Hello QAVvers

It’s another Tuesday.

The AORD was up for the week, but barely.

Over the last five years, the AORD is up 19%.

For comparison, this was the previous five years, 2013–2018.

That’s an increase of 25%.

Howard Marks suggests that, due to increasing/stable interet rates, that “This time it really might be different”.

We’ll see what TK think about that this week.

Let’s have a look at the portfolio.

QAV PORTFOLIO REPORT

The Dummy Portfolio is performing well against the benchmark over multiple time frames.

SINCE INCEPTION (02/09/2019)

FY REPORT

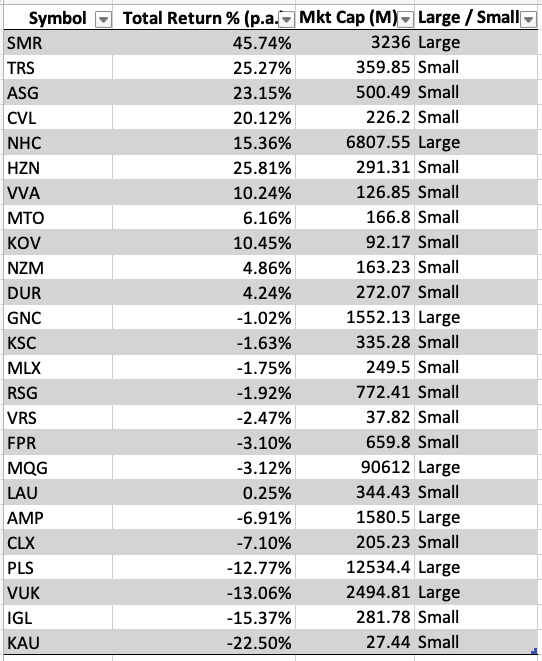

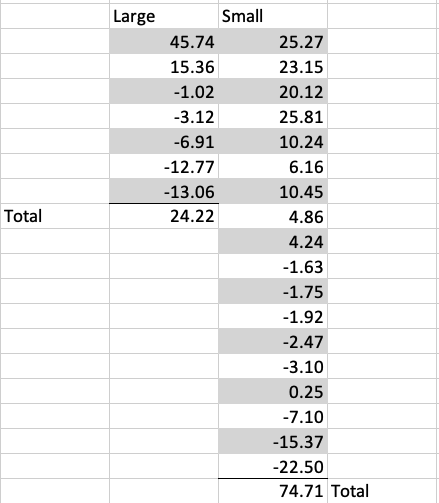

Following on from the discussion we had on the show last week about whether or not the small market cap companies were outperforming the high market caps, I did some further analysis on the portolio for the FY. I’ve called a stock with a market cap larger than $1B “large” and those under a billion “small”.

If I tally the results by Market Cap, it certain seems like the small have been outperforming the large so far this FY.

RECENT TRADES

No trades in the last week.

FREE WEBINAR

Thanks to everyone who attended last week’s webinar. I’ll hold another one in a few weeks.

STOCKS OF THE WEEK

During the last week, we traded some stocks in our Light portfolios. Details here.

** As always, please check our work, DYOR, and consult a financial advisor before making any investing decisions.

BUY LIST

Each week we produce a buy list that we share with our members. The intended primary purpose of this buy list is for club members to use as a reference for comparing their own buy list. In theory, all of our buy lists should look pretty similar each week.

As always, please check our work, DYOR, consult a financial advisor before making any investing decisions.

THIS SECTION CONTAINS CONTENT WHICH IS VISIBLE TO QAV CLUB SUBSCRIBERS ONLY.

LAST WEEK’S EPISODE

FREE EDITION:

The Club edition also contains: The RBA holds rates; Israel Gaza and oil; Joe Aston quits; HVN SD update; why was beginning of month chosen for josephines and not a rolling 30 day price; ‘value trap’ tool; the performance of our personal portfolios for this financial year vs the DP; performance of high v low ADT stocks.

Episode Transcription

[00:00:00] Cameron: Welcome to QAV episode 641. We’re recording this on the 10th of October 2023. Tony’s back down at Cape Schanck

[00:00:15] Tony: I am?

[00:00:16] Cameron: bit, little bit chilly down there, Tony.

[00:00:18] Tony: It is. Yeah, I can. Yeah, I am. It’s, it is chilly, but still lovely. It’s, it’s rare that it’s still, which I think is one of the reasons why it’s cold, but, that’s great for golf. Not playing in three club winds. It makes it much better and easier and more enjoyable.

[00:00:34] Cameron: That sounds pretty cold for this time of the year in Victoria, does it normally get that cold at Cape Schanck in October?

[00:00:39] Tony: No, no, it’s normally, well, it’s spring, so it’s normally sort of high teens. It’s probably about five degrees colder than normal, I guess.

[00:00:47] Cameron: Hmm. And why are you back down there? Is it horses?

[00:00:51] Tony: Yes, I came down to watch a horse run last Saturday. one of my friends texted me and said, how come I only have slow horses? [00:01:00] I went back and said, it’s even worse for me. I pay trainers to train them slowly.

[00:01:05] Cameron: Ha ha ha ha ha. Oh, that’s no good.

[00:01:08] Tony: we went, we had a great day at Flemington. Ruddy and I went out, we, went to the dining room, had a lovely lunch, but yeah, didn’t, that horse came last, so we didn’t take away any prize money with us.

[00:01:19] Cameron: Oh, I’m sorry to hear that. Speaking of prize money, the RBA gets the prize money for not lifting rates last week. You said you hoped that they wouldn’t do it, and they didn’t do it. For now,

[00:01:32] Tony: For now,

[00:01:33] Cameron: like they’re still saying they might do it.

[00:01:36] Tony: Yeah, plenty of people are saying they should do it, but I disagree. It’s, I don’t see how, when inflation’s caused by oil prices. A lot of inflation is caused by oil prices, how raising interest rates stops that one damn bit.

[00:01:51] Cameron: Because people need oil. They’re not going to stop buying oil because you raise interest rates, right?

[00:01:56] Tony: Well they might, I guess, you know, if they’re broke, like if they [00:02:00] can’t pay their mortgage and put the car up on stumps, I don’t know, but it’s pretty strange.

[00:02:06] Cameron: Yeah.

[00:02:07] Cameron: Well, speaking of oil prices, the whole situation in Israel and Gaza, which is very sad and unfortunate,

[00:02:15] Cameron: but I mention that partly because it’s tragic and partly because there is talk that oil prices might go up and I checked just before we got on the show today, oil prices are in fact going back up. They had been heading down, they’re going back up. Still a Josephine for us.

[00:02:32] Cameron: I think it’s about 88 now, it needs to get up around about 93, I think, for it to break its second buy line, become a buy again for us, but that’ll be something we’ll be watching next week. But, it’s just a, you know, another one of these global geopolitical factors that messes with our market, and, we’re a little bit hostage to it.

[00:02:54] Cameron: Market crash last week. I think it was US related figures [00:03:00] again. It’s

[00:03:00] Tony: US bond yields. Hmm.

[00:03:02] Cameron: It’s recovered quite a bit, but, I think we’re still at a six month low today. So it’s kind of frustrating as an investor to spend six months diligently following a process and then the market just cuts you off at the knees yet again for the

[00:03:18] Cameron: umpteenth time in the last couple of years.

[00:03:21] Tony: Yes, no, you’re right, it is frustrating, but it happens, that’s, that’s the business we’re in, unfortunately, or fortunately, in the long run, fortunately, in the short run at the moment, not so great, and I guess also, too, like, my note for today was, the hunt for Red October, because, October’s always the witching the stock market for some reason, and, the 87 crash happened in October, the GFC, plenty of starts for the GFC, but I think, maybe Lehman Brothers collapsed in October, I don’t know.

[00:03:49] Tony: yeah, like October always seems to be the, the thinnest ice in the stock market. So hopefully we’re, we’re, we’re going ahead, but, wouldn’t mind that this could, [00:04:00] this week could be a dead cat bounce, unfortunately, we’ll see.

[00:04:03] Cameron: I was blaming QAV club member Reg Travaskas because he said to me, the end, towards the end of last month, October’s always, you know, quite often the worst month. And I went back over the last five years and actually the last five years, October’s been reasonably a good month. I said, I don’t know about it.

[00:04:18] Cameron: He goes, oh, I read it on a forum somewhere.

[00:04:21] Tony: Yeah,

[00:04:21] Cameron: I said, I don’t know. I don’t know, Reg, I think you might be a little bit pessimistic about your October, of course. Very first day of October, the market crashed. So I was blaming Reg, but you’re backing him up that there is a history of October related

[00:04:34] Tony: look, it’s been. It is a market myth and it’s been debunked, but it is coincidence that, you know, the Wall Street crash that kicked off the Great Depression happened in October, 87 happened in October, GFC kind of got underway in October. And the old myth is sell and may and go away. That’s until the end of October.

[00:04:57] Tony: But again, there’s been plenty of research that shows it. [00:05:00] You wouldn’t have made or lost money if you adopted either of those strategies, but I mean, selling in October or, or sell in May and go away. But yeah, it’s a skinny month.

