Hello QAVvers

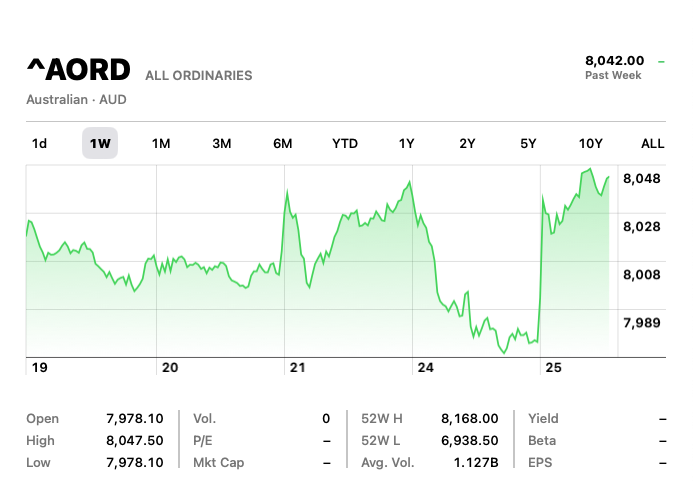

After yesterday’s retreat, the AORD rebounded today, on the news that Julian Assange has been released from jail and is coming home. Only kidding. Well not about him being released. But wouldn’t that be nice if the market was celebrating the reelase of an Australian hero?

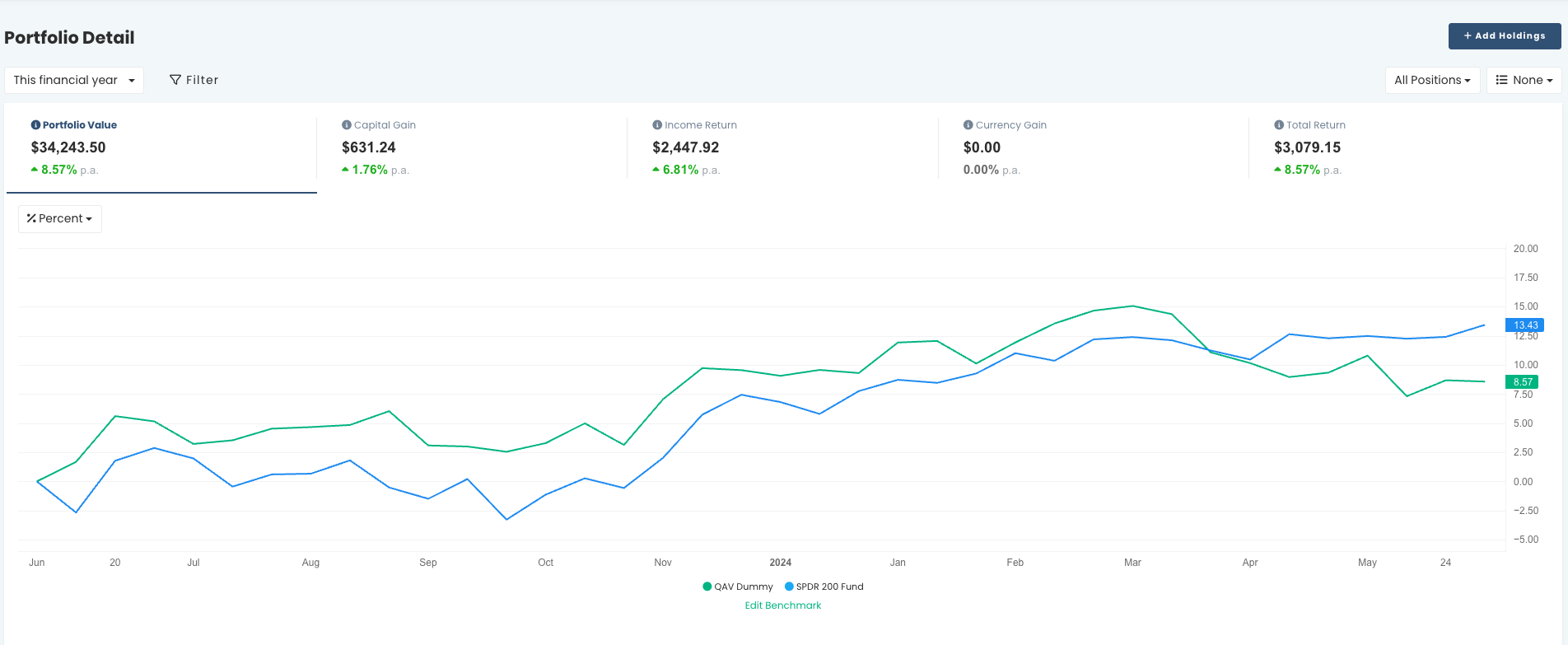

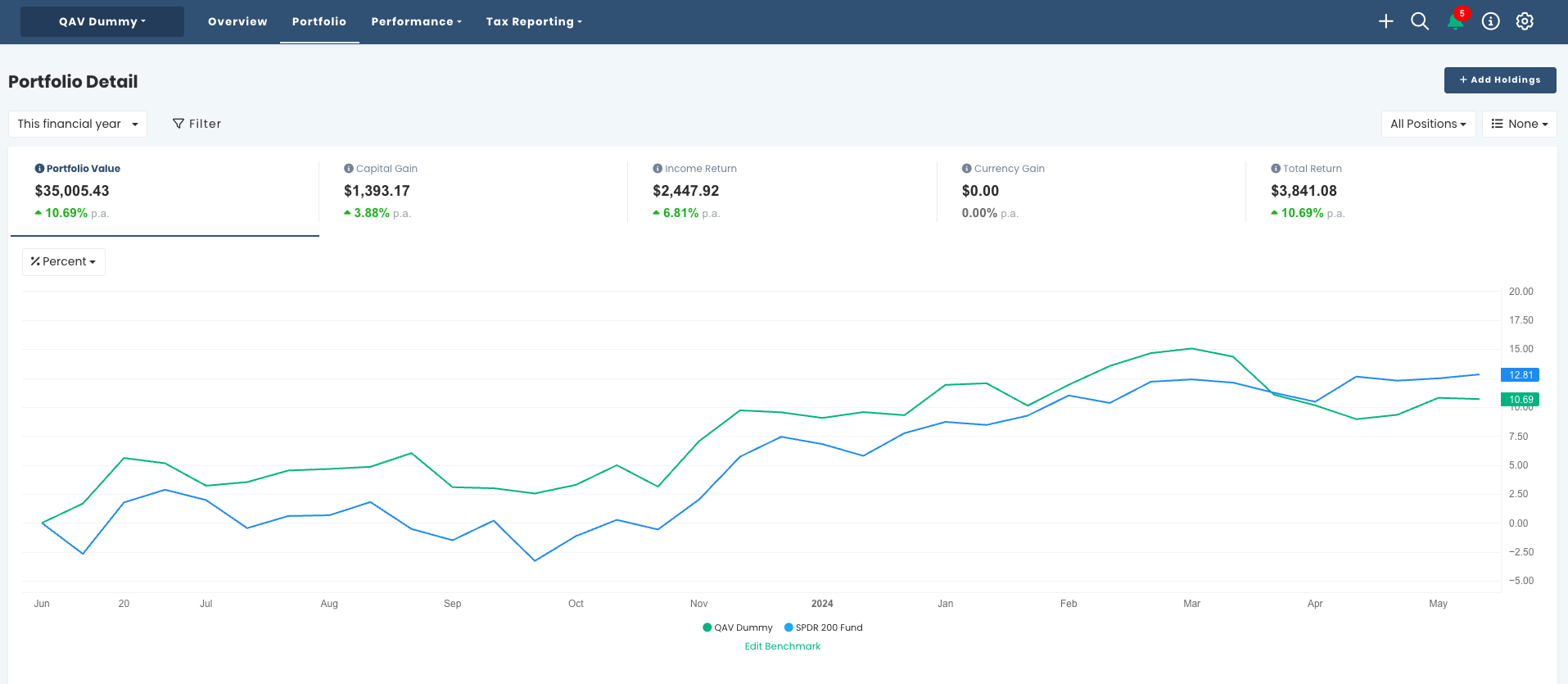

QAV PORTFOLIO REPORT

The Dummy Portfolio is performing well against the benchmark over most time frames.

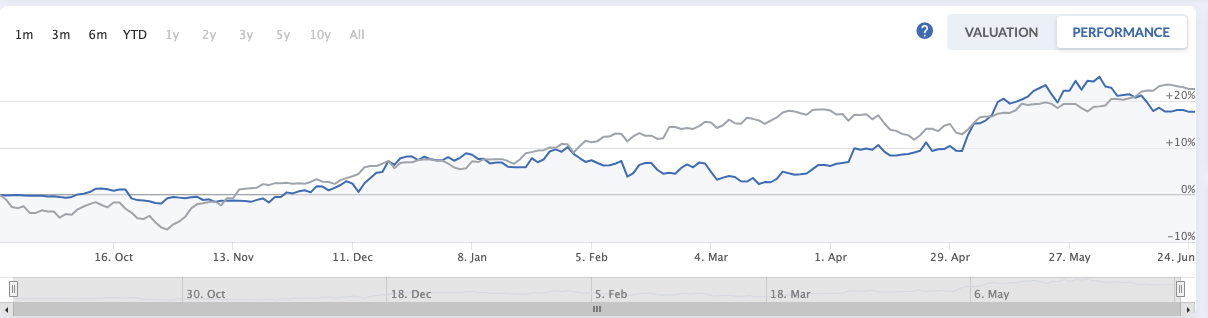

SINCE INCEPTION (15/04/2019)

Our portfolio is performing at a little below double market p.a. since inception (about five years).

For the 23/24 FY, the DP (8.57% p.a. CAGR) is significantly below the STW (13.43% p.a. CAGR), but still having a pretty good year.

In the last 7 days haven’t traded anything, and I still haven’t sold ASG, even though it’s still slightly below the 3PTL – it’s a “Vulcan Fudge”.

