on a daily basis.

[00:37:33] Tony: And so it sticks pretty close to that graph, uh, if not exactly one to one correlation, it’s pretty close. However, AFI is a close ended fund. So, um, what we’re probably seeing at the moment is that people are saying, uh, they’re selling out of AFI, um, possibly going into the ETF because it’s performing better.

[00:37:55] Tony: Um, but what that means is that AFI, Australian [00:38:00] Foundation Investments, will still have the same money invested in the, in the stock market because an ETF, every time someone sells a share, has to sell an underlying share or an underlying asset to pay that person out. Whereas, um, when AFI trades, it’s a, it’s a shareholder trading with another shareholder and the underlying fund isn’t, isn’t forced to buy or sell.

[00:38:24] Tony: That means though that AFI can trade at less than its net tangible assets or above its net tangible assets from time to time. At the moment it’s trading at less than NTA and I think that’s because people are selling because they’re worried about the market even though that’s forcing the share price of AFI below market performance.

[00:38:42] Tony: That won’t always happen but it is at the moment whereas SDW is tracking the market. The other thing that’s different between these two stocks at the moment is AFI’s Dividend yield is lower than STW. So I know AFI don’t always, um, try and track the market exactly. They [00:39:00] do, they do take sort of, um, oversized or undersized positions in companies they like.

[00:39:05] Tony: Um, but their yield is, is currently about 1 percent lower than STW. So you could even be seeing people sell out of AFI and buy STW if they’re a retiree, for example, just to get a better yield. So I think that’s what’s happening. But if you look at the graphs directionally, they both go in the same direction.

[00:39:22] Cameron: Any

[00:39:22] Cameron: follow up questions, Alex?

[00:39:24] Alex: Just absorbing. Yeah, I mean, I only ever look at the three point trend line when I look at AFI for whether I, you know, want to buy into it or not. So

[00:39:34] Alex: I don’t look at the macro

[00:39:36] Tony: It’s been a sell for a

[00:39:37] Tony: while. I think the three point

[00:39:39] Tony: trend line for it, yeah, has been,

[00:39:40] Tony: a sell for a while, yeah. So, if that’s what you’re doing, that’s good because you’re sold out and you’re probably sitting in cash waiting for it to be a buy again. So, that makes sense too. Perhaps that’s what’s happening in the market as well.

[00:39:53] Alex: Cool. Thank you.

[00:39:54] Tony: Okay.

[00:39:55] Cameron: you, Alex. Have a good week. Thanks for all your work on the buy list. Bye, Alex.[00:40:00]

[00:40:00] Cameron: this is a, this is a question from Anonymous. Didn’t want their name attached to this, uh, question. Um, I’m having trouble staying enthusiastic about my investment portfolio and it’s frustrating to watch it go between 0 percent and negative 20 percent over the past few years.

[00:40:16] Cameron: I think the average market downturn slash bear market is about 9 to 12 months. It feels like these unprecedented times just keep going with no end in sight and we are bleeding capital with no reserves. Death. By a thousand cuts. I was thinking about Ali’s recent post on the Facebook group about the return required to overcome a loss.

[00:40:36] Cameron: A 20% loss requires a 25% price increase. I know TK was able to leverage against his house coming out of the G F C and the capital losses sustained during this time. Given the frequency of market draw downs, can those of us that can’t leverage against assets actually overcome these losses in the short and long term and achieve Q A V like returns.[00:41:00]

[00:41:00] Tony: Well, yeah, I think so. Um, I guess my evidence for that is over the long term, the market’s gone up at roughly 10 percent per annum. So, uh, even though it zigzags a lot, you generally, the recoveries are a little bit stronger than the downturn. So, yes, you should definitely be able to recover your losses. But, uh, do I have a crystal ball to say how further we’re going to keep suffering losses and when they’ll turn up again?

[00:41:23] Tony: I don’t. It’s looking, as I said before, I’m painting a picture of, uh, of increasing bleakness in the U. S. and the gold prices reflecting that as well, so I don’t think it’s going to turn around anytime soon. So, Mr. or Mrs. Anonymous, or Ms. Anonymous, um, again, if it’s, if it’s worrying you, then you, or you feel like 20 percent is enough to, The stomach in terms of a give back to the market, then yeah, at least go somewhat to cash and, and take the four or 5 percent offered by the banks for your cash at the moment.