[00:05:10] Cameron: Well, on more entertaining news, I read this thing in the financial review last week. We didn’t get a chance to talk about it on last week’s show, but it’s about Keith Gill. The hero of the, AMC, debacle last year, was it last year or the year before that that happened? 2021, I guess it was a couple of years ago.

[00:05:33] Cameron: GameStop and AMC.

[00:05:35] Tony: right. Yeah, I took a photograph of a GameStop shop when I was over in the States in April. I should post that. It was, it was, there wasn’t a customer in sight.

[00:05:47] Cameron: Yeah, well, I’m sure people, we don’t need to go over the story, people remember it, WallStreetBets was the subreddit, and this, it was started by this guy, Keith Gill, who went by a number of aliases online, but there’s a new [00:06:00] movie apparently coming out, this month, based on his story called Dumb Money, starring Paul Dano.

[00:06:08] Cameron: There’s Keith Gill, and I thought this was just a really interesting story, I don’t know if you had a chance to read it in the Fin Review, but he was kind of pretty much a nobody, as they say in this, he was an unremarkable financial services guy living in an unremarkable rented house in an unremarkable Boston suburb, one of many millions of ordinary decent Americans, and But at night, he would post YouTube videos and write posts on Twitter and Reddit’s WallStreetBets about which stocks were catching his eye.

[00:06:38] Cameron: He mixed this advice with his thoughts on Belgian beers and would celebrate big gains by dunking chicken goujons in one of those beers or perhaps in a glass of Prosecco if he was feeling flash. Sometimes he would consult UNO cards or a Magic 8 Ball, a novelty toy shaped like a pool ball which offers 20 possible answers to any yes no question.

[00:06:59] Cameron: I [00:07:00] like that whoever wrote this felt like they had to explain what a Magic 8 Ball was,

[00:07:03] Tony: that’s what I thought when I read it too. This guy’s being paid by the word.

[00:07:07] Cameron: It’s the latest technology that people might not have caught up with yet, the Magic 8 Ball. He went by Roaring Kitty on YouTube and Twitter and deep effing value on WallStreetBets, but just the story about, you know, how he just got behind GameStop and how just people jumped on board and he, like, apparently he got out and made a Bucket load

[00:07:34] Tony: Mm hmm.

[00:07:34] Cameron: money, which he managed to hold on to.

[00:07:38] Cameron: He got out at the right time and a lot of people lost a lot of money, but he got out of it with about 20 million US dollars.

[00:07:47] Tony: good on him. Yeah, well, he was, I mean, what he was focusing on is… Companies that were being shorted and then he was trying to create what’s called a short squeeze. So I, I don’t know if he honestly believed that [00:08:00] GameStop was a good investment, but it was for him because he could see it was heavily shorted.

[00:08:04] Tony: And it makes sense because they’re trying to sell you physical games, game cartridges in the day and age when everything’s being streamed. It’s a bit like Blockbuster Video was towards the end. and Yeah, so, heavily shorted company, may even have been profitless, going broke, but he had enough followers to drive the share price up, which then forced a short squeeze, which was all the people who’d shorted the stock were then worried about unlimited losses if the share price kept going up, which happens when you’re short.

[00:08:39] Tony: and so they had to sell, which was, well, but first of all, they had to buy the stock and then give it back to the person that they borrowed it from to short it, so that pushed the price up as well, and then he got out, but unfortunately, in all the sort of, euphoria and memes and to the moon postings, [00:09:00] the retail So, People who supported him didn’t get out and then the short squeeze was over and GameStop dropped back to what it was originally in terms of its share price.

[00:09:10] Cameron: Yeah. And I remember we, we were talking about it at the time and you were positing that there were probably major players that were making a lot of money. And just laughing at the whole dumb money thing flowing in and the Financial Review sort of backs that up. It says, Inevitably, the real picture is not as clear cut as the David and Goliath narrative where retail investors make a killing while Wall Street takes the hits.

[00:09:37] Cameron: Plenty of hedge funds made serious money, both from their own stakes and from lending out stocks to panicking short sellers. Mudrick made 200 million, Senvest 700 million, BlackRock more than 2 billion. The hedge funds which did go under did so because rivals kicked them when they were down. GameStop might have brought the [00:10:00] likes of Melvin to its knees.

[00:10:02] Cameron: But it was Melvin’s competitors who didn’t let it get back up. And for every small time investor who cashed in, there were many others who held on to their stock too long and never saw a profit. GameStop is now trading at less than 18 a share, around the same level it was before the short squeeze began.

[00:10:21] Cameron: WSB is full of young aggressive traders who ignore fundamental risk management principles and regard letting go of stock as weak. So, I like this quote from an analyst, Michael Pachter. He said, The guys who got in because of the structural short, that was a smart move and that was the right thing to do.

[00:10:38] Cameron: The guys who stayed in because they believe in GameStop’s new Executive Chairman Ryan Cohen? Dumbasses. Keith Gill’s army may have won a battle, but Wall Street won the war. It usually does.

[00:10:52] Tony: yeah. Also he’s done well to make 20 million, but that’s pal’s insignificance compared to what Wall Street made.

[00:10:59] Cameron: [00:11:00] Yeah. So I thought that was, like, just, just another one of those stories of, people getting excited, following the hype, and many of them, most I would guess, getting burnt.

[00:11:18] Tony: And looking to TikTok for financial advice, or Reddit or wherever,

[00:11:23] Cameron: whatever. Yeah,

[00:11:24] Tony: yeah, and not checking it out themselves. And we’re seeing a version of that in reverse now, really, all the doom and gloom that’s going on. I saw a, I saw a post the other night on Facebook about how many Canadians were selling their holiday homes in their boats.

[00:11:40] Tony: at the moment because their mortgages were stressing out and how that was going to be the end of the end of the world for the Canadian stock market. Well, maybe, but, you know, again, following a post on Facebook and selling all your stocks is not good financial advice.

[00:11:56] Cameron: Hmm. Well, in [00:12:00] other sad news, your favorite financial review journalist, Joe Astin, is leaving.

[00:12:04] Tony: yeah, that is sad. He’s been compulsory reading for me every day because he’s the only person, whoever really exposes much in the financial markets. Most journalists, just like most fund managers have to keep on the good book, in the good books for the CEOs and CFOs so they can continue to have access to them.

[00:12:24] Tony: but Joe just told it like it was.

[00:12:29] Cameron: I didn’t realize how young he was. This article in BNT says, Joe took over the helm of Rewindow in 2011 at Just 28 years old, and over the last dozen years, he has turned it into Australia’s must read business and political column. Graduating from corporate star spotting to high level corporate analysis, he turned a gossip column into a form of journalism like never before seen in Australia, and arguably the world.

[00:12:57] Cameron: Don’t know about that, I mean, I think it was a little bit [00:13:00] Crikey esque a lot of the time,

[00:13:01] Tony: Yeah, true, true. And a little bit Hunter S. Thompson at times as well,

[00:13:06] Cameron: yeah,

[00:13:07] Tony: And he still did a lot of star spotting. I mean, you know, when the Australian Tennis Open is on, for example, or Melbourne Cup’s on, that’s all rear window is, is photographs of who’s with who. So there’s still a bit of star spotting going on.

[00:13:20] Tony: But yeah, I mean, in terms of his analysis on Qantas, and, you know, recently, but many other companies before that, he, he’s the only person who’s been telling truth to power, really.

[00:13:32] Cameron: So do you know, have you heard where he’s going, what he’s

[00:13:35] Tony: No, but I’m waiting to find out because it’d be, it’d be great to follow him wherever he goes. If he still stays in the industry, I guess. Maybe he’s like Steven Mayne and he’s lost his house to,

[00:13:45] Cameron: I

[00:13:45] Tony: to someone who’s suing him for libel. I don’t know.

[00:13:48] Cameron: think Fairfax probably has better lawyers.

[00:13:51] Tony: Or Channel 9

[00:13:52] Cameron: Yeah. I just wanted to update everyone on Harvey Norman, because I had mentioned a couple of times that [00:14:00] the numbers in Stock Doctor, the market cap numbers and the owner founder holdings seem a little bit wonky. They’ve got the market cap around 730 odd million.

[00:14:14] Tony: As opposed to Stockopedia and Yahoo Finance that have it at 4. 91 billion. And they have, I think, Harvey, Gerry Harvey’s holdings at 343 percent of the stock. these days.

[00:14:30] Cameron: and they’ve been at the top of the buy list, well, near the top of the buy list the last couple of weeks and I’ve been cautioning everyone, but So I went back after our show last week, I went back to Victor at Stock Doctor, cause I’ve been waiting for him for about a month to clarify the numbers.

[00:14:45] Cameron: He said they still haven’t got any clarification, but I re ran the score with the Yahoo Finance market cap. And I just put director’s holdings at zero, [00:15:00] which probably isn’t, but just to

[00:15:02] Tony: No, it wouldn’t be.