QAV STOCKOPEDIA DUMMY PORTFOLIO REPORTS

QAV AU DUMMY

Stockopedia doesn’t make it easy to report on the FY, but the Australian Stockopedia portfolio started in July 2023 and returned about 3.5% (Time-Weighted Return) for the year, versus the ASX200 at about 6.5%.

QAV US DUMMY

The US portfolio, which started in September 2023 and is now also below the benchmark, returning 18% versus the S&P 500 at 22.5%.

BUY LIST

Each week we produce a buy list that we share with our QAV Club members. The intended primary purpose of this buy list is for club members to use as a reference for comparing their own buy list. In theory, all of our buy lists should look pretty similar each week.

As always, please check our work, DYOR, consult a financial advisor before making any investing decisions.

LAST WEEK’S EPISODE

Join Tony and Cameron in episode 725 of QAV, recorded on June 18, 2024. They discuss Tony’s recent trends in the stock market, and the upcoming RBA decision. The episode dives deep into the Lindy Effect, its origins, and its implications in investing. Tony then presents a detailed ‘Pulled Pork’ analysis on Embark Early Education (EVO), highlighting its growth potential, financial metrics, and the colorful history of its founder, Chris Scott. The episode wraps up with discussions on industry competition, government subsidies, and some lively banter about Gold Coast entrepreneurs and RBA interest rates.

00:00 Introduction and Welcome

00:44 Market Update and Speculations

02:03 The Lindy Effect Explained

07:42 Pulled Pork: Embark Education

20:04 Management Controversies and Risks

28:34 Conclusion and Questions

Transcript

QAV 725 Club

[00:00:00] Tony: One, two, three.

[00:00:05] Cameron: Welcome back to QAV.

[00:00:07] Cameron: This is, uh,

[00:00:09] Tony: One, two, three.

[00:00:12] Cameron: you’re right there. This is, uh

[00:00:15] Tony: Yeah, yeah, we were talking about the Blues Brothers before. I just thought I’d give you a one, two,

[00:00:18] Tony: three.

[00:00:20] Cameron: You don’t have to go home, but you can’t stay here. This is episode 725. We’re recording this on the 18th of June, 2024. How are you, Tony?

[00:00:35] Tony: Very well, thank you, Cam. Just had a lovely long weekend with Alex up

[00:00:40] Tony: in Sydney doing lots of art gallery things, which was lovely.

[00:00:44] Cameron: She had such a lovely weekend. She forgot to send me the buy list yesterday.

[00:00:48] Tony: Oh, I got

[00:00:49] Tony: one

[00:00:49] Cameron: Yeah, you go one. I sent her a text at

[00:00:52] Cameron: like five 30 going. Are

[00:00:54] Cameron: you going to send

[00:00:55] Tony: Oh, no, I didn’t even notice you weren’t

[00:00:56] Tony: on the,

[00:00:57] Cameron: She said, Oh,

[00:00:58] Tony: I didn’t even notice you weren’t on . Weren’t on the

[00:01:01] Tony: email. Sorry.

[00:01:02] Cameron: quickly I

[00:01:02] Tony: No, I didn’t

[00:01:03] Tony: notice. Yeah.

[00:01:04] Cameron: Um,

[00:01:06] Tony: Yeah, she was working in working on it at my place

[00:01:09] Tony: too,

[00:01:10] Cameron: well, there you

[00:01:11] Tony: so I knew she did

[00:01:12] Tony: it. Yeah.

[00:01:13] Cameron: The market is up today. It

[00:01:15] Cameron: has been falling for the last, uh, three or four days. Went up on the 13th, morning of the 13th and then declined all the way down to this morning. It’s back up over 8, 000 this morning. Um, I don’t know why, don’t know what changed. Is it the RBA? Uh, decision that’s supposed to come down today, people are pre empting that,

[00:01:38] Cameron: maybe?

[00:01:38] Tony: I think so. Yeah, I think so. And obviously, you know, riffing off what’s coming in the us they’re about to release there. Equivalent of CPI numbers this week. So people are probably predicting that as well. Good luck to them.

[00:01:53] Cameron: Mm

[00:01:54] Tony: Isn’t it funny? It’s like, I’m so con so convinced. I know what’s going to happen in two days time.

[00:01:58] Tony: I’m going to place my bits now. I guess just kind of the opposite way of investing really. Isn’t it? If you think

[00:02:04] Tony: about it,

[00:02:05] Tony: how you should

[00:02:05] Tony: invest.

[00:02:06] Cameron: Well, we’ve, we’ve talked about this before, but, and it, it, I’m just continually amazed at, um, how flighty the market is. You know,

[00:02:17] Tony: Ooh,

[00:02:18] Cameron: nothing, you know, it’s just up and down. No one can decide what’s going on. It’s up one day, down the next, up the next, down the next, uh, anyway, I’m glad that. I just get to ignore it, mostly.

[00:02:31] Cameron: Um, people, since our last show, Tony, when we talked about the US, I’ve had a few people emailing me asking me to send them the US buy list. Um, uh, I don’t really have one. So the last one that I did was about a month ago, but I am going to have to do one in the next 24 hours because I have a stock I have to sell in the U.

[00:02:56] Cameron: S. today unless it goes back up against its three point trend line before I get around to it. MFG, I think it’s one of the finance companies that I hold. So what I’ve been

[00:03:07] Tony: Okay. That’s an Australian

[00:03:09] Tony: company as well. Magellan

[00:03:10] Tony: Financial.

[00:03:11] Cameron: Yeah, this is, a different one. Um, what I have been telling people is look, when I do one, I will make it available and you can have a look at it. Uh, the current version of it too, is really messy cause I didn’t design it for public consumption. Uh, so I’ll try and clean it up a little bit and give you a look at it.

[00:03:30] Cameron: But, um,

[00:03:31] Cameron: I’m not going to be doing

[00:03:32] Tony: I think

[00:03:33] Tony: there’s,

[00:03:33] Cameron: Any more often than I have to? That’s right. I was going to say, I’m not going to be doing them weekly at this stage.

[00:03:38] Tony: sorry.

[00:03:38] Tony: I didn’t mean to cut across you there. Yeah. So, I mean, it’s really important to note that this is a, we’re still trialing this. We haven’t got the checklist buttoned down yet. So I think if anyone takes that buy list for the US stocks and wants to make an investment decision, really do your own research and really look at the, look at your own analysis of those companies first, because we’re still.

[00:04:03] Tony: trialing a US version. And the other question I’ve got is, um, have you spoken to Stockopedia? Are they okay with

[00:04:10] Tony: sharing it at the moment? Because we’re using Stockopedia as a data

[00:04:13] Tony: source.

[00:04:14] Cameron: Well, I’m just going to

[00:04:15] Tony: And I think you’ve got some of their rankings and

[00:04:17] Tony: things like that in the in

[00:04:19] Tony: the checklist.

[00:04:20] Cameron: Good point. I’ll check with Elio about that. I mean, I could, providing the buy list is different from providing the checklist. So

[00:04:28] Cameron: I’ll maybe clean up the buy list and it’ll just be a scoring and that kind of stuff.

[00:04:36] Tony: Yeah.

[00:04:36] Tony: Okay.

[00:04:37] Cameron: The Lindy effect. Tony, have you ever heard of the Lindy

[00:04:40] Cameron: effect?

[00:04:42] Tony: I haven’t, but I read the link you sent me and I thought it was a great article.

[00:04:46] Tony: Near and dear to me, that kind

[00:04:47] Tony: of

[00:04:47] Tony: thinking.

[00:04:48] Cameron: This is something I picked up. Uh, in the last few days in Morningstar by James Gruber, distant relation to Hans Gruber, I believe, who sadly was, uh, murdered by an, uh, American terrorist, uh, in the Nakatomi building. Some decades ago. Um,

[00:05:10] Tony: Day or Christmas Eve. Whitefield.

[00:05:15] Cameron: to James Gruber. He says there’s a term called the Lindy Effect. The theory is that how long an idea or technology may last is correlated with how long it has already lasted. Put a different way, old things have better odds of getting older still than newer things. Getting older still than newer things.

[00:05:37] Cameron: He’s talking about, um, technologies that have stood the test of time, etc. The term was first invented by a media columnist before being taken on by statisticians, including Nassim Taleb, who popularized it in his book Anti Fragile, Anti Fragile. Taleb said of the Lindy effect, If a book has been in print for 40 years, I can expect it to be in print for another 40 years.

[00:06:02] Cameron: But, and that is the main difference, if it survives another decade, then it will be expected to be in print another 50 years. This simply, as a rule, tells you why things that have been around for a long time are not aging like persons, but aging in reverse. Every year that passes without extinction doubles the additional life expectancy.

[00:06:21] Cameron: This is an indicator of some robustness. The robustness of an item is proportional to its life. Taleb elaborated further in his later book, Skin in the Game, where he linked the Lindy effect to fragility. For Taleb, time is equivalent to disorder and resistance to the ravages of time, that is, what we gloriously call survival.

[00:06:43] Cameron: is the ability to handle disorder and things that have survived are hinting to us, ex post, that they have some robustness. And then, um, Hans Gruber Jr. goes on to talk about some of the oldest companies on the ASX. AGL, which I just added to my super this week because it’s on the buy list. Um, Washington H.

[00:07:04] Cameron: Sol Patterson, been around since 1872. AGL, by the way, has been around since 1837. ANZ, been around since 1835. Australian Foundation Investment Company, been around since 1928, Westpac 1817, BHP 1885, Equity Trustees, doesn’t say, Whitfield, um, been around since, Whitefield, sorry, since the 1920s, and Rio, which we talked about not too long ago, 1873.

[00:07:39] Tony: I think probably half that list has been a pulled pork at some stage

[00:07:42] Tony: too.

[00:07:42] Cameron: At least, yeah.

[00:07:44] Tony: Yeah.

[00:07:45] Cameron: you know, it obviously does tie in well with QAV because we are often looking for companies that have a good track record of, doesn’t necessarily need to be 150 years old, but a good track record of, um, running a healthy business, or turning around a badly run business, or a business that’s had some bad years, could be that way too.

