Hi folks,

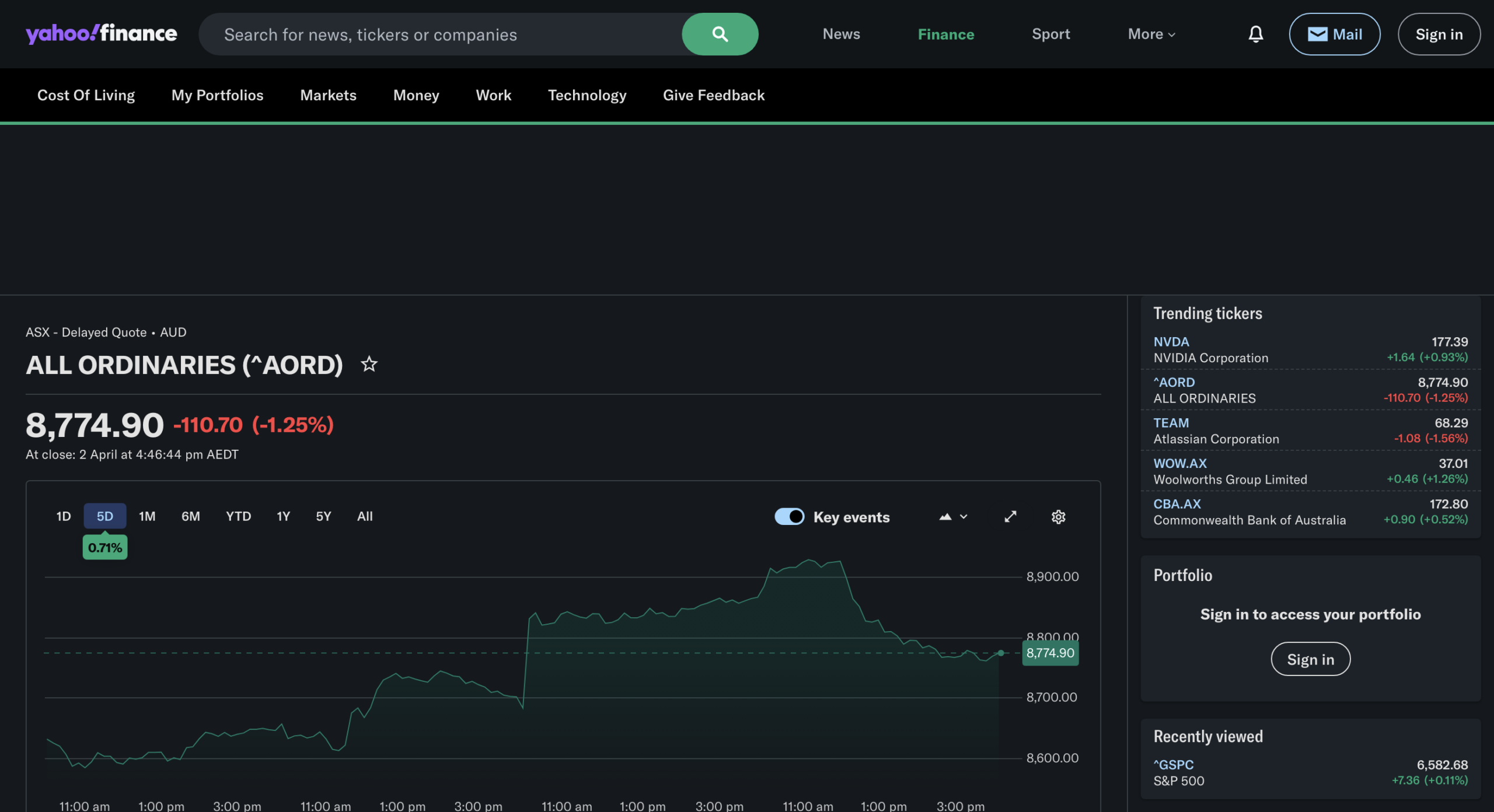

The All Ordinaries finished up over the five-day period, despite Albo’s warnings that we’re facing a difficult economic period and Trump’s talk about bombing Iran back into the “stone ages”.