[00:41:55] Cameron: Yeah, as we said before, if you don’t have, if you know, if it’s making you [00:42:00] lose sleep or you’re feeling sick over it, you know, make the right decision for your health. All right. Thank you for that. Alex, as I understand it, this is a question from Alex, I should say, as I understand it, the checklist isn’t made up of traditional fundamental investing metrics like ROE and DCF based on historic revenue growth, but instead scores different valuation metrics to see if a stock is undervalued.

[00:42:23] Cameron: The process of scoring and summing these valuation metrics produces a quality score. Dividing that score by the ratio of price to operating cash flow per share combines to indicate quality and value, even though PropCaf is already scored as a valuation metric. Could TK please help me understand how he differentiates between quality and value in his process?

[00:42:46] Tony: But this is coming from male Alex. Um, and, um, I think, I think the essence of the question is why am I putting valuation metrics in a quality score? Um, and I think that’s just largely historical. Uh, I [00:43:00] could, I should, I could. Evolve the process to clearly separate quality from value, but at the moment, there are some valuation scores in the quality score process.

[00:43:11] Tony: Um, and I’ve just left it that way and kept calling it a quality score. So, apologies to Alex. Um, you’ll make a good, uh, school teacher by picking me up, picking me up on my terminology and grammar. Um, if I could be fucked, I’d change it, but I’m not. I’m going to keep calling it a quality score. But Alex is right.

[00:43:28] Tony: Yeah, there are definitely some valuation metrics in there. Um, in terms of counting. I’m not sure if he’s suggesting I’m counting price to operating cash flow twice, whether that puts a big toe on the scale. It does, but it also weeds out companies that don’t have a good PropCaf before we get to the end score for the company.

[00:43:53] Tony: But it only is in the quality part of the process. It’s only giving companies a one or a zero for… Oh, I think it might be two [00:44:00] for PropCaf less than seven. Um, so it’s not really, in terms of weeding it out, it’s not going to weed out a whole heap, but it will weed out some. Um, there are other valuation metrics in the quality score, like IV1 less than IV1, less than IV2, less than book value, less than book plus 30.

[00:44:16] Tony: Um, there’s a couple of other ones in there. Um, so yes, it, it, it, it’s. I could call them both QAV scores, but it just seemed easier to call one a quality score because we are assessing, you know, management’s ownership, um, paying of dividends and other kind of quality measures in there. It’s just historically all being blended into one.

[00:44:35] Tony: That’s all.

[00:44:36] Cameron: Did you even break it down before we started the show, or did you just have a score?

[00:44:40] Tony: Uh, yeah, I didn’t, I didn’t call it quality. I just had a score. Yeah.

[00:44:45] Cameron: Yeah.

[00:44:46] Tony: Yeah. And then started dividing it by PropCaf because that was a good way of bringing the value into the process.

[00:44:51] Cameron: Yeah.

[00:44:52] Tony: I kind of magnified it. I mean, along the way I did, I did things like, um, you know, giving the price to cash flow less than [00:45:00] seven, a bigger score, um, and then just found it was, uh, it, it provided enough differentiation if I divided everything by the price to operating cash flow.

[00:45:10] Tony: So we want a low price to operating cash flow. So if you make it a denominator in the equation, it, it favors companies with low price to operating cash flows. Um, I could have taken it out of the top line again, but it’s um, it’s not going to make a huge difference.

[00:45:25] Cameron: Alright, how are we going for time here?

[00:45:30] Tony: Oh sorry, I guess the other thing too for leaving PropCaf in the quality score is that it’s telling me that the company is making lots of cash flow, which is, which is actually a quality score. It’s just that I’m calling it, I’m also putting PropCaf in there. Bring an element of price into it. So yeah, I could probably amend it to be strong operating cash flow, but then I’d have to do research on what the cutoffs were for that.

[00:45:50] Cameron: think it’s fine. Tony, uh, last question. Uh, Tony, this is Alex again, has spoken about 15 to 20 stocks being ideal, but 10 stocks being better, given you can [00:46:00] stomach the volatility. If you’re a younger investor with a longer time horizon to retirement, why would you not create a concentrated 10 stock portfolio?

