Hi folks,

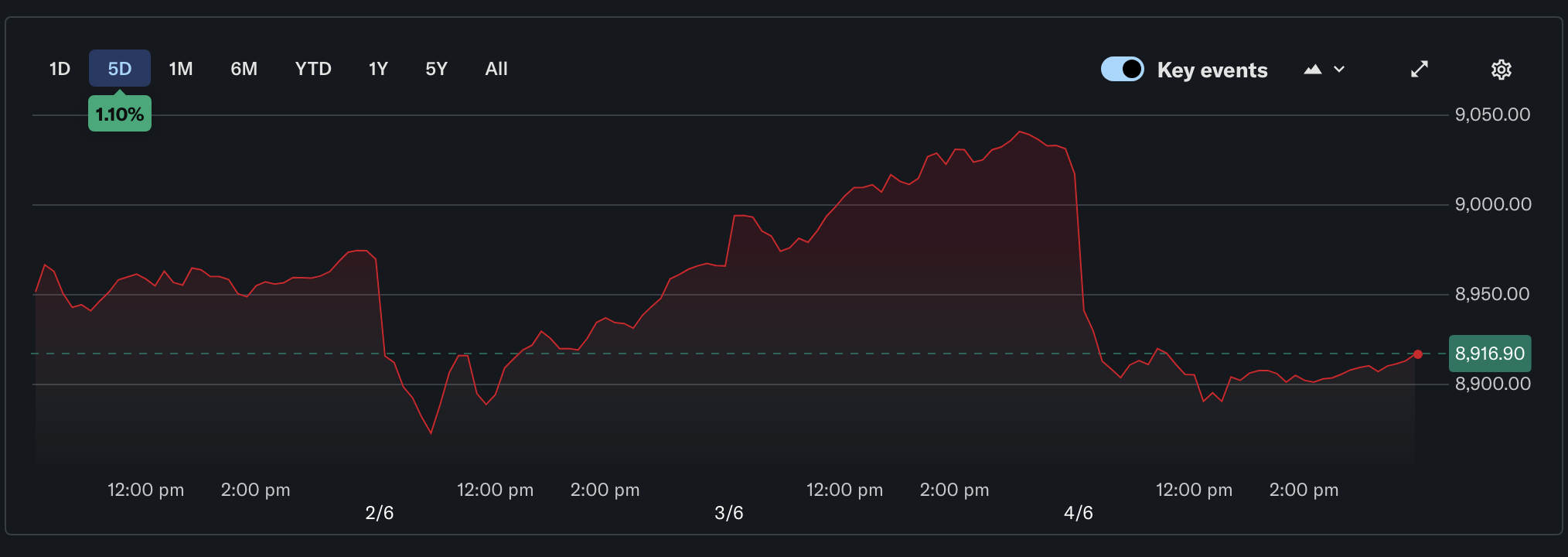

The Australian market experienced significant volatility over the five-day period, starting around 8,950 before climbing to peak near 9,040 and then suffering a sharp selloff that wiped the gains to close around 8,917. Middle East tensions and spiking oil prices drove the sharp pullback, creating widespread uncertainty across Australian equities.

The S&P 500 also experienced a volatile week, climbing from around 7,550 to peak near 7,600 before pulling back to close at approximately 7,584. The market’s choppy performance reflected mixed sentiment as the S&P 500’s impressive nine-day winning streak — its best stretch in weeks — finally came to an end amid profit-taking and concerns that Trump’s deal with Iran might be smoke and mirrors.

So, let’s get into my weekly updates and see where we are at.

All the Best,

Cam

QAV MYTH KILLERS

The Asymmetry of Ruin

I read this story in Tobias Carlisle’s latest book, “Soldier Of Fortune” (by the way, we interviewed him this week, should be out soon).

In October 1998, Warren Buffett stood in front of a room of business students at the University of Florida and offered them a deal.

Imagine I hand you a revolver, he said. A million chambers. One bullet. Put it to your temple, pull the trigger once, and I’ll pay you anything you want. Name the figure.

He said he wouldn’t do it for any amount of money because the upside didn’t justify the downside.

“I’m not interested in that kind of a game.”

And I think that’s one of the most important lessons about investing I’ve learned from Tony over the years we’ve been doing the podcast together. Investing successfully for the long term requires a philosophy of risk taking. There have to be certain risks you are willing to take, and ones you aren’t. It’s a mindset. It’s an attitude. It’s a discipline.