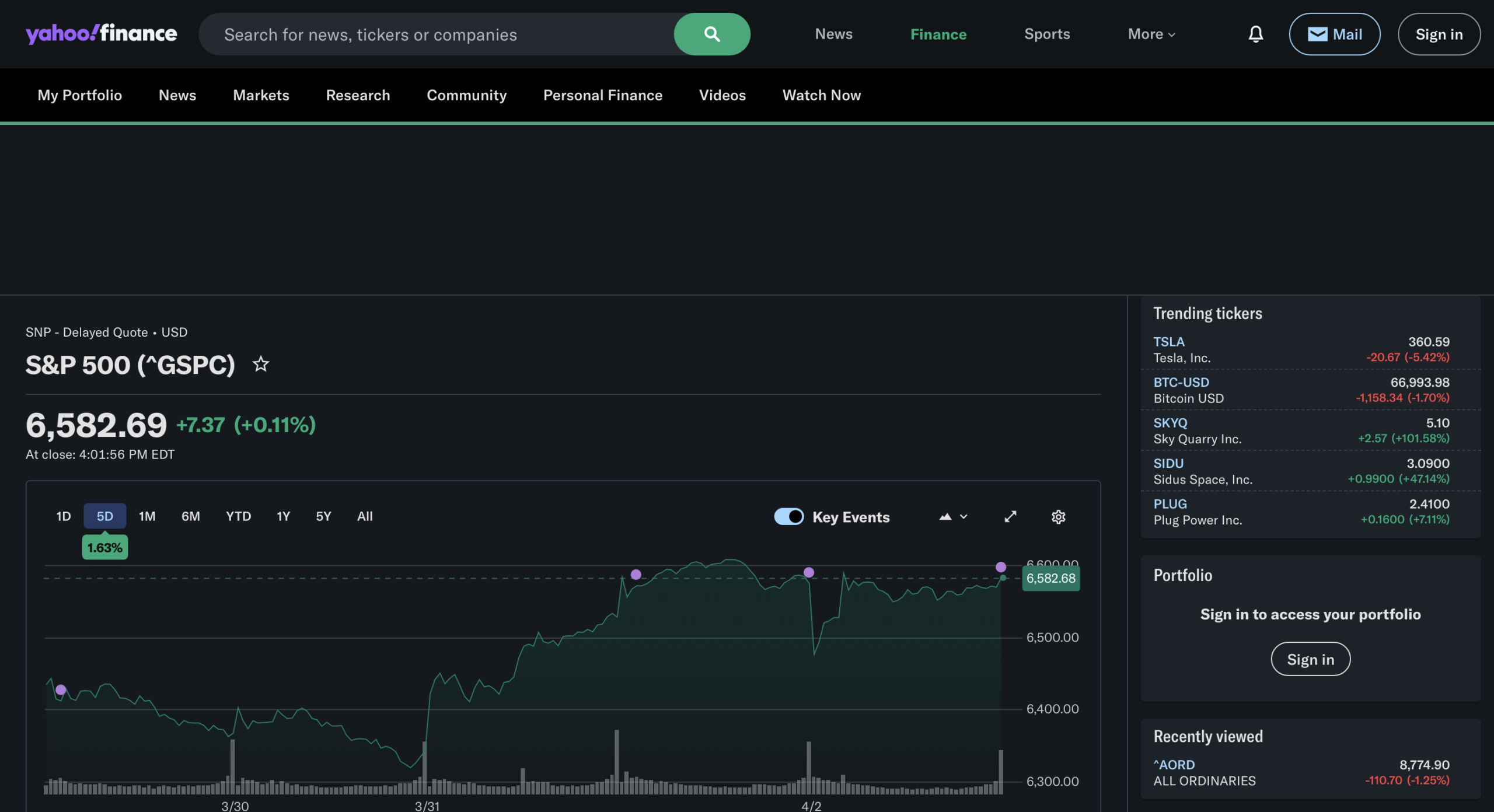

The S&P 500 is also up over the five-day period, climbing from around 6,400 to close at 6,582.69.

So, let’s get into my weekly updates and see where we are at.

All the Best,

Cam

QAV MYTH KILLERS

The P/E Ratio Is the King of Valuation Metrics

In the year 2000, Enron had a P/E ratio of around 60. Wall Street analysts were tripping over each other to slap “Strong Buy” ratings on it. Fortune magazine named it “America’s Most Innovative Company” for six consecutive years. The P/E ratio said it was expensive but worthy of the premium. The business, it turned out, was a spectacular fraud. Within eighteen months, it was rubble.

The P/E ratio did not see it coming. It never does.

The First Metric You Learn Is the Least Reliable One

One of the first metrics you’ll encounter when you start your investing journey is the P/E Ratio — the price-to-earnings ratio. It’s calculated by dividing the current share price by earnings per share (EPS), and it’s everywhere. Analysts cite it, financial journalists lean on it, and it’s the first number that comes up whenever someone asks whether a stock looks “cheap” or “expensive.”

Which makes it a problem. Because it’s also one of the easiest numbers to manipulate.

Why People Believe It

The appeal is obvious. The P/E ratio is simple. You can look it up in three seconds. It gives you a number, and numbers feel objective. A P/E of 10 feels like a bargain. A P/E of 50 feels alarming. This apparent clarity is enormously comforting in a world that’s otherwise messy and unpredictable.

There’s also the historical pedigree. Benjamin Graham, the godfather of value investing, used earnings as a core part of his valuation framework. And when Graham is your intellectual ancestor, the idea carries real weight.