[00:46:10] Tony: I think that’s a good idea. Um, it’s kind of just, well, there is investment research surrounding a 10, uh, sorry, 15 to 20 stock portfolio, um, as being ideal. Uh, and we’re not, so the smaller the stock portfolio, the greater the volatility, but if you get the stocks right, the better the outperformance. Bigger the drawdowns, I guess, during this kind of phase of the market.

[00:46:32] Tony: And if you get more than 20 stocks in the portfolio, you tend to start regressing towards the index. So that’s the sweet spot if you’re, if you’re kind of, I hesitate to use the term an average investor, but if you’re someone who wants to have a reasonably handoff, Hands off process and investing, 15 to 20 makes sense.

[00:46:52] Tony: But I agree with Alex, a smaller portfolio makes sense if you’re younger because you can ride out the volatility. [00:47:00] Charlie Munger suggests a four stock portfolio. That’s what he has in his personal holdings, one of which is Berkshire Hathaway. But he also has, I think from memory, Walmart and maybe Apple.

[00:47:11] Tony: I’m not sure what the other two are. And we’ve had people on the show. Which I’m always reminded of, the Collins Street Investor, uh, Investor. CIO, I think his name was Michael Goldstein from memory, had him on a couple of years ago, and he’s, he’s, he’s said consistently, uh, why, why invest in your 20th best idea when you can invest in your best idea, and that’s something which has stuck with me as well, so Personally, I’d be happy with a one stock portfolio and then watching it and trading it as I’m following the rules.

[00:47:45] Tony: Um, I guess I’m getting down to that process over time. Uh, but yeah, I think Alex, you’re right. If you can, if you can ride out the volatility, if you’re not the kind of person to say, holy hell, I’m down 50%, I’m going to sell out and, you know, [00:48:00] buy a house or something or put it in the bank. And then rue the fact when the market goes up that you would have made a four or five times gain on your 50%.

[00:48:08] Tony: Um, then definitely a small concentrated portfolio of well picked stocks and, and following impartial rules is definitely the road to wealth.

[00:48:18] Cameron: Michael Goldberg,

[00:48:20] Tony: Thanks. Michael Goldberg. Okay. Apologies. Yep.

[00:48:23] Cameron: Alright, uh, last question, again from Alex, what would Tony do, WWTD, if he had a significant value of cash, say 20 percent in his 20 stock portfolio, most of his existing positions were a falling knife or below the second buy line, would he, A, top up positions that are still a buy, even if they dominate his portfolio by weight, A, Two, sit in cash until something underweight becomes a buy, thus buying in at a discount.

[00:48:52] Cameron: Three, go over his 20 stock portfolio rule and buy things that met the QAV buy criteria. Or four, [00:49:00] something else, can I take a guess,

[00:49:04] Tony: Go ahead.

[00:49:06] Cameron: uh, go over your 20 stock portfolio rule and buy something that’s a buy.

[00:49:11] Tony: No, that’s, that’s, that’s the wrong answer. That’s all I wouldn’t do.

[00:49:15] Cameron: Oh, no, I thought you would go big and then pare it back a little bit later on when you had to sell stuff

[00:49:23] Tony: Oh, well, I think if I’m reading Alex’s question correctly, he’s saying he’s got an investment of 20 stocks. Um, he’s saying if the existing positions were a falling knife or below the 2BL, so I can’t buy. What are my existing positions? Then what will I do? I’d sit on cash and wait, wait for either something in the portfolio or something.

[00:49:42] Tony: Well, it’d be something in the portfolio. I don’t want to hold more than 20 stocks. Um, as I said, we’ll start getting indexed like performance if we hold too many stocks. Um, yeah, so that’s what I would do. I’d, my first inclination in this situation is to buy something new. We 20 stocks. My [00:50:00] second inclination is to double buy something in the portfolio.

[00:50:04] Tony: There’s nothing to buy in the portfolio. I have to sit on cash until there’s something that meets one or two.

[00:50:10] Cameron: Well, I thought you’d said in the past that you’ll, you know, you’ll buy double positions if you have to, and you can, um, uh, concentrating your risk a little bit, but then, you know, it’ll, you’ll try and even that out over time as you sell things, or you would go up a little bit. I mean, you know, go up to 22 or 23 and then pair back as soon as you have something to sell.