[00:08:08] Tony: Well, yeah, they know what they’re doing, don’t

[00:08:09] Tony: they? They’ve got a lot of experience.

[00:08:13] Cameron: So I don’t, I didn’t figure out why it’s called the Lindy effect though, Tony, did you figure that out?

[00:08:19] Tony: Oh, I assume it relates to Charles Lindbergh, but I don’t know why it would be called Lindy

[00:08:23] Tony: Effect.

[00:08:25] Cameron: Let me

[00:08:25] Tony: Uh, oh, yeah, don’t know. Yeah, I did like the, um, I did like the quote, uh, uh, where is it now? Or something about that if it’s, if you’ve been around for a long time, you’ve got a robust forecast for how long you’ll survive, which is kind of how I approach life.

[00:08:46] Tony: Been around for 61 years, and I’m

[00:08:48] Tony: definitely forecasting another 61

[00:08:50] Cameron: At

[00:08:50] Cameron: least.

[00:08:51] Tony: Not true. Not,

[00:08:52] Tony: yeah.

[00:08:54] Cameron: its name from Lindy’s, a famous

[00:08:56] Cameron: delicatessen in New York

[00:08:57] Cameron: City.

[00:08:59] Tony: Ah, there you go,

[00:08:59] Tony: I was wrong.

[00:09:00] Cameron: The term was

[00:09:00] Cameron: first coined in the 1960s by Albert

[00:09:03] Cameron: Goldman, and later popularized by Benoit Mandelbrot and Nassim Nicholas Taleb. The original idea was based on the observation of comedians discussing the longevity of their television appearances at Lindy’s.

[00:09:16] Cameron: They noted that the longer a show had been running, the longer it was likely to continue. This concept was then generalized to apply to various non perishable entities, leading to what is now known as the Lindy Effect. The name stuck because it encapsulated the informal wisdom shared among practitioners in an everyday setting, emphasizing practical longevity over theoretical predictions.

[00:09:39] Cameron: I like that. I

[00:09:41] Tony: Yeah, that’s

[00:09:42] Cameron: wonder if Lindy’s is, uh, still around.

[00:09:45] Tony: ha! Yeah.

[00:09:50] Cameron: I’m asking GPT. Uh, searching. Lindy’s, the famous delicatessen, blah blah blah, is no longer in operation. The original Lindy’s closed in 1969. A new restaurant using the Lindy’s name opened in 1979, but ultimately closed its last location in February 2018. There you go. Well, it doesn’t last forever. Last a long time.

[00:10:15] Cameron: Well, I’ll tell you who didn’t last a long time was MMS’s CFO, Tony. The, uh, MMS CFO resigned rather suddenly, it seems, in March. It’s on our buy list, but, um, I noted the other day when I was doing the Lite, uh, Portfolio, uh, report, that it’s dropped a lot since the CFO resigned. And, uh, there’s been no new appointment since then, from what I can tell.

[00:10:49] Cameron: Uh, there’s no notification in, uh, Stock Doctor or in their announcements page about a new appointment anyway. So I’m thinking it should have been a bad news sell, maybe, when the CFO suddenly resigned. I didn’t pick it up at the time, and the market hasn’t responded well to it. There might be other things going on with MMS, but nothing that I could see.

[00:11:09] Cameron: We own two parcels of it. It has turned around in recent weeks, but, um, I don’t know, man, I’m wondering, should I dump it, um, or is it too late now? Has the ship sailed, and I should hold on to it until it breaches one of the other, uh, Selling triggers. What do you think?

[00:11:26] Tony: I hold MMS, so I haven’t sold. And I actually think we spoke about this when the CFO resigned, but I could be wrong. But um, I think around that time that the share price decline happened, they lost, uh, I’m going to say the South Australian government contract was a big contract anyway for leasing vehicles.

[00:11:45] Tony: And that’s probably the main reason why MMS went down. It was also around the same time it went ex dividend, so it could be a bit of that because it’s got a good yield. Um. Uh, yeah, so I’ve been holding it still way above its sell price and it’s starting to turn around now.

[00:12:02] Cameron: Right.

[00:12:03] Tony: I saw the, I saw what you sent me, I saw the announcement, the CFO had been there for three and a half years, and they’re sticking around until a new one’s

[00:12:12] Tony: appointed, so I don’t think it’s a red

[00:12:15] Tony: flag.

[00:12:16] Cameron: Oh, really? He’s sticking around?

[00:12:19] Tony: Yeah, it was in the announcement, he was going to stay until a new one was appointed.

[00:12:24] Cameron: Oh,

[00:12:24] Tony: So no, red flag for me is like, it looks like someone’s resigned rather than sign off on the accounts, for example. Um, and there’s like a mad scramble, they’re out the door, they haven’t, they haven’t, um, there’s no successor in place.

[00:12:38] Tony: Um, yeah, and you can sort of read between the lines that they weren’t happy putting their name to

[00:12:43] Tony: numbers that were coming out. I’m pretty sure that’s not the case with MMS.

[00:12:47] Cameron: I missed that last line. Mr. Conn will remain with Macmillan Shakespeare during his notice period to support an effective transition.

[00:12:57] Tony: Yeah.

[00:12:57] Cameron: Okay, alright, well, no panic then.

[00:13:00] Cameron: So, we won’t sell that, we’ll hold on to it, keep holding on to it.

[00:13:04] Cameron: Uh, survey update, had a few people email me their FY survey results, and as last time, they’re sort of All over the place.

[00:13:15] Cameron: Scott, FY 2324 was up 2.5% cagr. He said overall, since October 22 is down 5%. cagr, uh, what’s that? October 22, 23, he said, coming up to two years, 18 months, and it’s been a rough couple of years as we know Ed. Said, uh, based on share site from 6 4 21 until this is, Ed gave me his results last week and told me it was from Inception and I said, hold on, you haven’t been around that long.

[00:13:49] Cameron: You haven’t been a member that long. From 6 4 21 until today, 8. 17%. Um, Says, Playing around with dates, I put in the start date of 1722, which was when I went and started following the rules to the letter and rolled everything I have in. The result is 10. 92%. He points out that capital gain is down 3%, but dividends is up nearly 14%, so it averages out at 11%.

[00:14:15] Cameron: Um, since July 22. I’m not sure if that’s per annum or I assume it is with Sharesight. Yeah, but maybe time weighted return and not a CAGA result. He says, I’m still happy with this and think I’m getting more disciplined and more composed with decisions now than when I kicked off a bit rip and tear. Um, Daryl sent me along Email with his results, um, basically again using Sharesight, I think.

[00:14:53] Cameron: His overall return, and this is going back since January 2020 to June 2024, is an average of 14. 63 percent per annum. He also has a leftover portfolio using Intelligent Investor, which is up 7. 44 percent over the same period of time. So these QAV portfolios Roughly double his Intelligent Investor portfolio, which is good.

[00:15:19] Cameron: But as he points out from January, 2020 to the end of June, 2022, his QAV portfolio was up nearly 37 percent versus Intelligent Investor up six and a half. And then since then, his QAV portfolio is down 6%. Versus Intelligent Investor Up 8. 3. So it’s been a rough couple of years, he says, um, said like in the last year, since 2022.

[00:15:45] Cameron: He said he’s bought 40 stocks in total, currently holds 4, 9 gains, 31 losses, 23 of them were 10 percent sells. And I said to him, yeah, look, you know, you and I have talked about this a lot, and it’s been my experience, particularly with my super portfolio, and to a lesser extent with the light portfolios. I think our, the market has been so volatile that our rule one trigger has been getting us out of stuff.

[00:16:15] Cameron: Um, for the right reasons, because it could keep going down, but then we buy something else, and then it rule one triggers, and then we buy something else, and it rule one triggers, and, and, those shares are going up and down and up and down, and the market’s been quite flighty over the last couple of years, tripping our triggers, again, which are there for a good reason, to prevent a calamity should we experience another GFC.

[00:16:43] Cameron: But, um, it’s been sort of tripping us up for the last couple of years.

[00:16:50] Tony: Yeah. That’s, that’s my experience as well. I agree.

[00:16:54] Cameron: I’ve

[00:16:54] Tony: But it has quietened down this year. I must, I must

[00:16:56] Tony: admit I haven’t done much trading at all this

[00:16:59] Tony: year.

[00:17:00] Cameron: I’ve been, I’ve been trying to, uh, do some analysis on my super portfolio over the last couple of years, um, to look at, Uh, you know, that same analysis I did for the light portfolios. Um, if, if I hadn’t sold the stocks that I had to rule one, what would have happened, would, you know, would I have netted, net be in a better position now than I am, I haven’t finished coding that yet, but it’s my plan in my spare time is to try and code up something that’ll do that.

[00:17:36] Tony: You’ve done that before though,

[00:17:37] Tony: haven’t you? I thought you

[00:17:40] Tony: did that a few

[00:17:40] Tony: months ago.

[00:17:41] Cameron: I did that late last year for the light portfolios.

[00:17:43] Cameron: Yeah. Um,

[00:17:45] Tony: Ah, it was

[00:17:46] Tony: for the light

[00:17:46] Tony: portfolios. Okay.

[00:17:47] Cameron: And that one came out and said that it

[00:17:49] Cameron: was

[00:17:50] Cameron: sort of

[00:17:50] Cameron: net. net. Um,

[00:17:52] Tony: Mm hmm.

[00:17:55] Cameron: Um, I think I did with the light portfolios, I did, No, I didn’t do it just for the high ADT. I looked at something else for the high ADT. That was a volatility analysis that I did.

[00:18:06] Cameron: Um, but yeah, I, uh, uh, I did do that and you would think I could just take that code and reapply it to this, but I’ve forgotten what I did and how I did it. So I have to, I have to figure it out all over again, um, by unpicking what I did. Shouldn’t be too hard if I can throw a couple of hours at it. But, um, yeah, I mean, I, even once I do that, I don’t know what it’s gonna.

[00:18:31] Cameron: What I’m going to get out of it, what it’s going to teach me, like it’s just, um, you know, really just a scratch and itch.