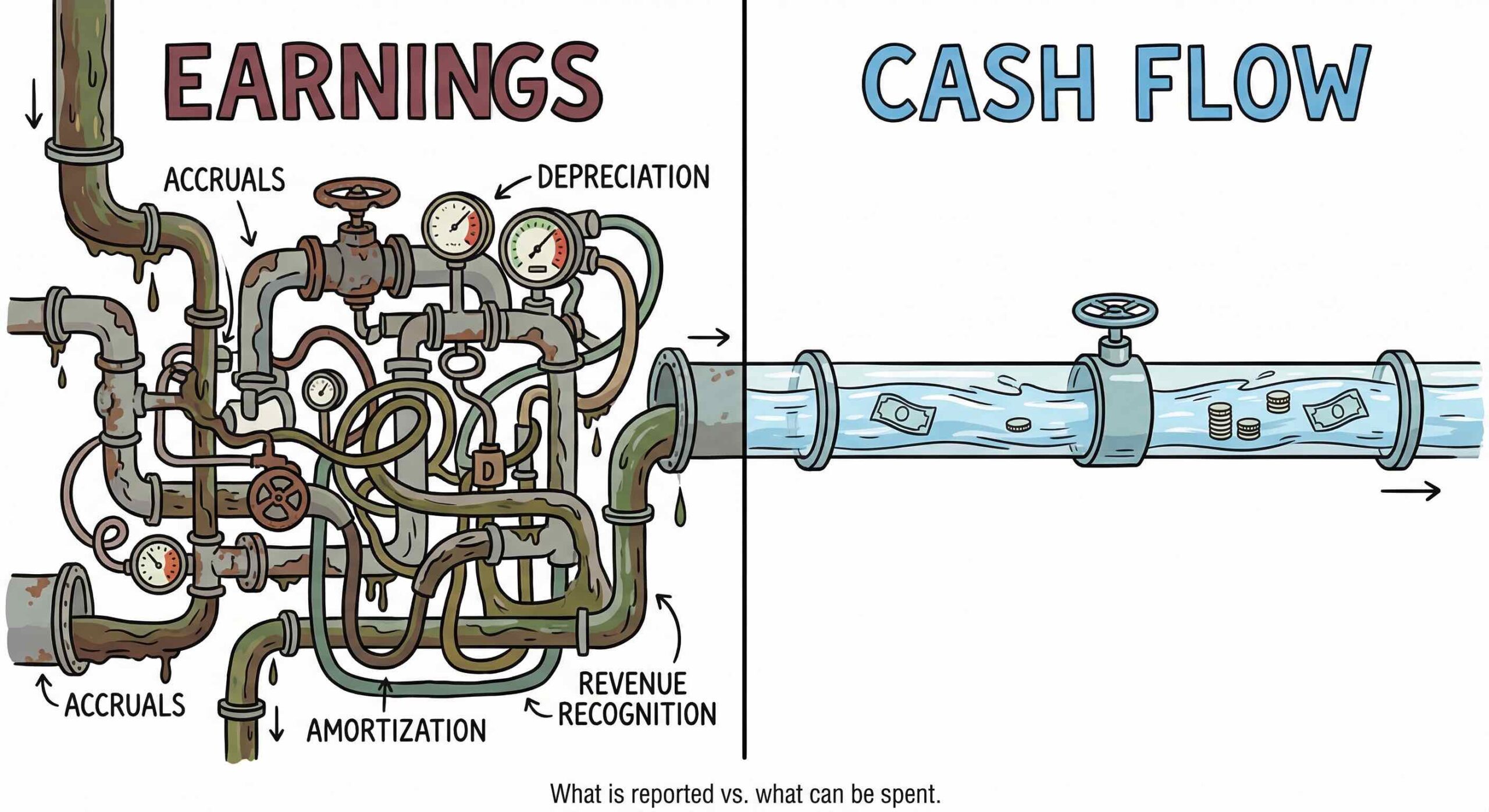

But here’s the thing about earnings: they’re a management decision.

The Levers Behind the Number

Let me put it this way. If you offered me a 50% share of your coffee shop for $100,000, the first question I’d ask is: how much cash is the business actually generating?

If you told me $200,000 a year in cash flow, I know I’d get my money back quickly — in rough terms, about a year, with zero overheads factored in. That’s a conversation worth having. If you told me the business was generating $10,000 a year, I know it’s going to take twenty years to get my money back. And twenty years is a long time. Think about what the world looked like twenty years ago. We were carrying Nokia 3310s and thinking Napster was a permanent lifestyle. A lot can change.

Cash flow tells me something real. Earnings tell me something that was constructed.

When we started doing the podcast, Tony explained the problem with earnings this way:

“What I’ve found over the years is that the further you go down a company’s financial reports, the more it becomes a management decision as to what figures get put in there. Operating cash flow, at the top of the statements, is the hardest thing to manipulate. Earnings are not. A manager can pull lots of levers across the three accounting statements — provisions on the balance sheet, adjustments to depreciation, decisions about goodwill amortisation — to make their numbers look however they want them to look. Sometimes they do it to hit a bonus target. Sometimes they do it to make next year’s comparisons easier. I’m not saying all managers are crooked. But it’s human nature to present yourself in the best possible light.”