But it’s an idea almost nobody bothers to talk about, because it doesn’t sell newsletters and it doesn’t make for an exciting hot tip. It isn’t about returns at all. It’s about not getting wiped out.

Rule #1: Never Lose Money

Temptation is a wonderful thing. We’re all still tempted by “the grass is greener” even though we’ve been warned about it for thousands of years. Eve wants to eat the fruit of the Tree of Knowledge. King Midas gets exactly what he optimised for — everything he touches turns to gold… including his food… and he died of starvation. Anakin wanted to save Padme and gave himself over to the Dark Side.

It’s easy to get sucked into the hot, new girl in the red dress (or, not to be sexist, the hot guy in the red shirt) — Mag7, SpaceX IPO, crypto, BNPL, whatever the latest hype is.

But that’s why you need to have rules.

We always ask ourselves the same few questions.

What is the value of a single share (or coin) today?

And can I buy it at less than that value?

How do I know what it will be worth a year from now?

How do I know when to sell?

Because there will always be another red dress. The market lives to produce them. And if you chase after one, why not chase after all of them? How much time and money do you spend chasing them? When does it stop? Where does it end?

History says… it usually ends in ruin.

You can have nine brilliant years in a row chasing hot young things, and a single year where you lose everything. Up 30%, up 25%, up 40%… then one ‑100% and you’re back to nothing, no matter how good the story was up to that point. Gains add up. A wipeout doesn’t subtract — it resets you to zero and takes the compounding with it.

Buffett wrote about exactly this in his 2010 letter to shareholders, looking back at when he first took control of Berkshire:

“Even in 1965… perhaps we could have judged there to be a 99 percent probability that higher leverage would lead to nothing but good. Correspondingly, we might have seen only a 1 percent chance that some shock factor, external or internal, would cause a conventional debt ratio to produce a result falling somewhere between temporary anguish and default. We wouldn’t have liked those 99:1 odds, and never will.”

And then the line that should be tattooed on the inside of every investor’s eyelids:

“A small chance of distress or disgrace cannot, in our view, be offset by a large chance of extra returns.”

That’s the asymmetry. The upside and the downside are not playing on the same field. A big chance of a bit more money is simply not worth a small chance of being carried out. You only get one portfolio, and you only get one life to spend it in. The arithmetic of ruin doesn’t care about your batting average.

If we’re going to take a story about risk from literature, we want to think of Icarus or Odysseus. Don’t try to fly too high. Don’t listen to the song of the Sirens. Block your ears. Focus on your goal. Have some discipline.

When genius failed

If you want to know how seductive the other side of this argument is, look at the smartest people who ever fell for it.

Because we all think “I’m too smart to get caught out — I’ll sell in time if things go tits up.” But are you smarter than the Nobel Prize winners at LTCM?

In the mid-90s a hedge fund called Long-Term Capital Management opened its doors with what was, on paper, the greatest brains trust in the history of money. Two Nobel Prize winners on the masthead — Myron Scholes and Robert Merton, the men who literally wrote the equations modern finance runs on.

Their risk models told them they were safe. Properly safe. According to LTCM’s own numbers, for the fund to lose all its capital in a single year would require a ten-sigma event — odds of roughly one in a septillion. That’s a one followed by twenty-four zeros. An event so rare it shouldn’t happen once in the lifetime of the universe.

So they did what the maths invited them to do. They geared up — about 50 dollars of borrowed money for every dollar of their own.

Then the Asian financial crisis began in 1997 and in August 1998 Russia defaulted on its debt, and the impossible turned up right on schedule. LTCM lost around 44% of its capital in that one month. About US$4.6 billion gone in under four months. The Federal Reserve had to march fourteen banks into a room and arrange a US$3.6 billion rescue, not to save LTCM, but to stop the wreckage taking the rest of the financial system down with it.

The event their models said couldn’t happen in the age of the cosmos happened inside four years of opening for business, not exactly anyone’s definition of “long term”.

Here’s the lesson buried in that. Markets do not follow the neat bell curve the textbooks draw. They have fat tails. The “six-sigma” catastrophe that’s supposed to show up once every few million years actually wanders past every decade or so — 1987, 1998, 2008, 2020. The bell curve isn’t a slightly-wrong map. On the days that matter most, it’s the wrong map entirely.