[00:18:39] Tony: Yeah, and, you know, we did a lot of research into using 20 percent stop losses, and so I’m using 20 percent in my own portfolio at the moment, and it certainly hasn’t done any worse. I guess all that’s stopping me from bringing in that rule change to the QAV portfolio is that there just hasn’t been much trading anyway.

[00:18:58] Tony: The market’s been a lot less volatile. This year, since I started using 20%, so it’s hardly, it’s not a great time to compare one against the other when there’s been almost no trading

[00:19:09] Tony: anyway.

[00:19:10] Cameron: Yeah, right. Have you been playing with Matt’s regression tools

[00:19:14] Cameron: much lately?

[00:19:15] Tony: Oh, not, not for a couple of weeks. I had a bit of a burst a few weeks ago, but I need to get back to it.

[00:19:22] Cameron: I haven’t heard from Matt for a while, so I don’t know where he’s at with that either. But, um, certainly, yeah, the testing that we did with that with 20 percent was, um, made some improvements, but it wasn’t huge from memory.

[00:19:36] Tony: Yeah, correct.

[00:19:39] Cameron: Well, that’s all my notes for today. Tony, until we get into questions, what have you got?

[00:19:44] Tony: I had a couple of things. So, um, I didn’t share this with you cause I only came across it late in the day, but I have an article about Grain Corp, which was in the Fin Review, I think on Friday. I just wanted to briefly touch on that, um, and the only reason, the only reason I raise it is because it was, GrainCorp was on the buy list up until, oh, just very recently, I think.

[00:20:11] Tony: I own it, so I’ll declare that as well, um, and, uh, it’s only just below our buy list at the moment. So, uh, it’s, there’d probably be people out there who have. Uh, heard about it. Um, the article was about the fact that there’s been a lot of, um, wet weather in, uh, Australia recently, and that’s supposed to be a sign that, uh, there’s a lot of planting going on for cereal crops, which, um, you know, GrainCorp is a company which, uh, stores, uh, grain when farmers harvest and then help market it overseas.

[00:20:52] Tony: So, um, no, sorry, I’m just trying to find the article again and it’s, uh. I must have closed the window. Um, but a couple of, couple of takeouts for me in reading it. Um, here we go. The article’s called, GrainCorp looks beyond life as a rainy day stock. And that was on June 16th in the AFR. And I thought that was interesting in itself.

[00:21:15] Tony: I hadn’t come across that before, but apparently there are fund managers out there who trade GrainCorp based on the weather. Um, and uh, they tend to buy it when it rains because that’s, you know, Sign that there’s going to be a lot of planting and a good crop coming up and then they sell out of it when the weather heats up because the drought is, um, is not good for this company or for wheat farmers in general.

[00:21:38] Tony: Um, however, uh, the MD of GrainCorp has said that that’s why they took out, uh, uh, Uh, insurance, so that if they have drought conditions, um, their insurer Aon, um, pays them out. And if they have bumper conditions, then they return the, return the favor and pay a premium to Aon. And, um, that’s always been one of my questions about the company is, is, you know, is that to the benefit of shareholders?

[00:22:06] Tony: Because it’s, they’re trying to smooth the results and I get that. But, um, yeah, it does, it does mute. Um, the returns in good times. However, the article points out that the, this is something I didn’t know, that the, uh, cumulative payouts for GrainCorp are capped at 270 million. So these are, these are paid out in good years and, um, that cap is expected to be exceeded this year.

[00:22:32] Tony: So the article highlights that number one, they’re expecting it to be a bumper wheat harvest because of all the wet weather. And number two. They’re expecting Graincorp to be able to bank a lot more profits this year because it’s getting towards the end of its capped payout during good time. So there was two good things to

[00:22:48] Tony: note in that particular article about Graincorp.

[00:22:52] Cameron: So you’re thinking about

[00:22:53] Tony: So that was Graincorp.

[00:22:54] Cameron: putting the rain into our commodity checks,

[00:22:59] Cameron: the three point

[00:23:00] Tony: Yeah, it’s a good question, isn’t it?

[00:23:04] Tony: Well, no, I think, I think we’re going to, um, you know, the three point trend line will probably serve us well anyway. If it’s a cyclical stock, once it starts to come off, we’ll sell it. So, yeah, um, no, not going to put the weather into it. Um, and I guess, you know, the point is that GrainCorp management have seen this happen before and they’re trying to smooth out their returns with this, uh, you know, hedging policy.

[00:23:27] Tony: Policy they have with the insurance, um, insurance policy with Aon, um, to try and stop that from happening. So it may not be even be worthwhile putting the weather into, um, our thinking about this company.

[00:23:39] Cameron: hmm,

[00:23:40] Tony: Um, the other thing I, I picked up from the article was that, uh, and this is a question that was raised once before is, GrainCorp does well during a bumper crop because it’s, you know, it’s, it’s storing more grain and it’s selling more grain.

[00:23:53] Tony: And that’s how it clips the ticket in the grain market. And someone asked us, well, what’s the point of tracking the commodity wheat price, um, if we’re, if we’re volume driven in this company? And it was a good question, but, um, you know, the, uh, The article makes the point that as the price rises, farmers are incentivized to plant more.

[00:24:14] Tony: Um, and so the volume should follow as well, and that made sense to me too. I guess just circling back to that question.

[00:24:21] Cameron: hmm,

[00:24:22] Tony: So that’s grain cork, the grain cork article, and I have a pulled pork to share with you as

[00:24:26] Tony: well today.

[00:24:27] Cameron: who’s pork are you pulling today

[00:24:28] Tony: um,

[00:24:33] Tony: I’m going to pull a book for a company called, I’ve changed names, it’s now called Embark Education, and it was called Evolve.

[00:24:45] Cameron: hmm,

[00:24:46] Tony: I’ve got to say, I really struggled finding a pulled pork today, mainly because I’ve done most of the companies on the buy list, and I know that it’s probably enough time for some of them to come back and circle back and revisit some, but I do try and find a new one every time to do.

[00:25:02] Tony: But, um, a lot of the ones I picked out, which I hadn’t done before, were either very close to their sell lines, or they were commodity sells, or they were, like it was, um, there was one company I had a look at which is now called Articor, it’s the old Red Balloon, um, it was, it’s new on the buy list this week for the, um, I don’t think it’s been on before, so new for the first time.

[00:25:25] Tony: But if I looked at this graph, it was, you know, a huge falling knife. So there was a couple of those as well. So I was struggling to find something to talk about. I started researching Embark and then I realized what it was, which is an education roll up and run by some People who I’ll go into when I talk about the risks associated with this company or talk about the company and its culture and narrative at the end.

[00:25:52] Tony: Uh, and I, I, I hesitated to do the pulled pork on it. I will do a pulled pork on it and I’ll present the facts and I’ll let people, listeners, make up their own mind. Um, but it’s an interesting one, I guess, just to tease out a couple of issues around. Culture. So, um, this company, uh, Embark Early Education, uh, small ADT stock, I’ll say from the outset.

[00:26:19] Tony: So it’s only about 36, 000. Traded on average per day. Uh, it’s an early child care preschool educator. It’s Gold Coast based. It used to be called Evolve. And, uh, which was a, an operator of a chain of New Zealand child care centre businesses. Uh, that, that particular chain was sold off last year. Um, to private equity and the money was used to move to Australia and fund the Australian expansion.

[00:26:46] Tony: I think it did have a couple of Australian child care centres, but it’s focusing on Australia, uh, going forward. Um, they currently have 29 centres and they’re split, I guess, almost half and half between Queensland and Victoria. Uh, and they, I don’t think they use the Embark brand as a banner brand. They operate under the legacy brands for these childcare centers.

[00:27:08] Tony: And that’s, I guess that’s a hint at one of the important things about this company. It’s a roll up. So we’ve talked, I’ve talked about roll ups in the past. Um, they, they, uh, in my opinion, they’re, they’re great for growth until they stop. And then they, um, they struggle, uh, later on in, in their life cycle.

[00:27:26] Tony: Um, there’s even a Sell Your Center tab on the Embark website, guiding potential vendors through the sales process. So they’re very, very focused on acquiring new centers as part of their growth, uh, for this company. And so that’s one reason for doing this small ADT stock, is that it may not trade at 36, 000 per day in the future as it, as it grows.

[00:27:48] Tony: Um, because, uh, you know, the fund managers will see the growth. It will eventually get big enough to fall into their, you Um, onto their radar, and then it’ll sort of, I expect it will take off from there. And that’s the history of these kinds of roll ups. But I just really caution people on holding a stock like this for the long term.

[00:28:10] Tony: Because, um, they tend to have problems once the growth, um, stops. Or, once there’s an economic, um, headwind, like a, like COVID. COVID particularly hurt the child care center industry. So, uh, well, everything’s going well. They do really, really well. But, um, when things slow down, they can, they can have problems.

[00:28:32] Tony: Um, okay. Anyway, getting back to, uh, the company, um, they, I think the smart thing they’ve done is that they’ve sold those New Zealand businesses and that’s put cash in their bank in Australia. So the, the recent acquisitions have been funded from cash and it’s still cash and no debt on their balance sheet so they can continue to acquire.

[00:28:50] Tony: Other, uh, uh, businesses, and they’ve called out the fact that they’re still acquiring. They’ve also said that they are now looking at debt facilities. So, eventually the New Zealand money will run out and they’ll start to borrow to, to acquire these businesses. And that’s fine. There’s nothing wrong with that.

[00:29:08] Tony: But, um, one thing that they do do is they focus on EBITDA as a key performance indicator. And, um, do you remember what Charlie Munger

[00:29:16] Tony: called EBITDA?

[00:29:17] Cameron: Bullshit earnings?

[00:29:19] Tony: Bullshit earnings, that’s right. Now, they make the point in their presentations that they focus on EBITDA because they want to, uh, they’ve had a lot of overhead costs in selling out of New Zealand and moving to Australia, so I accept that.