This is why the big scandals — Enron, WorldCom, HIH in Australia — are always earnings scandals. Nobody fakes the cash coming through the front door. That’s much harder to hide.

What We Use Instead

When you start using QAV, you’ll see we focus on a metric called Price-to-Operating Cash Flow — which we call PROPCAF.

Unlike earnings, operating cash flow is the real money a business is generating from its actual operations, before the accountants have had a chance to finesse it. It sits at the top of the cash flow statement, and companies are legally required to report it. The further down the financial statements you go, the more room there is for interpretation. Operating cash flow sits right up there at the top, in the clearest possible air.

Over years of regression testing our checklist, we’ve found that PROPCAF is one of the single most powerful metrics we have. When we strip everything else out and test our metrics individually, PROPCAF by itself delivers the most outperformance of any single variable. Everything else we check — management ownership, financial health scores, revenue trends — adds to the result, but PROPCAF does the lion’s share of the work.

We Don’t Completely Ignore P/E

To be clear, we haven’t thrown P/E in the bin entirely. One of our checklist items looks at whether the current P/E is the lowest it’s been over the last three years — which is a useful signal that a stock is cheap relative to its own history.

But we’re not using P/E as a north star. We’re using it as a single data point in a much more rigorous framework. One instrument on a large dashboard, not the whole instrument panel.

The Question to Ask

So the next time someone tells you a stock looks cheap because the P/E is low, ask them one question: What’s the operating cash flow look like?

Because earnings are what management wants you to see. Cash flow is what’s actually happening.

At QAV, we’ll always take the real thing.

STOCK ANALYSIS OF THE WEEK

I’ve found a few things to buy this week (surprise! Oil Stocks!) and you can see my Light posts here.

I also added something to the U.S. Light portfolio this week. U.S. Light and Club members can read about it here. Not an oil stock!

On the full Australian podcast this week, Tony did a deep dive on oil stock BRK. See the podcast link down below if you want to listen to his analysis.

On the American episode, I did a deep dive on Pitney Bowes (PBI). Really fascinating story. Been around 100 years, they handle the stamping and sorting of snail mail for businesses large and small. See the podcast link down below if you want to listen to my analysis.

BUY LIST

Each week, we produce a buy list based on our value investing system that we share with our QAV Club members. The intended primary purpose of this buy list is for club members to use as a reference for comparing their own buy list. In theory, all of our buy lists should look pretty similar each week.

QAV Value Investing Buy List (AU) 2026-03-29

Below is a link to the US list for this week (available to our U.S. Club members):

QAV Value Investing Buy List 2026-03-31

PORTFOLIOS

We compare our performance to what we think is the most relevant benchmark (SPDR 200 in Australia, S&P500 in the USA), but if you’re new to investing, these comparisons might not mean much. Instead, you can compare our performance to the top-performing Super Funds in Australia and see why an amateur active investor (who has a system to follow) can out-perform most of the “professionals”.