You’re not running 50 to one. So what?

Okay so maybe you aren’t borrowing fifty dollars for every dollar you own to invest. So how does this story apply to you?

It’s the principle of risk and reward. It’s the mindset. The slippery slope of “too good an opportunity to miss out on”.

The question is never just “what’s the upside?” The question Buffett actually asks is “what happens if I’m wrong at the worst possible moment, with the most money on the table?”

And what is my discipline? What am I prepared to walk away from?

As value investors, we choose to stick to a plan — buying high quality companies at a discount to their intrinsic valuation and then holding them as long as our rules will let us. And saying “no thanks” to everything that doesn’t fit that theme.

A system that won’t hand you the gun

This is where having a process earns its keep, and where QAV does its quiet, boring, unglamorous work.

The whole apparatus is built to survive first and optimise second. Position sizing, so no single stock can sink the ship. Sell rules that get you out before a loss turns permanent — rules that fire whether or not you’ve fallen in love with the company. Quality and value, spread across the buy list rather than bet on one roll.

None of that is designed to catch the absolute maximum upside. It’s designed to make sure you’re never the poor soul standing there with the revolver against your temple, doing the expected-value sum.

That’s the part people miss. A system isn’t there to make you a genius. The geniuses had a fund, and a Nobel Prize each, and they blew up anyway. A system is there so that being wrong — and you will be wrong, often — never becomes being finished.

The market will hand you the revolver eventually. The red dress will always show up.

But like Odysseus, we plug our ears, put our blinders on, and remember the words of Syrio Forel, Arya Stark’s dancing master — “there is only one thing we say to Death: ‘not today’.”

STOCK ANALYSIS OF THE WEEK

I added a couple of stocks to the Light portfolios this week and you can see my Light posts here.

I also added something to the U.S. Light portfolio this week. U.S. Light and Club members can read about it here.

On the full Australian podcast this week, Tony did a deep dive on WEB. See the podcast link down below if you want to listen to his analysis.

BUY LIST

Each week, we produce a buy list based on our value investing system that we share with our QAV Club members. The intended primary purpose of this buy list is for club members to use as a reference for comparing their own buy list. In theory, all of our buy lists should look pretty similar each week.

QAV Value Investing Buy List (AU) 2026-05-29

Below is a link to the US list for this week (available exclusively to our U.S. Club members):

QAV Value Investing Buy List 2026-05-31

PORTFOLIO PERFORMANCE

We compare our performance to what we think is the most relevant benchmark (SPDR 200 in Australia, S&P500 in the USA), but if you’re new to investing, these comparisons might not mean much. Instead, you can compare our performance to the top-performing Super Funds in Australia and see why an amateur active investor (who has a system to follow) can out-perform most of the “professionals”.

We publish a fresh performance snapshot once a month. Weekly noise doesn’t tell you much in a value-investing system — what matters is the trend.