[00:15:02] Cameron: of the equation.

[00:15:04] Tony: Gerry Harvey does have a significant holding.

[00:15:06] Cameron: I’m sure he does, but it still came out with a score of like 0. 36 or something, I think.

[00:15:12] Tony: Okay, let me,

[00:15:14] Cameron: came out looking pretty good.

[00:15:16] Tony: let me do a deep dive and check the figures in because I haven’t looked at it. And, when I saw it on the buy list, it has been on the buy list in the past. When I saw it there, I thought that looks a bit strange. So, I’ll, I’ll do a deep dive and get back to you.

[00:15:28] Cameron: Okay. well, what else have you got before we get into Q& A TK? Oh, so jokingly on the show last week, I said, Hey, if you run into my wife in Sydney, say

[00:15:39] Cameron: hi, the next day, she sends me a photo. Guess who I bumped into in the middle of Sydney.

[00:15:45] Tony: Yeah.

[00:15:46] Cameron: Now, I don’t know if she’s stalking you or you’re stalking her or you’re stalking each other.

[00:15:52] Cameron: What’s going on there, Tony? It’s like, what, 6 million people in Sydney. How do you bump into my wife?

[00:15:59] Tony: [00:16:00] very slowly . no, it was a complete coincidence. I was in town. I had to drop a package off to, a mate and then, grabbed a bit of lunch

[00:16:09] Tony: and,

[00:16:10] Cameron: fishy.

[00:16:11] Tony: oh no, I was, I played golf with a guy and inadvertently took his vest home with me. ’cause we had both the same sort of vest. So I dropped it back into town where he worked.

[00:16:19] Tony: and, I was walking back and, you know, sort of a direct line from town to our place goes past the Art Gallery of New South Wales, and there’s a, if you walk down past it into Woolloomooloo, there’s a footbridge across the freeway, and I was just walking there, and I looked up and I thought, you know what?

[00:16:37] Tony: That looks like Chrissy, about 20 meters ahead. And then I remember you told me her niece was there, and I thought, oh, that looks like little Chrissy from behind. So I yelled out, and then eventually they turned around. Yeah, it was just amazing. They’d been to the art gallery, and now we’re heading to Woolloomooloo for lunch.

[00:16:53] Cameron: Yeah. That’s crazy.

[00:16:55] Tony: It is, yeah.

[00:16:57] Cameron: That’s the odds of that. That’s

[00:16:58] Tony: And then we were going to [00:17:00] catch up for dinner, but I couldn’t make it in the end, because I decided to head off early for Wagga Wagga to come down here. My plans changed.

[00:17:08] Cameron: So you want to do a pulled pork?

[00:17:10] Tony: I do, I did prepare one. I know we said that we had lots of questions, but I started to do it before we agreed not to, so we may as well do it. We can always hold a question over to next week if you like.

[00:17:21] Cameron: Yeah. All right. Let’s do

[00:17:22] Tony: And one of the reasons for doing it was I wasn’t familiar with this company. When I had a look at it, I thought this is interesting and it’s worth talking about.

[00:17:30] Tony: So, small cap stock, so I’ll just get that out there first. ADT is only 111, 000, so it will only suit small portfolios. The company is Southern Cross Electrical Engineering, SXE, SEXY is the code,

[00:17:46] Cameron: Oh, I like it already.

[00:17:48] Tony: and it’s in the name, what it does, it’s An electrical contractor, it works across a number of industries, resources, commercial infrastructure, retail, started off as a very small company in Perth [00:18:00] back in 1998 and then grew by organic means.

[00:18:03] Tony: Many in the resource sector, but also through mergers and acquisitions listed in ASX. along the way, Southern Cross Electrical Engineering bought or merged with other companies. one was called Datel, or Datatel, sorry, one was called Hayday Group, SJ Electric, SEME Solutions, and TriVantage is the most recent.

[00:18:28] Tony: and the reason for mentioning that is it gives them… A broadening area of specialization, expertise in telecoms, they do supermarket, electrical work and retail fit outs, store fit outs. They do electronic security and they’re getting big into switchboard manufacturing and installation. So they’re covering a lot of the, a lot of the waterfront there for electrical engineering.

[00:18:52] Tony: and the, I think the real interesting prospect for that and for them is, in one of the presentations they made recently, [00:19:00] where they said if Australia is to meet its targets for, emission reduction by 2050, and then there’s the whole heap of stats to what has to happen. There’s got to be a 30 times increase in the battery storage area, a 9 times increase in wind and solar connection to the grid, a 5 times increase in distributed solar, which I guess is solar on the roof and factories, etc.

[00:19:24] Tony: A 2 times increase in electricity usage. I guess primarily to replace gas and then decommissioning of the gas and coal plants from the grid. So there’s a large potential for this company to ride the, that kind of electrification wave, which is, you got to say, even if Australia doesn’t meet its targets, which is probably doubtful because they’re fairly ambitious.

[00:19:47] Tony: it’s still going to mean a lot of work for electrical engineers, in the next, 25 odd years. So that caught my eye. and just sort of to back that up, some of the recent highlights for this company, they’ve just [00:20:00] finished, Staff Village Accommodation, I guess the wiring for those, for Rio and BHP, and, a lithium mine I hadn’t heard of, they’ve just finished, wiring up a solar farm, the not, the Tom Price battery storage facility.

[00:20:15] Tony: They’re starting work on the Western Sydney International Airport. They’ve just won the electrical installation at the Atlassian Building, which is being built in Sydney, and the Shoalhaven Hospital. They have multiple data center contracts in New South Wales. So they’re picking up lots of work. It’s expanding.

[00:20:32] Tony: The workforce is currently greater than 1, 400 people. And the other interesting thing is recurring revenue for this company is 35 percent of the work they’re doing. So the higher that is, the better because that gives them smoothing of their earnings going forward. Cause, you know, tendering for project work can be up and down and follow the cycles of the industries they’re in.

[00:20:56] Tony: so yeah, I thought this was a, an interesting play on that kind of [00:21:00]electrification of the, Of the, net of the industry and, and, Australia, I guess going to the numbers, the share price is currently 78 cents, which is, greater than IV one, but less than net equity per share, plus 30%. So nets for this company is 70 cents and book plus 30 is 91 cents.

[00:21:21] Tony: So it’s trading below its book value. it’s a high yielding stock at 6.4%, but it. Just falls below our cutoff, which has now risen to about 6. 5 percent because of rising mortgage rates. The PropCaf, however, is 4. 23 times, and this company had, I’m just trying to find the stat, a 46 percent increase in cash flow year on year.

[00:21:47] Tony: It’s picking up the work and it’s picking it up fast. And they’re also debt free, which I should mention. and so that’s one of the reasons why they’re starting to pay out the dividends at a higher rate than they have been. directors hold 3 percent of this [00:22:00] company in Stock Doctor. However, the original founder, a guy called Frank Tomasi.

[00:22:05] Tony: Frank Tomasi nominees, I guess his company, has 18%, but I couldn’t find him on the board or any, anyone named Tomasi, so it’s, it’s quite possible that’s, that’s, he’s retired, or moved on, and, it’s a passive investment, so I, I can’t quite give them owner founder status, but there’s still a, a fair bit there from the owner founder in terms of shareholdings, consistently increasing equity is a zero, but it was close, there was only one half When the equity went down a little bit, otherwise it’s been going up nicely.

[00:22:37] Tony: what else? The PE wasn’t the highest or the lowest in the last six halves, so can’t we score it a zero there. Does have a reasonably recent new upturn, so it gets a one there. Goes back to June this year. so all in all, it’s a QAV score of 0. 16. So it’s not high up the buy list, [00:23:00] but, interesting company.

[00:23:01] Tony: And you’d have to think if it can, if it can keep going the way it has been going and Ride this wave of electrification, the future looks bright. Pardon the pun.

[00:23:12] Cameron: Hmm. Oh, you should quick email them and suggest that as a new slogan, tagline for their advertising charge them a million dollars for it. I added it to one of our portfolios back in August. I think it’s up maybe 1 percent since then. It’s gone from

[00:23:30] Tony: Yeah, and,

[00:23:31] Cameron: cents to 78 cents or something.

[00:23:34] Tony: and the hard part is in finding a stock to even look at today, they’re all Josephines at best right across the boards. So

[00:23:41] Cameron: really hard to find anything to

[00:23:42] Tony: yeah, and this one’s a Josephine as well, but it has been going up nicely since its results came out.

[00:23:47] Cameron: Thank you, SXE. I had a request from Arash just before we started recording today for one on Perenti.

[00:23:56] Tony: Okay, next week.

[00:23:57] Cameron: next week, yeah.

[00:23:59] Tony: I think we’ve done [00:24:00] that one, haven’t we? But I’ll have a look.

[00:24:01] Cameron: I had a quick look on my notes, I know we’ve talked about it a few times, I’m not sure you’ve done one, but I thought you had, but I searched and couldn’t

[00:24:09] Cameron: quickly find it.