AUSTRALIAN

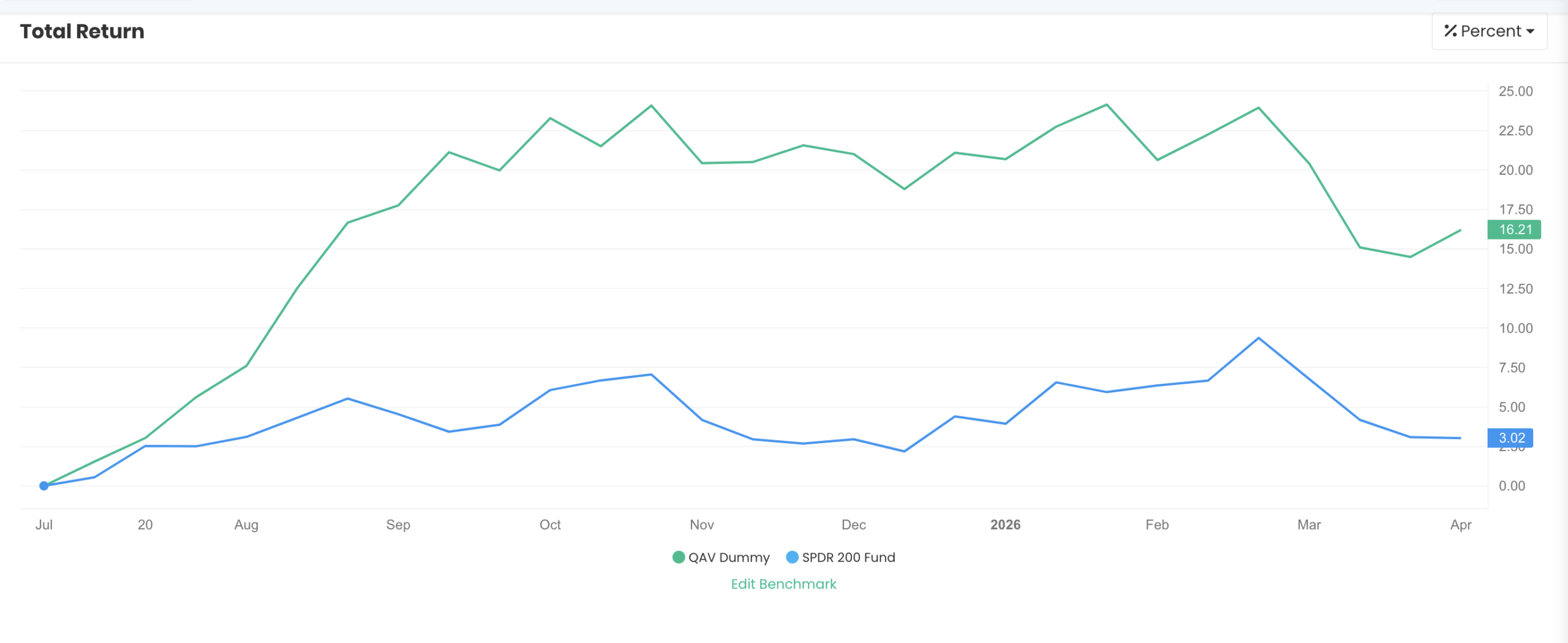

QAV DUMMY

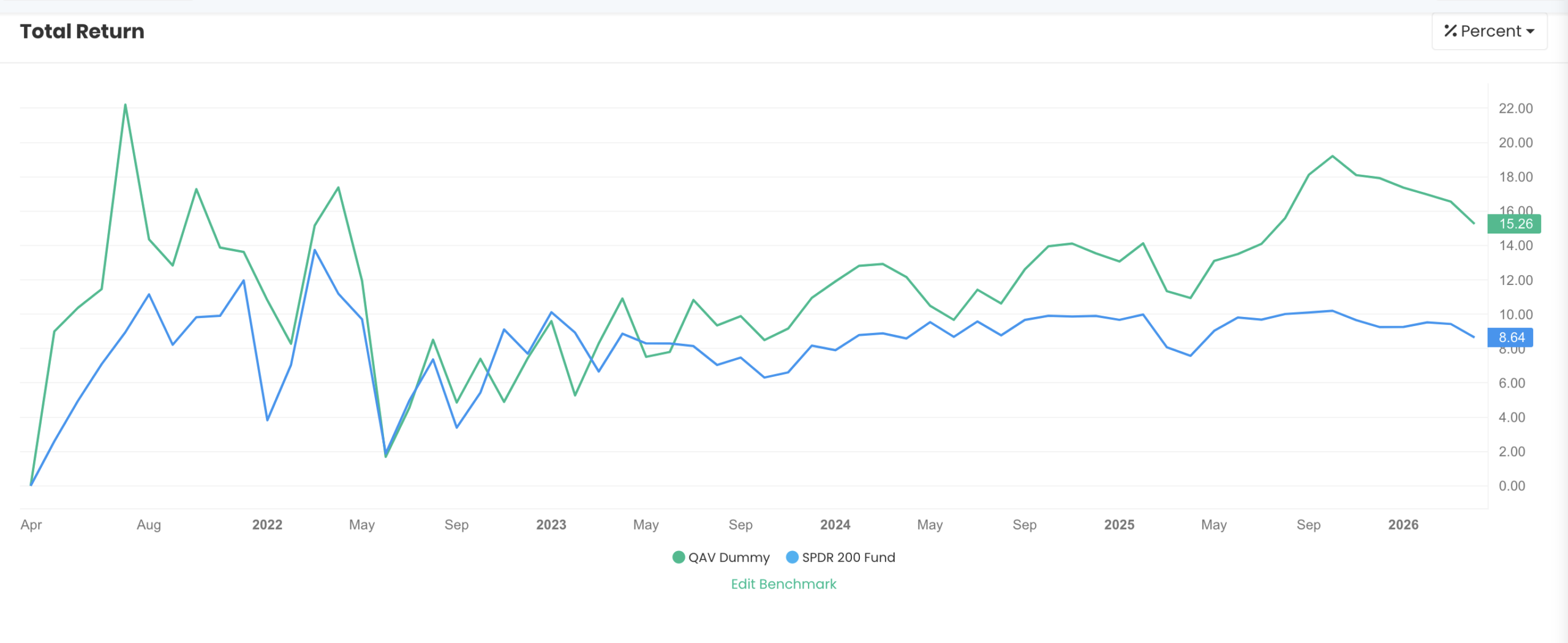

Five Year Report: QAV’s portfolio has delivered approximately 16% total returns over the period, significantly outperforming the ASX 200 benchmark which sits at around 9%, a meaningful 7 percentage point advantage over the broader market index.