[00:50:34] Tony: Yeah. Well, if I did, that makes sense as well, but, um, I’m more, I’m, I’m, I guess, again, on this theme of not trying to get a big portfolio going 20, you know, 20 stocks is probably my limit, I think.

[00:50:49] Cameron: right.

[00:50:49] Tony: But yeah, look, I could

[00:50:50] Cameron: there and just sit on cash.

[00:50:52] Tony: yeah, I could have said something different in the past, but that’s my current thinking anyway.

[00:50:56] Cameron: Yeah, no, I could have that wrong too. All right, thank you [00:51:00] for that. Good questions. That’s it, drew a line under it. What have you been doing for fun since we last spoke, Tony? And seeing as the market’s not fun, what have you been doing for fun and entertainment?

[00:51:14] Tony: We’re seeing concerts. We went and saw Mark Seymour on Saturday night in the undertow. That was great. Really good fun.

[00:51:20] Cameron: Yeah.

[00:51:21] Tony: Yeah, so

[00:51:22] Cameron: he, uh,

[00:51:24] Tony: for people who don’t know, Markie was the lead singer of Hunters and Collectors. So, the concert was, I mean, Neanderthal has been around now for a long time, so the concert was, um, I guess three quarters new stuff, but there was still half a dozen great old Hunters songs in there to, to jive to.

[00:51:39] Tony: It was great, really

[00:51:42] Cameron: undertoes, his new band? Right.

[00:51:44] Tony: It is, yeah. Well, when you say new, I think they’ve been around for about seven years.

[00:51:49] Cameron: Do you, do you listen to their stuff? Do you follow their stuff? Is it your fan?

[00:51:53] Tony: I am, but, um, I sort of resolved to go back and listen to it again after the concert, because there was a lot of good stuff in there.[00:52:00]

[00:52:01] Cameron: Hmm.

[00:52:01] Tony: Yeah, but yeah, great

[00:52:02] Cameron: of that. I’ll have to check them out.

[00:52:04] Tony: Yeah. And he’s amazing. I mean, he looks as fit as he does now at 67. And he did when I first saw him when I was about 26 or 20. I was at uni. So one of the bands I hired to play at the refectory when I was at uni.

[00:52:19] Tony: So I was probably about 18 when

[00:52:23] Cameron: Yeah. He’s always looked kind of buff. Like he works out a lot,

[00:52:27] Tony: I would

[00:52:27] Cameron: of himself and his voice is still good.

[00:52:29] Tony: Yeah, still great. Yeah, really good.

[00:52:32] Cameron: That’s

[00:52:32] Tony: And a really good

[00:52:33] Cameron: I mentioned on your Facebook. I mentioned on your Facebook post that, um, in one of the episodes of The Bear, one of the like, the, the, the big episodes of it, um, in Season 2, sort of finishes with a cover version by Eddie Vedder and somebody else of, um, I think it’s,

[00:52:54] Tony: Throw Your Arms.

[00:52:56] Cameron: Yeah, I think it’s Throw Your Arms Around Me.

[00:52:58] Cameron: Yeah. [00:53:00] You heard that cover version before?

[00:53:01] Tony: I have, yeah, it came out, oh, I think it was during a Pearl Jam concert in Melbourne about 20 years ago it came out.

[00:53:09] Cameron: Oh, really? Yeah. No, I said to Chrissy, Oh, wow, this is a Hunters and Collectors song. I didn’t, and obviously Eddie Vedder’s voice, but I hadn’t heard it before, but yeah, really good.

[00:53:18] Tony: Yeah, it’s a classic, that song, and it was great when he played it. Yeah. Oh, that’s the other thing too, I watched the, um, Ego documentary about Michael Godinski, and Hudders were in that, and Godinski said it was, that Throw Your Arms Around Me was probably the best song to come out of Australia ever. Which I, I, I probably agree with,

[00:53:38] Cameron: Really?

[00:53:38] Tony: yeah, but it’s a great

[00:53:40] Cameron: I hadn’t heard of that.

[00:53:41] Tony: sorry,

[00:53:42] Cameron: I hadn’t heard of it before. Is it good? The

[00:53:45] Tony: it’s really good, yeah, so it’s a Michael Godinski story, I think it was actually filmed just prior to his death as a doctor. documentary on his career, um, and it was released after he died. Um, and I think they probably [00:54:00] had interviews with the surviving member of, members of his family after that to add in too.