[00:29:31] Tony: But we’re not going to focus on EBITDA when we do our analysis of the company. And at the moment, um, You know, their profit looks good as well because they’ve just had this huge cash injection from selling out of New Zealand. But it’s something that people need to be aware of and in the back of their minds that we’ll, we’ll judge them based on our usual metrics of paying interest and how that affects profit and PE ratios and all those kinds of things and earning per share forecasts and financial health.

[00:29:59] Tony: They can focus on EBITDA all they like, all they like, but we may not. Uh, they’re also. They’re also in a fairly competitive space. So I did a pulled pork on G8 Education a little while ago. So that’s the large company in the space. So they’re going up against them and they’re much, much smaller. And there’s a few other smaller companies and other ones on our buy list as well, Mayfield.

[00:30:20] Tony: So it’s interesting that this sector is on G8, Now, Embark and Mayfield are on our buy list. We’ve, I’ve talked about that before too, how sometimes, you know, without necessarily being thematic, we find that there are a number of players in a particular industry, all on the buy list together. I’m going to run through the numbers now, because I think they’re good numbers.

[00:30:41] Tony: I’ll come back and discuss the positives and negatives. So, I’m doing a, um, an analysis based on the price of 71 cents, uh, which I think it still is today, actually, last time I had a look. Uh, 71 cents is less than consensus target. It’s more than IB1, but less than IB2, which is 82 cents, so it scores for that.

[00:30:59] Tony: Bye. Recently started paying a dividend, which is good. So their yield is currently 7%. So we can score it for that. It’s higher than the, um, the average mortgage rate at the moment. Stock Doctor financial health and trend is strong and steady. So we give it props for that. And, uh, there’s an owner founder and the owner founder holds 16.

[00:31:20] Tony: 44%. So we will score it well for that. And I’ll come back to the owner founder when I discuss the company at the end. Uh, the P is 14. 6, um, which. Even though it’s kind of market average, it’s the lowest in three years, so that’s good, we score it for that. PropCaf is getting up there, but at the moment it’s 6.

[00:31:37] Tony: 8, so 6. 8 times, so we can happily accept that. Equity per share is 46 cents, so we can’t score it for book or book plus 30. And the interesting thing, which happens with roll ups, is the net tangible assets for this company is a cent. So, big difference between book value, which incorporates all the goodwill that they’ve amassed when they’re buying out childcare centres, and the actual net tangible assets, in other words, what’s the value of what they’re buying, excluding goodwill.

[00:32:06] Tony: You know, I think, I think, Goodwill is legitimate in these cases because, uh, you know, if you’re buying an existing business and it’s a childcare center, for example, and you’ve got all these people signed up and you’re looking after their kids, um, and they’re paying, Good money to, for enrollments and everything’s working well.

[00:32:27] Tony: I think it’s fair to pay goodwill rather than just the, you know, the cost of whatever the leasing is, you know, slept on the lease and all that kind of stuff and whatever equipment’s in the, in the child care center. So, um, but anyway, there’s something to watch out for and people need to be aware that the, the, uh, book value and the net tangible assets are vastly different.

[00:32:44] Tony: Earnings per share growth is, is great. The forecast is for 75 percent earnings per share growth. Again, that’s a, um, something that we look, that is a characteristic of roll ups. So, you know, growth minded investors will love this. Uh, and growth over P is 5. 1 times, so that’s way above our, our cut off of 1.

[00:33:05] Tony: 5 before we score it. Uh, it’s a recent three point upturn. Uh, equity is not consistently increasing, and I guess that’s because they’re, they’re paying, you know, taking cash out of the bank from the New Zealand sale and putting it to work. So, we don’t score up for that, but that’s not necessarily a bad thing.

[00:33:23] Tony: Uh, this company has a quality score all in all of 100%, which is good, and a QAV score of 0. 15. So, on the numbers, it works well for us. Couple of positives, the childcare sector is, uh, receives a lot of support from the government via rebates. And even though I do hesitate to invest in sectors which require government support, because it can be taken away with a change of government, I think childcare is probably safe, in that childcare rebates are being increased on both sides of politics.

[00:33:54] Tony: And it would be a bit of a vote killer I think, if they ever, uh, Reduce childcare rebates in the future. So even though it’s reliant on government subsidies, I think it’s probably safe from that point of view. Um, the other positive is it’s an experienced owner founder, and he’s returning to the industry to compete against their old company.

[00:34:11] Tony: So Chris, Chris Scott, who was the founder, used to be the MD or CEO of G8, the company I did a pool talk on, um, a few months ago and, and the largest one in this sector. Um, I’ll go through the RIS, so, uh, I mean, I’ve highlighted that I don’t like focusing on EBITDA, um, we’ll have to, we’ll have to look at, um, the numbers, you know, a bit lower down, I think, than that, uh, and EBITDA, EBITDA, um, Won’t change necessarily, even though they’ll arrange debt and become more indebted.

[00:34:48] Tony: So, because it’s earnings before interest and taxation. And if they have a lot of debt, that won’t come through in the EBITDA numbers. So we’ve got to be careful of that. It’s a roll up and they end. And if you look at the sector, um, ABC Learning is the classic one. Back in the 80s, I think it was, or 90s, when Eddie Groves

[00:35:06] Tony: from Queensland rolled up childcare centers, first of all, and

[00:35:08] Tony: then crashed

[00:35:09] Tony: and burnt.

[00:35:10] Cameron: What’s he doing today, Eddie

[00:35:11] Cameron: Groves?

[00:35:13] Tony: I’ve got no

[00:35:13] Tony: idea.

[00:35:14] Cameron: Oh, Eddie Groves. What a

[00:35:17] Cameron: character.

[00:35:18] Tony: G8, the history of G8 is, it has a similar sort of, um, cycle to it, not as bad as ABC, but, but, uh, they rolled up and rolled up and rolled up, and then, uh, got to the stage where there was a glut of childcare providers in the industry, and builders were building childcare centers on spec, hoping that, you know, companies like G8 would roll, would buy them, and they never did.

[00:35:40] Tony: And then there was just, uh, there’s lots of government subsidies in the industry. So people were opening childcare centers, um, left and right and got to the stage where, you know, back in sort of the mid 2010s, there were childcare centers were offering incentives to enroll people into their childcare centers, like giving away free iPads is one I recall.

[00:36:04] Tony: So this, you know, this could happen again when an industry is so Um, I guess so attractive financially, obviously the returns get competed away. That’s a basic, uh, tenet of economics. So, um, they do, they do run in cycles, I guess is my point. Um, something to focus on, and this is where G8 came unstuck is occupancy rates.

[00:36:25] Tony: So the way to measure, you know, the glut in the market or the supply and demand in the market is to look at the occupancy rates and, um, G8 came unstuck, I think when they fell below 80%. Uh, and. Uh, Embark is above that now, but that would, that would be a metric to watch out for, um, in the future, uh, if people want to, uh, invest in this stock.

[00:36:46] Tony: The last point I want to make is to look at the people who are behind, um, this company. And I’m just going to read a few articles from the Fin Review. I’m not going to draw any conclusions, um, I think, I think the facts will speak for themselves, but people need to be aware of who they’re dealing with. So, uh, we’re talking about Chris Scott, who is the, uh, uh, the founder of this company.

[00:37:13] Tony: Um, I’ll give you some background on him. And this is from a financial review article going back to. Uh, 2015, so it’s at the time when he was running G8, uh, education. Um, there’s a subheading in the article which says opinion divided. Scott is a, I’m quoting here, Scott is a divisive person among fund managers and bankers.

[00:37:34] Tony: Those that know him call him determined and ambitious, while others have painted him as a person with a checkered past. Chris is a businessman. As a businessman, is an extremely shrewd operator that knows how to get the most out of the people who work for him and has a tray of wanting to get things done, said one source who has known Scott for more than a decade.

[00:37:54] Tony: There is no doubt Chris has upset people, which has made for a good news story. Uh, so that’s one, one, uh, quote. I’m going to go back and into this article a bit further and I’m going to just get a bit of a history. On Chris Scott. Here we go. So, whether he controls, oh, so, I’ll skip over that.

[00:38:19] Tony: Chris Scott grew up in inner city Melbourne. His father was a floor sander, his mother a clerk. He left school at 15 to labour in factory jobs and then became a truck driver. Chris says, we had no money, I just couldn’t go on with school. I like driving trucks and I got to see Australia. There was freedom when you left the depot.

[00:38:36] Tony: I was pretty rebellious. I don’t like being told what to do. That’s why I knew I needed to work for myself. Scott began studying law by correspondence and gained a break by taking an exam, which landed him a spot at Melbourne’s La Trobe University where he studied economics, earning honours. Sick of Melbourne’s cold weather and after a year in Sydney, he chased a Chinese girl he met at university to Penang.

[00:38:57] Tony: The pair married and Scott’s strong connection to Southeast Asia began. Scott moved to Singapore in 1978 starting a road transport business hauling refrigerated freight between Thailand and Singapore and cargo to and from Malaysia. He later started two successful sea freight handling and marketing firms before selling and moving his family to the Gold Coast.

[00:39:17] Tony: It was fortuitous timing. The Queensland tourism market was booming and Scott began acquiring property management businesses. That morphed into a company called S8, the S standing for Singapore and the 8 representing the prosperity to the Chinese. That company listed on the ASX in 2001. Before merging with the then high flying investment bank MFS in a 700 million deal, million dollar deal in 2007.

[00:39:44] Tony: Scott debuted on the BRW Rich list that year with a $280 million worth, but lost just about all of it. When MFS collapsed spectacularly the following year, uh, he and the chairperson, the lady called Jenny Hudson, tried to salvage some of the wreckage from MFS in its dying days, but it was too late. The PAM managed to extract 20 well performing childcare centers, and despite not knowing about childcare.

[00:40:08] Tony: They saw an opportunity in the wake of ABC Learning. Scott later moved back to Singapore, only to re emerge two years later, again combining with Hudson, and moved into what was then known as Early Learning Services. It merged with their company Pace Childcare, and they later renamed the firm GA Education.