Monthly Report: Over the past 30 days, the QAV portfolio declined approximately 3.96% while the ASX 200 benchmark fell around 3.78%.

No changes to our portfolio this week.

For FY26: The QAV portfolio is up approximately 16.2%, significantly outperforming the ASX 200 benchmark which is up around 3.0%. This represents an outperformance of roughly 13 percentage points and 5x market.

QAV LIGHT

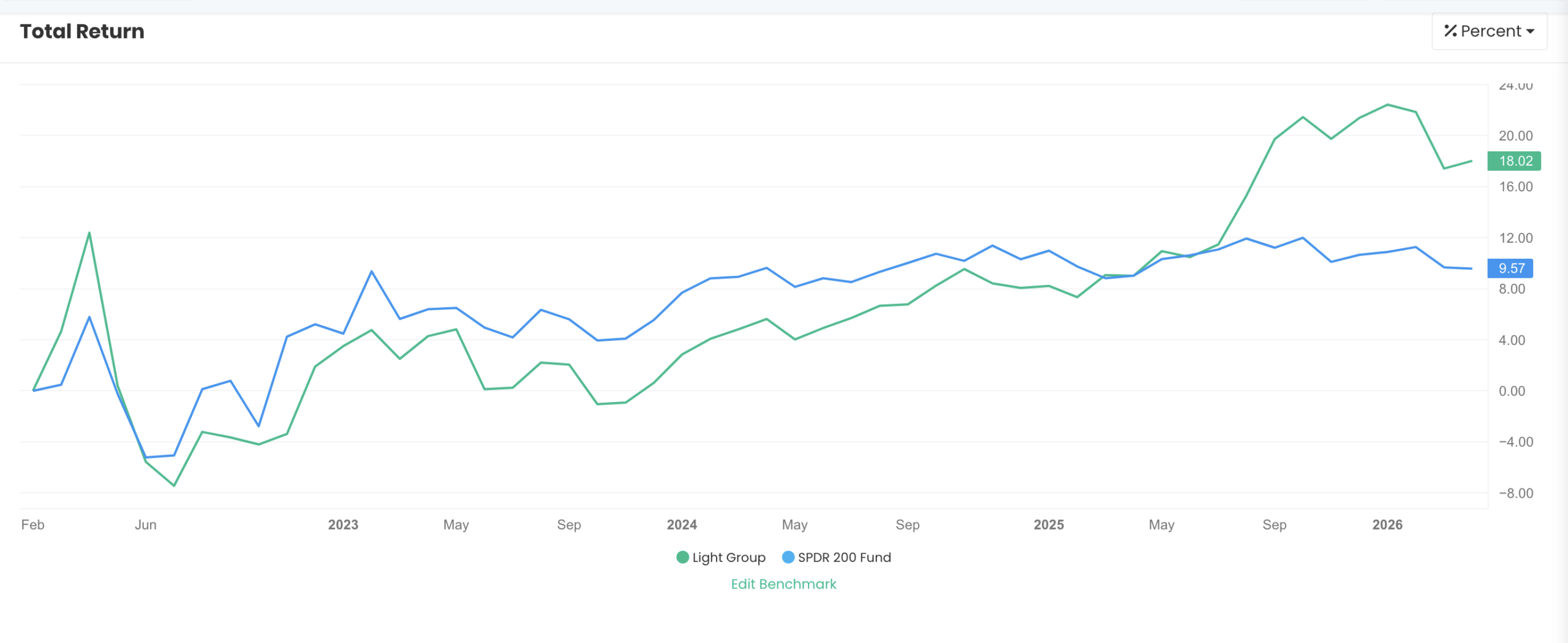

All Time

The QAV AU Light portfolio currently delivers an 18.02% total return compared to the ASX 200’s 9.57%, representing an outperformance of approximately 8.45 percentage points.

Financial Year to Date

The QAV AU Light portfolio has delivered a strong 22.99% return for the financial year to date, significantly outperforming the ASX 200 benchmark which returned 3.02%.

Last 30 Days

Over the past 30 days, the QAV AU Light portfolio delivered a return of approximately ‑3.2%, while the ASX 200 benchmark fell around ‑3.8%.