[00:24:10] Cameron: I’ll check again. yeah, what a, what a tough week I’ve been again. Sitting on some cash this week because I had to sell stuff and the system wouldn’t let me buy anything.

[00:24:22] Tony: Yeah. I haven’t gone to cash yet because, I, I decided that the two stocks which had breached their 10 percent rule once I would use as a trial for 20%, rule ones, and they haven’t reached that far down and they’d be coming back up again towards 10. So we’ll see. I won’t do any more than 10 or two stocks, sorry, just as a trial, but I thought I might as well since they were next calves off the rank to sell.

[00:24:47] Cameron: Right.

[00:24:49] Tony: But otherwise, I would have been sitting on some cash too, which is what we’re supposed to be doing. I mean, I kind of look, look, it’s tough at the moment. I’m not going to sugarcoat it. Markets, not reacting well [00:25:00] to higher 10 year bond yields in the U. S. And it kind of oscillates a lot between, we’re going to have a soft landing to, we’re going to have a recession as each new data point comes out.

[00:25:11] Tony: So that’s Mr. Mark being manic, Mr. Market being manic depressive. But, you know, my kind of longer term take on this is. I’m just, I’m thinking back over the last 30 odd years when I paid attention to this kind of data. And I reckon interest rates have always been around on average around the level they’re at now.

[00:25:32] Tony: We’ve just gone through a period because of COVID and I guess after the GFC, where they were negative in some years and written down to zero or half a percent. for long periods of time, which, you know, was manna for heaven if you were investing to borrow in the stock market or to, or for property or whatever else, or to invest in your own business.

[00:25:55] Tony: and that’s, it’s the rate of increase and the quickness of increase, which is catching some people [00:26:00] out. And, and people have been talking all the way along about zombie companies, companies with too much debt that could survive when interest rates were low, but they can’t survive when they’re a bit higher.

[00:26:09] Tony: I’ve gotta say, I mean, I’m, I, I’ve used this term before, it’s situation normal, for the stock market. I mean, interest rate, cash rates between, I mean the, the R B A wants the cash rate to be between two and 3%. So even if it comes down, it’s not gonna come down much below that. And I would’ve thought for most of the time I’ve held a mortgage, the interest rate’s been six or 7%, which is where it is now.

[00:26:33] Tony: You know, sort of the average. I mean, sometimes it’s been a lot more than that. Sometimes it’s been lower, but mentally, whenever I’m doing sums on what I can afford, I use a 7 percent mortgage rate, because I think that’s where it’s going to fall naturally in time. So I think, you know, this is a period of transition, which is never great for stock markets.

[00:26:49] Tony: But, I, you know, my, my, my instinct is it’s situation normal and yeah, it could get worse, could get better, but over time it’ll be fine.[00:27:00]

[00:27:00] Cameron: When you say situation normal, you mean the position that interest rates are in or the way that the market is just swinging wildly around and seems to have been… Going through rapid depressions. Because I know your portfolio suffered the last couple of years, my super

[00:27:18] Tony: Mm hmm. Mm

[00:27:19] Cameron: my super portfolio in the same way.

[00:27:20] Cameron: I think we’ve got a question later on, we might get into that. like, and I know you’ve had bad years before, but the last couple of years have been really bad. You know, two bad years, really bad years in succession. That’s not situation normal, is it? Or is it the fact that those cycles come around once a decade that’s the normal part?

[00:27:41] Tony: Yeah, it’s more the second part. I can’t recall having a run of bad years like this before. It could have happened, and I’ve had two bad years in a row before, I’d have to look

[00:27:50] Tony: at the

[00:27:51] Cameron: GFC, I think 2008, 2009 you did, and then you rebounded massively in 2010 or something.

[00:27:58] Tony: yeah, exactly. [00:28:00] so I have had a couple of bad years and this does kind of, my performance kind of reminds me a little bit of the GFC. It’s not quite as bad as that. but this kind of prolonged market skittishness as it readjusts to, I’ll call them normal interest rates rather than low interest rates. yeah, so that, but that is situation normal for the stock market. And I guess the reason why I’m raising that is You know, it’s human nature and I’ve certainly been doing it looking back over the last couple of years saying what are the signs and what could I have done differently, etc, etc. but the worst thing to do is to…

[00:28:30] Tony: is to capitulate now and sell out now. And it may be the best thing to do if October, if there’s a market crash from here in October, not, notwithstanding that, even if we do have that, I should say, it’s going to rebound. I mean, interest rates are going to normalize. Companies are going to get comfortable with it and it’s going to be business as usual.

[00:28:51] Tony: And the market, which is now cheaper than it was two years ago, is going to rebound back to the average top conditions.

[00:28:59] Cameron: I was [00:29:00] just remembering a couple of years ago when interest rates were zero and nearly negative in some cases. My mother telling me that she heard from someone that interest rates were going negative and that banks would start charging you to hold onto your deposits.

[00:29:22] Tony: Well, I kind of did because, you know, at the, at the depths of that. low interest rate for bank deposits. A lot of banks were charging you an admin fee and if you didn’t have enough money in the account, you’re earning 1. 1 percent interest on it, you were actually out of pocket paying the admin fee.

[00:29:39] Cameron: Yeah, good point. Alright, well I, we’ll get into portfolio performance later on and I’ll do the dummy portfolio performance then, but, you know, it hasn’t had a good week, but, It’s still doing well compared to the benchmark, better than my super portfolio is doing, and maybe we’ll be able to talk about why.[00:30:00]

[00:30:00] Cameron: Let’s get into some questions. First one’s from Max. Hey Cam, I follow a US value investor that filters companies based solely on their quality metrics. He then sits and waits for them to become undervalued and then buys in. He’s an avid Buffett fan and utilizes the Buffett and Munger metrics. I remember in the early days that Tony used to buy companies that scored at least 75 percent in quality and also had a QAV score over 0.

[00:30:24] Cameron: 1. Just curious as to why he stopped this. I’m assuming he did some backtesting and found that the quality score in isolation had No correlation to growth. It’s just interesting that Buffett prefers great companies at a fair price over fair companies at a great price. My guess is that once you’re investing billions, you’re limited by what you can buy.

[00:30:44] Cameron: So the quality becomes super important. Cheers, Max.

[00:30:49] Tony: Yeah, so, the QAV of 0. 1 cutoff and the quality score of 75 percent cutoff when I was using it are fairly arbitrary numbers. I picked the [00:31:00] QAV score of 0. 1 because it just seemed that that was giving me a buy list that was long enough to be useful and not too long to be unuseful and too hard, too unwieldy.

[00:31:09] Tony: And it was about sort of 70 to 100 stocks every week, which was a good enough group to focus on. same with the quality score. So I did use it for a couple of years and that was reducing the size of the buy list. And then some weeks it was reducing it right down to a low number. and, but what I found was it wasn’t making, I didn’t do, I didn’t actually do a regression test on it.

[00:31:31] Tony: It was more observation that, I was getting enough. Enough of a quality score and just having a QAV cut off of 0. 1 because the quality score feeds into the QAV score. So if you look at the buy list now, there are certainly stocks on the, on there below 75%, but they’re usually in the 50s or 60s. So there’s still reasonably, reasonably good quality.

[00:31:52] Tony: And certainly towards the top of the list, they’re usually,a high number. So yeah, so rather than be too [00:32:00] prescriptive, I, I dropped the 75 percent threshold for quality. but didn’t do any regression testing. I’d invite, Max to do some and let me know if it’s, it’s a better outcome than, than the way I do it now.

[00:32:14] Cameron: I’m just looking at this week’s buy list from top to bottom, ranked by QAV score, the quality scores are 67, 62, 92, 100, 65, 100, 108, 108, 65, 75, 108, 92, Viva Leisure, 87, 73. Yeah, so most of them are, you know, close to 70 and above, a couple of exceptions. Looking down the list. Okay, there’s one right down the bottom.

[00:32:50] Cameron: Estia, EHE at 50%. There’s another one at 57. Macmillan, Shakespeare, MMS. Yeah, but [00:33:00] most of them are up there. Oh, 55%. What’s that? NZM. But yeah, I mean, out of what’s that 70 odd stocks, I’d say 70 out of 75 stocks, about 70 of them are sort of 70 and above quality score.

[00:33:14] Tony: Yeah. So it was becoming a bit redundant filtering it down again to 75 percent and above the quality. so that’s why I don’t do it. I did want to spend a little bit of time talking about Buffett and Munger. I think it’s, I think a couple of things. There’s so much written about. What Buffett does that, people lose track of what he did when.

[00:33:33] Tony: So he’s been investing, obviously, since the 60s, and has a terrific record and all the rest of it. But he, he openly admits along the way that he changed the way he invested and quality. It was really Charlie Munger who made him into a quality Investor, and so he went from being buying companies because they were super cheap to buying companies because they were good quality at a fair price.

[00:33:56] Tony: And that wasn’t, I’m not sure exactly when that happened, but that [00:34:00] wasn’t near the start of his investing career. He was making a lot of good money, by buying deep value stocks at the start of his career and then changed. And possibly partly because the funds were getting… Bigger and bigger, and he couldn’t get into the small situations, a bit like what I’m doing with the buy list now.