[00:40:26] Tony: I guess the G stands for Gold Coast. Successes followed, though critics remained. Scott says he never considered the life he has led would have been possible as a young man driving trucks. So that’s his background. And one more quote, because I don’t want to go on too much more about this. If I can find it, um, No, I can’t find it. I won’t bother. The last quote I was going to read was, um, No, no, I can find it. Here it is, here, sorry. So this is another article from the Fin Review, and this is, uh, September 30, 2019. The headline reads, Jenny Hudson accused of using childcare cash for ANZ Share Buy. So I’m, I’m going back to a stage where, uh, Jenny Hudson, who was the chair of, uh, GA Education, when Chris Scott was the, uh, MD, was being investigated for using company funds.

[00:41:22] Tony: And, and, uh, I’m not going to make any, uh, comments about that. That’s, that’s been, um, done and dusted, that story. But during the, uh, during the trial, uh, Mr. Scott appeared as a witness. Amongst witnesses on Monday was Mr. Scott, I’m quoting from the Fin Review, who described first working with Ms. Hudson when she was a corporate lawyer with McCulloch Robinson to help float accommodation provider S8 in 2001.

[00:41:50] Tony: He described her as brilliant, aggressive like himself, and a stickler for observing the law. Mr. Scott, who described himself as a former truck driver, spoke of rapidly growing G8 through acquisitions. Jenny’s job was to make sure I didn’t cut too many corners, he said. That was the beauty of the relationship, it worked perfectly.

[00:42:08] Tony: A range of people bought G8 Child Care Center takeover opportunities, including Mrs. Hudson. Ms. Hudson, he said the hearing continues. So I guess I just wanted to make people aware. of the CEO of this company and the colourful background that he has, a very successful background, I want to add. People made a lot of money out of GA before it hit the rocks and the company is still around today and we did the pulled pork on it recently.

[00:42:37] Tony: I guess the interesting thing about GA, if I recall back to when I did that pulled pork, is that they have changed their strategy and they’re not trying to roll up child care centres now, they’re trying to. Make the ones they have more profitable and they’re focusing on things like, um, IT to, to drive efficiencies there.

[00:42:55] Tony: So, um, yeah, uh, I, in my lifetime, and you probably have too Cam, I’ve seen these Gold Coast entrepreneurs come and go. Um, Chris Scott has survived, albeit through the, you know, listing and then, demise of S8 and the listing and I guess difficult period for G8 when he left the company and now he’s back to go head to head against his old competitor.

[00:43:25] Tony: So I can paint a picture where it says he knows the ropes and won’t make any mistakes he made in the past again. Or you can, you know, look at those articles about a divisive, uh, You know, figure in the industry, um, who maybe push things too far. So I’m not going to comment on that, but I just wanted to make people aware.

[00:43:45] Tony: The company has great numbers at the moment. It’s small, it’s growing fast. It’s not a company I would recommend people hold, you know, for the rest of their lives because roll ups tend to stop rolling up and have problems, but

[00:43:56] Tony: it could be interesting in the short term or short to medium term

[00:43:59] Tony: anyway.

[00:44:01] Cameron: Yeah, I was trying to work out, uh, what happened with Jennifer Hudson’s legal issues. I

[00:44:09] Cameron: can’t find

[00:44:11] Tony: I, I mean, I, I, she came up when I was searching Chris Scott, um, on the AFR database, and I couldn’t find out what happened either. But there was a number of, uh, number of ASIC probes into, um, her role with GA at the, at the time, and one concerned, uh, they were buying out another childcare. provider, and one concerned, um, whether there was a misuse of funds for her to personally buy some shares as well.

[00:44:38] Tony: But I couldn’t see what the results were.

[00:44:40] Cameron: yeah, very strange, cause the charges were brought five or six years ago and there’s, I can’t find what happened.

[00:44:51] Tony: Well, they should be resolved, you would have thought, but sometimes these things are treated confidentially as part of a settlement too, so we might not ever find out

[00:44:58] Tony: what happened.

[00:44:59] Cameron: Um,

[00:45:00] Cameron: I know she was

[00:45:01] Tony: But certainly life is colourful on the Gold Coast.

[00:45:04] Tony: Yeah.

[00:45:06] Cameron: Jennifer Hudson was formerly Queensland’s business woman of the year, too, before all of her legal issues came to light.

[00:45:15] Cameron: Um, okay. So there’s a pulled pork, uh, but some question marks over the management.

[00:45:25] Tony: Yeah, certainly on the numbers it looks good. I put question marks on the manager, but the manager is a proven successful operator. My question mark is, it’s ended badly twice for this person in the past. I’m just highlighting the fact that that may not happen this time, but people don’t want to buy this one and put it in the

[00:45:45] Tony: bottom drawer,

[00:45:45] Cameron: Hmm.

[00:45:46] Tony: think.

[00:45:48] Cameron: EVO is still the code for Embark. EVO, it’s now Embark, it’s still EVO. I

[00:45:57] Tony: Yeah.

[00:45:59] Cameron: think I have owned them at some stage. I’m not sure if they’re still. Um, in my portfolios. Just going to do a quick check.

[00:46:08] Cameron: Waiting for my spreadsheet to run all of its things that it runs when I open it up.

[00:46:15] Cameron: Well, uh, while I’m waiting for this, uh, something that I just thought I should point out. When Alex did get around to sending me her buy list for the week, and I was comparing her buy list to my buy list, that I had done yesterday. Um, everything looked in order. The one difference was VUK, Virgin UK, which is at the top of her buy list this week, with a QAV score of like 0.

[00:46:42] Cameron: 51 and I had it at 0. 21 and I spent a long time this morning before I went to Kung Fu trying to figure out Where the differences were, which is hard to do because I’m using the AF model and she’s using your master list. And so I have to try and match up data. What I realized in retrospect, I should have done was just give it all to GPT and say, find the

[00:47:06] Cameron: find

[00:47:07] Tony: Ha ha

[00:47:08] Cameron: in these two data sets, which I actually did as

[00:47:11] Cameron: a test when I got back and it found it in a second.

[00:47:13] Cameron: So what I’ve worked, what I figured out was her PropCaf number was half of my PropCaf number. And I was like, that’s weird. When I dug into it further, I found out that It was her operating cash flow number was different to mine. What I figured out is Stock Doctor must have updated VUK’s results somewhere in between when I did my download on Friday night and when Alex did her download, I think on Sunday, the results are updated because they have a, you know, I think like a March end of financial year.

[00:47:57] Cameron: Um, and so, big difference in their financials, which screwed up the

[00:48:03] Cameron: PropCaf number. Yeah. like over the weekend, literally, which is weird. I do own EVO, there you go, it’s in one of the light portfolios. Bought it 23rd of April, 68 cents, currently 71

[00:48:20] Tony: hmm.

[00:48:21] Cameron: It’s up 5%. Okay, I will make a note to keep an eye on

[00:48:30] Cameron: that.

[00:48:30] Tony: Ha ha ha ha ha. I just noticed on the AFR website that rates are on hold still. The RBAs met and they’re not increasing or decreasing

[00:48:42] Tony: rates.

[00:48:42] Tony: I

[00:48:43] Cameron: What has the share market done as a result of that?

[00:48:47] Cameron: Nothing much.

[00:48:48] Cameron: It’s hard

[00:48:48] Cameron: to tell. It’s a bit of a delay

[00:48:50] Cameron: in my things on Yahoo Finance anyway.

[00:48:54] Tony: Yeah, it’s still about the same, up 0. 78%, which I think it was

[00:48:58] Tony: going into the meeting probably.

[00:48:59] Cameron: That’s good to know.

[00:49:02] Tony: Hmm.

[00:49:02] Cameron: Alright, some questions Tony. Um, starting off with Alex. There’s about 12 questions from Alex. Alex F this is, not your Alex.

[00:49:13] Tony: Mm hmm.

[00:49:13] Cameron: thank you Alex for keeping us, uh, on our toes. First of

[00:49:17] Cameron: all,

[00:49:18] Tony: Yeah.

[00:49:18] Cameron: can TK please provide an overview of the ASX Substantial Holder announcements and how to read them?

[00:49:24] Cameron: Why do they occur? Does TK view announcements becoming, changing or ceasing as good, bad or neutral? Why would this act as a fudge? ASG is a good example, with recent examples of different announcements. Why would CBA become a substantial holder in ASG? I have to admit, I see these substantial shareholder things happening all the time, and I look at them from time to time, I’m never really sure, you know, how important they are, so I’m glad Alex asked the question.

[00:49:59] Tony: Yeah, it’s um, to give an overview of what they are, so there’s a whole set of rules that the ASX imposes around notifying people. I think it’s within two business days when someone buys at least a 5 percent stake. That’s, that’s the first one anyway. So if a fund manager comes along or anybody comes along and buys 5 percent of a company, they’ve got two days to notify the ASX.

[00:50:23] Tony: That’s probably the most common notification. And I. I think there’s lots of them these days in particular because superannuation funds and and other institutional investors are getting larger and larger and so they often do buy 5 percent stakes in companies or 6 percent stakes in companies so we see it all the time. I guess the reason for this In the past, um, when things weren’t as common, uh, as they are now in terms of, uh, large institutions being able to buy 5 percent stakes in companies, is it could, it was seen as being a potential start of a takeover of the company. So if you think back into the 1980s, when you had lots of corporate raiders.

[00:51:07] Tony: Running around buying stakes in companies, you know, John Elliott would buy a blocking stake, and Robert Holmes Court would buy a stake, and so they would have to notify people within a time frame that they were buying a stake, and then, um, stockbrokers and analysts could focus on that company and say, Hey, what’s going on here?

[00:51:23] Tony: Is it in

[00:51:23] Tony: play? So that’s kind of the background

[00:51:26] Cameron: Dar Paper,

[00:51:27] Tony: Yeah, exactly. Yeah. Um, what we’re seeing happening now, though, is a bit, is a bit more mundane. So, Bye. Bye. There’s a couple of things. Oftentimes, these notices are issued by what’s called a nominee company, so, or a custodian. So, uh, and one of the points that Alex raises is that the Commonwealth Bank is involved in one of these notifications for ASG.