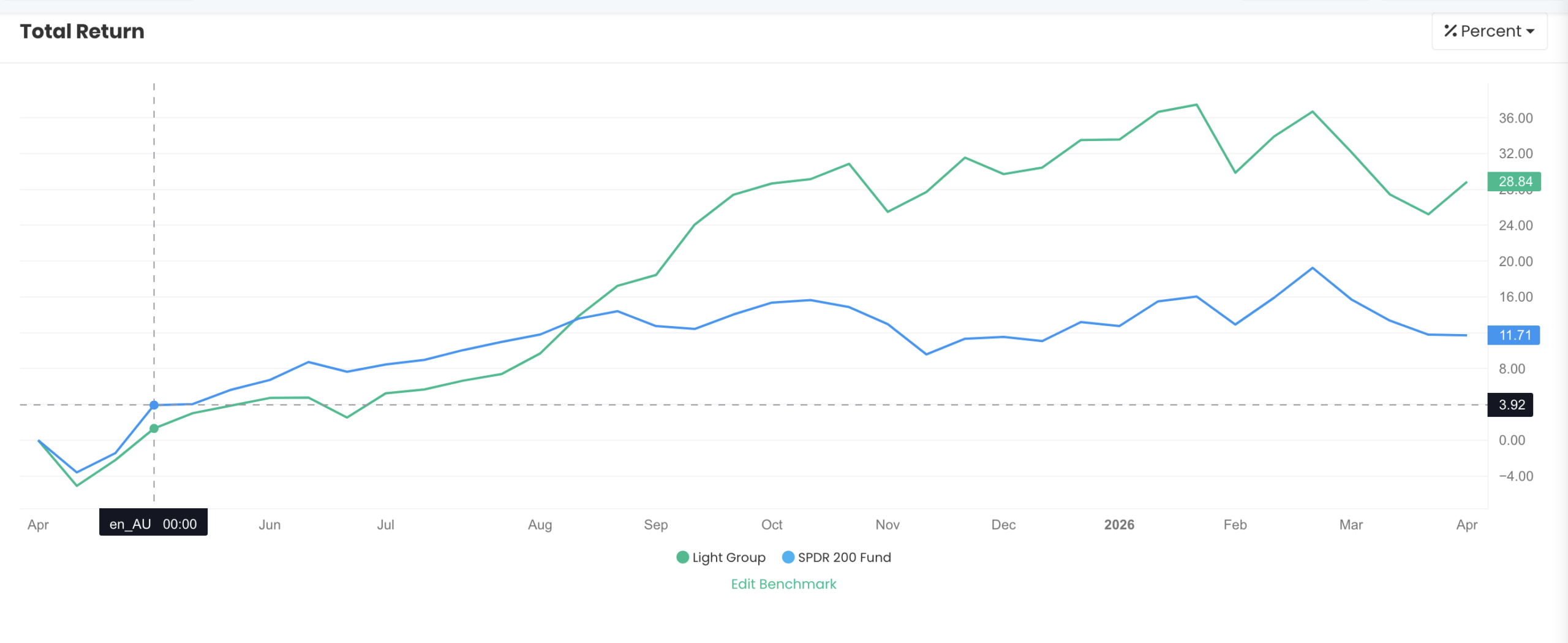

Last 12 Months

Over the past 12 months, the QAV AU Light portfolio delivered a total return of approximately 28.8%, significantly outperforming the ASX 200 benchmark which returned around 11.7%.

Become a QAV Light Member today and start your investing on the right track

If you want to find out what we’re trading in QAV Light each week, sign up to become a member. You’ll get an email from me every Monday letting you know what we’re buying and selling in that portfolio. You can choose to copy our trades or not. It’s the easiest way to start your rules-based investing career… and you don’t even need to know the rules. I’ll follow the rules for you. It’s a good first step to eventually becoming a QAV Club member and learning how to run the system by yourself.

(Note: Americans interested in joining QAV Light or Club please go here instead.)

AMERICAN

QAV DUMMY

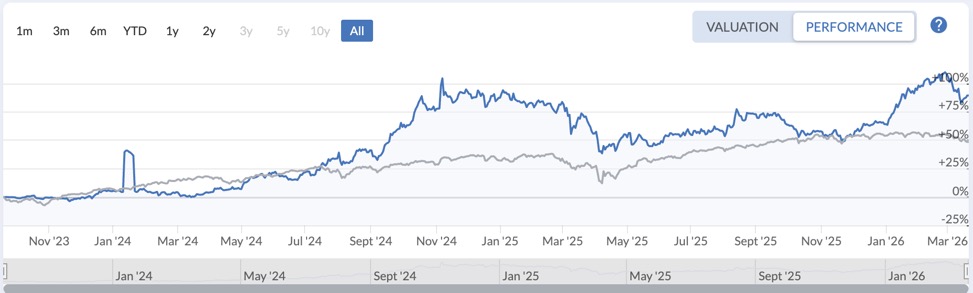

Since inception (Sep 2023), our portfolio is +94% vs the S&P 500 +48%. Not quite double market but pretty close.

Our U.S. portfolio for the last 30 days was ‑7% vs ‑4% for the S&P 500.

No trades this week.

QAV LIGHT

In December I started our U.S. Light portfolio, and it’s outperforming the index — it is currently +2% vs the S&P 500 ‑4%. It’s had a particularly good month, +5% vs the index ‑4%.