[00:34:16] Tony: So that’s certainly part of it. and, and the quote that sticks in my mind to use racing parlance that Charlie Munger, quoted was, Warren went from being a speed handicapper to a quality handicapper, which made he went, he went from focusing on how fast the thing ran to how good it was, what, what its quality was.

[00:34:35] Tony: and, If you go sort of further into the, the folk law, there’s the whole insurance industry thing and the concept of free float. So Berkshire Hathaway doesn’t have to borrow money because it makes us margin on all the money lying around in its insurance funds, waiting for redemptions eventually or not to be redeemed for expiration.

[00:34:55] Tony: So that’s a big leg up to Berkshire Hathaway. And the final thing I want to say [00:35:00] is that it’s probably been in the last maybe 20 years that Warren’s openly admitted that he’s even changed how he invests a little bit since becoming a quality investor. And I should just explain what he sees as being quality.

[00:35:12] Tony: It’s his concept of moat that’s important in that. And by moat, he means how difficult is it for someone, a competitor, to get started in the industry and to take down the incumbent? And how easy is it for the incumbent to raise their prices at any stage in the cycle? And so that’s why historically when you started…

[00:35:33] Tony: Me becoming a quality investor. He was buying things like, Proctor and Gamble and Amex and Coke, even though there were specific value reasons why he did that. There was a scandal with Amex. He worked out that, that Coke had, over depreciated or over, yeah. And Depreciate had a larger depreciation charge and it was going to need, would therefore write it back in time.

[00:35:55] Tony: So things like that happened. but in the last 20 or so years he’s gotten into. [00:36:00]Industries that he calls highly government regulated. Now, not every purchase fits that category. but if you look at things like the Berkshire Hathaway Energy business, which is all about, electricity generation and increasingly solar power, it operates in states where the government sets, sets the price.

[00:36:18] Tony: Pretty much, or at least that’s the guidelines for the price and they have, or they have large commercial contracts which have escalators in them, like a CPI automatic increase each year, for example, in price. Why is that important to Buffett? it gets back to this idea of a quality company being able to rise, raise its prices at any stage in the cycle.

[00:36:38] Tony: What it means is he can do a discounted cash flow on future earnings with some kind of certainty, which, you know, I’ve often argued is a, is a problem with discounted cash flows, that if we’re looking at a company like SXE, like we did today, Who the hell knows what’s going to happen in five years with that or 10 years with that.

[00:36:55] Tony: So factoring in all those things I talked about, like increasing [00:37:00] solar in the grid and decommissioning power plants and more data centers and things like that will have an effect on them. What, what, how much effect on the cash flow? I don’t even think they know. So that was the problem Buffett was having when he came to invest.

[00:37:15] Tony: He wanted to use discounted cash flows, but they were so opaque. In the most part, except for these companies that had strong notes, like your Walmarts and like your Cokes and those kinds of companies, where you could reasonably say, this company is going to be around in 20 years time or 30 years time, and B is going to be making more money than it is now.

[00:37:34] Tony: And you could look back over the years, it’s been running and kind of work out what, what sort of level of increase to put into his DC, DCF going forward. it’s even easier if you’re in Berkshire Hathaway Energy and you’ve got to deal with the government. 10 years of electricity sales or something like that.

[00:37:51] Tony: So it’s predictable cash flow that really drives him at the moment. so what he’s doing is taking that predictable cash flow and comparing it to a 10 [00:38:00] year bond or, or a 20 year bond or another investment which might be better value but harder to predict. And when he’s got these billions to put in, that’s what he’s doing.

[00:38:09] Tony: So I think that’s why he’s focusing on quality. It’s not just the quality of the company. It’s the quality of the cash flow going forward. And it’s a, for anyone starting out, it’s, it’s still not a bad way to invest, but it, it’s not going to give you the same sorts of returns as QAV will. and so at some stages, even the market will be in an index fund.

[00:38:29] Tony: So he’s got different needs now to what people in kind of our shoes do.

[00:38:34] Cameron: Wonder how Apple fits into that. Obviously it’s got a pretty good moat

[00:38:39] Tony: Yeah. Good moat.

[00:38:40] Cameron: of the brand.

[00:38:41] Tony: And it raises its prices during any sort of market cycle. Every year, an iPhone or every two years, an iPhone comes out. It’s never cheaper than the last one. They always go up. So, yeah. Yeah. And, and to be fair, Warren didn’t invest in Apple. One of his investment in Apple. Todd or Ted, the two guys he took on to take over from him, found [00:39:00] Apple and brought it to him, and he understood it.

[00:39:02] Tony: So, yeah, I mean, there are always, I mean, Warren isn’t wearing handcuffs and only investing in one way. He is open to situations, like he’s invested in all companies. And the last of the while, because he thinks that’s, you know, all prices are going to go up. So, yeah, but, but when he, when he invests large chunks of Berkshire Hathaway, he tends to try and find something that’s predictable.

[00:39:24] Tony: And that’s why he’s now called a quality investor.

[00:39:26] Tony: Okay. Thanks, TK. Thank you for the question, Max. All right. We’ve got Alex. Alex sent 400 questions last week. And to be fair, I did do a shout out for questions before I remembered that we’re having Chris Batchelor on from Stockopedia. so I think Alex was helping me out here. that’s

[00:39:45] Cameron: do a couple, we’ll do a couple of Alex’s and then maybe portion the rest out over the next four years of shows.

[00:39:54] Cameron: I welcome the questions. I mean, Alex’s questions are always good.

[00:39:57] Cameron: They are good. there’s just a lot here. Let’s [00:40:00] start with this one. How did Tony manage market downturns when he was leveraged? Or asked another way, where does the cash come from to pay off the loan in a falling market?

[00:40:11] Tony: yeah, good question. So I am still leveraged at the moment and it’s, it’s always dividends, which pays off the mortgage. And I want to stress, I’m talking about interest only loans there. So, You know, if you’re paying off principal as well, it’s a different kettle of fish, but at the moment, there are plenty of stocks on our buy list which are yielding enough to cover the mortgage rate on an interest only loan, which is about sort of six and a half to seven percent.

[00:40:38] Tony: and if you take into effect, you get a franking credit, which is a tax rebate. When your stock, when your tax return comes around, generally you’ll be able to cover the cost of the, of the, interest on the mortgage. and if you have a product like I used to have, but haven’t got at the moment, because they are, being clamped down on, which was,An overdraft type facility for as a retail investor, [00:41:00] so an interest only loan that would amortize the interest and allow you to make lumpy payments at some different stages.

[00:41:08] Tony: As long as you’re below the sort of maximum drawdown for the loan, you didn’t have to make a monthly payment. Then you could wait for dividends and pay them off that way in large Lumps twice a year, pay off your interest that way. So that’s how I did it. it didn’t make much difference whether the market was going up and going down.

[00:41:25] Tony: And Alex, I don’t know if you have, but go back and listen to one of our early episodes when we had Steve Sammartino on and he was talking about the Sammartino method and he makes a really good point. And so the Sammartino method in short is. He took his lump sum when he was, retiring from work and wanting to set up investments, put it into index funds, and then just forgot about it.

[00:41:48] Tony: And the reason why he was comfortable doing that is that companies are very low to cut their dividends. And even during the GFC, some companies cut their dividends, but it was generally only by about 25 or [00:42:00] 30%. So The cash was still coming in, from investments. They do, they cut their dividends last.

[00:42:06] Tony: They’d rather raise capital. Yet, yet some companies who are in really strange situations where they were borrowing to pay their dividend, that’s how desperate they are not to cut their dividend. So even though the stock price might drop, If you ignore the capital movements on your portfolio, generally, you’re still going to get at least sort of 70 percent of your dividends, even in the depths of the GFC.

[00:42:28] Tony: so you can cover your interest, you know, if you set it up properly and make sure you’re not over gearing, you can cover your interest from dividends at all, in all market cycles.

[00:42:37] Cameron: Okay, the next question from Alex is how does TK plan to live off his portfolio in retirement in down years? I’m

[00:42:46] Tony: I think I’ve

[00:42:47] Cameron: there will be Yeah,

[00:42:50] Tony: I was just going to say, I think I’ve just answered that. So, eventually when, it’s more when Jenny retires, she’s still active on boards. and so, you know, she gets enough income for us to live off and [00:43:00] then dividends pay for the mortgage, etc. but that can’t go on forever. So, we’ll, we will rejig our finances, pay down our debt.

[00:43:08] Tony: I would think we’ll probably sell our, our apartment in Sydney and… Pay off the mortgage, which isn’t that that big at the moment, compared to the value of the property and, you know. Probably move to Melbourne, it depends where Alex settles down, puts down roots and then use what’s left to, to buy something and invest, and then live off the dividends with what’s left.

[00:43:29] Cameron: so just living off the dividends.

[00:43:30] Tony: Yeah, exactly. Yeah. That’s, that’s what should be, all people should aim for that, I think, is to live off their dividends.