[00:54:05] Tony: But yeah, oh, it’s fantastic. It goes right back to the 1970s when he was just first starting and, uh, Skyhooks came along and gave him a really big boost. Um, Sort of like it was, the story is just like any sort of small business. He kept, he kept sort of just surviving and another act would come along and give him a great boost and he’d go lean for a while.

[00:54:25] Tony: And then another act would come along, give him a great, like say, split ends followed skyhooks. And it just goes on from there. And then he sold, he sold the business. He sold half the business to Rupert Murdoch, interestingly enough, to News Corp. And then rooted ever since, and then, um, set up. After he’s, I think he must have sold the rest of it over time, and then he set up, um, another, uh, well he set up a touring business to, to honour his non compete in the recording side of things, and then eventually went back and did a recording business.

[00:54:54] Tony: But you know, he’s had Debra Conway, Paul Kelly, Cutters and [00:55:00] Collectors. So they’re all in the documentary speaking about him. Became good mates with Jimmy Barnes, with, um, you know, Bruce Springsteen’s in the documentary, Sting’s in the documentary about how they just feel like Godinski was a true lover of music and a true supporter of music.

[00:55:14] Tony: Talks about the times when Godinski, um, like with. Within a week held a fundraising concert during COVID for the musos who weren’t getting paid and the support staff that weren’t getting paid. Just goes on and on. It’s just a really great rollicking story about his life.

[00:55:34] Cameron: Hmm. Oh, I have to check it out. I remember when he passed away, there was a lot of tributes from musicians came out in to honor him. Seems like he had a big impact.

[00:55:44] Tony: did. Yeah. And a worldwide impact too. He’s very well known overseas. Was getting lots of famous artists to come and tour in Australia.

[00:55:54] Cameron: Where’s that documentary?

[00:55:55] Tony: So it was only available, you had to buy it or rent it. So I think it was on Apple. [00:56:00] Either Apple or Prime, it was seven bucks to rent or something. I guess what that means it’ll be released in time on the streamers.

[00:56:07] Cameron: Yeah. Renting movies. That takes me

[00:56:12] Tony: Yeah, but it was good.

[00:56:15] Cameron: I often think about that when I, when I start getting upset about the number of streaming services that I subscribe to. And then I, I remember the days in the nineties when I’d go to the video store once or twice a week and get out four or five VHSs and it’d be like 25, 30 bucks a hit. To get them out, you do that four or five times a month.

[00:56:38] Cameron: It’s a lot more than the 30, 40 bucks a month I pay for streaming now. So, so we didn’t blink at it back then really. It was just, it was like exciting. You could watch whatever you wanted to watch. You’d had to drop five bucks or two bucks or whatever it was for a VHS. Hmm.

[00:56:55] Tony: Yeah, I agree. And it was, it was a great way of learning about movies too. [00:57:00] Cause like there wasn’t always a new release or a new blockbuster out to rent, but which would drive me into the. You know, the older movies and, and start to rip mean streets or, um, you know, even, even earlier than that, some of the sixties movies and fifties movies that were out was great.

[00:57:17] Tony: Good

[00:57:18] Cameron: great when you had, I, there was my local video store in Camberwell Road where the guy that owned that would, yeah, he was a real cult film guy and he’d have sections that like the Scorsese section or the Brian De Palma section and you could go and catch up on these films. You hadn’t seen all the Kubrick section or

[00:57:36] Tony: Well, the French, the French section too. I used to write a lot. French and German. Yeah.

[00:57:41] Cameron: Japanese little Kurosawa films, that kind of thing. Well, we finally caught up and finished Mr. Inbetween the other night. Uh, watched the final two episodes of that. Took us a long time to get through it, but wow. Well, I just gotta, like, credit to everyone involved. [00:58:00] Uh, Nate Edgerton and, uh, the guy who is the writer, creator, uh, star of it, um, played Ray.

[00:58:07] Cameron: Like, not a, not a bad episode in the three seasons, I thought. Everything was fantastic, the ending, he nailed the ending. Just left me with a big smile on my face, the final scene of the final episode. Just really, really great show, particularly for an Australian show. Like, wow, what an achievement.