[00:51:52] Tony: So, a nominee company or a custodian is somebody like a stockbroker or like a bank or someone who’s operating for institutions who are buying something on behalf of another beneficial owner. And they’ll have their own contracts in place to say that, you know, dividends flow through to the beneficial owner, even though in this case, I think it’s Colonial First State, which is owned by CBA.

[00:52:14] Tony: They own the shares, but they’ve got a back to back agreement with the actual person who’s paying for it, that they get the votes, the person who pays for it gets the votes and the dividends. So, um, that could be useful. For a whole heap of reasons, one of which is it’s a way for overseas investors to easily invest on the ASX if it’s done by a local broker or a local manager of these things, custodian.

[00:52:39] Tony: Or it could be that someone’s trying to keep their identity away from the stock market, so they don’t want the market to know that someone’s buying a position in the company. And it was, was interesting that one of the substantial Um, notices was from KKR who are, you know, a buyout firm. So this is for ASG.

[00:53:00] Tony: So, um, I thought that was interesting. I don’t for a minute think that KKR is going to launch a bid for ASG. Um, they may well just be, you know, investing as a, as an institutional investor in a company of their life. And the reason why I say it would be difficult for KKR to launch a takeover bid is that this company, um, is almost entirely owned by The car dealers who originally either started the company or who have been bought out and folded into the company.

[00:53:28] Tony: So there’s a lot of equity held by the key players, by the owner founders and by the subsequent car dealerships they’ve bought out. So it would be, unless it was a, unless KKL were going to launch a, a Knock out blow to get those people to sell. It’d be unusual for them to try and those owners and try and risk control from them.

[00:53:50] Tony: Um, but that’s what these, this is due, this is what these announcements are meant to do is to alert us to the fact that there’s big movements in the, either the voting control or the, um, the ownership of the company. And that’s another point to make is I think that the ASX rules talk about. Uh, Voting Control as, as their threshold for making announcements, not necessarily just ownership because companies, um, not so much in Australia, I don’t think we have.

[00:54:16] Tony: Different classes of shareholders in Australia, but in the states where they have similar rules, um, there can be voting stock and non voting stock, like in companies like News Corp, which allow people to retain control even though they don’t own the majority of the shares. So the ASX talk about voting control, a 5 percent stake, um, or controlling 5 percent of the votes, which is when you have to, uh, make an announcement.

[00:54:40] Tony: Uh, you then have to, I think it’s if you increase it by 1%. So if you own 5 percent made an announcement and then owned another 1%, so it’s now 6 percent you have to then announce it again to the ASX. So sometimes when we look at companies we see Page after page of ASX announcements in their announcement section, um, of these movements and it’s only because someone’s bought an issue like, like a colonial first state or even some of the index funds who are, you know, buying into larger companies, if they bought a stake of 5 percent and the share price has gone up and they’re forced to buy another 1%, they have to announce it.

[00:55:18] Tony: And so on and on it goes, um, there are then other rules. I think it’s, uh, I think it’s, I know the law says you can’t buy a 20 percent stake without launching a takeover, so I think you have to announce that if you get to 19 percent maybe, or maybe 20%, you have to make another announcement that you’ve increased your holdings.

[00:55:39] Tony: I think you have to do it again at 50 percent to let people know you now control the board. And then you have to do it again at 90%, which is when it’s a compulsory takeover. There’s probably some other ones in there too, but, but these are all, these announcements are all about alerting investors to the potential for corporate activity and potentially leading to a takeover in the company. Um, do I pay attention to them? Not really. No, I mean, occasionally I’ll, I’ll do it as part of my research, like for Austal, um, when they’re currently under takeover from a South Korean company who wants to buy the shipbuilder Austal. And I had a look at that when I was asked the question about it and noticed that Fortescue and I think one of the original owners had a large stake in the business.

[00:56:24] Tony: And I thought, well, that that is going to be difficult to, um, to take over a company when it’s got that kind of, um, cornerstone investment, uh, held by. Founders and locals. Not to say it can’t be, but it probably means that if it is taken over, it’ll be at a vast premium to

[00:56:40] Tony: where the share price is now.

[00:56:42] Cameron: AKR, speaking of Gordon Gekko, um, jeez, I remember reading a book of,

[00:56:48] Tony: yes.

[00:56:49] Cameron: remember reading a book about their takeover of RJR Nabisco back in the 90s, um, Merchants at the Gate, or Barbarians at the Gate, at the Gate,

[00:56:59] Cameron: you know, is it?

[00:57:00] Tony: And it’s a good movie too. Good movie starring James

[00:57:03] Tony: Garner

[00:57:04] Cameron: Oh, James Garner

[00:57:05] Cameron: Wow.

[00:57:07] Tony: Yeah,

[00:57:07] Cameron: I heard, uh, some of the Firefly crew talking about James Garner the other day. Um, yeah, I, I, uh, don’t think I ever saw the movie, but I remember reading the book. The whole junk bond, uh,

[00:57:20] Cameron: corporate takeovers, leverage buyouts, all those things.

[00:57:24] Tony: Marvin Milken, all those

[00:57:25] Cameron: Michael Milken, yeah.

[00:57:29] Cameron: yeah,

[00:57:32] Tony: Nabisco was the company that was, uh, you know, trying to be taken over. Uh, and it was a leverage, one of the first leverage buyouts, and they were struggling for growth, and one of the things they, their R& D lab had come up with was, um, cigarettes that didn’t have a smoke.

[00:57:48] Tony: There was no smoke to them like you could smoke them without blowing smoke in other words and that was going to be the great product launch going forward and then James Garner who’s the CEO is in the lab being shown. This cigarette and he goes, what’s that smell? And the scientist goes, yeah, yeah, we had to put this chemical in the cigarette to stop it from smoking.

[00:58:07] Tony: And Garner goes, it smells like shit. And the guy goes, yeah, yeah, we’re working on that. And Garner just goes, well, if it smells like shit, it looks like shit. I’m not launching this product. Yeah,

[00:58:24] Cameron: okay thank you for that, also from Alex, I appear to have missed crude being a cell, does that make ALD and pole a commodity cell? Now, I had a feeling we’d talked about this in the past, but I couldn’t find it in our notes. I had a look at the charts of crude oil and Ampol and there’s a little bit of correlation there.

[00:58:48] Cameron: I don’t know how strong it is. Uh, crude did become a sell a few weeks ago, so he’s right. Um, what do you think about Ampol and crude oil correlation toning?

[00:59:01] Tony: I think it, I think they do correlate because Ampol in particular out of, I think now all of the, well, there’s only two listed companies in Australia in the oil game. The old Shell, which is now Viva Energy, and Ampol. Ampol, well, they both actually have refineries, which would be impacted by the crude oil price, not, not less than the fact that, of course, retail petrol is affected by, the price of retail petrol is affected by the price of crude.

[00:59:29] Tony: Um, so, uh, I think it, I think it is a sell. Based on the price of

[00:59:33] Tony: crude.

[00:59:33] Cameron: Right,

[00:59:35] Cameron: well it’s not,

[00:59:36] Tony: I looked at, I looked at the buy list. We don’t have a, um, ALD as a comm stock in the, in the,

[00:59:42] Tony: um,

[00:59:42] Tony: spreadsheet.

[00:59:43] Cameron: that’s what I was about to say, yeah, I said that to Alex,

[00:59:45] Cameron: it’s, it’s not listed as a Comstock, um, is, uh, so we have to update that,

[00:59:53] Tony: I know when I, I owned Viva Energy stock last year and I remember selling it on the, on the three point trend line crude oil sell. Um, so I think at some stage we did consider Viva as a, as a, a stock which was moving. Not necessarily one to one, but certainly,

[01:00:10] Tony: um, influenced by the price of crude. Hmm.

[01:00:16] Cameron: Alex, good one, I’ll let the other Alex know to add that to the Comstock list so we, uh, pick that up in future. I wonder if I hold Ampol, uh, ALD, I do! Oh god, I hold it in several light portfolios, a super portfolio, my Stockopedia portfolio, and it’s downed a couple of percent on all of those too.

[01:00:44] Cameron: Ugh, Christ.

[01:00:47] Cameron: Okay.

[01:00:49] Tony: I had a discussion with Alex Hay about ALD a little while ago, and he was trying to position it as an electric vehicle charging company.

[01:00:57] Cameron: Who is he?

[01:00:58] Cameron: Musk? it’s

[01:01:00] Cameron: a robots company! Roll Robots! Elon got his payday approved by the shareholders. 45

[01:01:08] Tony: I did. my God. Yeah, I thought that, but, I mean,

[01:01:15] Tony: yeah. 84 billion US, yeah. I know Steven Mayne was, uh, Calling on, um, calling on, uh, the Future Fund to vote against it because they have a stake in Tesla.

[01:01:27] Cameron: So isn’t the Australian woman still the chairperson of Tesla?

[01:01:32] Tony: Yeah, Robyn Denham, I think her name

[01:01:35] Tony: is.

[01:01:36] Cameron: Former

[01:01:37] Cameron: Telstra?

[01:01:38] Tony: She was the CFO of Telstra. Yeah, yeah, she wrote the shareholders. Because remember that, um, Tesla was blocked from making the award because someone took them to court in Delaware, and a judge ruled that it was a ridiculous payment to make to any CEO, or worse to that effect.

[01:01:56] Tony: And then, uh, they put it to the vote in California or wherever Tesla is. Shareholders work and it got approved by vote. So, um, Robin wrote to all the Robin quite rightly as the chairperson wrote to all of the shareholders explaining why it was a good deal and they voted for it So there you go. What does the judge in Delaware know

[01:02:18] Tony: about the corporate responsibility?

[01:02:22] Cameron: Alright, moving right along, another question from Alex. He says in last week’s episode, TK explains value and quality investing. Value being buying a dollar for 50 cents, and then selling when it reaches its intrinsic value of a dollar. Okay. Quality, as I understand it, and to quote Buffett, is buying wonderful businesses at fair prices.