[00:43:38] Cameron: in down years when the capital value of your portfolio declines, you’re still getting the dividends.

[00:43:46] Tony: Correct. Yep. Yeah. So the capital generally declines, well, the capital declines, but the yields. Goes up ’cause a dividend dollar amount doesn’t. Now look, you know, there’ll be one or two companies, which, which will stop paying a dividend for a year. and [00:44:00] they will, their share price will drop ’cause it’s the sort of the last act of a desperate company.

[00:44:04] Tony: but most of them will continue to pay. Some of them will cut. So yeah, I wouldn’t bank on getting a hundred percent or year in, year out of what you’re getting now. But, you saw the 70% would be good to plan. your numbers are in, yeah.

[00:44:17] Cameron: Okay, well let’s skip the rest of Alex’s questions for now because we’ve got a few more and we’re Getting on in time. We might come back if we have some more time later. Phil, at the beginning of the month, there can be a lot of Josephines. Why was beginning of the month chosen and not a rolling 30 day price?

[00:44:35] Cameron: Is it possible to have a rolling 30 day price comparison? And does this influence when stocks are bought, i. e. less at the beginning of the month and more at the end?

[00:44:47] Tony: Yeah, we’ve talked long and hard about Josephine’s, it’s a good idea. to be honest, the way it’s set up now is my lazy way of doing it, because I can just look up the closing month end price in Stock Doctor pretty easily. [00:45:00] And if you want to code a rolling 30 days, I don’t know any sort of data source that gives us a rolling 30 days comparison.

[00:45:06] Tony: but if you wanted to calculate the coding, it’s got to take into account. 30 days ago, maybe in a weekend or a public holiday, and make all those exceptions. So it’s a lot more complicated. If we could lean on Brett to change the bread later to do it, I’d be happy to use it. but, we’ve already used up a lot of his good graces, I think, and the great work he’s done for us now.

[00:45:25] Cameron: And he just got a new job,

[00:45:26] Tony: He did. Okay. What’s he doing? Good.

[00:45:30] Cameron: he didn’t say it was confidential, so I’m just going to put it out there, Brett. he works, he’s got a job at BlueScope as a IT guy, you know.

[00:45:40] Tony: Well, he can give us some insight into how they’re going, because I think BlueScope’s often on the buy list from time to

[00:45:46] Cameron: They are. Yeah.

[00:45:47] Tony: Yeah. Yeah. Maybe that’s why, maybe that’s why he chose to work there.

[00:45:51] Cameron: Yes. So he can feed, it’s all about QAV and that’s, it’s all he thinks about. Morning, noon, and night. How can I help [00:46:00] QAV members?

[00:46:01] Tony: Well, he might, but I think it’s also… I’ve always thought, I’ve never done this myself, because it just hasn’t worked out that way career wise, but it’s a good way of getting cheap QAV stock, or cheap stock in a company that’s on the buy list, because you know, hopefully he’s got, stock issuance as part of his compensation package, he’s not paying for it.

[00:46:21] Tony: Yeah.

[00:46:23] Cameron: Good, good thinking Brett. But, yeah, I’m sure we could probably do it in, stock history in Excel as well, with my Josephine calculator. So I’ll ask my other Brett, ChatGPT for help in doing that. I’m sure we can work it out.

[00:46:38] Tony: Yeah, good idea. Thanks, mate.

[00:46:40] Cameron: Paul, asked about Alpha Spread, and he, well he pointed to Alpha Spread, and he sent me an apology, earlier saying I’m sorry I suggested this the same week you had Stockopedia on, but that’s okay, more the merrier. Alpha Spread looks like it might be an interesting eventual competitor to Stock Doctor.

[00:46:56] Cameron: It doesn’t have quite the detail that Stock Doctor does. However, it does have some interesting [00:47:00] valuation tools, including a discount cash flow. Valuation tool and a relative valuation tool, which are the main two tools used by boffins who value companies. These look similar to our IV1 and IV2 figures, but I’ll do some more comparison and see how they stack up.

[00:47:18] Cameron: I haven’t looked at alpha spread before of you, Tony.

[00:47:21] Tony: no, I haven’t.

[00:47:24] Cameron: however, one interesting tool it does have, Paul continues, which I haven’t seen before, is the value trap tool. This measures a company’s price versus its intrinsic value over 10 years. If there’s an ongoing and significant gap between them, the company is labeled a value trap as not ever coming close to its intrinsic valuation.

[00:47:45] Cameron: Has Tony ever come across such a valuation or tool before and could it add value to our checklist?

[00:47:52] Tony: I haven’t come across that tool. I’ve, I’ve heard the term value trap and I tend to use it a little bit differently. it’s, it’s normally a company [00:48:00] that’s cheap for a reason and sentiment tends to handle that for us because. You know, the market’s worked out that this company is going broke or, you know, has a serious problem, which isn’t coming through in the current numbers yet, that kind of thing.

[00:48:13] Tony: So that’s my definition of a value trap. But again, yeah, interesting concept. my, my question about it would be, We’ve seen companies, and I think I spoke about Nick Scali a couple of weeks ago, that from time to time come back and reappear on the buy list and, never seem to sort of go away long term from the buy list and, and I think that’s because they’re generally not rated, you know, with a high P.

[00:48:40] Tony: E. by the stock market, but they still go up. I mean, Nick Scali, if you look at its graph over the long term, I mean, I think it floated at about a buck and I don’t know what its share price is now, 14, 15 or something like that. So they still go up, even though they can be on a low PE. So I’d need to see some figures around this value trap metric before I [00:49:00] decided to take any action with it.

[00:49:02] Cameron: Hmm,

[00:49:03] Tony: And look at FMG. I mean, I don’t know what the P is at the moment for FMG, but it won’t be high. so you could always argue that, you know, it’s sitting below it’s, it’s true valuation as well, but it always does. so I guess my point is you can have companies that look like value stocks for a long time, but you can still make a lot of money out of them.

[00:49:21] Cameron: hmm. And, like, intrinsic value for us isn’t the be all and end all metric either,

[00:49:30] Tony: No.

[00:49:31] Cameron: it’s part of the scoring matrix, but it doesn’t really, weigh super heavy, I think, on the overall QAV score.

[00:49:43] Tony: No, just before I answer that comment, Cam, so I just looked up FMG, so it’s current PE is 8. 9 times, and the market average PE is 17. 5 compared to Stock Doctor, so, you know, who knows which way FMG is going, but it’s always [00:50:00] tended to trade at Much lower P. E. than the market, but as you can see from its graph, you can make good money out of it.

[00:50:07] Tony: yeah, so, yeah, so getting back to how, how useful a metric is in intrinsic value. as part of a valuation process, I think it’s okay. So as part of a heat map, I guess, is the term I use for, Valuation, but it gets back to this DCF problem I have is, you know, you’ve got to polish a crystal ball to see what you put into the DCF model 10 years hence with any sort of certainty at all. So that’s, that’s a, that’s a problem I have with DCFs and even with intrinsic values, they’re indicators rather than being definitive valuers of a company.

[00:50:39] Cameron: Yeah. I mean, that kind of reminds me of the classic startup entrepreneurs pitch to a venture capital firm saying, we’re going to make a trillion dollars in our fifth year. I mean, every business I’ve ever been part of making projections very far into the future. No one has any idea really what’s [00:51:00] going on.

[00:51:00] Cameron: It’s all sticky tape and chewing gum and fingers in the air. Right. It doesn’t matter what

[00:51:05] Tony: I remember Shell went through a long, when I was working, he went through a long detailed process of making five year business plans, a bit like the Communist Party in China. And after I’d been there for a few years, they all look like the Nike swoosh. They were all, you know, we’re going to go down next year, but then after that, hallelujah, it’s to the moon.

[00:51:24] Tony: And it’s just, and then I’ve seen that so many times in the stock market as well. It’s just, it’s all bullshit.

[00:51:29] Cameron: It’s all bullshit. I mean, there’s nothing wrong with having a business plan and it gives you something to focus on and work towards and strive towards, but yeah, our ability to think very far into the future is obviously not very good, so.

[00:51:43] Tony: and that’s one of the reasons why the stock market has these unsettling times is because, this, yeah, I’m trying not to use the term this time was different because it’s not, it’s, this is what happens, but generally, whenever there’s a problem, it’s always a different problem. Igniter for it. [00:52:00] So like the GFC was, what do they call them?

[00:52:02] Tony: Ninja loans, no income, no job. Loans in the States. That’s not happening now, as far as I’ve heard or can tell. you know, in, in 87, it was all the, the cowboys like the Christopher Scacers who were highly leveraged and it didn’t take much to throw them off their perch. A little bit of that going on now, but again, interest rates are.

[00:52:21] Tony: They’re higher than they have been, but they’re lower than they have been longer term as well. So I don’t think that’s going on. So it’s kind of like the market gets into this jittery phase. Oh, 10 year bond yields are up. Well, that, you know, that, that correlates with, you know, as a, as a predictor for market crashes in the past.