THIS WEEK’S EPISODES

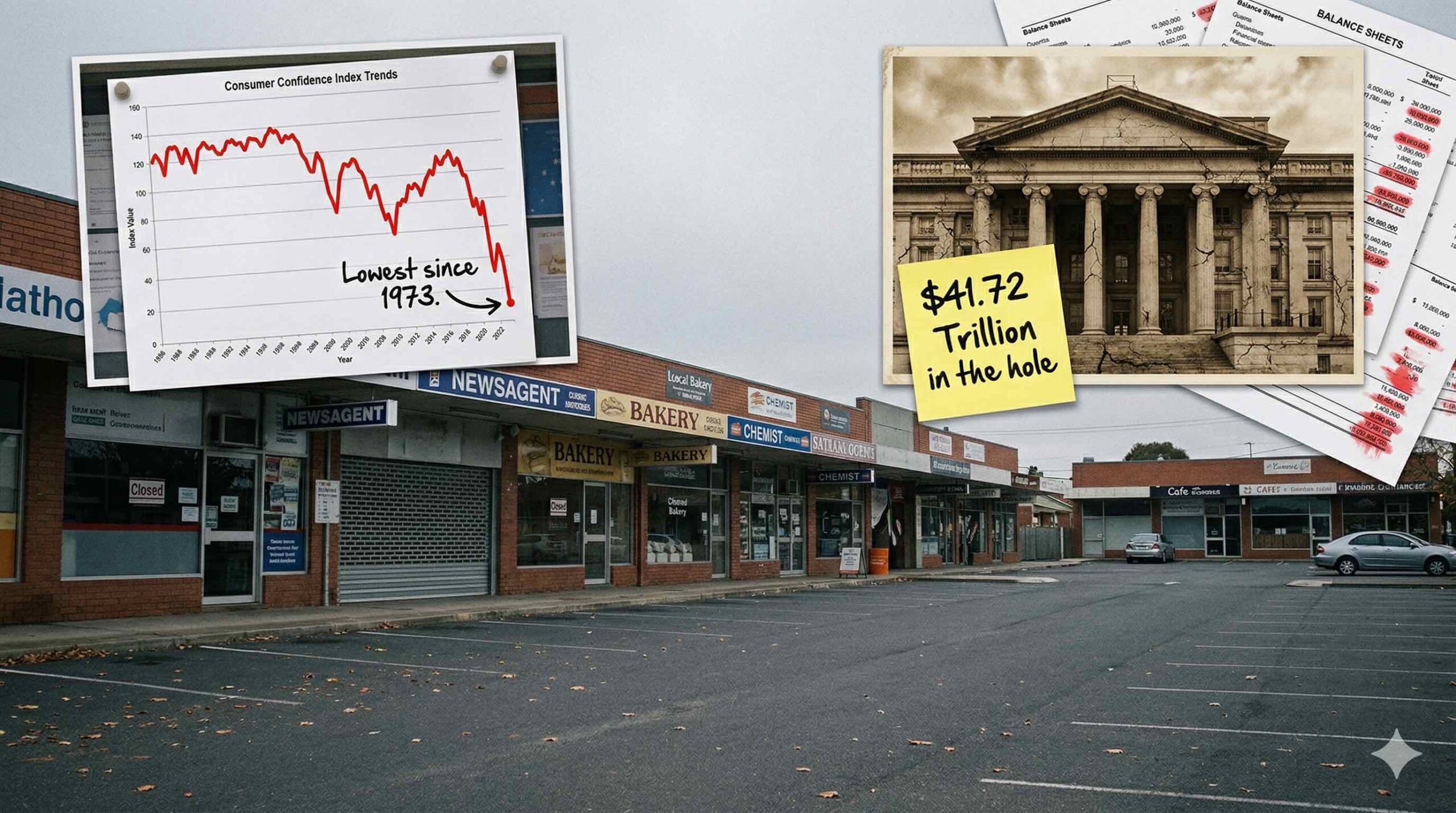

Drilling for Dollars: BRK, the Strait of Hormuz, and America’s $41 Trillion Hole — QAV AU 913

Profiting from Chaos – QAV America 46

STOCK NEWS AND UPDATES

COMMODITIES

No significant commodity status changes this week.

DISCLOSURE

Please review our trading and disclosure policy.

SIGNING OFF

Well, that’s another week of digging deep into the numbers and staying focused on what really matters — finding quality companies at sensible prices. While everyone else is chasing the latest shiny object, we’re building wealth the old-fashioned way — by building a portfolio of one undervalued quality company at a time.

I’m off to Bundy with the family for a week, so if I’m slow replying to emails or publishing buy lists or whatever, you know why. I’ll be doing kung fu on a beach, drinking Bundaberg Ginger Beer and chasing soldier crabs with Fox.

SSDD!

- Cam

That’s it for the week!

QAV A GOOD SHAREMARKET!

Got a question? [email protected]