[00:58:29] Tony: Yeah, I wholeheartedly agree. It’s been a real find for me too over the last couple of years. And I just can’t believe that he, the lead actor, whose name escapes me, just hasn’t been in more stuff than just Mr. Inbetween. It’s incredible.

[00:58:41] Cameron: it, that’s all he’s ever done in his whole career. Um,

[00:58:46] Tony: And like as the, as the series went on, he started to attract more and more actors, like known actors to play in the series.

[00:58:52] Tony: So he’s obviously getting the word out that this, Hey, this is worth being a part of.

[00:58:56] Cameron: Yeah, Scott Ryan is the guy’s [00:59:00] name. Um, yeah, like he, I know he’s supposedly working on something else. Uh, now can’t wait to see what it is, but what an incredible achievement that show really was, David Herriman. It was great, in it, um, the guy who plays Gazza, Justin Rosniak, like the whole cast, the girl who played his daughter, who I think is Nat Edgerton’s daughter,

[00:59:24] Cameron: she was fanta yeah, yeah, she was fantastic, she watched her grow up and her performance was always fantastic,

[00:59:31] Tony: And uh, his girlfriend at one stage, um, what’s her name?

[00:59:34] Cameron: Brooke Satchwell

[00:59:35] Cameron: from the first season.

[00:59:37] Tony: And then you had the guy from, who was the guy from Chances, that old soap opera.

[00:59:42] Cameron: Jeremy Sims in the last couple of

[00:59:44] Cameron: episodes.

[00:59:45] Tony: it’s just, just great how they all make cameos again. It was fantastic.

[00:59:50] Cameron: Yeah. It was one of those things where I’d be like, Oh my God, it’s him. I haven’t seen him in 30 years. And Chrissy’s like, what, what, who the hell are you talking about? I’m like, [01:00:00] uh, I don’t know, some guy. I hadn’t even forgotten it was Chances. I thought he was off of like Home and Away or something. I don’t think I ever watched the original.

[01:00:07] Tony: I thought it, I

[01:00:08] Cameron: But yeah, no.

[01:00:09] Tony: jumped the shark a little bit when they started getting into the pedophilia ring and going out into the country with the machine guns and all that kind of stuff. But up until then, it was just like, you could just imagine those kind of characters, you know, with a phone.

[01:00:27] Tony: I’ve been sent around to collect the money. Yep. Yep. Pay him. Well, what’s your job? I’m here to make sure you pay him. It’s just like, all low key.

[01:00:39] Cameron: Well, that’s the thing about his character, Ray. He is just very low

[01:00:42] Tony: Yeah, pragmatic, isn’t it? Yeah.

[01:00:45] Cameron: all he has to do is smile at you and you’re gonna, you’re gonna hand it over. If you’ve got half a brain,

[01:00:51] Cameron: just that smile.

[01:00:52] Tony: as soon as a smile comes on, you just know you’re in trouble, don’t you?

[01:00:56] Cameron: Yeah, yeah, yeah. [01:01:00] that was great. So thanks for putting me under that. I see, uh, your old mate Dez just discovered it a week or so ago on

[01:01:05] Cameron: Facebook. He mentioned he just got on it.

[01:01:07] Tony: Okay.

[01:01:08] Cameron: So if you ever talk to him again, you got something to talk about. Um,

[01:01:13] Tony: I

[01:01:14] Cameron: Fox and I watched another one of the Roald Dahl Wes Anderson films, Poison.

[01:01:19] Cameron: Have you seen that one?

[01:01:20] Tony: I haven’t, no, they’ve kind of disappeared off my list.

[01:01:24] Cameron: Oh,

[01:01:24] Tony: I’ve got to go and sort of ferret them out now.

[01:01:27] Cameron: Yeah, it’s really good, you know, same as the first one. Yeah, same cast, uh, really, really well done. Beautifully told. Yeah, good stuff. And yeah, I did my two hour show on Israel and Gaza on the bullshit filter last Friday. So that’s been a lot on my mind this week, is just what’s going on over there, speaking to some of my Israeli listeners about their take on it, and how they feel about it, and that kind of stuff.