[00:52:39] Tony: Well, yeah, it correlates with a lot of things too. So, you know, they only pull out what they want to see and they get jittery. But, yeah, it’s five years ago, no one would have said that. No DCF would have said there was going to be a COVID outbreak. so, so how do you do a DCF with any sort of clarity at all?

[00:52:57] Cameron: Black Swan events and, you know, wars breaking [00:53:00] out and all that kind of stuff, no one

[00:53:01] Tony: Hmm. Yeah.

[00:53:02] Cameron: And it’s one of the things that I value about QAV is that our assumptions are pretty simple and conservative. Market tends to go up over the long haul, well run companies, when you can get them at a discount, tend to outperform not well run companies or companies that you’re paying a premium for.

[00:53:22] Tony: Mm hmm.

[00:53:23] Cameron: That’s it. Very, very

[00:53:25] Tony: Yeah. Lots, lots of cash is good.

[00:53:27] Cameron: yeah.

[00:53:28] Tony: is good. Lots of debt is bad.

[00:53:30] Cameron: Yeah, like at the very heart of it, it’s just very, very simple logic that’s very hard to argue with.

[00:53:39] Tony: Yeah. And we, I tried to put a bit of math around it so we can scan the market quickly. Yeah.

[00:53:43] Cameron: Yeah. And humans have a tendency to overcomplicate things. A lot of people come into QAV and want to overcomplicate it. I

[00:53:56] Tony: I think it’s, I think it’s overcomplicated at the moment, so I could probably do with the [00:54:00] trim.

[00:54:01] Cameron: yeah, yeah, yeah. It’s a bit like, ChatGPT. I mean, the boffins computer science people that are trying to work out how large language models do what they do, guys like Kurzweil has been saying this, that when we, it’s really important that we understand how it does what it does because nobody seems to understand it.

[00:54:26] Tony: Hmm.

[00:54:27] Cameron: He says, I think when we understand how it does what it does, we will realize that we can get it to do what it does with 10 percent of the effort that we’re currently putting into it.

[00:54:36] Tony: Yeah. Good point. Yeah. And QAV is probably the same.

[00:54:41] Cameron: hmm,

[00:54:41] Tony: we had a crack at trying to change the weightings in QAV, but it’s just been a mammoth task to work out which ones generate the bulk of the returns and by how much.

[00:54:52] Cameron: give me six months and I’ll get ChatGPT to do it.

[00:54:55] Tony: That’d be great.

[00:54:56] Cameron: Steven

[00:54:57] Tony: I’ll say, sorry, can I make, sorry, [00:55:00] before we go, can I make a comment about regression testing?

[00:55:03] Tony: and it’s just another one of my musings, but, I’m starting to lean towards forward testing rather than regression testing. I’ve been going through the results of, of Ryan’s work that he’s finished off now on buying from the top of the buy list versus buying from the bottom and, and rule ones and big cap versus small cap, et cetera.

[00:55:20] Tony: and it’s, it’s good stuff and it, it’ll, tell us what to do and. when we, when I finally get to a stage where I can present it, which shouldn’t be too far away. I’ll do that. but then I’ll trial it going forward with a, you know, the dummy portfolio on paper first to make sure it doesn’t have any, to make sure the backtesting wasn’t just fit for that sort of last four years of QAV.

[00:55:41] Tony: but by the same token, I’m, I’m, Almost, I’ve also set up some dummy portfolios anyway, like with the Renko testing. And I’m almost, I’m starting to think now that if people have ideas like on, on, value traps or whatever else we’ve talked about today that changes the QAV might be, it’s [00:56:00] almost like, well, go to the buy list, pick out the stocks that fit that pattern and put them into a portfolio and see how they perform going forward against the dummy portfolio.

[00:56:09] Tony: You know, if that has some legs, then we can do some further research from there. Because it is, it is a ball breaking task going back and trying to backtest in granular form this process with a large amount of data.

[00:56:22] Cameron: Mmm, yeah, okay. Steven, Cam, out of curiosity, are you able to share the performance of your personal portfolio and TK’s portfolio for this financial year? I’m currently down 7%. I understand the DP is up 5 percent but holds a lot of low ADT stocks. My performance in the last three years has been similar to TK’s performance.

[00:56:47] Cameron: I believe I’m following the system as accurately as possible. It would be good to compare with TK for this financial year to confirm this. Thanks. And I said to Steven, I don’t know about Tony’s, but I went and had a [00:57:00] look at my super funds performance for this financial year, and it was down about 6%, and it’s limited to high ADT, ASX 300 stocks.

[00:57:13] Cameron: So it’s performance isn’t as good as the dummy portfolios, but obviously I’m following the same process. It’s not quite as old as the dummy portfolio, but it’s been running for, I don’t know, 18 months or so, I think, two years maybe. So, and I know that last year it had a bad year. I think at the end of the financial year we were about the same.

[00:57:35] Cameron: It was about, I think last financial year was down 15, 17%, something like that. It had a shocker. so I told him what my numbers were and yeah, it’s, it doesn’t correlate with the dummy portfolio. And so I, I do wonder if the low ADT stocks are helping the dummy portfolio. What do you think?

[00:57:58] Tony: Yeah, so my performance is similar. [00:58:00] I’m down 10 percent this financial year. So it hasn’t been a good run for the last couple of years. my, so my thoughts on that are that. Yeah, if we look at the sort of questions that people have raised over the last three or four years of QAB, it generally coalesces around two things.

[00:58:17] Tony: One, it’s the sell process is 10 percent rule one, right as a number. And so we’ve been doing some backtesting on that and it’s sort of indicating 20 percent might be better and that’s at the stage it’s at. I’ll try and get the numbers definitively worked out. and I’m doing a test now anywhere on 20%, because I think, what’s, you know, my, my feeling from the last couple of years is there’s just been too many consecutive sells.

[00:58:41] Tony: So I sell something, I find something else on the buy list, I have to sell it. I find something else, I have to sell it. So rather than being like the GFC, which was stocks fell off a cliff or like in COVID, this has been just a slow burn of decline, decline, decline, decline. And part of that has been sort of consecutive rule one.

[00:58:59] Tony: [00:59:00] So I’m thinking about changing that. We’ll see what happens. And the other question that people have had consistently is, I’m up 30 or 40 percent on a stock and it’s way above its sell line. How do I avoid giving that back? And so I’m testing the Renco process as well, which may be a solution to that. I haven’t made my mind up on that yet.

[00:59:18] Tony: Let’s see how it plays out. So yeah, I mean, I’m not sort of sitting idly by and accepting 10 percent loss this financial year. I’m trying to work out what we can tweak. but it’s, yeah, it’s certainly my numbers match your numbers, which also matches, Steven’s numbers. And yeah, I, I, unfortunately this happens.

[00:59:39] Tony: From time to time in the market, and, and what will also happen is we’ll wake up one day and there’ll be peace in the Middle East, and, Zelensky will get a Nobel Prize, and the oil industry will be on its knees, and the Fed will be marking down interest rates, and, the stock market will, you know, double in the space of a [01:00:00] month, so it’s just how it goes, unfortunately, it’s hard to predict, but yeah, all I’d read of the rate is, It’s better to be in the market following a process than to be a prisoner of your emotions during these times and trying to second guess and trying to work out another way of doing things.

[01:00:17] Tony: To your question about large ADT and small ADT stocks, I’ve researched that before and people can do it now themselves. There are indexes for, as you said, Large cap stocks and small cap stocks, and they’re available on the internet. I think Dow Jones probably has them or S& P has them. And over time, they generally come out evenly, but from time to time, small caps will beat big caps or big caps will beat small caps.

[01:00:44] Tony: And I think we’re going through a period at the moment where, at least in terms of the value of the market, the small caps are doing better than the big caps.

[01:00:52] Cameron: why would that be? What’s the theory behind that?

[01:00:54] Tony: I don’t know, Cam, and if I… So to pay attention to other market commentators, they reckon that [01:01:00] the small caps end of the market is doing poorly.

[01:01:02] Tony: But it doesn’t seem to be our perception of what’s going on. But I think they might be influenced by the high growth stocks which have come back to earth, which are usually small cap type stocks. I don’t know. I suspect, you know, we’re in the big cap end of the market and it’s not too, we’re trying to pick the eyes out of the index, I guess is one way to put it.

[01:01:24] Tony: and so we, you know, up to this stage, we’re underperforming the index, but not by a dramatic amount. And I suspect that that’s just the way it works. Sometimes we underperform and sometimes we overperform, but in the long term, on average, we overperform.

[01:01:37] Cameron: Yeah, I’d suggested to Steven that I could, run some analysis over the dummy portfolio and, you know, break down the best performing stocks and determine their ADT status and see if there’s a correlation between our best performing stocks and their ADT. Because [01:02:00] obviously we’re following the same process with the dummy portfolio that you and I and Steven are following and the performance is somewhat different.