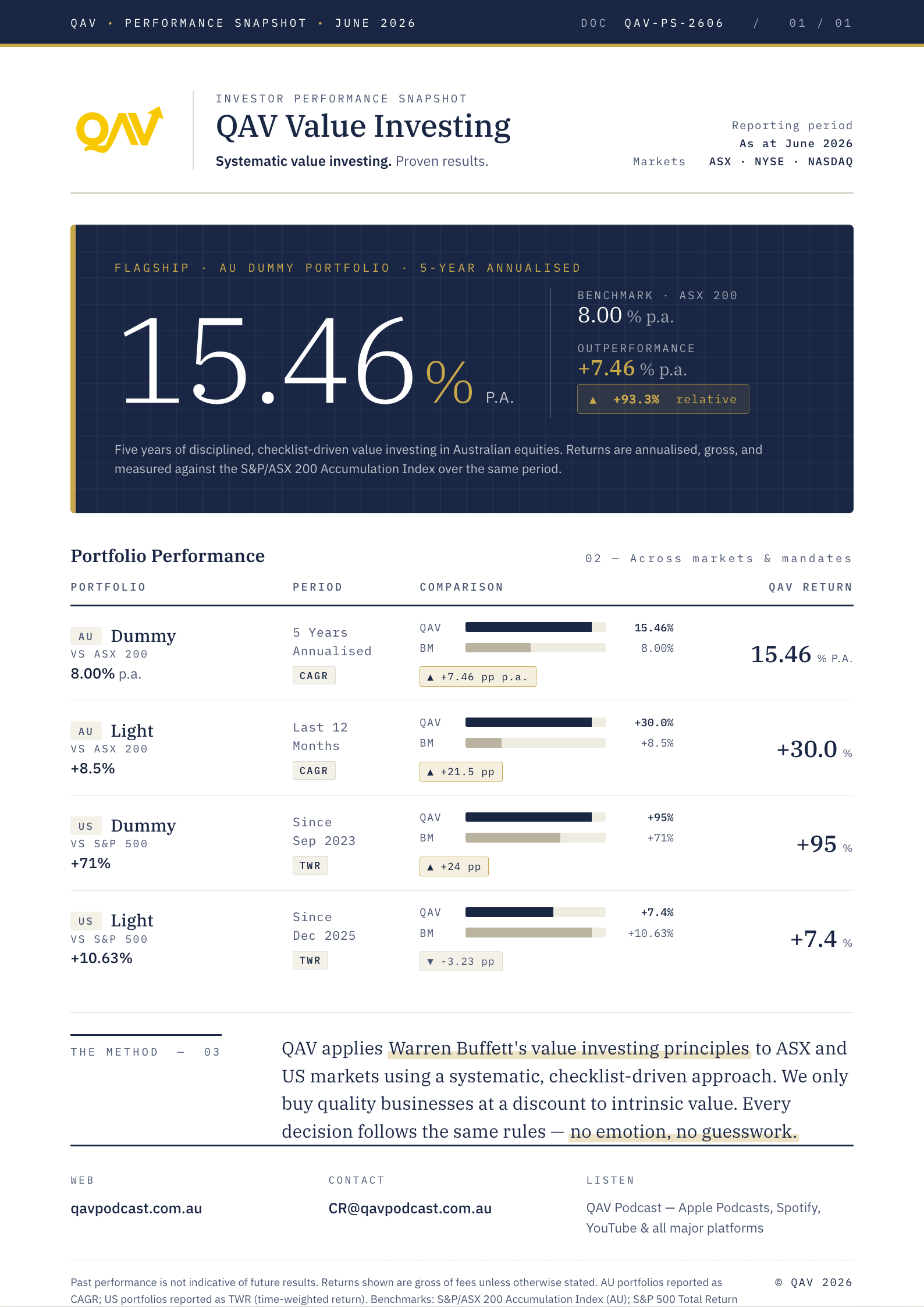

June 2026 performance snapshot.

Become a QAV Light Member today and start your investing on the right track

If you want to find out what we’re trading in QAV Light each week, sign up to become a member. You’ll get an email from me every Monday letting you know what we’re buying and selling in that portfolio. You can choose to copy our trades or not. It’s the easiest way to start your rules-based investing career… and you don’t even need to know the rules. I’ll follow the rules for you. It’s a good first step to eventually becoming a QAV Club member and learning how to run the system by yourself.

QAV LIGHT: Someone already cleared the way.

(Note: Americans interested in joining QAV Light or Club please go here instead.)

THIS WEEK’S EPISODES

Beds, Banks and Bionic Men: WEB Travel in the AI Age: QAV AU #922

Anchored Down in Anchorage: NRIM – QAV America #55

STOCK NEWS AND UPDATES

COMMODITIES

This week the big changes to commodities were the following:

| Commodity | Status |

|---|---|

| Coal (thermal) | BUY |

| Magnesium | BUY |

| Wheat | SELL |

DISCLOSURE

Please review our trading and disclosure policy.

SIGNING OFF

Hope you found this week’s deep dive into WEB enlightening – always fascinating to see how the numbers tell the real story behind a company’s prospects. With coal and magnesium both flashing BUY signals, it’s a good reminder that value opportunities often hide in the unglamorous corners of the market while everyone else chases the shiny objects. Remember, successful investing isn’t about being right all the time, it’s about being patient, disciplined, and letting the data guide your decisions. Keep sticking to the checklist, trust the process, and don’t let the market noise distract you from building long-term wealth.

SSDD!

- Cam

That’s it for the week!

QAV A GOOD SHAREMARKET!

Got a question? [email protected]