[01:02:41] Cameron: The former, we know, has higher turnover and trading costs. He then went on to use the two terms interchangeably, even though they have different meanings. Quite different buy and sell triggers. Can he please explain this further in the context of his system and the A SX as I believe our exchange is far more cyclical as it’s dominated by commodity stocks and banks.

[01:03:02] Tony: Okay, so if I did Conflate quality and value stocks. I apologize. I wasn’t meaning to but perhaps I was talking about QAV, which is a system which blends quality scores and value scores when I was talking about that. But yeah, certainly, yeah, value stocks are something you’re looking to buy cheaply and have them regress to the mean.

[01:03:21] Tony: I don’t necessarily advocate selling them when they reach their intrinsic value or their, or their intrinsic value. Um, or a dollar in this case, uh, and the quality side of things is just to give us some measure of comfort that the company’s going to be around for a while because it’s well managed. Um, but our, but our triggers are usually based on, on, um, on, well, really on momentum going out of the stock and falling either below our buy price plus 10

[01:03:49] Tony: percent or a three point trendline sale.

[01:03:53] Cameron: Yeah, and I, I, I would say even though Buffet obviously uses those terms and has his own way of applying them, QAV isn’t buffet.

[01:04:05] Tony: No, not at all. It’s probably closer to early Buffett before he was influenced by Munger and started to look for quality companies to buy at fair prices. We’re value, we’re primarily value investors. Price to operating cash flow drives most of

[01:04:20] Tony: our decision or a large part of our decision. And what to

[01:04:23] Tony: buy.

[01:04:24] Cameron: And as you explained it, this is the way I’ve come to understand it. The quality overlay is to make sure we’re buying businesses that seem to be well run, because we’re not experts in businesses or in sectors or in verticals. And we don’t want to be, we don’t want to invest the time and effort to become experts in businesses, which is different to Buffett

[01:04:46] Cameron: and what Charlie did.

[01:04:48] Cameron: They do spend all day, every day becoming experts in the businesses. And the industries that they invested, we don’t want to do that

[01:04:57] Cameron: because you’re lazy and I’m dumb.

[01:05:00] Cameron: So the lazy and dumb partners,

[01:05:06] Cameron: um,

[01:05:06] Tony: That should be just our standard answer to all of Alex’s questions from now on.

[01:05:10] Tony: Yep. We’re lazy

[01:05:11] Tony: and

[01:05:11] Cameron: we’re lazy and dumb. He’s Mr. Lazy and I’m Mr. Dumb. It’s goodnight from, goodnight from Lazy and it’s goodnight from me, goodnight. I was, I was explaining this. I, we had a new member I was doing sort of a zoom call with the other day. And, you know, I was explaining, you know, Tony doesn’t want to spend all day reading annual reports.

[01:05:35] Cameron: He wants to play golf and chase horses, um, you know,

[01:05:41] Cameron: or

[01:05:42] Tony: Hopefully I won’t catch them. Hopefully they’re faster than that. Yeah. Um, yeah, that’s a good point. I mean, you know, it’s, I know enough about business to know that there are some truisms. Like, if you have a lot of debt, it’s a bad thing. If you have a lot of cash, it’s a good thing. If you have an owner founder who’s very experienced in the industry, it’s a good thing.

[01:06:03] Tony: And various other things I’ve noticed over the years that we can put into a checklist. Which is generally applicable to businesses rather than on a case by case basis on it going to be right for every individual circumstance. So it’s a statistical approach, I guess, as much as

[01:06:18] Tony: anything really.

[01:06:20] Cameron: I’m just noting lazy and dumb as the title for this episode, it’s not going to count them all.

[01:06:26] Tony: You should write dumb and dumber and then cross

[01:06:28] Tony: out dumber and put in lazy.

[01:06:32] Cameron: Another question from Alex. Reflecting on the FY performance results, how do you live off a share portfolio that has several years of negative returns in retirement? Assuming you’re 100 percent invested in shares, e. g. if you have an S3, MSF with a value of a million dollars and for the sake of simplicity requires a hundred thousand each year to live and had a negative 15 percent return your capital is now 850, 000.

[01:06:58] Cameron: You couldn’t have many down years before you’re out of capital. Surely the good years wouldn’t get you back up to your starting position following such a drawdown.

[01:07:07] Tony: Yeah, it’s a good question and I guess it’s one that I’m facing going into retirement myself. Um, but I, I just, you know, want to, uh, emphasize the fact that you, the way I approach this and the way I think anyone should approach this is that you’re not living off the capital of your investments, you’re living off the dividends, the income.

[01:07:28] Tony: And there’s a thing in That any financial planner will be trained in from day one. I think it’s, well, I have different names for it. It’s generally called the rule of 25, sometimes the rule of 24 or 20, but basically it’s saying you want your capital to be 25 times higher than your needs to live off in retirement, because the average market dividend is about four and a half percent.

[01:07:51] Tony: Um, so, You, you know, if you’ve got a million dollars worth of capital, then you are only going to get 45, 000 income from dividends. And you might get a bit more if it’s in your super fund and you’re not paying tax on that and you get the franking credits associated with that. But, but that’s what you’re really banking on.

[01:08:07] Tony: It’s, it’s, um, a bit like, uh, going back to your mate who, uh, the guy you do the future podcast with, I’ve forgotten his name.

[01:08:15] Cameron: Sabatino,

[01:08:17] Tony: Samatino, thank you. The Samatino method, which was, um, we talked about one of the very early podcasts when we had Steve on the show. He, um, you know, he put money into the share market and forgot about the capital.

[01:08:27] Tony: He bought an index fund and has been living off the dividends ever since. And over the long term, that will go up. Um, despite years of negative drawdowns, like Alex talks about, could be down 15%, but generally companies don’t cut their dividends when the share price drops. They’ll, they’ll do whatever they can to maintain their dividend.

[01:08:46] Tony: Um, and that’s certainly the case in the market. I think even in the GFC, the market dividend may have gone down by like, 30 percent tops. So yeah, you might tighten your belt that, that year, but generally you’re getting a, you’re focusing on the income and the incomes, um, a lot more stable and continuous than the capital amount, which can move around.

[01:09:08] Tony: Um, so the, I guess the take up is make sure you’ve got enough capital and, and then some, and a buffer when you retire so that you can live comfortably off the dividends and I guess add a bit to take into account that, um, they may get cut slightly during particularly bad recessions.

[01:09:25] Cameron: Warren Buffer, Diljidev.

[01:09:28] Tony: Warren Buffett, yeah, right.

[01:09:31] Cameron: Thank you, Alex. Good questions. Um, last question, well, it’s not really a question. It’s, well, it is kind of from John. He says, My Excel sheet identifies Rio, yet it doesn’t appear in your stock filter. What am I doing wrong? Can you please assist? I checked on the Rio website, just in case more financial data was released.

[01:09:55] Cameron: Rio. Published Q1 2024 operations review. The report doesn’t include any financial statement data, and he gave me his numbers, which had a prop calf of 2.21, which was based on operating cashflow of 22.163, uh, 22, sorry, 22,163 million, so 22.163 billion. Shares issued 371, 000, no sorry, 371, 216, 214 shares. So I looked up Rio in my checklist that I did Monday.

[01:10:37] Cameron: I had a PropCaf of 8. 8, which is why it wasn’t showing up on my buy list. Um, and that was based on operating cash of 22, 163, the same as his. Thanks. Bye.

[01:10:52] Cameron: But op cash per share of 13.66 in a price, uh, at the time was

[01:10:57] Cameron: 120, uh, 20. When I drilled into stock doctor, it had shares outstanding as 1 6 2 2 0.53, which I think is in the millions, which is very different from the

[01:11:14] Cameron: 371

[01:11:15] Tony: mm hmm.

[01:11:17] Cameron: that, uh, uh,

[01:11:19] Cameron: John quoted when I went to the most recent annual report.

[01:11:24] Cameron: Uh, ASX, Rio said, weighted average number of shares, basic millions, is 1621. 4 million. Oh, is it dollars?

[01:11:36] Cameron: No, it should be

[01:11:37] Tony: Shouldn’t be a million dollars, no,

[01:11:38] Tony: it’s 1. 6, yeah, 1. 6

[01:11:41] Tony: billion.

[01:11:41] Cameron: My note is wrong. But on the ASX website for Rio, it says shares on issue, 371, 216, 216 million. So, there’s this difference here between weighted average number of shares, which seems to be what Stock Doctor’s using, and shares on issue.

[01:11:58] Cameron: And then I asked ChatGPT

[01:12:00] Cameron: to explain the difference between the two. It said weighted average number of shares. This figure generally represents the average number of outstanding shares during a particular reporting period accounting for any changes in the number of shares over that time frame. It’s a calculation used to determine earnings per share.

[01:12:18] Cameron: Factoring in share issues, buybacks and other alterations throughout the year. Shares on Issue is a snapshot of the total number of shares currently outstanding on a given date, as listed on the ASX website. It’s a straightforward count of all shares that have been issued and are held by shareholders as of the most recent date.

[01:12:36] Cameron: Seems to me like we should be using Shares on Issue for PropCaf and not Weighted Average Number of Shares, but tell me what you think, Tony.

[01:12:47] Tony: I think this is a good example of garbage in and garbage out, as to why AI won’t necessarily rule the world. Because I don’t think it’s a, I don’t think that’s the issue here. I don’t think it’s whether we’re using AI. Um, waived shares or shares on issue. Um, I had a look at it and there’s two companies that Rio trades under.

[01:13:08] Tony: One’s on the ASX, Rio Tinto Ltd, and the other one’s on the London Stock Exchange, Rio Tinto PLC. The ASX one has 371 million shares, the English one has 1255 million shares. If you add them together, you get to the 1. 622 number which Stock Doctor has. So, there’s uh, I’ve seen this before when BHP was a dual listed company, um, The companies report on their worldwide numbers, but they have different share numbers depending on the stock exchange, and if the data provider hasn’t twigged that they need to search a bit further and add the London numbers in, you get garbage in and garbage out.