[01:02:07] Cameron: I mean the dummy portfolio is up around about five and a half, no sorry, three and a half percent as of this morning when I looked at it. After the decline from the last couple of days it was up around six a couple of weeks ago. Three and a half CAGR per annum for the financial year versus the STW down two and a half.

[01:02:26] Cameron: For the financial year. but, and I don’t think my super fund’s giving me a CAGR figure. It’s probably a time weighted return figure as well. So there’ll be some differences in the calculations, but still there’s a, there’s a pretty big difference between up three and a half and down six, whatever it is.

[01:02:44] Tony: I asked Ryan to have a look at that in the four years worth of buy lists that he was churning numbers through. And he, he made I guess the insight, and neither of us know if it’s universal or not, but his insight was that if you look at the small cap stocks, even though, [01:03:00] even though both large cap and small cap stocks have both been churning over these last few years, so his, his analysis was for the first couple of years of the, the buy lists, they were doing similar type returns.

[01:03:12] Tony: But for the last couple of years, they’ve both been churning, but what, and by churning, I mean, there’s been lots of selling and buying as things have breached rule one or three point trend line sales or commodity sales. but his insight is that there’s been a larger number of small cap stocks, which have large increases.

[01:03:31] Tony: So very specific one off stocks that have gone up, say 300 percent or 400%. and you only need a couple of those in the portfolio to improve your performance, enough to be. The big cap stocks, which aren’t, we tend to see large increases in them of being a doubling at the most. so that’s his analysis as to why the small cap stocks are doing better than the large cap ones.

[01:03:52] Tony: But again, it could just be a stage in the cycle that we’re at.

[01:03:56] Cameron: Well, if I look at, I can do a quick analysis, I guess. [01:04:00] In Navexa, so if I look at the dummy portfolio this financial year, SMR is up 38%. SMR’s market cap is…

[01:04:15] Cameron: 3.2 billion for Stanmore Resources. So up 38%. That’s kind of a large cap stock.

[01:04:22] Tony: Yep.

[01:04:23] Cameron: TRS up 25%.

[01:04:27] Tony: That’s reasonably large too. But I think if you look at Ryan’s example, you’ll, you might find there’ll be a small cap stock, which has gone up more than that. So the big cap stocks tend to go up. The ones that do well, go up 30 or 40%, maybe double at the most, but the small cap ones can double or triple.

[01:04:43] Tony: TRS’s market cap is about 359 million at the moment.

[01:04:48] Tony: That’s smallish,

[01:04:49] Cameron: ASG up 23%,

[01:04:52] Cameron: market cap, 502 million. That’s still a large market cap from our perspective, right?

[01:04:59] Tony: [01:05:00] from yours.

[01:05:02] Cameron: Ha, ha, ha, ha, ha. That wouldn’t make them top 300.

[01:05:06] Tony: possibly, yeah. But have a look at what are some of the small cap stocks we’ve got that have done well. Lindsay, LAU, I think is a small cap stock from memory.

[01:05:14] Cameron: Yeah, not this financial year.

[01:05:16] Tony: Oh, okay. It’s down, isn’t it?

[01:05:18] Cameron: down, yeah. And the next one on the list is HZN, VVA is up 14%, NHC is up nearly 13%, CVL, KOV, NZM, there’s a lot, MTO, yeah, but they get down. But certainly the big performers in the dummy portfolio for this financial year, SMR, TRS, ASG, big ish, particularly SMR, which is the bigger of the three.

[01:05:45] Tony: Yeah, right. And I guess the other problem that, that I have, and I guess you might in the ASX 300 and Steve might, I don’t know his, his, portfolio size, but if he’s focusing on large ADT stocks, it’s reasonable in size, I imagine. The problem is the alternative is if you want to [01:06:00] focus on small cap stocks, cause you think they’re going to outperform, you’ve got to have a large portfolio of small cap stocks.

[01:06:05] Tony: And I’ve, I’ve tried that. My experience is that the problem with that is, You’re buying titling amounts in small companies to not sort of, like, to not drive the price up when you’re buying, so you’re trying to buy 20 percent of their ADT, maybe even a little bit more than that, and you end up with a 50 stock portfolio, and then what I found is that it was, it was always the larger weightings that drove the performance, because if you had, you know, 10, 000 of something which went up 100%, and it was only 1 50th of your portfolio, it was the thing that you had, you know, 100, 000 in, that went up 30%, which is going to be a much bigger drive of the portfolio.

[01:06:44] Tony: So you may as well allocate more of your capital towards those positions anyway, because they’re going to drive your portfolio.

[01:06:51] Cameron: The other thing I noticed looking at the best performing stocks in the dummy portfolio is Stanmore. We’ve owned since October last year.[01:07:00] TRS we’ve owned since July last year, ASG we’ve owned since August last year, Horizons a new buy, only bought that August this year, but, those other ones, you know, we’ve held them for a long time, they’ve been very stable.

[01:07:17] Cameron: And, you know, Stanmore’s had a corker, it’s up 100%, oh hold on, no, if I look in the last 12 months, Lindsay’s up 100%, DUR is up 63%, where’s Stanmore? 35%, so all of Stanmore’s growth has come this financial year actually, but we held on to it for, we’ve had it for a year.

[01:07:38] Tony: So maybe the tide, maybe the tide’s turning when we’re getting out of that sort of churning phase of the market that we’ve been in,

[01:07:45] Cameron: yeah, I don’t know, TK. Don’t, who knows? It’s, it’s, I thought that a week ago.

[01:07:52] Tony: Yeah.

[01:07:53] Cameron: look at this, market’s up over six months, things are like stabilizing, and then it crashed and burned. [01:08:00] Who knows?

[01:08:01] Tony: Yes. Thank you, Middle East.

[01:08:04] Cameron: All right, well,

[01:08:04] Tony: 10 year bond yields. Yep.

[01:08:06] Cameron: let’s wrap, let’s talk, let’s go into after hours. apart from Slow Horses and Cape Schanck, what else have you got

[01:08:12] Tony: That’s it. Slow horses in Cape Schanck. Yeah, no, having a wonderful time down here playing golf. It’s been lovely. Buddy’s been great company. yeah, yeah. Been having fun.

[01:08:24] Cameron: That’s good.

[01:08:25] Tony: Yeah. no, good fun.

[01:08:28] Cameron: I didn’t think he was that great when he emailed me and told me what, how much I had to pay for my BAS payment yesterday. I’m like, ah, shit. So that time again,

[01:08:37] Tony: That’s a good thing though.

[01:08:38] Cameron: BAS, is

[01:08:39] Cameron: it?

[01:08:39] Tony: paying, paying tax, yeah, means you’re making money.

[01:08:43] Cameron: Yeah, in theory, yeah. well… You know, I, started to realize one of your entrepreneurial visions,

[01:08:51] Tony: Wow.

[01:08:52] Cameron: from years ago. Do you remember you had the idea, 10 years ago, maybe, for a device that you could like take a photograph of a [01:09:00] plate of food and it would tell you how many calories are in it? Well, GPT.

[01:09:06] Tony: Wow.

[01:09:07] Cameron: I’m not taking a photo of it yet, but it’s the next best thing. Now there’s this new version of GPT that’s rolling out at the moment where you can take photos of things straight into GPT, and it’ll tell you what you’re looking at, but you know, I’ve been using a calorie tracker again for the last six months to try and lose more weight.

[01:09:26] Cameron: And it’s one of those apps, you know, you have to look up the thing and figure it out. And if it’s something that’s complicated, like it’s not something you can scan a barcode on, you have to kind of work it out. What I had been doing for a while is asking GPT to work out the calories of things and then putting that into the calorie app.

[01:09:45] Cameron: And I just worked out this week, what the hell, I’ve just used GPT as my calorie tracker. So now I literally say to it, Hey, I just had a chicken thigh and a boiled egg. And, in a bowl of veggies and [01:10:00] maybe quarter cup of rice. And it’ll just work out what the calories are and it’ll keep track of it for me.

[01:10:08] Cameron: And then, and I can ask it questions as I go. I can say, you know, what should I have? Like how many, what, what’s my calorie deficit? What, what’s my, what are my macros? It says, Oh, you’re probably a little bit low on protein today. Okay. What should I, what should I look at that’s going to give me the protein, but be under my calories and blah, it’ll, it’ll make, give me suggestions.

[01:10:29] Cameron: It’ll talk to me, tell me what it thinks I can, you know, just ask it for recipe suggestions in the process. Just talk it, having, it’s like a nutritionist and a calorie

[01:10:41] Tony: Wow.

[01:10:42] Cameron: And a fitness instructor I can just talk to and it just is there waiting for me to tell it what I can just tell it. Oh, I ate this and a bit of that and this thing had a dressing on it.

[01:10:54] Cameron: Not sure what it was, but probably, you know, honey soy dressing and it’ll just [01:11:00] ballpark the calories for you

[01:11:02] Tony: That’s brilliant.

[01:11:03] Cameron: It is fantastic, I’d tell ya. And I can’t wait till I get the new photo,version. I’m gonna try just taking a photo of a bowl of food and saying, what do you reckon the calories of this are and see what it can work out.