[01:01:55] Cameron: So, yeah. It’s obviously a complete clusterfuck [01:02:00] and a tragedy and um, just, I don’t know, horrible situation all told, like Russia and Ukraine.

[01:02:07] Tony: Hmm.

[01:02:08] Cameron: uh, very sad for all sides, everyone involved.

[01:02:13] Tony: Yeah, it is. And it’s not close to resolution. I feel like the Israeli government is going to go in and try and get the hostages out. They’re going to try and exterminate Hamas, Hamas if they can. I don’t think that’s possible. So it’s just going to be, it’s going to drag on probably like the Ukraine war did, I feel.

[01:02:32] Cameron: Yeah, but I mean, it has been dragging on. This

[01:02:34] Tony: Oh, for

[01:02:35] Cameron: a hundred, it’s been going on for a hundred years over there, it’s uh, yeah. Something big needs to change for it to ever get a resolution and um, I can’t see how

[01:02:46] Tony: No, you’re going to have to relocate 2. 3 million people out of Gaza somehow. And A, they may not want to go. And, uh, B, where do you put

[01:02:56] Cameron: push, or push Israel back below the, back [01:03:00] behind the green line or further.

[01:03:01] Tony: Yeah. I mean, that’s what I’m saying. You

[01:03:03] Cameron: really make a, yeah, really have a solid attempt at a two state solution. But you know, the Palestinians don’t want a two state solution. What they want, they want their own, their own country back the way it was pre 1947.

[01:03:17] Tony: Yeah, and that’s possibly a mistake they made. They had a chance of a two state solution back in 1947, but they turned it down. Didn’t want to give up any land. And I kind of have sympathy for that. I mean, like this whole thing of parachuting all these people into your country and saying, yeah, yeah, it’s not yours anymore is, um, well, it’s a whole, it’s akin to the whole, uh, Aboriginal discussion we had last week about invasion.

[01:03:42] Cameron: But it happened 75 years ago, not. 250 years ago, even, you know, yeah. And, you know, it was, as I pointed out in the episode we did last week, that happened at a time when the developed world was rejecting. Immigration. [01:04:00] Australia still had its white Australia policy. The US wasn’t, weren’t taking European immigrants.

[01:04:07] Cameron: Australia was barely starting to think about taking Italian and Greek immigration from after World War II, but certainly not Jewish immigration. The rest of the world was like, No, we’re not accepting Jewish immigrants. You know, I always talk about the, on my shows, the Evian Conference. That, uh, FDR called in the early 1940s to try and figure out what to do with the, uh, Jewish refugees out of Germany.

[01:04:37] Cameron: Hitler said, I will send the Jews anywhere in the world that, that will take them. I’ll pay for the transport. Yeah, I’ll send them anywhere you want. And the rest of the world said, no, we don’t want them. Not our problem. And you know, they were still coming out of the great depression and, you know, ramp up for World War II and all that kind of stuff.

[01:04:58] Cameron: But I, I like [01:05:00] Australia’s foreign minister at the time was Mr. White and we had the White Australia policy, not named after him, but I’d like to think it was. He famously said at the, uh, or infamously said at the Evian conference, Australia doesn’t have a racial problem and we don’t intend on importing one. Really?

[01:05:19] Tony: Because they’re all

[01:05:20] Cameron: to our Indigenous population about that? We don’t have a racial problem? Anyway, uh, yeah. It’s just been a long time brewing that mess, and

[01:05:32] Tony: Yeah, and I feel uncomfortable even offering opinions because I don’t know enough about it. And my opinions are probably platitudes, really.

[01:05:41] Cameron: Yeah. Alright, well with that, um, happy, happy ASXing, Tony.

[01:05:48] Tony: Yes, happy ASX camp. I was going to lead off with that, but it just didn’t seem appropriate. Happy, happy ASX for next week.

[01:05:57] Cameron: Yes, you too. [01:06:00] QAV a good week, everyone.

[01:06:01] Tony: right, bye.

[01:07:00]

DISCLOSURE

In the interest of full disclosure, we would like to advise that as of the date of this post, the QAV team currently hold these stocks:

ANZ BPT EHE FHE FPR JHG KAR PRU QBE RMS SSM VEA VUK WAM WDS WGX WHC

If you’re interested in learning more, please review our trading and disclosure policy.